☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: Goldilocks lasted one day. The regime has shifted violently to stagflation scare. Core PPI printed +0.8% MoM — nearly triple the +0.3% consensus. Every index red: ES −0.87%, NQ −0.99%, YM −1.10%, RTY −1.56%. Meanwhile, the commodity complex is sending the most powerful inflationary signal of the year: WTI +3.68%, platinum +6.65%, silver +5.61%, corn +3.29%. Bonds are rallying DESPITE the hot PPI — 10Y broke below 4.00%. VIX back above 20. NVDA closed −5.46% yesterday despite its beat-and-raise.

The Number That Matters: Core PPI +0.8% MoM (vs. +0.3% est., prior +0.7%). Headline PPI +0.5% MoM (vs. +0.3% est.). Full-year core wholesale prices +3.6%. Services led at +0.8% MoM, highest since July. Second consecutive core print above +0.7% — annualized ~9–10%. Several components feed directly into PCE. March 13 PCE report will run hot. March 17–18 FOMC will be complicated. Rate cuts in May/June significantly less likely.

The Setup: Five different regimes in five days. Monday: mean-reversion. Tuesday: reflation. Wednesday: reflationary boom. Thursday: Goldilocks. Friday: stagflation scare. Commodities say “inflation.” Bonds say “growth scare.” Equities say “sell everything.” FX says “safety.” The bond-commodity divergence must resolve. How equities close today determines which interpretation wins into next week.

2. OVERNIGHT SESSION RECAP

Asia-Pacific

Nikkei −0.26% for second consecutive red session. TOPIX −0.81%. The semiconductor complex rolled over. South Korea and Taiwan pulled back from record highs. Cautious ahead of PPI.

Europe

Euro Stoxx 50 −0.62%, DAX −0.23%. The European reallocation trade is pausing. Energy stocks the sole bright spot as crude surges.

US Pre-Market

NVDA “Sell the News” — devastating. Closed −5.46% at $184.89 despite beating every metric. Now −1.55% more pre-market to $182. Data center sequential growth decelerated 25% → 22%, Q1 guidance implies ~15%. Share buybacks declining. The dot-com comparisons have surfaced. Stocks falling on great news is a regime signal.

Yesterday’s session: S&P 500 −0.54%, Nasdaq −1.18%. SOXX crashed −3.04%. Only 4/11 sectors green.

PPI devastated the tape. Core +0.8% hit at 8:30 AM. Futures gapped lower. The inflation impulse is not just commodity-driven — it’s embedded in services (healthcare, financial services, portfolio management). Worst combination for equities: input cost inflation with no pricing power relief.

Pre-market: ES −0.87%, NQ −0.99%, YM −1.10%, RTY −1.56%. Every Mag 7 red. MSFT −2.18%, NVDA −1.55%, META −1.40%, TSLA −1.07%.

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 02/26/26. Provided for informational purposes only; not as investment advice.

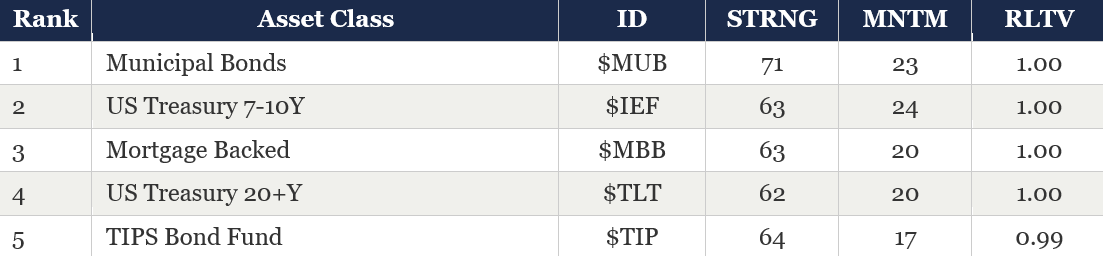

Asset Classes — Top 5

Asset Classes — Bottom 5

Regime signal: Top 5 entirely bonds. TIPS at rank 5 — inflation-protected bonds climbing while nominals lead = stagflation pricing. Dollar MNTM 15, surging. S&P 500 MNTM now −1. Senior loans ($BKLN, STRNG 27) still at the bottom.

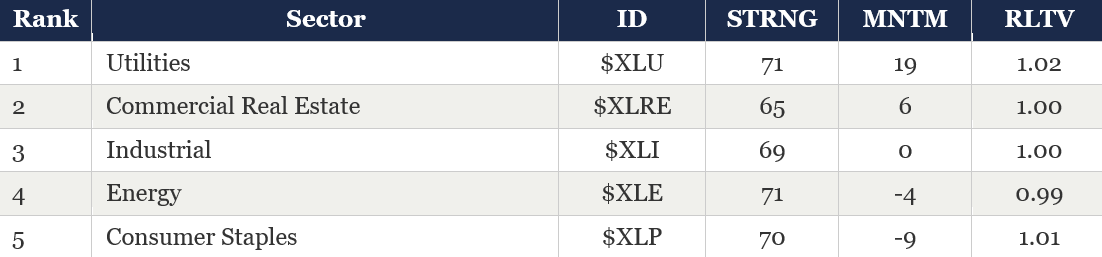

Sector ETFs — Top 5

Sector ETFs — Bottom 5

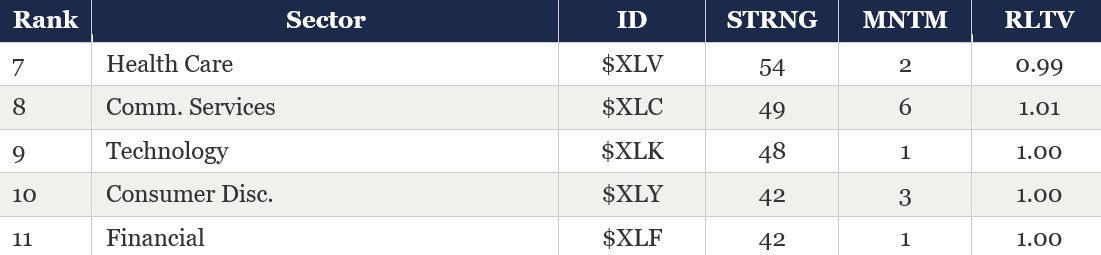

Regime signal: Pure defensive leadership. Utilities, Real Estate, Industrials (MNTM collapsed to 0), Energy, Staples at top. Technology STRNG 48. Consumer Disc. and Financials tied at bottom (STRNG 42). Materials MNTM −10. Unambiguously defensive.

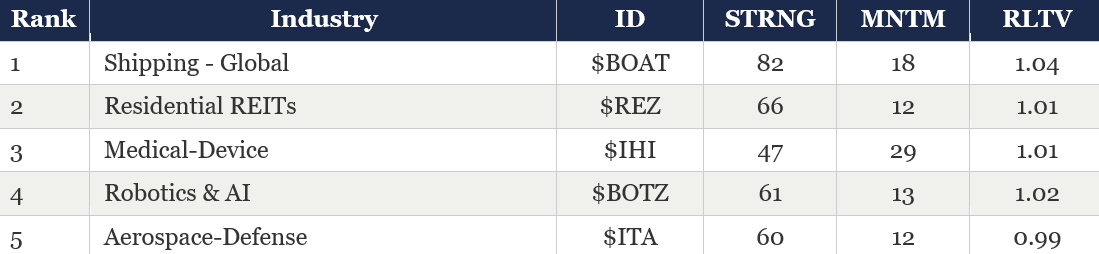

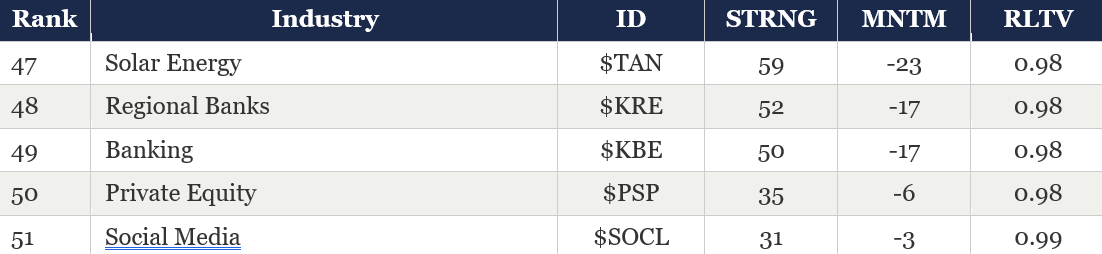

Industry ETFs — Top 5

Industry ETFs — Bottom 5

Regime signal: Medical-Device ($IHI) MNTM 29 — highest on the board, classic defensive healthcare rotation. Semiconductor ($SMH) MNTM turned negative (−5). Solar (−23), Banks (−17) worst momentum. Software ($IGV) MNTM +18 diverging from semis.

4. MORNING DATA REACTION

Core PPI +0.8% MoM — the number that changed everything. Nearly triple consensus. Headline +0.5% vs. +0.3%. Full-year core +3.6%. Services +0.8%, highest since July. Second consecutive month above +0.7% — annualized ~9–10%.

Three critical implications: (1) PPI components feed into PCE — March 13 PCE will run hot. (2) Two consecutive prints above +0.7% is signal, not noise. (3) Fed on hold at 3.50–3.75% longer; May/June cuts significantly less likely.

Market reacted with equities selling and bonds rallying — growth scare over inflation. 10Y below 4.00% despite scorching PPI. The bond-commodity divergence is the session’s central paradox.

Also: Chicago PMI at 9:45 AM, Construction Spending at 10:00 AM — growth data that could tip the balance.

5. THE DYRH READ

Regime: Stagflation Scare. Confidence: LOW. Cross-asset signals genuinely conflicting.

Yield Curve: Bull Steepener Despite Hot PPI. 10Y broke below 4.00% to 3.991% on the same morning core PPI printed +0.8%. Bond market choosing growth scare over inflation. ZB +0.19%, ZN +0.18%. Genuine duration demand consistent with safety, not rate-cut positioning.

Commodity Complex — Most Inflationary Signal in Series. Every energy contract green. Every metal green. Seven of eight grains green. WTI +3.68%, platinum +6.65%, silver +5.61%, corn +3.29%. Energy reversal obliterates the disinflationary thesis. Precious metals two-day swings of 10%+ indicate extreme positioning.

The Central Paradox. Commodities say inflation. Bonds say growth scare. Both cannot be right simultaneously. Today’s equity close determines which wins.

NVDA “Sell the News.” Down 5.46% on a blowout. Now −1.55% more pre-market. Dot-com parallels surfacing. Price action on great news is a regime signal.

VIX Back Above 20. 21.36 (+14.65%). Back above the fear threshold. Surged 3.79 points in 48 hours. Vol regime transition underway. MOVE 63.93 (+2.40%).

Breadth Will Reverse. Yesterday’s all-20-readings-green was the healthiest print. With RTY −1.56% and IJR −1.45%, breadth will contract significantly. COR1M spiked +28.33% — macro factors reasserting dominance.

Sector/Factor — Pure Defense. XLE sole green sector (+1.29%). USMV sole green factor. IJR (−1.45%), SPHB (−1.51%), MTUM (−1.53%) liquidated. “Energy up, everything else down” = classic stagflation positioning.

FX — Flight to Safety. Swiss franc sole G10 gainer. Commodity currencies NOT confirming commodity surge. Bitcoin −2.05% — risk asset, not inflation hedge. Dollar conflicted.

6. THE GAME PLAN

Today’s Key Events: PPI released (Core +0.8%). Chicago PMI 9:45 AM. Construction Spending 10:00 AM. CFTC positioning 3:30 PM. End-of-week rebalancing flows.

The Bull Case: Bond market says growth risk > inflation. 10Y below 4.00% means eventual rate cuts. Yesterday’s breadth was genuinely improving. NVDA fundamentals remain extraordinary. PPI methodology update complicates the read. If equities find a floor intraday below −1%, this could be a one-day event.

The Bear Case: Two consecutive core PPI prints above +0.7% is a trend (∼9–10% annualized). March 13 PCE will run hot. NVDA falling 5% on a blowout is the most bearish AI price signal yet. Energy reversing +3.68% obliterates the disinflationary thesis. The commodity-bond divergence means the market is genuinely confused. RTY −1.56% destroys the broadening thesis. VIX above 20 means hedges need rebuilding.

Regime: Stagflation Scare. Hot PPI + energy reversal + broad equity selloff + bond rally = conflicting macro signals. Five different regimes in five days. The market has not found stable equilibrium since the tariff shock. Today’s close determines whether stagflation scare becomes the new regime. Confidence: Low. This is a “reduce risk” environment until the bond-commodity divergence resolves.

Watch List

10Y vs. 4.00% — Holds below = growth scare dominates. Reverses above = inflation repricing reasserts.

RTY below 2,620 — Break below signals multi-day small-cap damage.

WTI above $67 — Energy reversal holds = disinflationary thesis dead.

Chicago PMI / Construction — Weak growth data validates bonds. Strong data validates commodities.

NVDA $180 — 200-day MA near $173. If $180 breaks, sell-the-news cascades into broader tech deleveraging.

Morning check: the regime changed overnight. The Goldilocks window was one day. The tape is now pricing stagflation risk, and the bond-commodity divergence must resolve.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.