THE 5 O'CLOCK PRINT

What happened today. What it means. How to prepare.

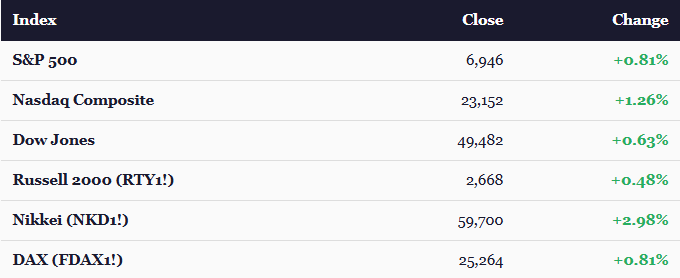

TODAY’S CLOSING PRINT

This is no longer a bounce. This is a regime change. Day three of the post-tariff recovery delivered the clearest cross-asset signal of 2026: equities up, all five metals up, yields up across the entire curve, dollar down, Bitcoin surging nearly 8%. The market has evolved from “post-selloff recovery” to something the data forces us to call what it is — a reflationary boom. And then NVDA confirmed it after the bell.

The leadership rotation tells the story. Yesterday, Russell 2000 led at +1.09%. Today, Nasdaq led at +1.26% while the Russell decelerated to +0.48%. The torch has passed from small-cap short-covering to large-cap tech-driven risk appetite. That’s a higher-conviction, more sustainable rally driver — and it’s exactly the setup the tape needed heading into NVDA’s after-hours report.

The Nikkei is the global standout for the third consecutive session, surging 2.98% to 59,700 — now up nearly 3,000 points in three days. Japan is telling you the global growth impulse is real.

What Drove the Session

1. NVDA earnings positioning dominated everything. The market spent all day accumulating ahead of tonight’s report. NVDA rallied 1.41% into the close, rising from yesterday’s weakest Mag 7 gainer (+0.68%) to the middle of the pack. Tech (XLK +1.92%) seized leadership from Consumer Discretionary. Semiconductors (SOXX +1.65%) confirmed the sector bid. The options market had priced ~8% implied move — the tape was constructive but hedged.

2. Trump’s State of the Union set the overnight tone. The record-longest SOTU in history spent a full hour on affordability. The key market-moving announcement: the “Rate Payer Protection Pledge” — Trump announced that tech companies have agreed to cover their own power costs for AI data centers, directly addressing the voter backlash over rising electricity bills. He also pushed for congressional stock trading bans (bipartisan cheers), codifying drug price reductions through “most favored nation” pricing, and tax cuts through reconciliation including no tax on tips, overtime, or Social Security. On tariffs, he was defiant: these “powerful, country-saving tariffs will remain in place” and he believes they will eventually “substantially replace the modern-day system of income tax.” Futures were stable after the speech — no new tariff escalation, no Iran military action announced. The market got what it wanted: no surprises.

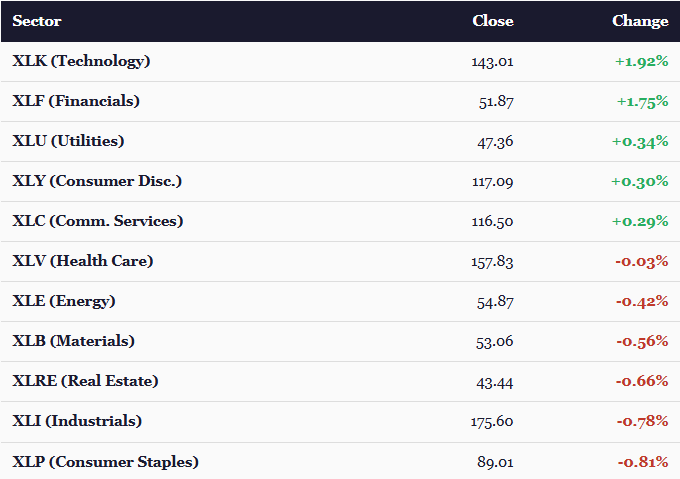

3. The rally narrowed dangerously. Only 5 of 11 sectors were green today, down from 9 yesterday. The S&P 500 gained 0.81% while its 200-day breadth declined 0.93%. Consumer Staples (-0.81%), Industrials (-0.78%), Real Estate (-0.66%), and Materials (-0.56%) all sold off. The index is being carried by Technology (+1.92%) and Financials (+1.75%) — two sectors, not eleven.

Key tell: When the S&P 500 rallies 0.81% and only 5 of 11 sectors are green, the index is being carried by a few large names. When 200-day breadth simultaneously declines, that’s a classic negative divergence. The rally is real. The breadth is a yellow flag.

THE SIGNAL IN THE NOISE — THE PRECIOUS METALS EXPLOSION & NVDA’S VERDICT

Two things happened today that reshape the macro framework. First, the clean gold-to-copper rotation from yesterday broke down — now everything is rallying. Second, NVDA delivered the beat-and-raise that removes the biggest binary risk of the week. Both demand a careful read.

The Precious Metals Explosion

This is the most important table in today’s report. Yesterday we flagged the gold-to-copper rotation as the clearest regime signal — gold falling, copper surging, industrial replacing monetary metals. That rotation has broken. Today, all five metals rallied simultaneously. Platinum exploded 6.60%. Silver surged 3.98% to $90.99, approaching the psychologically significant $91 level. Gold reclaimed $5,226 after yesterday’s selloff. And copper held its multi-week highs at $5.99.

This is no longer a clean pro-cyclical rotation. The market is layering inflation hedging on top of the growth bid. When all hard assets are surging — industrial and monetary metals together — while yields rise across the entire curve and the dollar weakens, you are in a reflationary regime. Growth expectations up. Inflation expectations up. Rates up. Stocks up. Hard assets up. That’s the textbook definition.

Gold’s GVZ volatility fell 6.90% even as gold rallied — meaning the move is orderly and expected, not a panic bid. This is systematic inflation hedging, not fear. That distinction matters enormously for positioning.

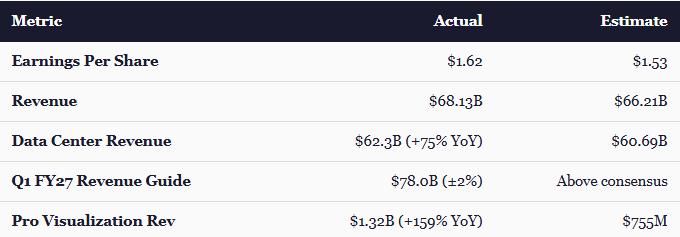

NVDA — The Beat-and-Raise

After the bell, NVDA delivered:

Beat on every metric. Revenue up 73% year-over-year. Data center now over 91% of total sales. Hyperscalers remained the largest customer category at just over 50% of data center revenue. And the Q1 guide of $78 billion blew away expectations.

The after-hours reaction was telling: NVDA traded to ~$196, up about 3.5% — a measured move, not an explosion. The beat was largely priced into today’s +1.41% cash session rally. That’s actually constructive: the market was correctly positioned, reducing the risk of a gap-down that the narrow leadership base would have struggled to absorb.

The cross-asset chain: NVDA beat → AI capex validated → hyperscaler spending at $700B combined capex this year → copper, power infrastructure, grid buildout all bid → AMD-Meta $100B deal from Monday confirmed as expansion of TAM, not competitive zero-sum. The AI hardware buildout thesis just got its biggest validation since Meta’s capex guidance.

Salesforce — The SaaSpocalypse Test

Salesforce also reported after the close: $3.81 EPS (vs. $3.04 est.), $11.20B revenue (vs. $11.18B est.) — the fastest revenue growth rate in two years at 12% YoY. Agentforce closed 22,000 deals in Q4, ARR for Agentforce and Data Cloud hit $1.8B. But the stock fell ~5% after hours on lukewarm FY27 guidance of $45.8-46.2B (consensus was $46.06B). Benioff announced a $50B buyback — “because these are some low prices” — after CRM has fallen 28% in 2026. The SaaSpocalypse continues: even a beat can’t save you if the forward guide doesn’t accelerate.

THE MACRO BACKDROP

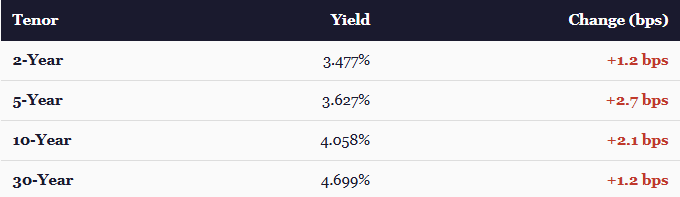

Rates — Parallel Bear Shift Replaces Bear Steepener

The yield curve regime evolved again. Yesterday was a bear steepener — the 2-year led higher while the 30-year caught a bid from duration buyers pricing a one-time tariff adjustment. Today, those duration buyers stepped back. The entire curve is selling off, with the 5-year belly leading at +2.7 bps. This is a parallel bear shift — the market is no longer pricing tariff as a one-time price-level adjustment but as a persistent inflationary impulse that weighs on the entire curve.

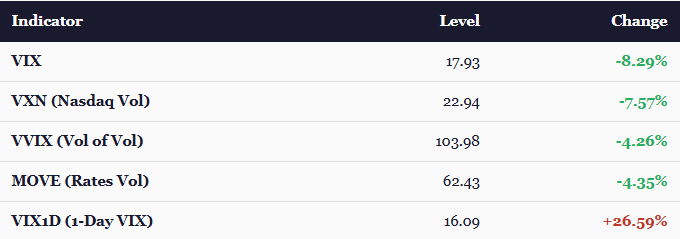

The 2s10s spread widened slightly to ~58.1 bps. MOVE fell another 4.35% to 62.43 — third consecutive day of rates volatility de-escalation. The curve move is orderly, not panicky. But the 30-year mortgage is still at 6.01% — if the parallel bear shift continues, mortgage rates will start drifting higher in the next weekly print.

FX — Dollar Weakness Confirms the Regime

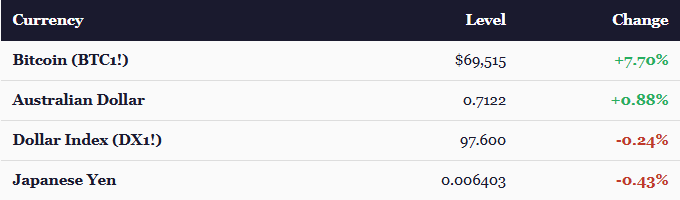

Bitcoin is the day’s single most explosive asset at +7.70% to $69,515. It has recovered virtually the entire tariff-induced drawdown from $67,825 pre-SCOTUS. The capitulation low of $62,970 on Monday morning is now definitively confirmed. A $6,545 recovery (+10.4%) in 36 hours.

The dollar weakened 0.24%, reversing yesterday’s strength. Equities up, metals up, dollar down — textbook reflationary correlation. Commodity currencies surged: AUD +0.88%, NZD +0.47%. If DX1! breaks below 97, it opens the door to further depreciation that would amplify the commodity and precious metals rally.

Volatility — VIX Below 18, But Watch VIX1D

VIX crashed below 18 for the first time since the tariff shock. This is approaching calm-market territory. VVIX below 104 means tail hedging demand has completely evaporated. But VIX1D surged 26.59% to 16.09 — the only volatility measure that rose today. This intraday vol spike reflected the NVDA event risk concentrated in the final hours. With the beat-and-raise now delivered, this anomaly resolves constructively.

Correlation Collapse — The Stock-Picker’s Market Intensifies

COR1M crashed another 25.90% to 10.73. That’s the second consecutive day of double-digit correlation collapse, following yesterday’s -15.57%. At 10.73, 1-month implied correlation is at extreme lows — stocks are moving almost entirely independently. COR3M (-14.76% to 12.76) and COR6M (-8.67% to 15.49) confirm the de-correlation is cascading across the term structure. SKEW is flat at 141.94 — the market is not bidding tail risk protection. The macro-driven “sell everything” regime from Monday is a distant memory.

BREADTH — THE BIFURCATION

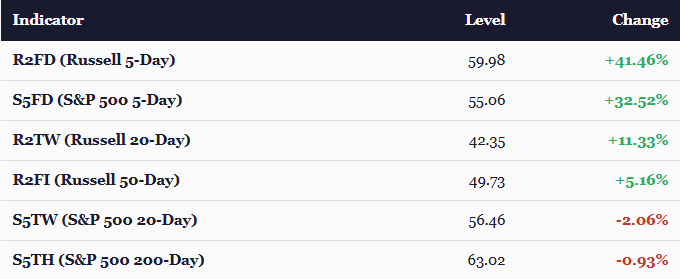

The breadth story has bifurcated. Short-term breadth has violently repaired: R2FD surged from 30.04 on Monday to 59.98 today — a 30-point two-day recovery that confirms the short-term washout is completely healed. S5FD jumped from 41.55 to 55.06.

But longer-term S&P 500 breadth is eroding: S5TH declined 0.93% to 63.02, S5TW fell 2.06% to 56.46, and S5OH was flat. When the index rallies and long-term breadth declines, the rally is narrowing to fewer, larger names. R2FI at 49.73 is once again just below the critical 50% threshold — the close relative to 50 remains the key breadth confirmation signal.

THE MACRO READ — CONNECTING THE DOTS

Here’s how everything connects. One theme, every asset.

The regime has evolved from post-selloff bounce to reflationary boom. The data is unambiguous: equities rallying, all five metals surging (platinum +6.60%, silver +3.98%, gold +0.96%, palladium +0.94%, copper +0.93%), yields rising across the entire curve with the belly leading, dollar weakening, Bitcoin surging 7.70%. This is a repricing of the inflation-growth mix toward higher on both dimensions.

The precious metals explosion is the single most important regime change from yesterday. The collapse of the gold-to-copper divergence means the market is no longer differentiating between safe-haven and pro-cyclical metals — it is bidding all hard assets as inflation hedges. Combined with the parallel bear shift in yields (5Y leading at +2.7 bps), this confirms inflation expectations are being ratcheted higher across the curve. Not transitory tariff noise. Persistent inflationary impulse.

NVDA’s beat-and-raise removes the dominant binary risk. $1.62 EPS vs. $1.53 est. Revenue of $68.13B vs. $66.21B est. Data center +75% YoY to $62.3B. Q1 guide of $78B. The muted after-hours response (~$196, +3.5%) is actually constructive — the market was correctly positioned. The AI capex thesis is validated. Combined with Monday’s AMD-Meta $100B deal, the infrastructure buildout story has never been stronger.

But the rally is narrowing. Only 5 of 11 sectors green. S&P 200-day breadth declining while the index rallies. The market is being carried by MSFT (+2.98%), META (+2.25%), TSLA (+1.96%), and the tech-financial-momentum complex. Momentum (MTUM +1.68%) seized leadership from High Beta (SPHB +1.58%) — the rally is becoming more selective and trend-following, not broadening. Thematic leadership is entirely digital: ARKW +4.04%, FINX +3.95%, BLOK +2.37%. Physical infrastructure (PAVE -1.04%, ITA -0.78%) is selling off.

Trump’s State of the Union was a non-event for markets but a structural signal for AI infrastructure. The Rate Payer Protection Pledge — forcing tech companies to cover their own power costs — is the first policy signal that could create a bifurcation in AI infrastructure winners. Companies that can self-power (nuclear, dedicated generation) will have structural advantages over those dependent on grid capacity. Tariffs “remain in place.” April 2nd reciprocal tariffs coming. Tax cuts through reconciliation. No Iran military escalation announced. Markets got no surprises, which is exactly what they needed.

CRM’s after-hours selloff confirms the SaaSpocalypse is alive. Even a beat ($3.81 vs. $3.04 est.) can’t overcome lukewarm forward guidance in a market where AI is simultaneously the biggest opportunity and the biggest threat to software margins. Benioff’s $50B buyback is capitulation-level signaling from management.

SECTOR SCORECARD

Sector spread widened to 273 bps (XLK +1.92% to XLP -0.81%), up from yesterday’s 194 bps. Only five sectors green versus nine yesterday. The most stunning individual move: Industrials collapsed from +1.23% yesterday to -0.78% today. Consumer Discretionary decelerated from +1.52% to +0.30%. The regime is rewarding growth and tech while punishing rate-sensitive, defensive, and physical-economy sectors.

MAG 7 PERFORMANCE

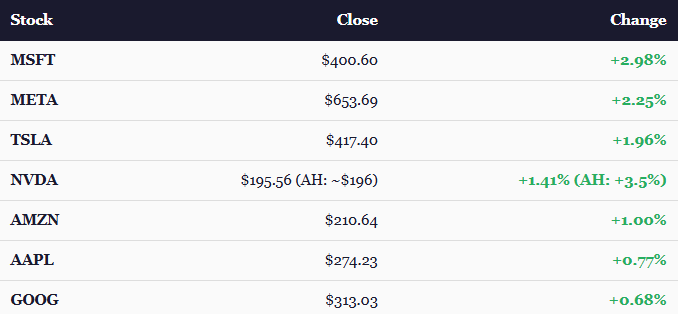

All seven green for the second straight day. MSFT surged to Mag 7 leadership at +2.98% — up from +1.18% yesterday. META reversed from near-flat +0.32% to +2.25%, resolving the ad-cyclicality tariff concern. GOOG finally broke its two-day losing streak. AAPL (+0.77%) is the day’s second-weakest after three days of leading — classic profit-taking rotation.

WHAT TO WATCH

NVDA post-earnings reaction tomorrow — $196 after hours implies a measured open; the question is whether the beat broadens the rally or just reinforces the narrow tech leadership

CRM after-hours -5% — lukewarm FY27 guide continues SaaSpocalypse theme; watch software ETFs at the open for contagion or isolation

Iran nuclear talks Thursday in Geneva — Gang of Eight was briefed on Iran hours before the SOTU; if talks produce a framework, crude could fall below $65 and inject a disinflationary impulse

Platinum at $2,331 (+6.60%) — may reflect positioning squeeze rather than fundamental demand; watch for follow-through or reversal

Silver at $90.99 — approaching $91 psychological level that could trigger momentum buying or profit-taking

R2FI breadth at 49.73 — still just below 50; a close above confirms breadth repair, a failure means the narrow-leadership concern intensifies

Dollar Index at 97.60 — if DX1! breaks below 97, it opens the door to further dollar depreciation that amplifies the commodity rally

US Initial Jobless Claims Thursday — consensus 216K; any reading above 225K gets attention

Fed speakers: Bowman and Barkin Thursday — listen for “patience” vs. “flexibility” on cuts after the parallel bear shift repriced inflation expectations higher

PPI Friday — the inflation data point that tells you where CPI is going; after PCE at 3.0%, a hot PPI confirms the reflationary thesis

CLOSING THOUGHT

Three days ago was panic. Today is a reflationary boom. The market round-tripped the entire tariff shock and then kept going — into a regime where equities, metals, yields, and risk assets are all moving higher simultaneously while the dollar weakens. NVDA delivered the beat-and-raise that validates the AI infrastructure thesis. Bitcoin reclaimed its pre-tariff levels with a 7.70% surge. Platinum exploded 6.60%. All five metals rallied at once for the first time in this cycle.

But the breadth is narrowing, not broadening. Five of eleven sectors green. Long-term S&P 500 breadth declining. The index is being carried by a handful of mega-cap tech names and a momentum-led factor regime. That creates fragility — and NVDA’s beat, while powerful, can’t fix the breadth problem alone. It can only keep the narrow leadership intact a little longer.

The question shifts now: Can the reflationary regime broaden? Can copper, platinum, and the commodity currencies pull industrial and physical-economy sectors back to green? Or does this become a two-tier market — tech and hard assets surging while everything in between erodes?

The regime has told you its name. Reflationary boom. Now we find out if it can last. Come back tomorrow night — NVDA’s morning reaction and the Iran nuclear talks will tell us a lot about where this goes next.

See you at The 5 O’Clock Print.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.