The Bifurcation

Between Stagflation and Reflation

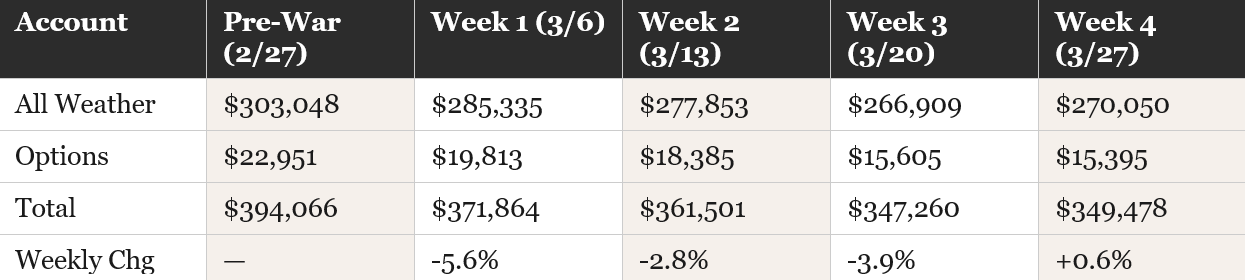

The Numbers

Total family portfolio: $349,478.40. All Weather Macro: $270,050.33. Options: $15,395.57.

For the first time since the war began, the All Weather portfolio posted a green week. Up $3,141 from last week’s $266,909. The total portfolio recovered $2,218 — modest, but directional. After three straight weeks of red, the bleeding stopped.

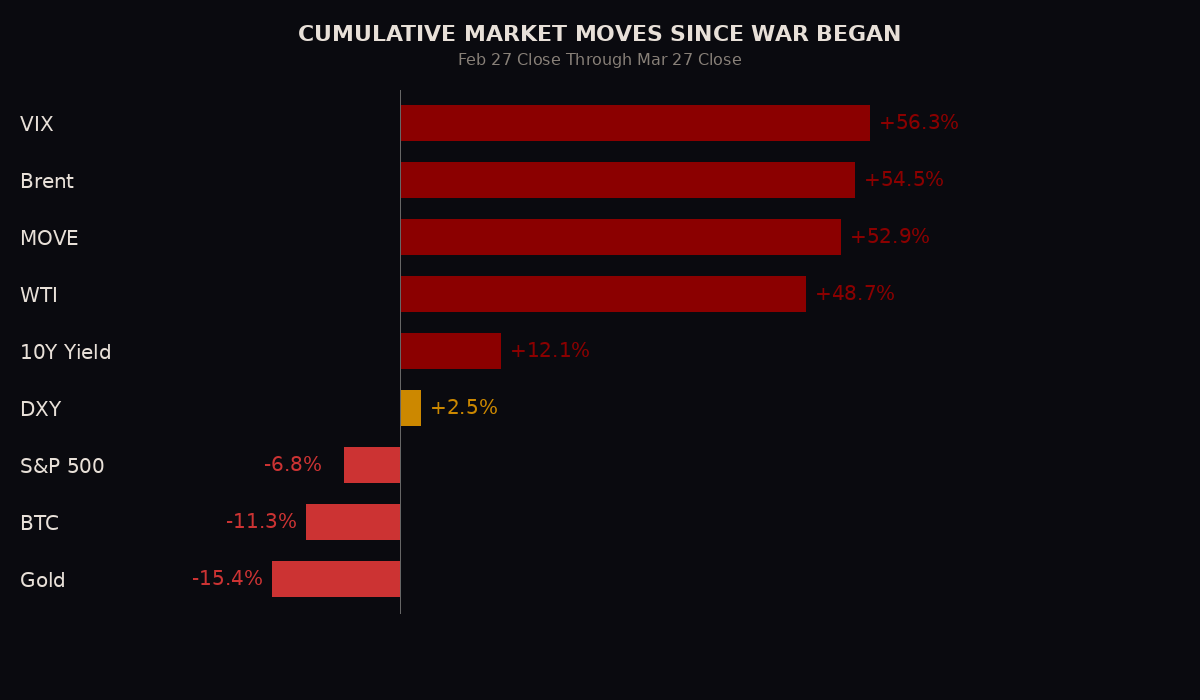

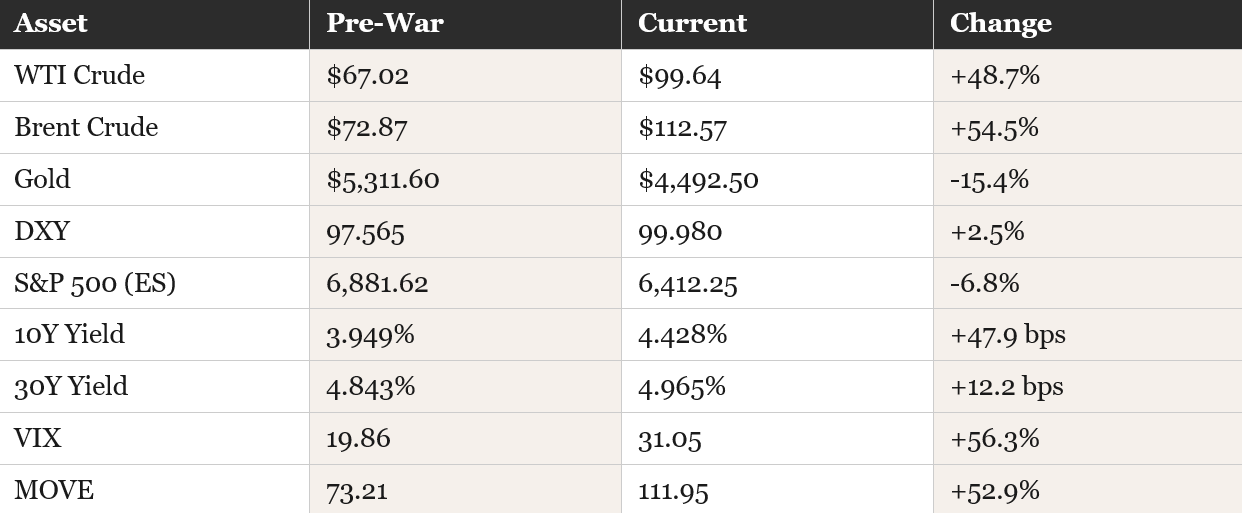

But let’s be honest about the environment. The S&P posted its 5th consecutive weekly loss — the worst streak since 2022. The Dow briefly entered correction territory on Friday. The Nasdaq is 12.5% below its October high. VIX breached 30 for the first time in the war. The 30-year yield touched 5.00% intraday. Brent settled at $112.57 — the highest since the war began. Consumer sentiment cratered to 53.3 with inflation expectations unanchoring at 3.8%.

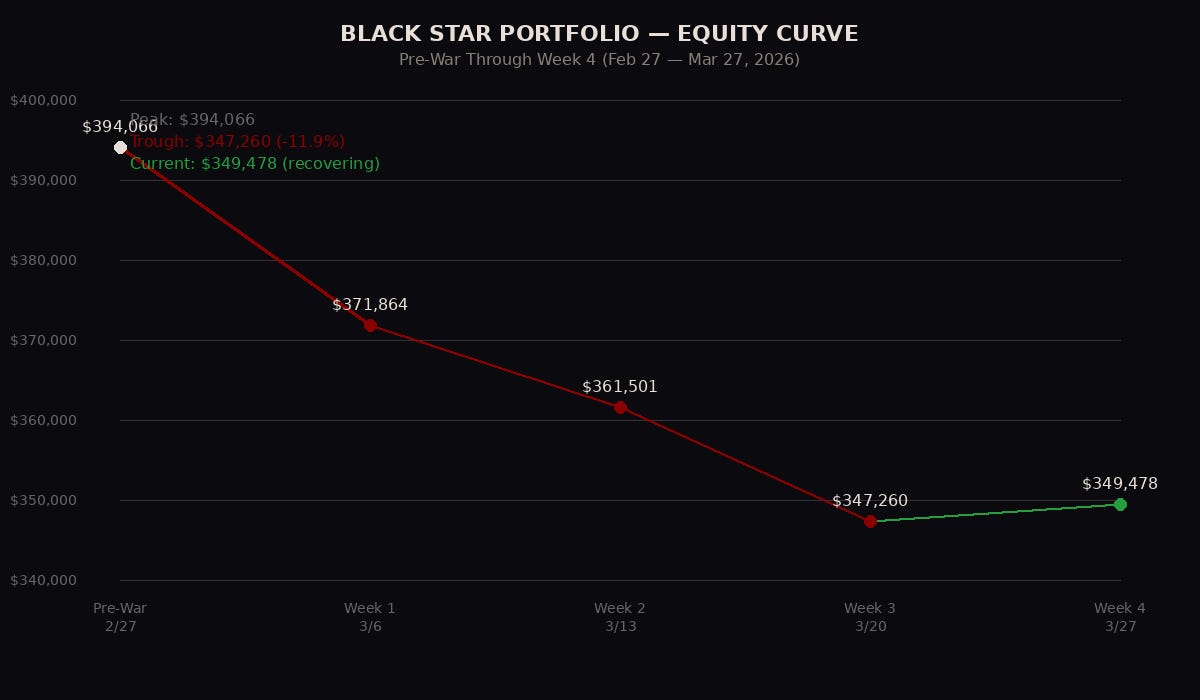

The portfolio stabilized while the broader market deteriorated further. That’s the framework holding.

Portfolio Snapshot

The metals complex that was driving the drawdown is showing signs of turning. Gold bounced $116 from its war low on Friday — up 2.66% with GVZ (gold volatility) barely moving. That’s the signal that forced liquidation is exhausting itself. All five tracked metals finished green for the first time since Day 20 of the conflict. The margin-call death spiral that pushed gold from $5,311 to $4,376 may be running out of sellers.

The Economy Is Splitting in Two

This is the macro read that matters for your positioning. The economy isn’t in full stagflation and it isn’t in reflation. It’s both at once — depending on where you look.

The reflationary side:

Flash Manufacturing PMI beat expectations across the board last week. US at 52.4. Germany at 51.7 — a massive beat against a 49.5 forecast, 45-month high. Eurozone at 51.4 — also a 45-month high. UK at 51.4. Manufacturing is expanding globally, driven by defense spending, stockpiling behavior ahead of supply disruptions, and the AI infrastructure buildout that shows no signs of slowing.

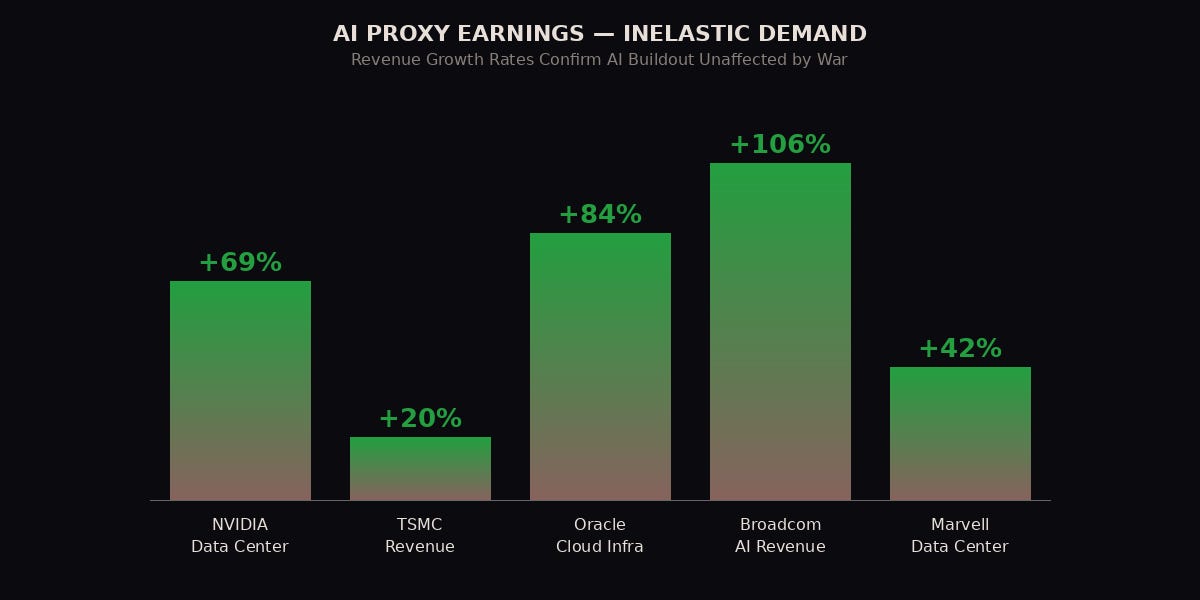

The AI spending engine is inelastic. NVIDIA controls 92% of the AI accelerator market and guided $78B for Q1 — assuming zero China revenue. TSMC boosted capex to $52-56B for 2026 and raised its AI accelerator growth forecast through 2029. Oracle beat across the board — cloud infrastructure revenue surged 84% to $4.9B with a $553B backlog, up 325% year-over-year. Broadcom’s AI revenue hit $8.4B, up 106%. Marvell’s custom AI silicon went from near-zero to $1.5B in one fiscal year. The five largest hyperscalers have committed $700B to AI data centers in 2026.

Data centers don’t stop building because oil is at $112. That demand is deadline-driven, not price-discretionary. The same dynamic supports the copper triple convergence — military demand, AI infrastructure, and construction seasonality don’t respond to crude prices the way discretionary spending does.

Unemployment claims came in at 210,000 — right at expectations. Continuing claims fell to 1.819 million, the lowest since May 2024. The labor market is in “low-hire, low-fire” mode. No deterioration yet despite the war’s energy shock.

The stagflationary side:

Flash Services PMI missed in Germany — 51.2 vs 52.5 expected. Commentary pointed directly to stagflationary pressures from the Iran war. Manufacturing is holding up on industrial demand, but consumer-facing services are weakening from energy costs.

UoM Consumer Sentiment cratered to 53.3 — the lowest since late 2025. The dangerous number: 1-year inflation expectations jumped to 3.8% from 3.4%. That +40 basis point spike is the largest monthly increase since April 2025 and signals inflation expectations becoming “unanchored” — the Fed’s nightmare scenario. When consumers expect nearly 4% inflation, they change behavior: demanding higher wages, accelerating purchases, reducing savings. That creates a self-fulfilling spiral.

GDP revised to 0.7%. NFP was -92,000 last month. Gas approaching $4/gallon. Brent at $112.57 — war high. Core PCE at 3.1%. The consumer is being squeezed from every angle.

The bifurcation: The industrial/AI/defense economy looks reflationary. The consumer/services economy looks stagflationary. The economy is splitting along this fault line, and your positioning needs to reflect which side you’re on.

The Fed Trap Is Not What You Think

Markets are now pricing a 52% probability that the Fed’s next move is a rate hike. First time crossing the 50% threshold. That headline sounds terrifying. But I want you to understand what’s actually happening because most financial media is framing this wrong.

The Fed holding rates at 3.75% is not the same as the emergency tightening cycle of 2022. In 2022, inflation was demand-driven — the economy was overheating, consumers were spending, and the Fed actively hiked from 0% to 5.5% in 18 months to cool demand. They had a tool for that problem.

This time, inflation is supply-driven. Oil is above $112 because the Strait of Hormuz is closed, not because consumers are overspending. The Fed knows cutting into $100+ oil would pour gasoline on the inflation fire. But they also know the economy is weakening — GDP at 0.7%, negative NFP, sentiment cratering.

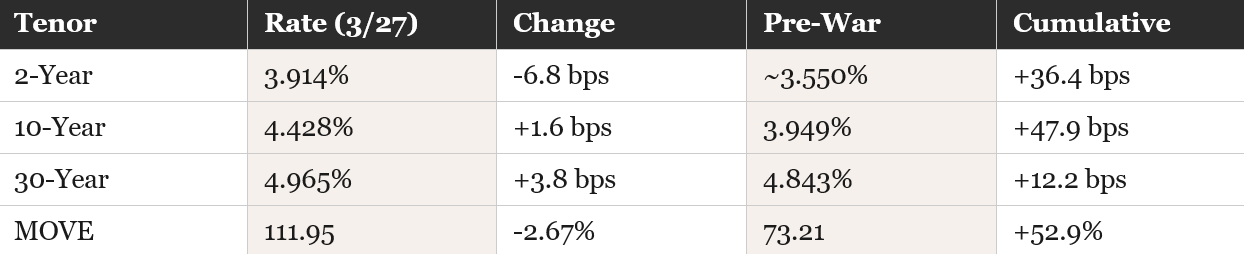

So they hold. And holding at 3.75% while inflation rises from supply shocks means real rates are tightening passively without the Fed doing anything. The market is doing the Fed’s work through higher energy prices, tighter financial conditions, and a rising term premium on the long end. The 30-year touched 5.00% intraday on Friday — that tightens mortgages, corporate borrowing, and equity valuations without a single Fed action.

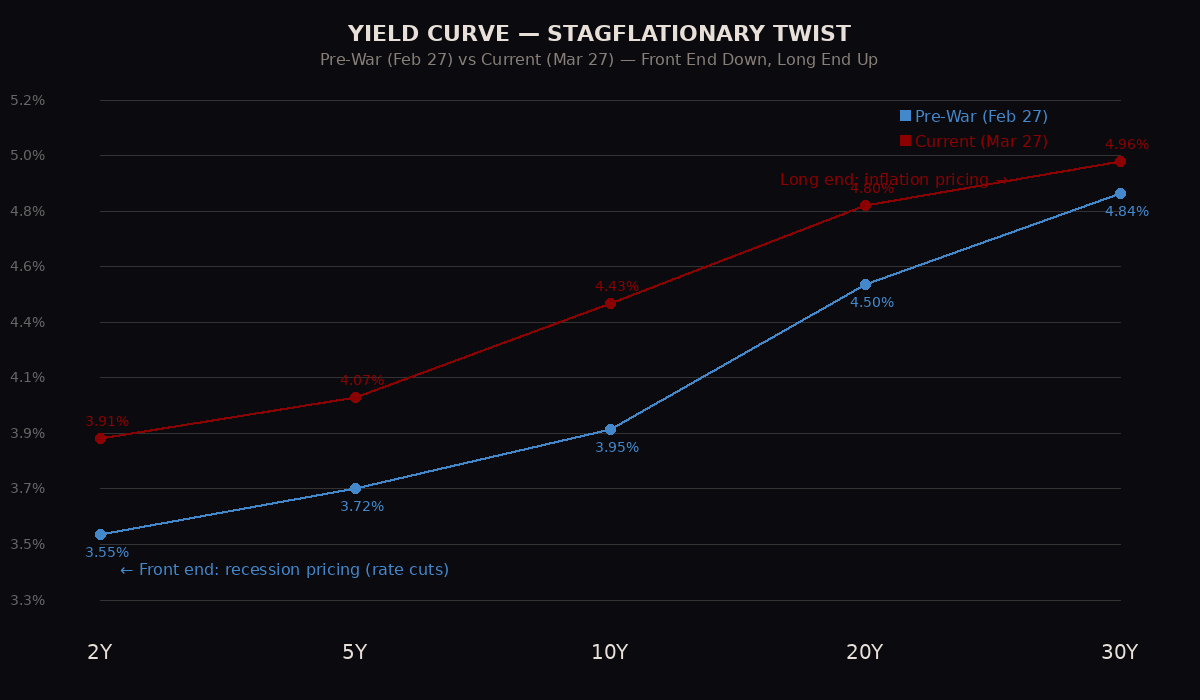

The yield curve told this story in real time on Friday. The front end rallied — 2-year down 6.8 basis points to 3.914% — because the market is pricing eventual rate cuts when the growth collapse forces the Fed’s hand. The long end sold off — 30-year up 3.8 basis points to 4.965% — because no one wants to hold long-duration bonds with Brent at $112 and inflation expectations at 3.8%.

That’s the stagflationary twist — simultaneously pricing recession at the front end and inflation at the long end. The signature of a 1970s-style supply shock. Different from 2022 in every way that matters.

Trump Controls the Narrative

I need to say this clearly because it affects every position in the portfolio and every data point in this newsletter.

Every major market move since February 28 has been initiated by a Trump statement, not by economic data. The data confirms or challenges the move afterward, but Trump initiates it:

Liberation Day April 2025 — Trump crashed the market with tariffs, then tweeted “buy” and the market reversed. Monday March 23 at 7:05 AM — Trump announced productive talks with Iran and futures flipped green in real time. Saturday March 22 — the 48-hour ultimatum crashed Asian markets. The 5-day pause spiked equities. The extension to April 6 provided temporary relief. Every time.

The economic calendar this week is loaded — Powell speaks today, JOLTS Tuesday, ISM Manufacturing Wednesday, NFP Friday. But any single Truth Social post can override all of it. Until the war resolves, the macro regime is a Trump narrative regime. The data tells you where the economy is. Trump tells you where the market goes.

This is also why I believe Trump wants the deal more than he’s letting on. His actions tell a different story than his words. He keeps announcing “productive talks” that Iran denies are happening. He extended the strike pause twice — first 5 days, then to April 6. He sent a 15-point peace plan through Pakistan. Iran rejected it and issued their own 5-point counteroffer. The body language says negotiation, not escalation.

He can’t frame it as wanting the deal because that would appear weak. But $112 oil, a market in correction, gas approaching $4, and inflation expectations unanchoring at 3.8% are all politically toxic. Treasury Secretary Bessent told the nation: “50 days of higher prices for 50 years of no Iran nukes.” They know the trade-off. The question is how long the market lets them make it.

The War Is Causing Structural Damage

Two developments this week shifted the war’s market impact from temporary disruption to structural economic damage.

Iraq declared force majeure on ALL foreign-operated oilfields. Iraq can’t ship through Hormuz, so it shut down production. This means oil disruptions have expanded beyond Iran to its neighbors. Even if Trump and Iran agree to a ceasefire tomorrow, Iraq’s force majeure persists until Hormuz shipping actually resumes. The damage is self-reinforcing.

Iran turned back two Chinese-owned container vessels from Hormuz. China was previously treated as a neutral party by Iran. Blocking Chinese ships signals the blockade is expanding, not loosening. This threatens to bring China directly into the conflict and further restricts global oil flows.

These aren’t headline risks that disappear with a tweet. These are structural supply disruptions that take weeks to unwind even after a resolution.

China, Europe, and the Ally in the Middle

The Wall Street Journal reported this week that China’s economy is falling behind due to deflation and a weak currency. The energy shock from Hormuz is transmitting directly into their economy — and now Iran is blocking their ships too.

Think about China’s position: 80% of Iran’s oil exports went to China. 50% of China’s crude transited Hormuz. Trump sanctioned 84% of Iranian tankers. He postponed the Xi summit because of the Iran conflict. He’s asking China to send warships to Hormuz. He’s systematically destroying their energy supply chain while telling them to come help fix it.

Europe confirmed what the data already showed — the war is crushing them through energy prices. Flash Manufacturing PMI beat expectations (Eurozone 51.4, 45-month high) but services weakened and inflationary pressures intensified markedly. Macron’s nuclear rearmament — expanding France’s arsenal, deploying jets to 8 allies, the France-Germany steering committee — is the structural response to an energy and security crisis that Europe can no longer outsource to the US.

Japan is the wild card nobody is talking about. Japan is one of America’s closest Pacific allies, the largest foreign holder of US Treasuries, and a massive net energy importer at 2.8 million barrels per day. The yen weakened to 160 this week — intervention risk territory. Trump met with Japan’s Prime Minister, and on the surface it’s cherry blossom trees and diplomatic niceties. But underneath, Japan is being squeezed by the same energy crisis Trump is using as leverage against China. He’s asking Japan to send warships to Hormuz while simultaneously creating the conditions that are crushing Japan’s economy. Managing that ally relationship is the geopolitical thread most analysts are missing.

What Institutions Are Telling You

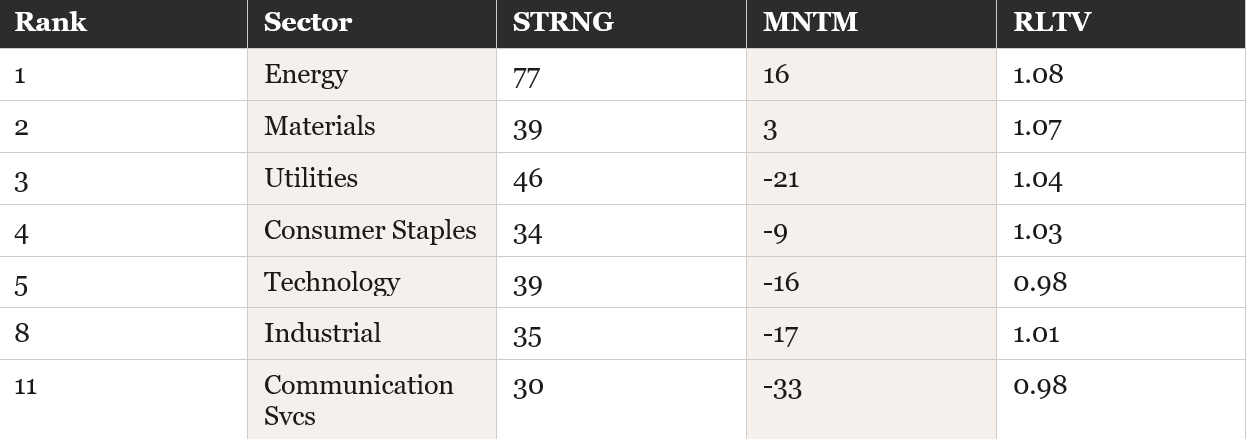

The Quiggle rankings from Friday March 27:

Sectors:

The headline: Materials jumped from #11 (dead last for three straight weeks) to #2. That’s the single biggest sector move of the entire war. Momentum flipped to positive (+3). The double squeeze — crude costs plus dollar conversion — is unwinding as the forced liquidation exhausts itself and structural demand reasserts. This is the early signal of the regime shift you’ve been positioned for.

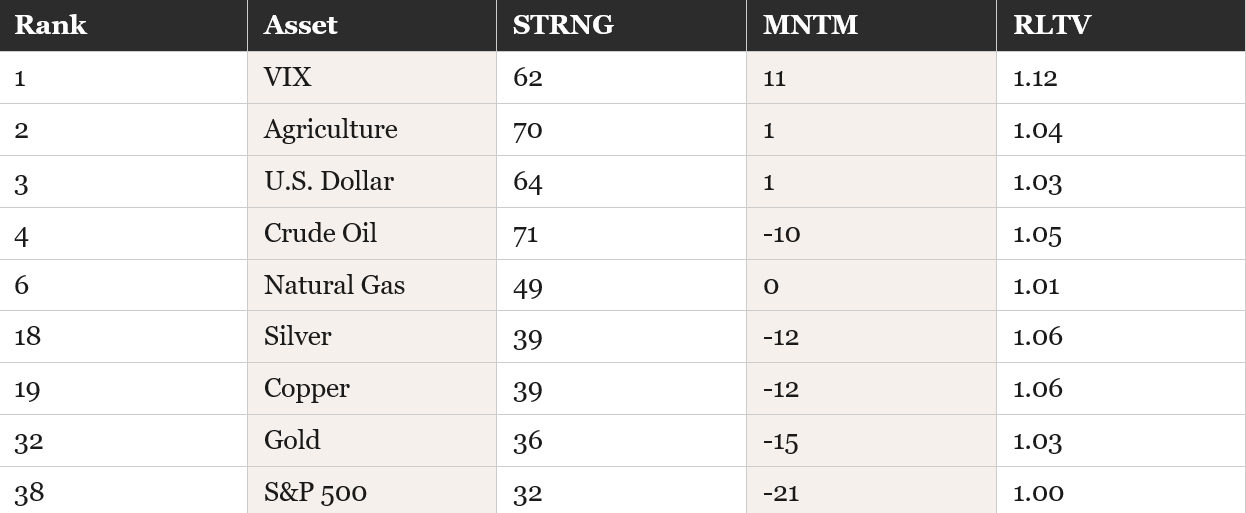

Top Assets:

VIX at #1 tells you fear is the top-performing “asset” on the board. But crude oil’s momentum flipped negative (-10) for the first time — the war premium may be peaking. Silver and copper RLTV both at 1.06 — starting to outperform the market despite the drawdown. Gold still buried at #32 but RLTV at 1.03 — beginning to recover.

Industry: Aerospace-Defense cratered to #50 out of 51 industries. Still selling during a war. Meanwhile O&G E&P holds #1, O&G Services #2, Lithium jumped to #6, and Copper Miners at #24 with RLTV 1.06.

Earnings Confirm the Bifurcation

The AI proxy earnings tell you which side of the economy is winning:

Oracle: Revenue $17.2B (+22% YoY). Cloud infrastructure +84% to $4.9B. Backlog $553B, up 325%. Raised FY2027 guidance to $90B. Stock jumped 10%.

NVIDIA: 92% AI accelerator market share. $78B Q1 guidance excluding China. $700B hyperscaler commitment across the top five cloud providers.

TSMC: Revenue beat estimates. Capex raised to $52-56B. AI accelerator growth forecast raised through 2029.

Broadcom: AI revenue $8.4B, up 106%. Q2 guide $22B. Line of sight to $100B AI chip revenue by 2027.

Marvell: Data center record $1.65B. Custom AI silicon from near-zero to $1.5B in one year.

Manufacturing PMI beating. AI spending accelerating. Defense production ramping. This is the reflationary engine running underneath the stagflationary headlines.

The economy is bifurcated — and the side you want to be on is the side building infrastructure, not the side paying $4 for gas.

The Week Ahead: March 30 – April 4

This is the most consequential week since the war began. The April 6 deadline — Trump’s extended pause on attacking Iran’s energy facilities — expires this weekend.

Monday (today): Powell speaks at 10:30 AM. LME Copper Inventories already reported at 2,350 vs 425 prior — massive build worth watching for the copper thesis.

Tuesday: CB Consumer Confidence (88.0 forecast vs 91.2 prior — expected decline). JOLTS Job Openings (6.90M forecast).

Wednesday: Core Retail Sales (0.3% forecast), Retail Sales (0.4% forecast), ISM Manufacturing PMI (52.3 forecast vs 52.4 prior), ISM Manufacturing Prices (73.6 forecast vs 70.5 — inflation accelerating in manufacturing inputs).

Thursday: Unemployment Claims (212K forecast vs 210K prior). Natural Gas Storage. Baker Hughes Rig Count.

Friday: NFP (56K forecast vs -92K prior). This is the week’s centerpiece. Last month was catastrophic — negative 92,000 jobs. The forecast of +56K would be a massive reversal. If it beats, the labor market narrative holds and the “between stagflation and reflation” thesis strengthens. If it misses again, pure stagflation takes over.

The wild card: April 6 is Saturday. If the deadline passes without a deal or extension, strikes could resume on Iranian energy infrastructure. If Trump extends again or announces progress, markets get another relief rally. Every position in the portfolio is subject to whatever Truth Social says this weekend.

Cumulative Market Moves (Feb 27 close through March 27)

Process Over Prediction

The portfolio stabilized while the market crashed. Materials jumped from dead last to #2. Gold bounced from war lows. The forced liquidation is pausing. Manufacturing PMI is beating globally. AI spending is accelerating. The structural theses — copper, defense, energy leverage — haven’t broken.

But VIX is above 30. The 30-year touched 5%. Inflation expectations are unanchoring. Iraq declared force majeure. The war is causing structural damage that persists beyond any ceasefire headline.

The economy is bifurcated. The side building AI infrastructure and producing defense equipment is reflating. The side paying $4 for gas and watching sentiment crater is stagflating. Your job as a macro investor is to be positioned on the right side of that split.

And hanging over all of it — every data point, every thesis, every position — is one man’s Truth Social account. Until the war resolves, that’s the regime.

Process over prediction. Data over headlines. Framework over fear.

Glossary

Stagflationary Twist: A yield curve where the front end rallies (pricing recession/rate cuts) while the long end sells off (pricing inflation). Both sides of stagflation priced simultaneously.

Force Majeure: A legal clause allowing parties to suspend contractual obligations due to extraordinary circumstances. Iraq’s declaration means oil production halted regardless of whether fighting stops.

Unanchored Inflation Expectations: When consumers expect high inflation (3.8%) and change behavior accordingly — demanding higher wages, accelerating purchases. Creates a self-fulfilling spiral the Fed can’t address without crashing the economy.

VIX Backwardation: When short-term VIX (VIX1D) trades above the 30-day VIX — signals the market expects more volatility today than over the next month. The signature of intraday panic dynamics.

COR1M: One-month implied correlation. At 41.68 (war high), every stock moves together. Zero stock-specific alpha available.

Bifurcation: The economy splitting along a fault line — one side reflationary (manufacturing, AI, defense), the other stagflationary (consumer, services, energy costs).

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.

The goal is not for you to depend on me. The goal is for you to not need me.