THE 5 O'CLOCK PRINT

What happened today. What it means. How to prepare.

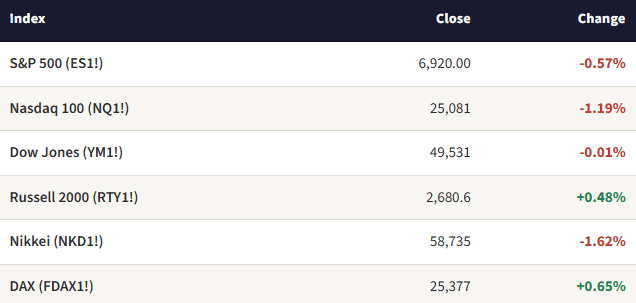

TODAY’S CLOSING PRINT

The index fell. Everything underneath it got healthier. That’s today’s paradox — and it’s the most constructive signal since the tariff shock. NVIDIA crashed 5.46% after beating on every metric. The Nasdaq dropped 1.19%. But all twenty breadth readings improved. Every single one. The market didn’t break. It rotated. And what it rotated into tells you exactly where this goes next.

Russell 2000 outperformed Nasdaq by 167 basis points. That’s the widest NQ-RTY divergence since the tariff shock. The Dow was flat. The DAX rallied. Small caps gained. The only thing that fell was large-cap tech — and that’s exactly the correction this market needed. Yesterday we warned the rally was too narrow, too dependent on Mag 7. Today the market fixed it.

What Drove the Session

1. NVIDIA’s “sell the news” crash was the catalyst. Despite beating on every metric — $1.62 EPS, $68.13B revenue, $78B Q1 guide, data center +75% YoY — NVDA fell 5.46% to $184.89 on 351 million shares (2x average volume). The stock had rallied from $192.85 Monday to $195.56 yesterday, pricing in the beat. Today it gave back the entire post-tariff recovery and more. This is the largest single-day Mag 7 post-earnings reversal in recent memory. AMD fell 3.41%, Intel -3.03%, SOXX -3.04%. The semiconductor selloff cascaded across the entire chip complex.

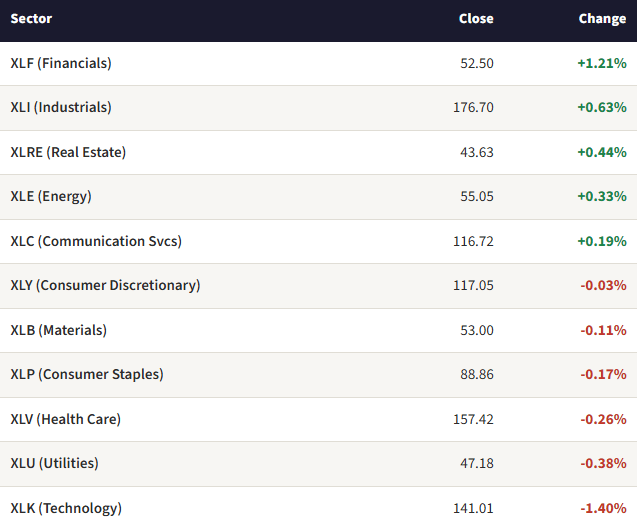

2. The rotation was immediate and violent. Capital didn’t leave the market — it moved within it. Financials surged +1.21%. Industrials bounced +0.63% after yesterday’s -0.78%. Real estate gained +0.44% as yields plunged. Genomics exploded +4.51%. Software stocks rallied broadly, with the iShares Tech-Software ETF (IGV) up 2.2%. The market sold the crowded trade and bought everything else.

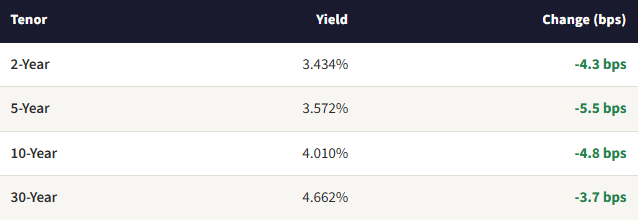

3. The bond market confirmed the regime shift. The entire yield curve rallied — 5-year down 5.5 bps, 10-year down 4.8 bps, 2-year down 4.3 bps. The 5-year’s move was the largest single-day decline since the tariff shock. Yesterday’s parallel bear shift (yields rising) has been completely replaced by a bull steepener (yields falling, front end leading). The 30-year mortgage broke below 6.00% for the first time.

4. Iran talks produced “progress” but no deal. The third round of US-Iran nuclear talks in Geneva lasted six hours. Both sides called the discussions “positive” and “serious,” with technical talks to continue in Vienna Monday. No framework announced. The USS Gerald R. Ford departed Crete for the Middle East during the talks. Energy markets barely moved — crude flat, but heating oil crashed 5.54% for its second straight day of massive declines.

Key tell: Equal-weight S&P (RSP) outperformed the cap-weighted S&P by 113 basis points. The average stock is rallying while the index falls. That’s not a selloff. That’s a redistribution.

THE SIGNAL IN THE NOISE — THE GREAT ROTATION

Here’s what today actually was: the market’s self-correcting mechanism operating at peak efficiency. Monday through Wednesday, the post-tariff rally concentrated in fewer and fewer names. Today, the market broke the concentration and redistributed the gains. This is the healthiest possible version of a down day.

The Breadth Paradox

S&P 500: -0.57%. S&P breadth readings: all ten improved. That sentence shouldn’t be possible. But it is, because NVDA alone contributed roughly 40 points of drag on the S&P, while hundreds of smaller constituents rallied. S&P 5-day breadth surged +14.82% to 63.22. S&P 20-day breadth jumped +12.31% to 63.41. S&P 200-day breadth rose +3.78% to 65.40 — reversing the negative divergence we flagged yesterday. Russell 2000 20-day breadth broke above 50 to 51.79 for the first time since the tariff shock.

All twenty breadth readings improved on a down day for the index. This has not occurred since before the tariff event. The tariff breadth damage has been fully repaired across all timeframes for both indices.

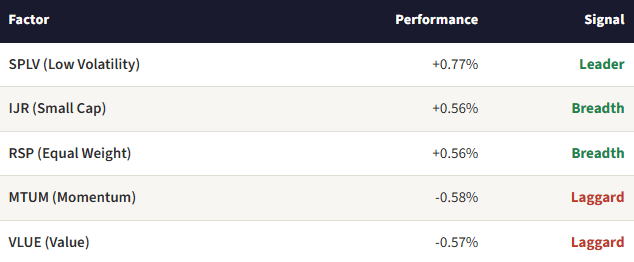

The Factor Inversion

SPLV-to-MTUM swing: 320 basis points in one session. Low volatility went from the worst factor for four straight days to today’s best. Momentum went from yesterday’s best to today’s worst. This is a textbook momentum crash — the market’s recent winners (NVDA, tech, Mag 7) sold off aggressively while recent losers (low vol, defensives, small caps) were bought. It’s the factor equivalent of the sector inversion.

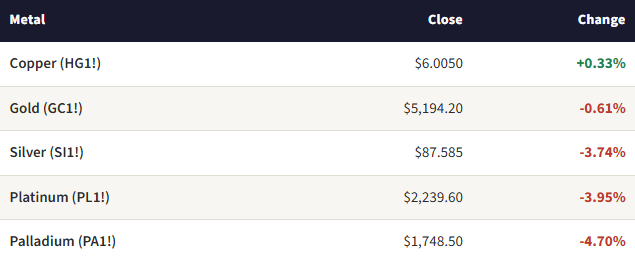

The Precious Metals Reversal

Yesterday’s reflationary boom thesis is dead. Platinum gave back $92 of its historic $144 gain — a 64% retracement in one session. Palladium dropped $86. Silver fell from $91 back to $87.58. The broad precious metals inflation-hedging trade that defined yesterday has been violently unwound. But copper held above $6.00 — the sole green metal for the second straight day. The copper-precious metals divergence is now at its widest in the post-tariff period. Copper says industrial demand is intact. Precious metals say the inflation scare is over. Combined signal: disinflation with growth.

THE MACRO BACKDROP

Rates — Bull Steepener

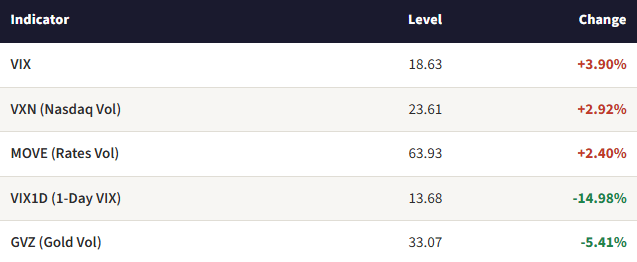

The yield curve has told a different story every day this week. Monday: bull flattener (growth scare). Tuesday: bear steepener (inflation repricing). Wednesday: parallel bear shift (reflationary boom). Thursday: bull steepener (disinflation with rate cuts pricing back in). Four different curve regimes in four days. Today’s 5-year decline of 5.5 bps is the largest single-day drop since the tariff shock. The 10-year is testing 4.00%.

The bond market is pricing three things simultaneously: the energy collapse as disinflationary (heating oil -5.54%, two-day decline ~12%), the NVDA-led tech selloff as dampening animal spirits, and increased probability of a Fed cut in the medium term. MOVE rose 2.40% to 63.93 — the first increase in five sessions, meaning this is not a calm move but a genuine repricing event.

30-year mortgage: 5.98%. Below 6.00% for the first time. That’s the most tangible consumer-level consequence of the yield decline. XLRE (+0.44%) responded immediately.

Initial Claims — Non-Event

212K initial claims, in line with expectations. Continuing claims fell 31K to 1.83M. The labor market is stable and provided no catalyst in either direction. The market’s attention was entirely on NVDA and the rotation.

Iran Talks — “Progress” Without Framework

Six hours of indirect talks in Geneva. Iran’s FM Araghchi called the discussions “serious” and said they entered “a review of the elements of an agreement.” Technical talks scheduled for Vienna Monday. US officials described the session as “positive.” But the mediator acknowledged both sides need to consult their governments. Meanwhile, the USS Gerald R. Ford departed Crete for the Middle East and VP Vance said a drawn-out war is unlikely. The market read: talks are alive but not producing enough to remove the geopolitical premium. Crude was essentially flat.

Volatility — The Divergence

VIX up, VIX1D down. This is a rare and analytically rich divergence. Multi-day VIX is rising (+3.90%) because the NVDA crash and mega-cap rotation introduce medium-term uncertainty. But VIX1D plunged 14.98% because intraday realized volatility was low and short-term event risk (NVDA earnings) has been resolved. Translation: the market sees continued rotation risk over the next few weeks, but tomorrow specifically should be calm. MOVE rising 2.40% after four straight declines means rates volatility is reawakening.

Correlation — Re-Correlation on Rotation

1-month implied correlation surged 28.33% to 13.77. After two days of double-digit declines, correlation spiked sharply. But this isn’t the dangerous kind. During the tariff panic, correlation spiked because everything was selling together. Today, correlation rose because broad swaths of the market are moving in the same direction (up) while a concentrated group (mega-cap tech) moves the other way. Rotation-driven correlation, not panic-driven correlation.

THE MACRO READ — CONNECTING THE DOTS

Here’s the regime change in one sentence: the reflationary boom lasted exactly one day. What replaced it is better for more of the market.

The regime has shifted from “reflationary boom” to “broadening with disinflation.” Yesterday: equities up, metals up, yields up, dollar down. Today: mega-cap tech down, broad market up, yields down, precious metals crushed, copper holds. The reflationary thesis — growth and inflation both rising — lasted exactly one session. It’s been replaced by something more sustainable: growth rotating and broadening while inflation expectations moderate.

The yield curve told a different story every day this week — and that IS the story. Bull flattener → bear steepener → parallel bear shift → bull steepener. Four regimes in four days. The market is working in real time to discover the right price for the tariff, the right price for AI, and the right price for inflation. Today’s bull steepener (5-year -5.5 bps leading) is the bond market saying: the inflation scare from the tariff is fading, the energy collapse is disinflationary, and Fed cuts are back on the table.

NVDA’s crash doesn’t kill the AI thesis. It redistributes the gains. $1.62 EPS on $68B revenue with $78B Q1 guidance is not a weak report. The stock sold off because it had priced in the beat, because sequential data center growth is decelerating (22% Q4 vs 25% Q3, guided ~15% Q1), and because the market decided the concentration was unsustainable. But where did the capital go? Genomics (+4.51%). Cybersecurity (+1.85%). Fintech (+1.94%). Software (IGV +2.2%). The AI disruption trade is alive — it’s just spreading from hardware to the applications built on top of it.

The breadth explosion is the single most important signal since the tariff shock. All twenty readings improving on a down day means the market’s foundation is getting stronger even as the mega-cap superstructure cracks. RSP outperforming ES by 113 bps means the average stock is rallying. R2TW breaking 50 means small-cap 20-day breadth is now majority-positive for the first time. This is the market’s self-correcting mechanism working at peak efficiency.

Copper above $6 while precious metals crash is the clearest regime signal. Industrial demand intact. Inflation hedging unwinding. Combined with the bull steepener and falling energy prices, the macro regime is: growth yes, inflation no. That’s the best possible backdrop for financials, rate-sensitive sectors, and the broad market. Just not for the names that led the last four days.

SECTOR SCORECARD

XLK-to-XLF spread: -261 basis points. That’s a complete leadership inversion from yesterday’s +17 bps and the widest single-day sector divergence in the post-tariff period. Financials benefiting from the bull steepener. Industrials rebounding after yesterday’s -0.78%. Real estate catching a bid from plunging yields. Energy finding a floor. This is cyclical/financial leadership replacing tech leadership — the classic rotation from late-cycle momentum into mid-cycle value.

WHAT TO WATCH

PPI tomorrow morning — THE data event of the week. Hot PPI would reignite the inflation narrative the metals just abandoned. Cool PPI confirms the disinflation thesis and gives the Fed breathing room

MSFT after-hours -1.70% — if it holds, the mega-cap selling spreads beyond NVDA into the broader tech complex. Watch the open carefully

NVDA at $184.89 — well below the pre-tariff level of ~$192.85. The earnings beat was not rewarded. Support at $180.99 from accumulated volume

Iran technical talks in Vienna Monday — no deal but “progress”; USS Gerald R. Ford heading to Middle East. Geopolitical premium still in play

10-year yield testing 4.00% — a close below 4.00% would be the first since before the tariff shock

30-year mortgage at 5.98% — below 6.00% for the first time. Watch housing-related names and XLRE for continuation

Copper at $6.005 — sole green metal for second straight day. If it holds $6, the pro-cyclical signal is structurally intact

Heating oil two-day decline ~12% — the most important disinflationary signal in the commodity complex. Overshooting?

R2TW at 51.79 — just broke above 50. Confirmation above 52 tomorrow would be significant

China PMI Sunday — the weekend risk. Above 50 supports the broadening thesis; below 50 tests it

CLOSING THOUGHT

Today was the day the market fixed itself. For four days, the post-tariff recovery concentrated into fewer and fewer names — NVDA, MSFT, META, momentum, tech — while breadth eroded underneath. We flagged the fragility every night. Today, NVIDIA delivered a perfect earnings report and crashed 5.46%, and the market’s response was the healthiest possible outcome: it didn’t panic, it rotated. Capital flowed out of the crowded mega-cap trade and into financials, industrials, real estate, small caps, genomics, cybersecurity, and software. All twenty breadth readings improved on a down day. The equal-weight S&P outperformed the cap-weighted by 113 basis points. The 30-year mortgage broke below 6%. The yield curve shifted to a bull steepener with the 5-year down 5.5 bps. The reflationary boom lasted one day. What replaced it — broadening with disinflation — is a fundamentally more sustainable regime. It doesn’t need NVIDIA to go up every day. It doesn’t need all five metals surging. It needs the average stock to participate, and today that’s exactly what happened. PPI tomorrow morning is the next test. If the data confirms what the bonds and metals are already pricing, the broadening has room to run. If not, the market will have to discover another regime. Five in one week. The tape never stops talking. Listen to it.

See you at The 5 O’Clock Print.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.