THE 5 O'CLOCK PRINT

What happened today. What it means. How to prepare.

TODAY’S CLOSING PRINT

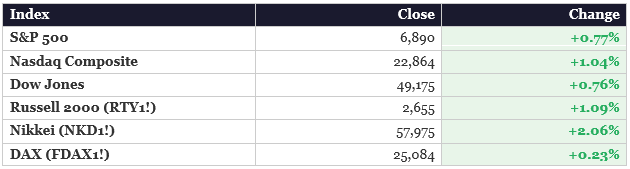

Yesterday was panic. Today was the repricing. Markets bounced across the board, volatility collapsed, and the tape told you exactly what kind of selloff Monday was — a one-day event, not a regime change. But the real story? It wasn’t the bounce. It was what bounced hardest.

Russell 2000 led the recovery at +1.09%. That matters. Monday’s selloff was led by small-caps and financials. Today the Russell led the bounce — textbook short-covering from the breadth washout we flagged last night, when 5-day breadth collapsed 47% to 30.02. The Nikkei surged over 2% for the second straight day, now up over 2,000 points in two sessions.

What Drove the Recovery

1. The tariff panic lasted exactly one session. Treasury Secretary Bessent spent the day soothing markets. The formal order to raise Section 122 tariffs from 10% to 15% is in process but the market has already digested it. The Supreme Court ruling that felt like a crisis on Friday and triggered Monday’s selloff has been fully repriced. Uncertainty didn’t disappear — it just got priced in.

2. The Meta-AMD mega-deal reshaped the AI narrative. Meta announced a multiyear partnership to deploy up to 6 gigawatts of AMD’s Instinct GPUs across its data centers — a deal worth potentially $100 billion. AMD surged 8.77% to $213.84. Intel gained 5.71%. This came days after Meta’s Nvidia deal, and the message is unmistakable: AI infrastructure spending is not slowing down. It’s accelerating and diversifying. The SaaSpocalypse in software is real, but the hardware buildout underneath it just got a massive vote of confidence.

3. Consumer confidence came in above expectations. CB Consumer Confidence rose to 91.2 from a revised 89.0, beating the 87.6 consensus. But dig deeper: the Expectations component only rose to 72 — the 13th consecutive month below the 80 recession-signal threshold. Present Situation actually fell 1.8 points to 120. Consumers are slightly less pessimistic about the future but more negative about right now. That’s the stagflation sentiment in one data point.

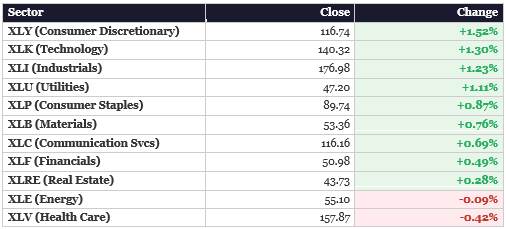

Key tell: Consumer Discretionary (XLY +1.52%) and Technology (XLK +1.30%) led the session — they were yesterday’s worst sectors. Health Care (XLV -0.42%) was today’s worst — it was yesterday’s second-best. A complete sector inversion. The tape is telling the story: this was a mean-reversion day, not a new trend.

THE SIGNAL IN THE NOISE — THE METALS ROTATION & THE AMD EARTHQUAKE

Here’s what most people missed while they were watching the bounce: the commodity market just drew the clearest regime map of the year. And AMD may have just broken Nvidia’s monopoly pricing power — 24 hours before NVDA reports earnings.

The Pro-Cyclical Metal Rotation

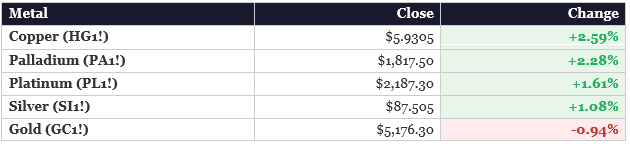

This is the most important table in today’s report. Yesterday, gold surged $145 while copper fell. Today, copper surged 2.59% to multi-week highs while gold gave back $49. The gold-to-copper ratio reversed sharply. Industrial metals are surging. Monetary metals are fading. The market has decisively repriced the Section 122 tariff from “growth shock requiring Fed cuts” to “inflationary impulse the economy can absorb.” That’s a fundamentally different macro regime.

Palladium and platinum confirming alongside copper is cross-asset confirmation — this isn’t a one-commodity story, it’s a pro-cyclical rotation across the entire industrial metals complex.

The AMD-Meta Deal — Why It Matters Beyond AMD

Meta just committed to potentially $100 billion in AMD chips — 6 gigawatts of GPU capacity, including a 160-million-share warrant giving Meta up to 10% of AMD. This came days after Meta’s Nvidia deal. The implications ripple across every AI infrastructure name:

AI capex isn’t just intact — it’s so large that hyperscalers need multiple suppliers at scale. Nvidia’s monopoly pricing power is now under structural pressure heading into tomorrow’s earnings. AMD just became a real second source, not a niche alternative. And the total addressable market for AI chips just expanded — Meta alone is spending $135 billion in capex this year.

The cross-asset read: AMD +8.77%. Intel +5.71%. NVDA +0.68%. The market is telling you that AI infrastructure demand is so massive it’s creating space for competition. That’s bullish for the buildout thesis — copper, power infrastructure, data centers — even if it complicates the NVDA monopoly narrative. Watch how NVDA responds to this setup tomorrow.

THE MACRO BACKDROP

Rates — Bear Steepener Replaces Bull Flattener

The yield curve regime flipped in one day. Yesterday was a bull flattener — the 5-year led the rally, pricing growth risk. Today is a bear steepener — the 2-year rose 2.5 bps while the 30-year fell 1.5 bps. The 2s10s spread widened to approximately 57.2 bps. Translation: the bond market is pulling back roughly one Fed cut from 2026 expectations. The front end is repricing the tariff as inflationary (keeping the Fed on hold), while the long end is catching a bid from duration buyers who don’t see a secular inflation problem — just a one-time price level adjustment.

MOVE index fell 4.07% to 65.27 — a major de-escalation after yesterday’s intraday reversal to +5.86%. Bond market volatility is normalizing. The 30-year mortgage dropped to 6.01%, the first reading below 6.05% in this cycle.

Consumer Confidence — The Recession Signal Persists

Headline: 91.2 (beat consensus of 87.6). But the Expectations component at 72 remains below the 80 recession-signal threshold for the 13th consecutive month. Present Situation fell 1.8 points. Consumer write-in responses skewed toward pessimism around prices, inflation, and cost of goods — with mentions of trade and politics increasing. This is a consumer who feels slightly less bad about the future but worse about right now. Not a confidence recovery. A pause in the deterioration.

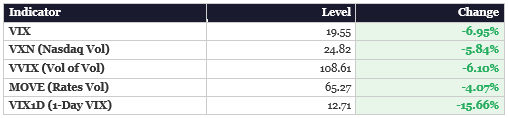

Volatility — The Fear Collapsed

VIX broke back below 20. That’s the single most important signal in the vol complex today. VVIX below 110 means tail hedging demand has evaporated. VIX1D at 12.71 (-15.66%) confirms zero spot panic. And 1-month implied correlation collapsed 15.57% — meaning stocks are moving independently again. The macro-driven “sell everything” regime from Monday is over. Stock-picking and fundamentals are back in the driver’s seat. Right on time for NVDA earnings tomorrow.

State of the Union — Tonight at 9:00 PM ET

Trump delivers the Union tonight. He’s expected to tout affordability, push for new personal and corporate tax cuts through reconciliation, and lay out a trade agenda that contextualizes the Section 122 tariffs. Markets will be watching for any specifics on tariff duration, Iran military posture, and deregulation. Virginia Governor Abigail Spanberger delivers the Democratic response. Any market-moving language on tariffs, taxes, or Iran will hit futures overnight — this is the wild card that could set tomorrow’s tone heading into NVDA earnings.

WEEK AHEAD — WHAT’S STILL ON DECK

⭐ Wednesday, February 25 — THE DAY

NVIDIA Earnings After Close — Consensus: $1.53 EPS | $65.7B Revenue. The setup is now maximally interesting. AMD just got a $100 billion vote of confidence from Meta, validating AI infrastructure demand but raising competitive questions. NVDA was the weakest Mag 7 gainer today at +0.68% while SOXX rallied 1.46% — the market is hedged but constructive. Goldman has a $250 target calling for a beat-and-raise. The options market implies ~8% move. A beat with strong Blackwell guidance would confirm the regime. A miss or weak guidance in the context of AMD’s Meta deal would raise serious questions about Nvidia’s pricing power.

Salesforce (CRM) also reports. The SaaSpocalypse test continues.

Cross-asset chain: NVDA beat → AI capex confirmed → copper and power infrastructure bid → grid buildout accelerates. But now add: NVDA beat + AMD deal = multi-vendor AI buildout thesis → even more bullish for copper, power, and data center infrastructure than a single-vendor story.

Thursday, February 26

US Initial Jobless Claims — Consensus: 216K. Any reading above 225K gets attention. Fed Speakers: Bowman and Barkin — listen for “patience” vs. “flexibility” on cuts. Iran nuclear talks reportedly resuming Thursday — energy weakness today (WTI -1.03%) may be pricing in optimism on a deal framework. If talks produce progress, crude could fall below $65 and inject a disinflationary impulse.

⭐ Friday, February 27

US PPI — the inflation data point that tells you where CPI is going. After PCE at 3.0%, a hot PPI confirms sticky inflation. A cool PPI gives the Fed breathing room. Canada GDP and Eurozone Final CPI round out the week.

Weekend Watch

China PMI (Sunday) — Prior: 49.3, below 50. Commodity currency sensitivity remains high.

THE MACRO READ — CONNECTING THE DOTS

Here’s how everything connects. One theme, every asset.

The tariff-shock regime lasted exactly one session. Monday’s 458 bps sector spread, 308 bps factor spread, and historic breadth washout have been completely reversed. XLY replaced XLP as sector leader. SPHB replaced SPLV as factor leader. A 462 bps swing in the SPHB-to-SPLV spread in a single day — the sharpest factor reversal we’ve tracked. The market round-tripped the entire panic in 24 hours.

The yield curve tells you what regime we’re actually in. The flip from bull flattener (Monday — pricing growth shock and Fed cuts) to bear steepener (Tuesday — pricing inflation and Fed on hold) is the macro tell. The bond market is saying the tariff is inflationary but manageable. Not a recession trigger.

The copper-gold rotation is the clearest confirmation. Gold -0.94% while copper surges 2.59%. Industrial metals up, monetary metals down. Palladium and platinum confirming. The market is rotating from safe-haven positioning to pro-cyclical positioning. Cross-asset confirmation of the bear steepener thesis — growth expectations are stabilizing, not collapsing.

The AI infrastructure buildout just got bigger, not smaller. Monday’s SaaSpocalypse selloff was real — AI is disrupting software revenue. But the Meta-AMD deal confirms that the hardware layer underneath is growing so fast it needs multiple suppliers at scale. The AI capex story went from “Nvidia wins everything” to “the market is so large that AMD, Intel, and Nvidia all win.” That’s more bullish for copper, power, and data center infrastructure than the single-vendor narrative ever was.

The correlation collapse means stock-picking is back. 1-month implied correlation cratered 15.57%. Monday’s macro-driven “everything correlates” session is over. Individual fundamentals matter again. And the biggest individual fundamental this week arrives tomorrow after the close: NVDA earnings.

SECTOR SCORECARD

Sector spread compressed from 458 bps yesterday to 194 bps today. Complete inversion — yesterday’s leaders are today’s laggards. Nine of eleven sectors green. XLF (+0.49%) recovering but still weak relative to the tape — structural headwinds remain beyond the rate story.

WHAT TO WATCH

▸ NVDA earnings tomorrow after close — the AI infrastructure verdict, now with the AMD-Meta deal as backdrop

▸ State of the Union tonight at 9 PM ET — watch for tariff specifics, Iran language, and tax cut details that could move overnight futures

▸ Salesforce earnings Wednesday — the SaaSpocalypse test continues

▸ PPI Friday — confirms or contradicts the sticky inflation narrative after PCE 3.0%

▸ Iran nuclear talks Thursday — energy weakness today may be front-running a deal; crude below $65 would be disinflationary

▸ Fed speakers: Bowman and Barkin Thursday — March FOMC calibration after the bear steepener repricing

▸ Copper at $5.93 — multi-week highs; if it holds, the pro-cyclical rotation is confirmed

▸ R2FI breadth at 49.74 — right at the 50% threshold; a close above 50 tomorrow confirms breadth repair

▸ China PMI Sunday — EM and commodity FX directional signal

CLOSING THOUGHT

Monday was panic. Tuesday was the repricing. The market round-tripped the entire tariff shock in 24 hours — a 462 bps factor swing, a complete sector inversion, VIX crushed below 20, and the copper-gold rotation drawing the clearest pro-cyclical signal of the year. But the real story today was Meta handing AMD a $100 billion deal and telling the market that AI infrastructure demand is so large it needs multiple suppliers at gigawatt scale. That’s not a threat to the AI thesis — that’s the thesis getting bigger. Now comes the test. NVDA reports tomorrow after the close. Trump speaks tonight at 9 PM. The regime has shifted from fear to fundamentals, from correlation to stock-picking, from panic to positioning. The macro told you Monday was a one-day event. The close confirmed it. Stay positioned, stay focused, and come back tomorrow night — NVDA and the State of the Union are going to tell us a lot about where this goes next.

See you at The 5 O’Clock Print.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.