☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: The pro-cyclical recovery that began yesterday is under immediate stress. Oil has BROKEN OUT of the $73–76 stabilization range: WTI +3.00% to $76.90, Brent +2.29% to $83.27, heating oil +5.14%. The energy ceiling has been breached. Bond selling is ACCELERATING into its sixth consecutive session: ZB −0.61% is the sharpest pre-market long bond selloff in the DYRH series. 10Y at 4.136% (+18.7 bps cumulative from Friday). All US futures red: ES −0.34%, NQ −0.43%, RTY −0.88%. Sector rotation has flipped back to stagflation: XLE the only green sector, XLY (yesterday’s leader at +1.78%) is now the worst performer (−0.66%). All Mag 7 red in pre-market. Dollar reversing higher to 99.025 (+0.25%). VIX bouncing to 21.88 (+3.45%). But this is NOT a return to the acute liquidation regime — the pullback is orderly. ES is only giving back 0.34% after yesterday’s +0.78% gain. The key question: was yesterday’s regime transition durable, or was it a one-day relief rally?

The Number That Matters: WTI at $76.90 — up 3.00% overnight and back above the $73–76 “manageable war premium” range that anchored yesterday’s bullish thesis. The two-day energy stabilization is over. Brent at $83.27 is pushing toward $85, the threshold where the inflation impulse becomes economically significant. If WTI breaks $80, the entire “war premium is contained” narrative collapses. Cumulative: WTI is now up $9.88 (+14.7%) from Friday’s $67.02. Heating oil +5.14% and gasoline +3.14% confirm refined product tightness is intensifying. The overnight war escalation is the driver: Iran struck Azerbaijan (geographic expansion to new countries), death toll at 1,230+, threats to target “all economic centres in the region.”

The Setup: The regime is being stress-tested. Yesterday’s strong ADP (+63K) and ISM Services (56.1, highest since July 2022) killed the growth-scare narrative and triggered the first green close since the war began. But overnight, oil’s breakout and accelerating bond selling are re-introducing the stagflation impulse. The sector rotation has flipped 180 degrees in 12 hours — from pro-cyclical (XLY leading, XLE lagging) to stagflation (XLE leading, XLY lagging). Three outcomes to watch today: (A) oil pulls back, claims benign, equities recover → recovery confirmed; (B) oil pushes through $78–80, claims spike, equities close red → stagflation reasserts; (C) oil stabilizes $76–78, equities chop near flat → market in transition, pending tomorrow’s NFP for resolution.

2. OVERNIGHT SESSION RECAP

Asia-Pacific

TOPIX +0.79% — Japan green but well off yesterday’s +3.77%. Nikkei (USD) −1.54%, sharply diverging from TOPIX. Korea’s KOSPI still digesting Tuesday’s approximately −12% crash (worst day on record per Reuters). The Japanese bounce is decelerating.

Europe

DAX −0.46%, Euro Stoxx 50 −0.51%. Europe giving back after Wednesday’s recovery. The overnight oil re-acceleration is hitting European equities harder given direct energy import dependence. Bessent’s 15% global tariff expected to take effect today or tomorrow — EU expects exemption but uncertainty is weighing.

US Pre-Market

Operation Epic Fury — Day 6. No de-escalation. Iran death toll now 1,230+ (up from 1,045 yesterday). Fresh strikes across Tehran, Karaj, Isfahan overnight. MAJOR: Iran struck Azerbaijan’s Nakhchivan International Airport — geographic expansion to new countries. Iran warned it will target “all economic centres in the region” if attacks continue. Khamenei’s mourning ceremony postponed — regime struggling. Israel warned any successor would be “an unequivocal target for elimination.” US told Americans to avoid Cyprus. Italy considering deploying destroyer. Turkey/NATO intercepting Iranian ordnance. CRITICAL: Reports that Iranian operatives reached out to the US to explore potential PEACE TALKS — first diplomatic feeler since the war began. Unconfirmed but market-moving if validated.

Prior session (March 4 close): The first green close since the war began. S&P +0.78%, Nasdaq +1.29%, Dow +0.49%. ADP +63K (beat 48K est; January revised DOWN to 11K from 22K). ISM Services 56.1 (highest since July 2022, vs. 53.5 est). MOVE collapsed to 70.03 (below pre-war 73.21) — rates volatility crisis definitively ended. VIX −10.27% to 21.15. COR1M −19.72% to 17.95. Breadth snapped higher: R2FD +56%, S5FD +13%. SPHB-USMV spread −169 bps (widest risk-on signal in series). All 11 thematics green for first time.

Today’s data: Challenger Job Cuts (February) at 7:30 AM. Initial Jobless Claims at 8:30 AM (expected 215K vs. prior 212K) — HIGH IMPACT: first weekly claims data since war began, will be scrutinized for early war-related disruption. Trade Balance and Import/Export Prices at 8:30 AM. Factory Orders at 10:00 AM. Natural Gas Storage at 10:30 AM. TOMORROW: February Non-Farm Payrolls at 8:30 AM — THE main event of the week.

CrowdStrike (CRWD) reported after hours Tuesday: beat on revenue ($1.31B, +23% YoY) and EPS ($1.12 vs. $1.10 est), record $331M net new ARR (+47% YoY), but stock fell approximately 4% on forward guidance concerns. Kroger, Costco, and Marvell report today.

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 03/04/26. Provided for informational purposes only; not as investment advice.

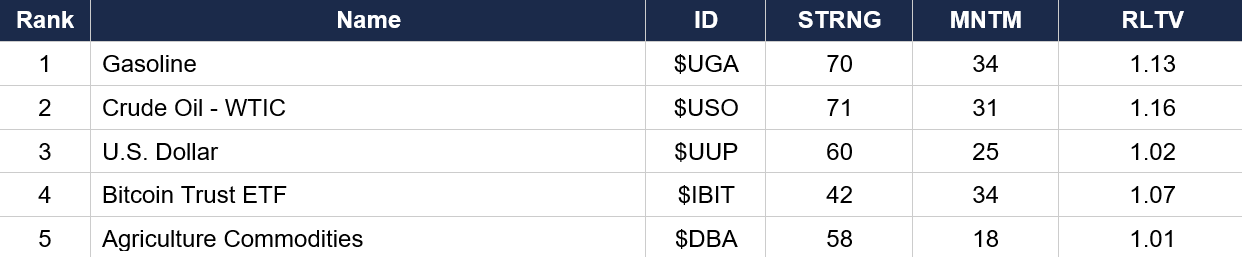

Asset Classes — Top 5

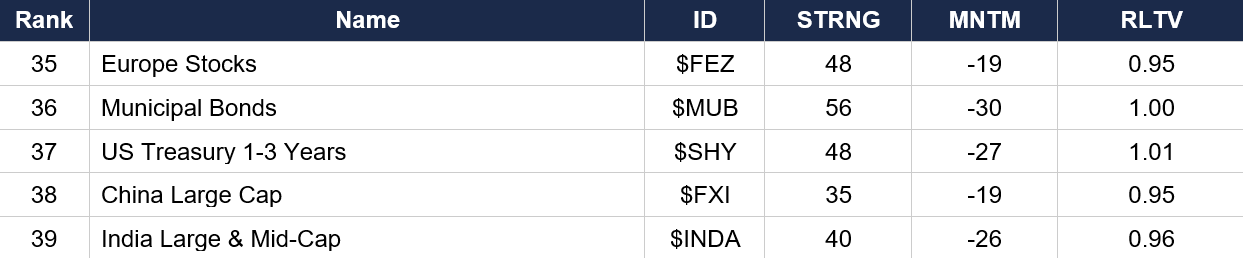

Asset Classes — Bottom 5

Regime signal: Gasoline has overtaken crude oil for the #1 rank (MNTM 34) — the refined products tightness signal is dominating. The dollar holds rank 3 but MNTM has decelerated slightly to 25. Bitcoin ($IBIT) has SURGED to rank 4 with MNTM 34 (tied for highest on the board) — crypto is now a top-5 asset class, reflecting yesterday’s +7.27% BTC surge. Agriculture ($DBA) at rank 5 with MNTM 18 — supply chain disruption is lifting the ag complex. Gold has FALLEN to rank 9 (MNTM 1) — essentially zero momentum, confirming its failure as a war hedge (cumulative −3.3%). VIX ($VXX) slipped to rank 14 from rank 4 (MNTM −2) after yesterday’s −10% VIX crush. TIPS at rank 18 with MNTM −14 — collapsed from rank 5, as real yields rise. S&P ($SPY rank 11, MNTM 6) and Nasdaq ($QQQ rank 7, MNTM 15) have JUMPED on yesterday’s rally. Japan ($EWJ, MNTM −23) and Emerging Markets ($EEM, MNTM −20) remain deeply negative. Municipal Bonds ($MUB, MNTM −30) is the worst momentum on the board — muni selling extreme.

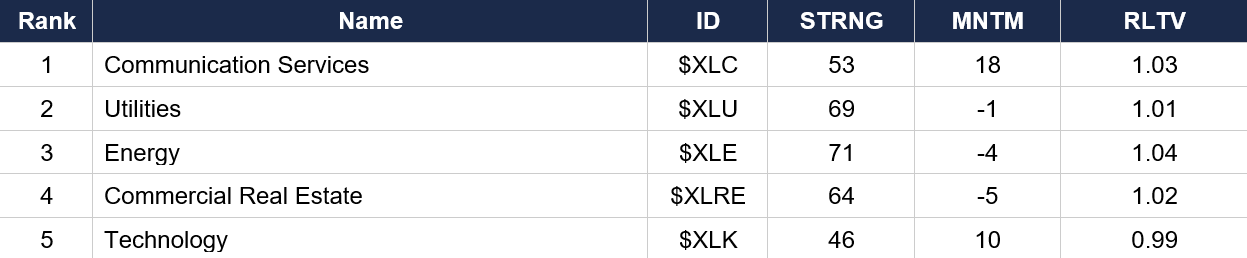

Sector ETFs — Top 5

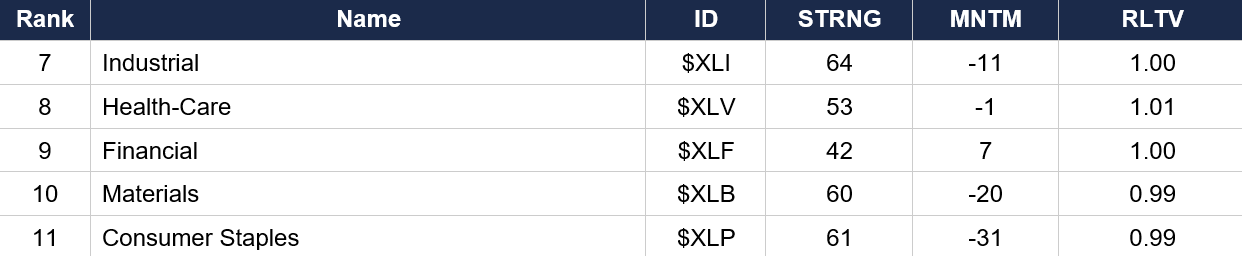

Sector ETFs — Bottom 5

Regime signal: Communication Services ($XLC) has SEIZED rank 1 with MNTM 18 — the highest sector momentum on the board. This is a major shift: a growth/cyclical sector now leads. Technology ($XLK) at rank 5 with MNTM 10 confirms the tech recovery from yesterday’s +1.70% session. Consumer Discretionary ($XLY) at rank 6 with MNTM 12 — strong momentum despite being today’s worst pre-market sector. Energy ($XLE) holds rank 3 but MNTM remains at −4 — the energy equity trade continues to fade in rankings even as crude surges. Consumer Staples ($XLP, MNTM −31) is by far the worst sector momentum — defensive staples are in freefall. Materials ($XLB, MNTM −20) second worst. Industrial ($XLI, MNTM −11) deteriorating.

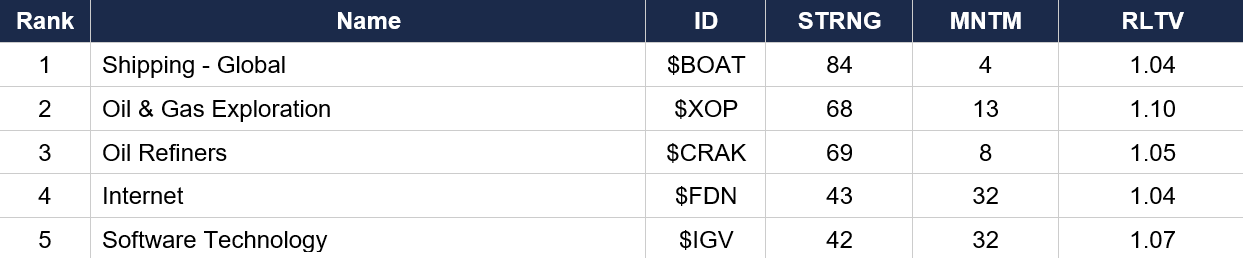

Industry ETFs — Top 5

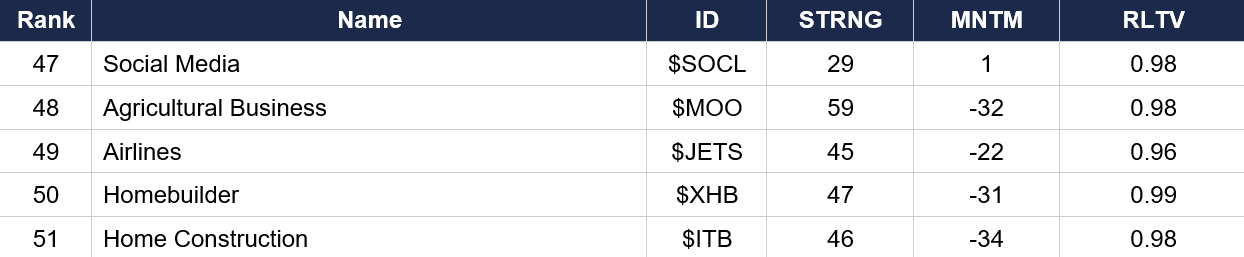

Industry ETFs — Bottom 5

Regime signal: Internet ($FDN, MNTM 32) and Software ($IGV, MNTM 32) share the HIGHEST industry momentum on the board — the tech/internet recovery from yesterday’s rally is generating extreme momentum readings. Oil Refiners ($CRAK) have entered the top 3 at rank 3 (MNTM 8) — the crack spread widening is lifting refinery margins. Aerospace-Defense ($ITA) at rank 7 with MNTM 9 — defense has stabilized. Mobile Payments ($IPAY, MNTM 22) at rank 11 is a notable fintech signal. Homebuilders ($XHB, MNTM −31) and Home Construction ($ITB, MNTM −34) remain the worst industry momentum — rising rates and energy costs devastating housing. Agricultural Business ($MOO, MNTM −32) second worst. Banking ($KBE, MNTM −14) and Regional Banks ($KRE, MNTM −17) continue to lag.

4. MORNING DATA REACTION

Yesterday’s data dominated the session: ADP National Employment Report (released Wednesday, March 4): +63K (vs. approximately 48K expected). January revised DOWN to 11K from 22K. The beat was led by education/health services (+58K) and construction (+19K), with hiring concentrated in just two sectors. Manufacturing lost 5K. Small businesses created 60K of the total. The headline beat expectations but breadth was narrow.

ISM Services PMI (released Wednesday, March 4): 56.1 (vs. 53.5 expected, prior 53.8) — the highest since July 2022 and the 20th consecutive month of expansion. Business Activity surged to 59.9 (from 57.4). New Orders jumped to 58.6 (from 53.1). Employment improved to 51.8. Prices DECLINED to 63.0 (from 66.6). The combination of strong activity with declining price pressure was the ideal soft-landing print — growth accelerating while inflation moderates. This killed the stagflation narrative for a day.

Today: Initial Jobless Claims at 8:30 AM (expected 215K vs. prior 212K) — the first weekly claims data since the war began. A spike above 225K could reignite growth fears; at/below 215K confirms labor market resilience. Trade Balance, Import/Export Prices also at 8:30 AM. Factory Orders at 10:00 AM. Natural Gas Storage at 10:30 AM (expected −122B draw vs. prior −52B). TOMORROW: February Non-Farm Payrolls at 8:30 AM — the main event of the week.

Friday’s PPI (released February 27) showed final demand +0.5% MoM with Core PPI +0.3% for the ninth consecutive increase. Monday’s ISM Manufacturing (released March 2) held expansion at 52.4 with Prices Paid surging to 70.5 (highest since mid-2022). The inflation pipeline was already hot before the war. Yesterday’s ISM Services Prices decline to 63.0 from 66.6 was a rare counterpoint.

5. THE DYRH READ

Regime: Recovery Under Stress Test — Oil Re-Acceleration Challenging Pro-Cyclical Pivot, Stagflation Dynamic Re-Emerging. Confidence: Moderate on characterization. Low-Moderate on recovery sustainability.

Yield Curve: Bear Steepening Accelerating — Sixth Straight Session. 10Y at 4.136% (+18.7 bps cumulative from Friday). ZB −0.61% is the sharpest pre-market long bond selloff in the series. The 5Y belly is leading (+5.1 bps) with the 2Y catching up (+4.2 bps) as “no rate cuts” solidifies from strong data. 30Y at 4.755% (+2.2 bps). Triple headwind for bonds: strong economic data (eliminating rate cut hopes) + oil re-acceleration (adding inflation expectations) + 15% tariff imminent (further inflation impulse). Watch MOVE at the open — yesterday it collapsed to 70.03 (below pre-war 73.21). If MOVE stays below 73 despite the bond selling, the repricing is orderly. If MOVE spikes above 75, the rates volatility crisis is re-engaging.

Commodity Complex — Oil Breakout, Gold Still Failing. WTI +3.00% to $76.90 has broken above the two-day stabilization range ($73–76). Brent +2.29% to $83.27, approaching $85 significance. Heating oil +5.14% and RBOB +3.14% — crack spreads widening further. Natural gas +1.65%. The energy re-acceleration is THE dominant overnight signal and the primary threat to yesterday’s recovery. Gold at $5,137 (+0.04%) is flat — cumulative −3.3% during the war, confirming its failure as a geopolitical hedge. Industrial metals SELLING: copper −1.65%, palladium −1.73% — yesterday’s pro-cyclical metals bid is fading. Grains broadly green (oats +2.84%, wheat +0.88%, corn +0.62%).

Sector Rotation Flipped to Stagflation. XLE the ONLY green sector in pre-market (+0.30%) — the mirror image of yesterday when XLE was one of the weakest. XLY (yesterday’s leader at +1.78%) is now the worst at −0.66%. XLV −0.48%, XLI −0.41%, XLK −0.40%. This 180-degree flip in 12 hours is the classic stagflation signal: energy up, everything else down. The sector structure is testing whether yesterday’s pro-cyclical pivot was a one-day event or a durable shift.

Factor Structure Reverting Defensive. USMV outperforming SPHB for the first time since Tuesday (+15 bps spread). All factors red in pre-market. SPHB −0.25% (was yesterday’s leader at +1.84%). IJH −0.44%, VLUE −0.51%. The magnitude is modest — consolidation rather than capitulation — but the direction has reversed from yesterday’s emphatic risk-on signal.

Equities: Orderly Pullback, Recovery Pattern Being Tested. ES −0.34%, NQ −0.43%, YM −0.59%, RTY −0.88%. Small caps giving back the most (rate and oil sensitivity). All Mag 7 red: TSLA −0.79% worst (yesterday’s +3.44% being unwound), NVDA −0.70%, META −0.67%. The intraday recovery pattern is THE test: Monday recovered from −1.2% to flat, Tuesday recovered from −2.5% to −0.92%, Wednesday closed +0.78%. If today opens red and closes red, the pattern breaks and the market transitions from “buy the dip” to “sell the rally.”

FX — Dollar Reversing Higher. DXY at 99.025 (+0.25%) breaking the two-day weakening trend. All G10 currencies declining. AUD −0.78% worst (commodity currency hit despite oil rally — market pricing negative growth implications of the energy shock). BTC at $72,800 (−0.88%), modest pullback from yesterday’s +7.27% surge. The dollar’s reversal higher signals risk-off FX repositioning.

Critical Wild Card: Peace Talk Reports. Reports that Iranian operatives reached out to the US to explore potential peace talks — the first diplomatic feeler since the war began. If confirmed, this could cap oil’s upside and reinstate the “short war, manageable premium” thesis. A single credible headline would reverse the overnight risk-off posture. Unconfirmed but worth monitoring closely.

6. THE GAME PLAN

Today’s Key Events: Initial Jobless Claims 8:30 AM (expected 215K vs. prior 212K — HIGH IMPACT). Trade Balance 8:30 AM. Factory Orders 10:00 AM. NG Storage 10:30 AM. Earnings: Kroger, Costco, Marvell. War headlines continuous. 15% tariff implementation possible today/tomorrow. TOMORROW: February Non-Farm Payrolls 8:30 AM — the week’s main event.

The Bull Case: Yesterday’s data was unambiguously strong: ADP +63K and ISM Services 56.1 (highest since July 2022) killed the growth-scare narrative. MOVE collapsed below pre-war levels (70.03) — rates vol crisis ended. The equity pullback is orderly (ES −0.34% after +0.78%). Breadth snapped sharply higher (R2FD +56%). Peace talk reports could cap oil. Israeli official says war goals achievable in “two weeks.” Iran’s conventional military being systematically destroyed. If oil pulls back toward $75 and claims come in benign, the recovery holds.

The Bear Case: Oil has broken above the stabilization range — WTI $76.90 approaching the $80 critical threshold. Bond selling is the most aggressive of the series (ZB −0.61%). Sector rotation has flipped 180 degrees back to stagflation in 12 hours. The 15% global tariff adds a fresh inflation impulse on top of the oil shock. Iran struck Azerbaijan (geographic expansion). Death toll 1,230+. Threats to target “all economic centres.” The recovery pattern is being tested — Monday recovered 100%, Tuesday 63%, Wednesday green. If today opens red and closes red, the pattern breaks. Small caps −0.88% suggests rate sensitivity is biting. Gold still failing (−3.3% cumulative during a war). NFP tomorrow creates positioning caution.

Regime: Recovery Under Stress Test. The overnight oil breakout and accelerating bond selling are directly challenging yesterday’s pro-cyclical pivot. The sector rotation has flipped back to stagflation (XLE only green, XLY worst). This is NOT a return to acute liquidation — the pullback is orderly. But the “war premium is contained” pillar that supported yesterday’s rally is cracking. The key question: was yesterday a genuine regime shift or a one-day relief rally? Today’s close and tomorrow’s NFP will answer that.

Watch List

WTI above $78–80 — If crude pushes through $78 toward $80, the “contained war premium” thesis collapses. Every additional dollar generates more inflation fear, more bond selling, more stagflation rotation. Currently $76.90.

Jobless Claims at 8:30 AM — Expected 215K vs. prior 212K. First weekly claims data since war began. Above 225K reignites growth fears. Below 210K confirms labor resilience.

Intraday recovery pattern — The defining test. Mon: recovered. Tue: recovered 63%. Wed: green close. If today opens red and closes red, the market transitions from “buy dips” to “sell rallies” — a bearish regime shift.

MOVE at the open — Prior close 70.03 (below pre-war 73.21). If MOVE stays below 73 despite aggressive bond selling, the repricing is orderly. Above 75 = rates vol crisis re-engaging.

Peace talks confirmation — Iranian peace feeler reports are the wild card. A credible diplomatic headline would cap oil, reverse dollar strength, and reinstate the recovery narrative instantly.

Morning check: the recovery is under stress. Oil has broken out. Bonds are selling the hardest of the series. The sector rotation has flipped back to stagflation in 12 hours. But the equity pullback is orderly, and peace talk reports are circulating for the first time. Yesterday’s strong data provides a floor; today’s oil breakout provides a ceiling. The regime is genuinely in transition — today’s close and tomorrow’s NFP will determine which direction.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.