THE 5 O'CLOCK PRINT

Daily Closing Bell Report. What happened today. What it means. How to prepare.

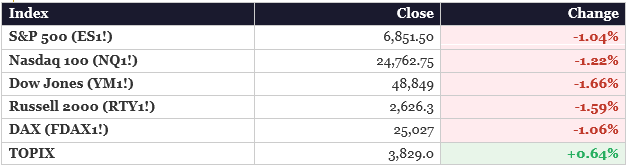

TODAY’S CLOSING PRINT

Markets sold off hard to start the week. The tape was red across the board — but as always, what’s underneath the surface matters more than the headline number. Today, what’s underneath is a breadth washout of historic proportions.

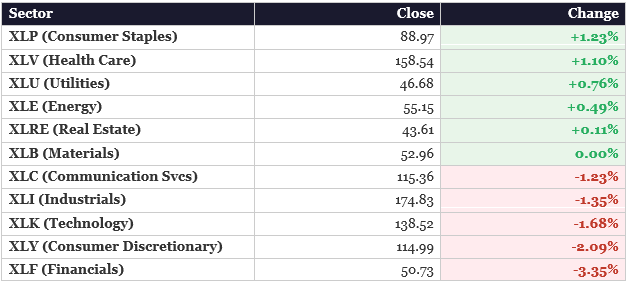

Biggest Dow losers: IBM -13.4%, American Express -7.3%, Salesforce -5.1%. Financials (XLF) were the worst sector at -3.35% while Consumer Staples (XLP) led at +1.23%. That’s a 458 basis point sector spread — extreme by any historical measure.

What Drove the Selloff

Two forces hit simultaneously:

1. Tariff regime chaos. The Supreme Court struck down Trump’s reciprocal tariffs Friday. By Monday morning, Trump responded by imposing a new 15% global tariff under Section 122 — a different legal mechanism entirely. Markets rallied Friday on the court ruling, then woke up Monday to more uncertainty. The European Parliament paused ratification of its US trade deal. India pushed back. The regime didn’t resolve — it just changed shape. The dollar closed nearly flat at 97.665, but commodity currencies (AUD -0.33%, NZD -0.29%) priced it as a global trade negative.

2. AI displacement fears. Software stocks were crushed. IBM dropped 13.4%. Cybersecurity (CIBR) fell 4.12%. Fintech (FINX) fell 4.07%. The catalyst? Anthropic’s new agentic coding tools. The market is repricing what AI disruption means for traditional software revenue. This is the SaaSpocalypse playing out in real time — and it’s broadening beyond SaaS into adjacent enterprise software categories.

Key tell: Walmart gained 2.3% while software bled. Consumer Staples and Health Care (+1.10%) led the session. Capital rotated into defensive names. SPLV was the only green factor on the day. The tape is telling the story.

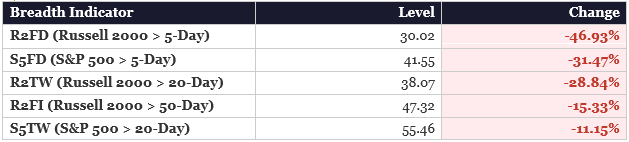

The Breadth Washout — What the Index Level Doesn’t Show

The S&P fell 1%. That sounds manageable. What happened underneath was not. Russell 2000 5-day breadth collapsed 46.93% to 30.02. S&P 500 5-day breadth fell 31.47% to 41.55. Russell 2000 50-day breadth dropped below 50% for the first time — meaning more small-cap stocks are in downtrends than uptrends. This is participation damage far worse than the headline number suggests.

When breadth collapses this fast, it typically precedes either a sharp snapback rally (if a catalyst arrives) or a multi-day continuation lower. Wednesday’s NVDA earnings are now the binary catalyst that determines which path the market takes.

THE SIGNAL IN THE NOISE — GOOGL, NVDA & THE HAVEN DIVERGENCE

Here’s what most people missed while they were watching the selloff: two of the most important names in the AI infrastructure trade got upgraded today. And the cross-asset haven map just drew its clearest line of the year.

Alphabet (GOOGL) — Upgraded to Overweight | Wells Fargo

Analyst Ken Gawrelski set a new price target of $387, up from $354 — implying over 22% upside from Friday’s close. GOOGL closed Monday at $311.69 (-1.02%), meaning the upside gap actually widened on the selloff.

The thesis rests on three pillars: Data (Google’s consumer data advantage is unmatched AI training fuel), Distribution (Search, YouTube, Android — the pipes are already built), and Compute (Wells Fargo’s internal model projects Google’s compute expanding from 15GW to 35GW by 2028). Google Cloud capacity rising from 7.6GW to 16.9GW by 2028, with operating income projections running 10-15% above Street estimates for 2026-2027.

Bottom line: While everyone focused on AI disrupting software, Google is quietly becoming the infrastructure layer that AI runs on.

NVIDIA (NVDA) — Overweight Reiterated & Upgraded

KeyCorp reiterated Overweight with a $275 target. Aletheia Capital upgraded to Buy from Hold — calling it ‘too cheap to ignore.’ NVDA closed at $191.55 (+0.91%), the strongest Mag 7 name on the day, gaining momentum into the close ahead of Wednesday’s earnings.

Wednesday consensus: $1.53 EPS (+71.9% YoY) on $65.7B revenue (+67% YoY). Morgan Stanley projects ~63% revenue growth. Goldman Sachs has a $250 target calling for a ‘beat and raise’ quarter. The upgrades going into earnings are a tell — smart money is not fading this print.

The Haven Divergence — Gold vs. Bitcoin

Gold gained $145 while Bitcoin lost $3,315 on the same day. This is the widest cross-asset haven divergence of 2026. The market is definitively pricing physical and sovereign havens over digital and speculative ones. The digital-gold narrative is dead for this cycle. The gold-silver ratio at ~60.4:1 confirms silver’s structural outperformance — and the precious metals bid has zero industrial spillover (copper -1.00%, platinum -1.08%). This is a pure monetary safe-haven trade.

The cross-asset read: When analysts upgrade NVDA and GOOGL on a red day, they’re telling you the AI infrastructure buildout thesis is intact. The rotation out of software doesn’t kill AI — it redirects capital toward the hardware and cloud layer. Meanwhile, gold and silver are catching the risk-off flow that used to go to crypto. The regime is the same. The expression is evolving.

THE MACRO BACKDROP

Rates & the Yield Curve

Regime: Bull Flattener. The 5-year yield led the decline at -6.3 basis points — the belly of the curve is pricing growth risk. The 2s10s spread closed at approximately 59.1 bps. Long bond futures (ZB1!) gained +0.51% into the close, confirming real money was adding duration, not just futures positioning.

The MOVE index (bond market volatility) flipped from -5.53% intraday to +5.86% at the close. That’s a massive intraday reversal — the rates market started the day calm about the tariff implications and grew increasingly uncertain as the EU, India, and other trade partners pushed back. Rates vol accelerating into the close alongside equity vol is the condition where the growth-inflation mix becomes genuinely uncertain.

What We’re Digesting From Last Week

Q4 2025 GDP came in significantly below expectations — growth is slowing. Core PCE (the Fed’s preferred inflation gauge) printed at 3.0% — hotter than expected. Initial jobless claims dropped 23K to 206K — labor market still holding. University of Michigan Consumer Sentiment barely moved, sitting 13% below year-ago levels.

The regime read: Slowing growth + sticky inflation = stagflation risk on the table. The Fed is caught. PCE above 3% makes cuts harder to justify, but slowing GDP puts pressure on them to act. This is why the yield curve and Fed speakers this week matter so much.

Volatility Regime

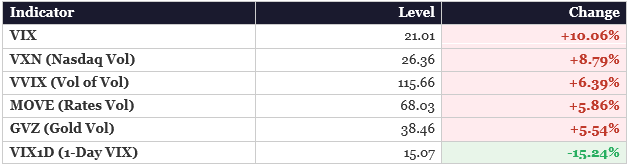

VIX1D at 15.07 (-15.24%) is the lone vol decliner — and it’s the most important signal in this table. The market’s fear is forward-dated (event-driven around NVDA earnings and Iran), not spot-driven. The 1-month implied correlation surged 23% — signaling a macro-driven selloff where idiosyncratic stock selection is being overwhelmed. SKEW fell 2.81% to 141.43, meaning the market is pricing an ordinary correction, not a crash.

Iran Geopolitical Risk

Trump stated he will decide within 10 days whether to launch military strikes against Iran. Crude oil rose ~2% on the tension last week, though WTI closed today at $66.31 (-0.26%). Heating oil was the energy standout at +3.57% on refining dynamics. This is a live tail risk — if military action occurs, energy markets will reprice rapidly. Defense positioning remains relevant.

WEEK AHEAD — KEY EVENTS TO WATCH

Plan the trade. Trade the plan. Here’s what’s on deck this week and why it matters for your positions.

Tuesday, February 24

CB Consumer Confidence (10:00 AM ET) — Consensus: 87.6, prior: 84.5. January confidence crashed 9.7 points to its lowest level since 2014. A bounce is expected, but

if the Expectations component comes in below 80, that’s a recession signal watch. Cross-asset watch: Weak confidence = dollar pressure = potential EM and metals bid. Strong confidence = reflation narrative = watch XLF and cyclicals.

Fed Speaker: Governor Waller. He’s been one of the more data-dependent voices on the FOMC. Watch for any commentary on the PCE print and March meeting positioning.

⭐ Wednesday, February 25 — BIGGEST DAY OF THE WEEK

NVIDIA Earnings After Close — Consensus: $1.53 EPS | $65.7B Revenue. This is the market event of the week. The breadth washout and binary Mag 7 divergence (NVDA +0.91% while software dropped 4%) means NVDA’s report carries the weight of the entire equity complex. A beat-and-raise with strong Blackwell guidance would likely trigger a violent short-covering rally in the beaten-down software and thematic ETFs (CIBR, FINX, ARKW). A miss or weak guidance could send VIX above 25 and extend the breadth washout to levels not seen since the April 2025 tariff shock.

Salesforce (CRM) also reports Wednesday. The software sector is already in a SaaSpocalypse from AI disruption fears. If CRM shows cracks, software bleeds further. A surprise could spark a relief rally.

Cross-asset chain: NVDA beat → AI capex intact → copper and power infrastructure bid → defense and grid buildout confirmed. This is The Chain playing out live.

Thursday, February 26

US Initial Jobless Claims — Consensus: 216K (prior: 206K). Any reading above 225K gets attention and could signal labor market deterioration. Fed Speakers: Bowman and Barkin — both provide calibration before the March FOMC. Listen for ‘patience’ vs. ‘flexibility’ — that’s the tell on whether cuts are coming.

⭐ Friday, February 27 — DATA ANCHOR

US PPI (Producer Price Index). PPI tells you where CPI is going. After last week’s hot PCE at 3.0%, a hot PPI confirms the sticky inflation narrative and pressures the Fed to stay on hold. A cool PPI gives the Fed breathing room.

Canada GDP tells you about the North American growth story and has implications for CAD, oil, and commodity exposure. Eurozone Final CPI (consensus: 1.7% headline, 2.2% core) — if confirmed, the ECB easing path stays intact and EUR weakness remains a viable macro expression.

Weekend Watch

China PMI (Sunday) — Prior: 49.3, below the 50 expansion/contraction line. A reading staying below 50 is a headwind for commodity currencies and EM. A surprise above 50 could be a catalyst for commodity FX strength — BRL, CLP, ZAR, AUD all have sensitivity here.

THE MACRO READ — CONNECTING THE DOTS

Here’s how everything above connects to the bigger picture. This is where the regime thinking matters.

The tariff regime is not resolved — it just changed form. Section 122 tariffs (15% global) replace the struck-down reciprocal tariffs. The dollar is flat at 97.665 but commodity currencies are pricing global trade damage. EUR, JPY, and CHF are catching a haven bid. Our DXY thesis isn’t over.

The AI rotation is happening in real time. Capital is not leaving AI — it’s moving from software to infrastructure. GOOGL and NVDA being upgraded on a red day while IBM loses 13% and cybersecurity/fintech drop 4% is the clearest possible signal of where institutional money is going. NVDA closed as the best Mag 7 name at +0.91% while MSFT (-3.21%) and META (-2.81%) bled.

Stagflation risk is rising. Slowing GDP + PCE at 3.0% + Fed on hold = the environment where metals, real assets, and defense tend to outperform. Gold at $5,225 and silver at $86.57 are confirming this thesis. The bull flattener in rates (5Y leading at -6.3 bps) is the bond market telling you it’s worried about growth more than inflation.

The breadth washout changes the setup. When Russell 2000 5-day breadth drops 47% in a single session and falls to 30, you’re looking at participation damage that the index level doesn’t reflect. The market has sold everything except NVDA and AAPL. Wednesday’s earnings are now maximally binary — this is the catalyst that either reverses the washout or extends it.

Iran geopolitical risk is not priced. Crude barely moved today despite Trump’s 10-day decision window. If this escalates, energy and defense get a significant bid. Position accordingly — not with panic, with awareness.

SECTOR & FACTOR SCORECARD

WHAT TO WATCH THIS WEEK

▸ NVDA earnings Wednesday — the AI infrastructure verdict and the binary catalyst for the breadth washout

▸ CB Consumer Confidence Tuesday — recession signal watch below 80 on expectations

▸ PPI Friday — confirms or contradicts the sticky inflation narrative post-PCE

▸ Fed speakers throughout — Waller (Tue), Goolsbee, Bowman (Thu) — March FOMC calibration

▸ Iran developments — tail risk that could move crude and defense sharply within 10 days

▸ China PMI Sunday — EM and commodity FX directional signal

▸ Software sector — is the SaaSpocalypse a rotation or a collapse? Salesforce Wednesday will help answer that

▸ 2s10s spread — if the bull flattener accelerates below 55 bps, the bond market is pricing a more severe growth shock than equities reflect

▸ MOVE index — if rates vol continues climbing alongside equity vol, no asset class is safe except physical gold

CLOSING THOUGHT

The market sold off today. That’s the headline. But underneath, the breadth washout tells a bigger story — Russell 2000 5-day breadth collapsed 47%, S&P 5-day breadth dropped 31%, and the participation damage is far worse than the index level suggests. Meanwhile, Google got upgraded with 22% upside. NVIDIA gets called ‘too cheap to ignore’ days before earnings and closed as the strongest Mag 7 name. Gold surged to $5,225 while Bitcoin crashed 5%. Walmart gained while IBM collapsed. This isn’t a market in fear — it’s a market in rotation, with a breadth washout that’s forcing a decision. The question isn’t whether to be in. It’s where. The regime is the same. The expression is evolving. Stay focused, stay positioned, and come back Wednesday night — NVDA is going to tell us a lot about where this goes next.

See you at The 5 O’Clock Print.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.