☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: RISK-ON WITH DEFENSIVE ROTATION — ES 7,165.25 (+0.30%). NQ +1.17% LEADING ON SOXX +2.14% SEMIS BROADENING. MOVE REVERSED BACK DOWN TO 67.70 (−3.12%) — THE BOND MARKET CAPITULATION HELD. TSLA BEAT Q1 EPS ($0.41 vs $0.37) BUT STOCK −3.56% ON $25B CAPEX RAISE. MSFT −3.97%, META −2.31% POSITIONING INTO ACTUAL APRIL 29 EARNINGS (DYRH HAD DATES WRONG). WTI $95.79 (−0.06%) STABLE. BRENT −5.51% TO $99.28 — MOST DRAMATIC BRENT SINGLE-SESSION DECLINE SINCE DAY 29. CLAIMS 214K (FIRST POST-TARIFF PRINT — SLIGHTLY ABOVE 210K CONSENSUS). MICHIGAN REVISED SENTIMENT 10 AM TODAY. FACTOR TAPE DEFENSIVE: USMV-SPHB +1.20%. SPLV LEADING FACTORS.

The MOVE Index is the story. After three consecutive sessions of expansion toward the 73.21 pre-war baseline (65.70 → 67.90 → 70.78), MOVE reversed sharply to 67.70 (−3.12%) on Thursday — the bond market’s capitulation thesis HELD. The expansion toward baseline that threatened to reverse the post-Day-35 capitulation has been walked back. MOVE at 67.70 is now 5.51 points below the pre-war 73.21 baseline, and the trajectory shows the expansion was a positioning adjustment around the ceasefire expiration binary rather than a fundamental regime reversal. The bond market remains comfortable with the frozen-conflict framework.

Tesla delivered a clean Q1 beat on Wednesday after close: adjusted EPS $0.41 vs $0.37 consensus (+10.8%), revenue $22.39B vs $22.35B (slight beat), automotive gross margin improved to 19.2%, energy storage margins hit a record 39.5%, free cash flow $1.4B. Musk called Optimus ‘probably the biggest product ever.’ BUT — TSLA stock initially rallied +4% after hours and then REVERSED after the earnings call revealed 2026 capex guidance of $25B, up dramatically from the prior $20B guidance — a $5B capex increase that the market read as margin-dilutive. TSLA closed Thursday at −3.56%. The TSLA pattern is now the war’s cleanest ‘beat and invest forward’ trade: earnings beat but capex concerns overwhelm the beat reaction.

CRITICAL CALENDAR CORRECTION: The DYRH listed GOOGL, MSFT, META, and CAT as reporting Thursday April 23 after close. This is WRONG. Per Microsoft’s own investor relations page and multiple verified sources, MSFT reports fiscal Q3 on April 29 after close. GOOGL and META also report April 29. The MSFT −3.97%, META −2.31%, and GOOG −1.47% pre-market moves are regular Thursday trading and pre-positioning — NOT earnings reactions. The mega-earnings day has been RESCHEDULED to next Tuesday April 29, which is also the FOMC meeting day. This creates an extraordinary convergence: FOMC statement + Powell press conference + MSFT/GOOGL/META earnings all on the same day.

NQ at +1.17% leading all indices despite MSFT/META/TSLA red tells you the rally is being driven by SOXX (+2.14% — semis broadening beyond NVDA into AMD, AVGO, MU) and PAVE (+2.21% — infrastructure bid on the frozen-conflict supply-chain investment thesis). The factor tape has flipped DEFENSIVE: USMV-SPHB spread +1.20% (the widest positive spread since Monday’s weekend-risk session). SPLV +1.50% leading all factors — low-vol premium is being paid. This is not a broad risk-on session — it is a narrow tech-semis rally with defensive underpinning everywhere else.

The Number That Matters: MOVE 67.70 (−3.12%). The Bond Market’s Capitulation Held. The Three-Session Expansion Toward 73.21 Was A Positioning Adjustment, Not A Regime Reversal.

MOVE trajectory this week: 65.70 (Friday floor) → 65.70 (Monday) → 67.90 (Tuesday) → 70.78 (Wednesday — peak expansion, 2.43 from baseline) → 67.70 (Thursday — reversal). The expansion was driven by: ceasefire expiration binary, Warsh hearing governance uncertainty, Retail Sales hawkish repricing. The compression is driven by: ceasefire extended (tail risk removed), TSLA earnings digested (no contagion), and the market’s recognition that the next catalysts (FOMC + mega-earnings April 29) are five days away. MOVE at 67.70 gives equities room to extend.

The Setup: Mixed / Indeterminate — Risk-On — Energy Steady. MOVE Reversed Back Sub-Baseline. Factor Tape Defensive. TSLA Beat But Reversed On Capex. Mega Earnings Now April 29 (FOMC Day). Michigan Sentiment 10 AM Today. Frozen Conflict Continues.

2. OVERNIGHT SESSION RECAP

Wednesday Cash Session — TSLA After Close

Wednesday’s session was constructive with ES rallying +0.63% on the ceasefire-extension relief trade. TSLA reported after close: Q1 adjusted EPS $0.41 vs $0.37 (+10.8% beat), revenue $22.39B vs $22.35B (+0.2% beat), auto gross margin 19.2% (up from 16.3% YoY), energy storage margin 39.5% (record), FCF $1.4B (+117% YoY), total revenue +16% YoY. Musk emphasized Optimus humanoid robot and AI5/AI6 chip development. BUT — the 2026 capex guidance of $25 billion (up $5B from $20B) was the session-killer. Capex jumped 67% in Q1 to $2.49B from $1.49B YoY. The market read: strong earnings being reinvested at the expense of near-term margins. TSLA initially +4% after hours, then reversed.

Thursday Cash Session (Day 40 Close)

Thursday’s curve settled in a BEAR FLATTENER — the hawkish front-end repricing continued: 2Y +2.8 bps to 3.832%, 5Y +2.6 bps to 3.955%, 10Y +2.0 bps to 4.325%, 30Y +0.4 bps to 4.914%. The front end rising faster than the long end reflects sustained hawkish pricing from the Retail Sales beat + Warsh hearing + Claims slightly above expectations. Thursday’s Claims at 8:30 AM: 214K for the week ending April 18, vs 210K consensus, prior revised to 208K. This is the FIRST post-tariff Claims print — the week ending April 18 is the first that could plausibly contain tariff-driven layoff filings. The slight miss (+4K above consensus) is modest — well within normal weekly variation and NOT indicating a tariff shock in the labor market. The 4-week moving average remains healthy.

Asia-Pacific

Nikkei +1.43% to 59,845 — Japan’s second consecutive strong rally, driven by SOXX semis broadening and the frozen-conflict de-escalation trade. The Nikkei is now at its highest level since before the war’s ceasefire collapse. Topix −0.09% — the Nikkei-Topix divergence persists (concentrated export-tech vs broad domestic).

Europe

DAX −0.07% to 24,305 essentially flat. EuroStoxx 50 −0.15% to 5,844. Europe continues soft in the frozen-conflict framework — the sustained blockade with WTI at $95.79 keeps European energy costs elevated. Brent’s dramatic −5.51% decline to $99.28 is a notable development — potentially reflecting expectations of diplomatic progress or shadow-fleet supply leakage past the blockade. UK Retail Sales this morning beat at +0.7% vs 0.0% consensus — the UK consumer is strong, consistent with the US Retail Sales blowout from Tuesday.

US Pre-Market

Day 57 of Operation Epic Fury. Q2 Day 18. Friday — last trading day of the week. FOMC blackout active.

US FUTURES DIVERGENT: NQ 27,248.50 (+1.17% — LEADING), ES 7,165.25 (+0.30%), RTY 2,796.40 (+0.37%), YM 49,418 (−0.15% — Dow the ONLY red index). The NQ-Dow divergence (+1.17% vs −0.15% = 132 bp spread) is the widest of the week and tells you this is a TECH-SEMIS rally, not a broad cyclical bid. The Dow’s weakness reflects TSLA −3.56% (Dow component via inclusion weight) and CAT positioning.

MAG 7 TWO GREEN / FIVE RED: AAPL +0.10% (barely green — Apple stabilizing after the multi-session weakness). GOOG +0.01% (essentially flat). AMZN −0.11%. NVDA −1.41% (semis rally bypassing NVDA for broadening names). META −2.31%. TSLA −3.56% (capex-raise reversal). MSFT −3.97% (the worst Mag 7 — pre-positioning into April 29 earnings, NOT a Thursday earnings reaction as MSFT actually reports April 29). The Mag 7 at 2 green / 5 red for the fourth session in five is now a sustained pattern — the non-Mag 7 market is carrying the index.

SECTORS — EXTREME BIFURCATION: XLU +2.72% LEADING (utilities — the most dramatic utilities bid of the war, driven by defensive rotation + MOVE compression + lower long-end yields). XLI +1.77%. XLP +1.67%. XLRE +1.15%. XLE +0.78%. Five sectors green, six red. XLK −1.42% (tech LAGGING despite NQ +1.17% — the divergence is SOXX semis driving NQ while broad XLK pulls back on MSFT/META weakness). XLY −1.00%. XLF −0.79%. XLC −0.42%. The defensive/cyclical leadership (XLU/XLI/XLP) with tech lagging is the clearest ‘late-cycle rotation’ signal of the post-ceasefire period.

FACTORS DEFENSIVE: SPLV +1.50% LEADING (low-vol at the top of the factor stack). VYM +0.65%. VLUE +0.50%. DGRO +0.32%. USMV +0.23%. SPHB −0.97% (high beta at the BOTTOM). USMV-SPHB spread +1.20% (DEFENSIVE — the widest positive spread since the weekend-risk session). QUAL −0.62%. LRGF −0.70%. 5/12 factors green but all greens are defensive/income names. This is an unambiguously defensive factor rotation.

SOXX +2.14% — the standout thematic. Semis broadening beyond NVDA. PAVE +2.21% (infrastructure — frozen-conflict supply-chain investment theme). ICLN +1.46%. ITA −0.02% essentially flat (defense stabilizing after two sessions of cratering). ARKW −3.08%. FINX −3.87%. ARKG −3.50%. Every ARK/innovation thematic deeply red — the rotation is INTO old-economy/defense/infrastructure and OUT of high-growth/innovation.

3. THE PRIOR DAY’S REGIME (34 Macro Price, Strength & Momentum Rankings)

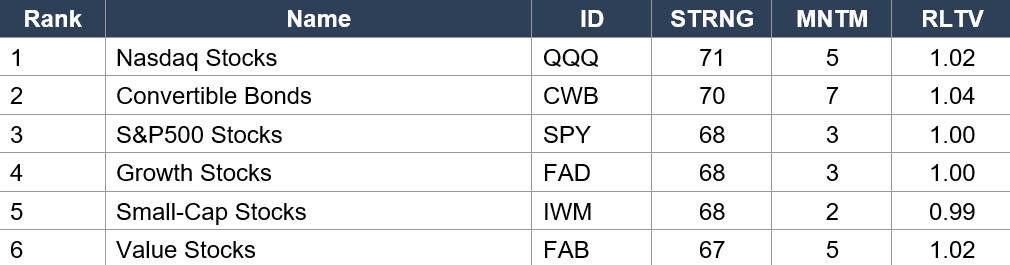

34 Macro Price, Strength & Momentum Rankings — Daily Close, Thursday April 23. SPY Baseline: STRNG 68 | MNTM +3 | RLTV 1.00.

Asset Classes — Leaders

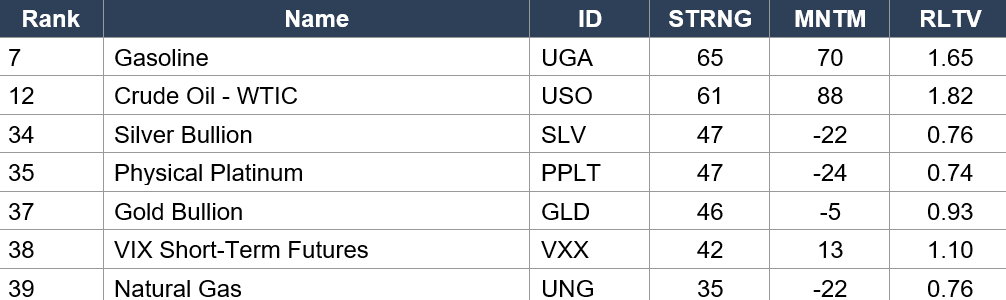

Asset Classes — Energy Explosion / Metals Collapse

Regime signal: QQQ (rank 1, STRNG 71) holds #1 for a fourth consecutive data set — Nasdaq leadership structural. CWB (rank 2, RLTV 1.04) holds #2 — credit risk-appetite confirmed. IWM (rank 5) slipped from rank 2 with MNTM cooling from 5 to 2 — small-cap momentum fading slightly. ENERGY EXPLOSION CONTINUES: Crude Oil (USO MNTM +88, RLTV 1.82!!!) — momentum ACCELERATED AGAIN from +78 to +88. This is now the most extreme single-asset momentum reading in the HISTORY of the 34 Macro data series. RLTV at 1.82 means crude is outperforming the market by 82% on a relative basis. Gasoline (UGA MNTM +70, RLTV 1.65). The energy-momentum extreme reflects WTI’s rally from $81 Friday crash to $95.79 (+18% in four sessions). PRECIOUS METALS COLLAPSING FURTHER: Silver (SLV MNTM −22, RLTV 0.76), Platinum (PPLT −24, 0.74), Gold (GLD −5, 0.93). The precious-metals liquidation is the cleanest ‘safe-haven unwind’ of the war — the ceasefire extension removed urgency and the frozen-conflict framework does not support haven demand. VIX (VXX MNTM +13, RLTV 1.10) — fear momentum remains positive, confirming the defensive rotation in the factor tape.

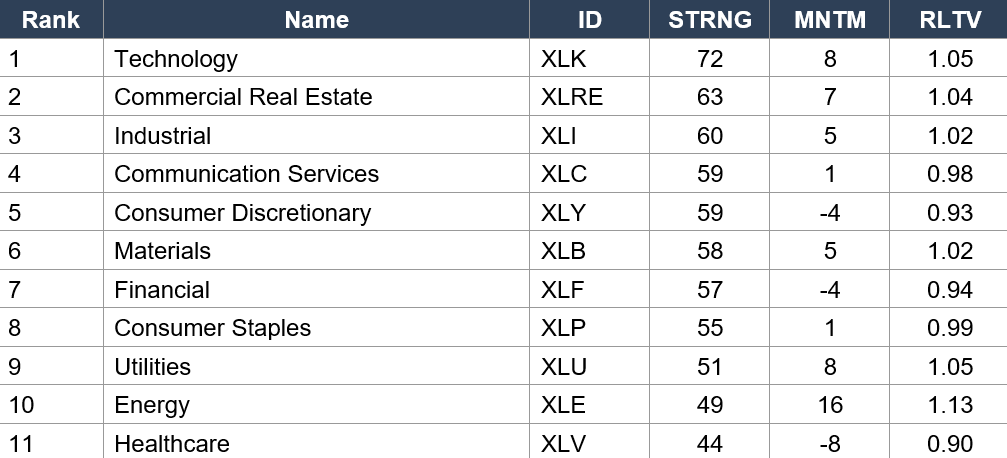

Sector ETFs — Full Ranking

Regime signal: Technology (XLK rank 1, STRNG 72, RLTV 1.05) holds #1 sector for the third consecutive data set since dethroning XLRE. XLRE (rank 2, STRNG 63, RLTV 1.04) stabilized after the Wednesday −1.93% crash — RLTV at 1.04 says it is still outperforming the market. Industrial (XLI rank 3, STRNG 60, RLTV 1.02) climbed to Leaders — the frozen-conflict infrastructure investment thesis is being captured. Utilities (XLU rank 9, MNTM +8, RLTV 1.05) — the HIGHEST RLTV alongside XLK at 1.05 — utilities catching a massive bid on the MOVE compression and the defensive rotation. Today’s +2.72% XLU pre-market will extend this further. ENERGY (XLE rank 10, MNTM +16, RLTV 1.13 — still the HIGHEST RLTV of any sector for the FOURTH consecutive data set). The energy Phoenix trade continues. Health-Care (XLV rank 11, MNTM −8, RLTV 0.90 — still the WEAKEST sector despite Tuesday’s UNH beat). Consumer Discretionary (XLY rank 5, MNTM −4, RLTV 0.93) — TSLA capex-raise dragging the sector.

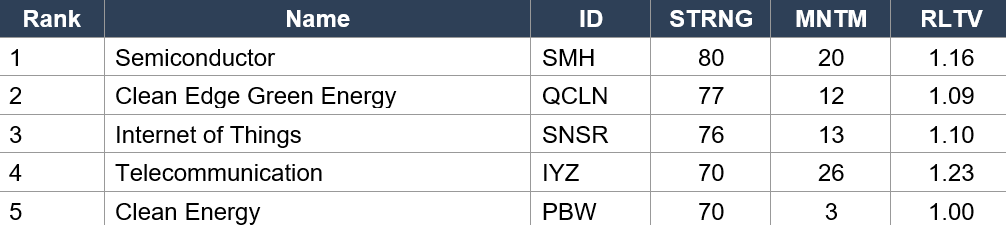

Industry ETFs — Top Leaders

Industry ETFs — Notable Shifts

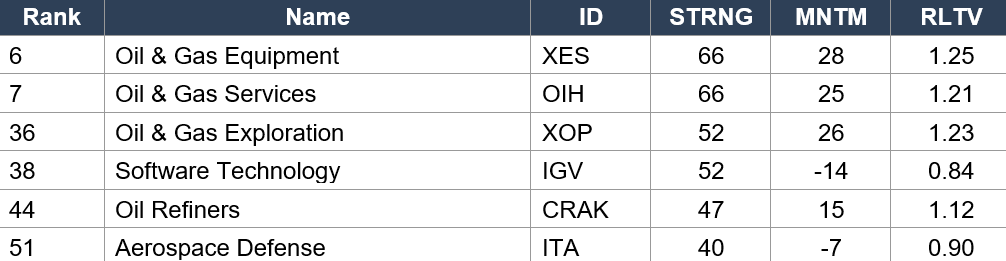

Regime signal: Semiconductor (SMH rank 1, STRNG 80 — HIGHEST STRNG IN THE ENTIRE WAR ACROSS ALL DATA SETS, MNTM +20, RLTV 1.16) holds #1 industry for the FIFTH consecutive data set. STRNG at 80 is a NEW ALL-TIME WAR HIGH for any single asset in any Quiggle/34 Macro data set. The semis broadening trade (SOXX +2.14% today via AMD/AVGO/MU rather than NVDA) is structural. Telecom (IYZ rank 4, MNTM +26, RLTV 1.23 — highest RLTV of any industry) continues its structural leadership — the defensive-growth hybrid is the perfect frozen-conflict positioning. CRITICAL: Software Technology (IGV rank 38, MNTM −14, RLTV 0.84) DEEPENED its collapse — from 0.87 to 0.84. IGV is now in the Laggers category. The software recovery that peaked at RLTV 1.09 on April 17 has fully broken and is getting WORSE. MSFT’s −3.97% today pre-April-29 will deepen this further. Energy value chain: XES (1.25), OIH (1.21), XOP (1.23) — all above 1.20 RLTV for the second consecutive set. Aerospace-Defense (ITA rank 51, MNTM −7, RLTV 0.90) — defense at the BOTTOM of the entire industry ranking. The frozen-conflict framework is the worst possible scenario for defense stocks: no combat = no urgency premium.

4. MORNING DATA REACTION

10:00 AM — REVISED UNIVERSITY OF MICHIGAN CONSUMER SENTIMENT APRIL. Consensus 48.5. Prior 47.6 (All-Time Record Low In 74-Year Survey History). The Most Important Sentiment Read Of The War.

The revised Michigan Sentiment print at 10 AM is the session’s dominant data event. The preliminary April reading of 47.6 on Day 31 (April 10) was the ALL-TIME RECORD LOW in the survey’s 74-year history, eclipsing the mid-2022 low during the inflation crisis. That print combined with CPI gasoline +21.2% and 1-year inflation expectations jumping from 3.8% to 4.8% (largest one-month leap ever) defined the war’s ‘peak consumer stress’ narrative. Today’s revised reading captures two additional weeks of consumer attitudes — including the ceasefire extension and the oil crash-to-$81-and-recovery. If revised UP from 47.6 toward the 48.5 consensus, it would signal peak consumer stress is behind us and support the bifurcation thesis. If revised DOWN below 47.6, it would set a new all-time low for the second consecutive month and challenge the ‘strong consumer’ narrative from Tuesday’s Retail Sales beat.

Thursday 8:30 AM — INITIAL JOBLESS CLAIMS: 214K (vs 210K consensus, prior revised to 208K). FIRST POST-TARIFF PRINT. Slight Miss But Well Within Normal Range.

Claims rose 6K from the prior week to 214K, slightly above the 210K consensus. This is the first weekly claims print that could plausibly contain tariff-driven layoff filings (week ending April 18). The slight miss is NOT alarming — 214K remains well within the historically healthy 200K-250K range and does not indicate a tariff shock to the labor market. The 4-week moving average remains constructive. However, the direction (rising from 207K → 208K → 214K over the past three weeks) warrants monitoring. If next week’s print continues the upward trajectory above 220K, the labor-market narrative shifts from ‘structurally tight’ to ‘emerging softness.’ For now, the claims data is neutral — not strong enough to add to the hawkish front-end repricing, not weak enough to trigger dovish pivot expectations.

Wednesday After Close — TESLA Q1 2026: Adjusted EPS $0.41 vs $0.37 Est (+10.8% Beat). Revenue $22.39B vs $22.35B. Auto Gross Margin 19.2%. Energy Storage Margin 39.5% (Record). FCF $1.4B. BUT — 2026 Capex Raised To $25B From $20B. Stock Initially +4% Then Reversed. TSLA −3.56% Thursday.

Tesla’s Q1 was a strong operational quarter: 52% non-GAAP EPS growth YoY ($0.41 vs $0.27), total revenue +16% YoY to $22.39B, auto gross margin improving 290 bps YoY to 19.2% (from the trough of 16.3% in Q1 2025), energy storage margins hitting a record 39.5%, free cash flow of $1.4B (+117% YoY), cash position growing to $44.7B. The beat is clean. But the $5B capex increase ($25B from $20B guidance) was the market’s focus — capex jumped 67% in Q1 alone to $2.49B. The market read this as: Tesla is reinvesting its earnings improvement into AI/autonomy/robot infrastructure at the expense of near-term shareholder returns. Musk calling Optimus ‘probably the biggest product ever’ on the call signaled the strategic shift. TSLA at −3.56% is the ‘beat and invest forward’ trade — identical in structure to NFLX’s ‘beat and guide lower’ pattern from last week.

CALENDAR CORRECTION: MSFT, GOOGL, META Report April 29 — NOT April 23. The DYRH Had This Wrong. April 29 = FOMC + Powell Press + MSFT/GOOGL/META Earnings. The Most Concentrated Single-Day Event Calendar Of The Entire War.

Per Microsoft’s own investor relations page, MSFT fiscal Q3 reports after market close on Wednesday April 29. Multiple sources confirm GOOGL and META also report April 29. The DYRH listed all three as April 23 (Thursday) — this is incorrect. The correction is critical: April 29 is ALSO the FOMC statement day + Powell press conference. FOMC statement at 2 PM + Powell press 2:30 PM + MSFT/GOOGL/META after close = the most concentrated single-day event calendar of the entire 57-day war. The market has five calendar days to position for this convergence.

5. THE DYRH READ

Regime: Mixed / Indeterminate — Risk-On — Energy Steady. MOVE reversed to 67.70 (−3.12%) — the bond market’s capitulation held after three sessions of expansion. Factor tape defensive (USMV-SPHB +1.20%). NQ +1.17% leading on SOXX semis broadening. Dow −0.15% lagging. Five sectors green (defensive/cyclical leaders: XLU +2.72%, XLI +1.77%, XLP +1.67%). Six sectors red (tech, consumer, financials). Claims 214K — first post-tariff print, slight miss but not alarming. Michigan revised sentiment 10 AM — the most important sentiment read of the war. TSLA beat but reversed on $25B capex raise. MSFT/GOOGL/META actually April 29 (FOMC day). Frozen conflict continues. Confidence: MODERATE-HIGH — MOVE compression is bullish but defensive factor rotation and narrow NQ leadership complicate the read.

Yield Curve: Mixed / Indeterminate — 2Y +0.4 bps to 3.836%, 10Y −0.3 bps to 4.322%, 30Y Flat at 4.914%. The Front End Is Rising On Hawkish Repricing. The Long End Is Stable.

The curve is no longer clean bull or bear — it is mixed/indeterminate. 2Y rising (+0.4 bps) reflects the cumulative hawkish repricing from Retail Sales beat + Claims slight miss + Warsh hearing tone. 10Y falling (−0.3 bps) reflects residual long-end growth pessimism from the frozen-conflict framework. 5Y and 30Y flat. The Thursday bear flattener (2Y +2.8 bps leading all tenors) has modestly eased into Friday. The 2Y at 3.836% is the highest since mid-April — the market has fully priced out near-term rate-cut expectations. This puts pressure on the April 29 FOMC to either validate the market’s hawkish repricing (hold with hawkish tone) or push back (hold with dovish lean) — either way, the FOMC is a binary for the front end.

MOVE 67.70 (−3.12%) — Reversed From 70.78 Peak. The Three-Session Expansion Was A Positioning Event, Not A Regime Reversal. Bond Market Capitulation Intact.

MOVE at 67.6962 is the most bullish cross-asset signal this morning. The trajectory: 65.70 → 67.90 → 70.78 → 67.70. The expansion to 70.78 on Wednesday (approaching the 73.21 baseline) was driven by ceasefire-expiration positioning, Warsh hearing uncertainty, and Retail Sales hawkish repricing. The compression back to 67.70 says: those catalysts have been absorbed. The ceasefire was extended, Warsh hearing passed without shock, and the Retail Sales beat is priced. MOVE at 67.70 is 5.51 points below pre-war baseline — the widest sub-baseline margin since Thursday April 16. If MOVE holds sub-70 through Friday close, the market enters the April 29 FOMC/mega-earnings convergence from a position of rates-vol comfort.

ES 7,165.25 (+0.30%) — Constructive. +4.1% Above Pre-War Baseline. But Narrow NQ Leadership And Defensive Factor Tape Create A Complex Read.

ES at +0.30% is green but the internal structure is complex: NQ +1.17% (SOXX-driven semis broadening) while Dow −0.15% (TSLA/cyclical drag). Factor tape 5/12 green but all greens are defensive (SPLV, VYM, VLUE, DGRO, USMV). SPHB −0.97% at the bottom. The breadth numbers from Thursday’s close are strong (S5FD 89.40, R2FD 85.10, S5TW 72.80 — all expanding) but the Friday pre-market factor tape contradicts the breadth data. The market is in the middle of a rotation FROM growth/momentum/high-beta TO value/low-vol/income — the classic ‘late-rally’ rotation that can either extend the rally via broadening or presage a top via leadership exhaustion.

WTI $95.79 — Oil Has Rallied +18% From The Friday $81 Crash In Four Sessions. Brent −5.51% — The Brent Crash Is The Session’s Wildcard.

WTI at $95.79 (−0.06%) is essentially flat Friday after rallying from $81 (Friday crash close) → $85.89 (Monday) → $87.52 (Tuesday) → $90.80 (Wednesday) → $95.79 (Thursday close) — an 18% four-session rally that has fully reversed the Friday de-escalation crash and then some. WTI is now ABOVE the pre-weekend $94 level. Brent at $99.28 (−5.51%) is the session’s wildcard — the most dramatic single-session Brent decline since the Day 29 ceasefire announcement. The Brent-WTI spread has narrowed from ~$8 to ~$3.50 — the tightest of the war. The Brent crash may reflect shadow-fleet supply leakage past the blockade (Senator Murphy cited reports of 28+ shadow ships bypassing the blockade), or expectations of diplomatic progress, or simply a technical correction after Brent approached $105.

6. THE GAME PLAN

Today’s Key Events: Michigan Revised Sentiment 10 AM (consensus 48.5, prior 47.6 all-time record low). PG, Colgate-Palmolive pre-market. NEXT WEEK: TUESDAY APRIL 29 — FOMC statement 2 PM + Powell press conference 2:30 PM + MSFT/GOOGL/META after close. THE MOST CONCENTRATED SINGLE-DAY EVENT CALENDAR OF THE ENTIRE WAR. PCE April 30. Housing Starts + ISM Manufacturing May 1.

The Bull Case:

MOVE reversed to 67.70 — bond market capitulation held, 5.51 points sub-baseline. NQ +1.17% on SOXX +2.14% semis broadening. Nikkei +1.43%. ES +4.1% above pre-war. TSLA beat Q1 cleanly ($0.41 vs $0.37). Strong breadth (S5FD 89.40, R2FD 85.10 — both expanding). Ceasefire extended indefinitely. Claims 214K within normal range. Seven consecutive data beats (PPI/Empire/Philly/Claims Apr 16/Retail/UNH/TSLA). Brent crash may signal easing supply constraints. PAVE +2.21% infrastructure bid. XLU +2.72% utilities rally on MOVE compression. 34 Macro shows SMH STRNG 80 (new all-time war high). If Michigan revised UP toward consensus, peak consumer stress is confirmed as behind us. April 29 FOMC/mega-earnings convergence gives the market five days to position for the defining binary.

The Bear Case:

Factor tape DEFENSIVE — USMV-SPHB +1.20% (widest positive since weekend-risk session). SPLV leading. SPHB at the bottom. Mag 7 at 2 green / 5 red for the fourth time in five sessions — sustained tech weakness. MSFT −3.97%, META −2.31%, TSLA −3.56% — three of the most important names deeply red. TSLA ‘beat and invest forward’ on $25B capex raise is the war’s latest warning for earnings season: strong Q1 does not mean shareholder-friendly guidance. IGV RLTV crashed to 0.84 (from 1.09 peak — software recovery fully broken). Claims rose to 214K — first post-tariff print trending higher (207→208→214). ARK/innovation thematics deeply red (ARKW −3.08%, ARKG −3.50%, FINX −3.87%). The defensive rotation (XLU/XLP/XLI leading, XLK/XLY/XLF lagging) is the classic ‘late-rally’ signal. VXX RLTV 1.10 — fear outperforming the market. Oil rallied 18% in four sessions — if the blockade maintains, $100 WTI returns and the inflation narrative re-engages. April 29 FOMC + mega-earnings concentration is the most extreme single-day event risk of the war — five days of pre-positioning could produce de-leveraging rather than accumulation.

Regime: Mixed / Indeterminate — Risk-On — Energy Steady. The market enters Friday in a bifurcated state: MOVE compression says risk-on (bond market comfortable), factor tape says defensive (equity market cautious), NQ leadership says semis-driven (narrow), and the sector rotation says late-cycle (XLU/XLP leading, XLK lagging). The resolution comes April 29 — the most concentrated single-day event calendar of the entire war: FOMC statement + Powell press + MSFT/GOOGL/META earnings. Five calendar days of positioning into that convergence begin today. Michigan sentiment at 10 AM is the immediate catalyst. If revised UP, the bifurcation thesis gets its final confirmation and the market enters April 29 from strength. If revised DOWN to a new all-time low, the consumer-stress narrative re-engages and the defensive rotation intensifies.

Watch List

Michigan Revised Sentiment 10 AM — Peak Consumer Stress Test

Consensus 48.5 vs prior 47.6 (all-time record low). A revision to 48-49 confirms peak stress was the preliminary April print. A revision below 47.6 sets a new all-time low for the second consecutive month. The 1-year inflation expectations component (4.8% preliminary) is equally critical — any revision above 5.0% would be the highest since the early 1980s.

April 29 Convergence — FOMC + Powell + MSFT/GOOGL/META

The market has five calendar days to position. FOMC statement at 2 PM (consensus: hold, with hawkish lean given Retail Sales/Claims). Powell press at 2:30 PM (key question: does the Fed ‘look through’ the war-inflation shock or signal concern about inflation expectations?). MSFT fiscal Q3, GOOGL Q1, META Q1 after close. If all three deliver: equities extend into a structural bull market. If any disappoints: the narrow NQ-driven rally breaks and the defensive rotation accelerates.

Brent Crash — Supply Constraint Easing Or Technical?

Brent −5.51% to $99.28 while WTI −0.06% is a dramatic divergence. If the Brent crash reflects shadow-fleet supply bypassing the blockade (Murphy cited 28+ ships), the war premium in oil begins structurally compressing regardless of the diplomatic outcome. If it’s technical, Brent bounces Monday and the frozen-conflict energy premium remains.

TSLA ‘Beat And Invest Forward’ Read-Through To Mega Earnings

If TSLA’s $25B capex raise pattern repeats in MSFT (Azure capex), GOOGL (AI capex), or META (Reality Labs capex), the April 29 mega-earnings day could produce the same ‘beat but reverse on spend guidance’ dynamic across all three names simultaneously. The AI capex cycle is the defining tension of 2026 earnings: strong top-line growth being reinvested at the expense of near-term margins.

Morning check: Day 57. The war is fifty-seven days old. MOVE reversed to 67.70 — the bond market’s capitulation held. The three-session expansion toward the 73.21 baseline was a positioning event, not a regime reversal. Tesla beat Q1 ($0.41 vs $0.37) but stock reversed −3.56% on a $25B capex raise. The DYRH had MSFT/GOOGL/META reporting Thursday — they actually report April 29, which is also FOMC day + Powell press conference. That makes April 29 the most concentrated single-day event calendar of the entire war. The factor tape turned defensive: SPLV leading, SPHB at the bottom, USMV-SPHB +1.20%. The sector tape shows late-cycle rotation: XLU +2.72%, XLI +1.77%, XLP +1.67% leading while XLK −1.42%, XLY −1.00% lag. NQ +1.17% on SOXX +2.14% semis broadening — SMH STRNG 80 is a new all-time war high. Claims 214K — first post-tariff print, slight miss but not alarming, trending higher (207→208→214). Michigan revised sentiment at 10 AM — consensus 48.5 vs the 47.6 all-time record low. Gold failing to rally on dollar weakness — the day’s most important divergence per the DYRH. The frozen conflict continues: ceasefire extended indefinitely, blockade active, no talks scheduled. Five days to position for April 29. Take the MOVE compression as the floor. Respect the defensive factor rotation as the ceiling. And remember: April 29 resolves everything — Fed path, mega-cap fundamentals, and the war’s market legacy — in a single session.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.