☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: Fed Day meets hot PPI meets overnight war escalation — three regime-defining forces converging on a single session. February PPI (released 8:30 AM, delayed from March 12 by the government shutdown) came in HOT: +0.7% MoM (vs. +0.5% January), +3.4% YoY (largest 12-month advance since February 2025). Final demand goods surged +1.1% — the first hard data confirming that war-driven energy costs are transmitting into producer prices. Core PPI ex food/energy/trade: +0.3% MoM (9th consecutive increase). Services +0.5%. The Fed was “flying blind” without this data until this morning. Gold crashed $129 to $4,879 (−2.58%) — BACK BELOW $5,000 — but this is rate REPRICING, not forced liquidation (MOVE is −7% at 79.23, bond vol crisis is over). The entire precious metals complex is in rout: platinum −4.81%, palladium −4.53%, silver −2.77%. Brent at $105.86 (+2.36%) is a new SERIES HIGH (+45.3% from pre-war). The war escalated overnight: Israel killed Ali Larijani (Iran’s security chief) and Basij commander; Iran launched missiles killing 2 in Ramat Gan, Israel; the US dropped 5,000-lb GBU-72 bunker buster bombs on hardened Iranian missile sites along Hormuz; Gulf states intercepting drones/missiles. EU flatly rejected Trump’s call for Hormuz military assistance. However, 8 non-Iranian vessels transited Hormuz Monday (“permission-based”), nearly double recent days. ES at 6,743.75 (−0.44%) — an orderly pre-FOMC pause, remarkably sanguine given the PPI shock. Wall Street has COMPLETELY abandoned rate cut expectations for 2026 (was pricing two cuts pre-war). The 2Y surged +3.4 bps in a bear flattener. The market’s bet is now on a hawkish-leaning hold — Powell at 2:30 PM is the session.

The Number That Matters: PPI at +0.7% MoM with goods +1.1%. This is the smoking gun: the Hormuz closure and $90–105 oil are transmitting through the supply chain into producer prices. This is pre-war February data in terms of the collection period, but energy prices were already rising sharply. The YoY rate of 3.4% is the highest since February 2025. This data arrives 5.5 hours before the Fed’s rate decision, making the dot plot and Summary of Economic Projections the most consequential in years. The Fed faces an inflation that is ACCELERATING (PPI +0.7% after +0.5% after +0.4%) while growth is DECELERATING (GDP 0.7%, NFP −92K, Empire State −0.20). Textbook stagflation — now confirmed in both consumer AND producer price data.

The Setup: FOMC Day. Decision at 2:00 PM. Dot plot + Economic Projections. Powell presser at 2:30 PM. Hold at 3.50–3.75% is universal. The dot plot is the fulcrum: does the median dot confirm zero cuts in 2026 (validating the market’s hawkish repricing) or show one cut (preserving a shred of dovishness)? Powell’s language on the oil shock is critical: “transitory supply shock” = markets stabilize; “persistent inflationary pressure requiring vigilance” = gold crashes further, yields spike. The recovery regime’s STRUCTURAL pillars remain intact: breadth surging (S5FD 66.60), MOVE at 79 (bond vol crisis over), COR1M declining (29.50), VIX in healthy contango. But the surface is stressed: gold below $5,000, PPI hot, oil at series highs, bear flattener. Micron earnings after the close add a second catalyst to an already dense session.

2. OVERNIGHT SESSION RECAP

Asia-Pacific

TOPIX −1.30% — Japan worst index, hit by overnight escalation and hot PPI driving yen weakness. Nikkei −0.34%. Asia retreating from the 3-day rally as the Larijani killing and continued Hormuz escalation weigh on sentiment.

Europe

Euro Stoxx +0.09%, DAX −0.04% — essentially flat. Europe waiting for the Fed. EU foreign ministers flatly rejected Trump’s call for Hormuz military assistance. Germany: “not NATO’s war.” Australia and Japan also declined to send ships. The international isolation of the US military position is deepening.

US Pre-Market

Day 18 — War Escalating on Every Front. Israel killed Ali Larijani (top security official) and Basij paramilitary chief Soleimani. Iran launched missile barrage killing 2 in Ramat Gan, Israel. US dropped 5,000-lb GBU-72 bunker buster bombs on hardened Iranian missile sites along the Strait of Hormuz. Gulf states (Kuwait, UAE, Qatar, Saudi Arabia) actively intercepting Iranian drones and missiles. Fujairah Oil Industry Zone struck by drone (the vital Hormuz BYPASS route). Drone hit Baghdad’s Green Zone near US Embassy. USS Gerald Ford fire burned 30+ hours. Trump’s National Counterterrorism Center director Joe Kent resigned over the war. Gulf oil exports down 60% in week to March 15. Death toll 2,200+. Gas $3.79/gallon (+26% since war). However: 8 non-Iranian vessels transited Hormuz Monday (“permission-based”), nearly double recent days — the partial reopening narrative persists despite escalation.

February PPI (released today 8:30 AM — delayed from March 12 by government shutdown): Headline +0.7% MoM (accelerating from +0.5% Jan, +0.4% Dec). YoY +3.4% (largest since Feb 2025). Final Demand Goods +1.1% (war/oil pass-through). Final Demand Services +0.5% (portfolio management +1%, securities brokerage +4.2%). Core ex food/energy/trade +0.3% (9th consecutive increase). Food +2.4%, Energy +2.3%. Within food, fresh/dry vegetables +48.9%. This is the first hard data confirming inflationary pass-through from the Hormuz closure into producer prices.

Prior session (March 17 close): S&P +0.78% to 6,773 (3-day rally, ~60% of war drawdown retraced). MOVE collapsed to 79.23 (−7.06%). S5TH reclaimed 50. Gold green for 2nd session ($5,008). SPHB led factors 3rd straight day. All 11 sectors green. 11 of 12 factors green. COR1M 29.50. The recovery regime confirmed at very high confidence — until this morning’s PPI stress test.

Today’s events: FOMC Decision 2:00 PM + Dot Plot + Summary of Economic Projections. Powell Press Conference 2:30 PM (second-to-last as Chair). Micron Technology (MU) Q2 earnings after close (~$9 EPS, $19B+ revenue expected, AI demand litmus test). Bank of Canada decision. Tomorrow: ECB, Bank of England, SNB, BOJ decisions; Jobless Claims; Philly Fed Manufacturing; New Home Sales.

3. THE PRIOR DAY’S REGIME (Jeff Quiggle Data)

Data from JeffQuiggle.com as of 03/17/26. Provided for informational purposes only; not as investment advice.

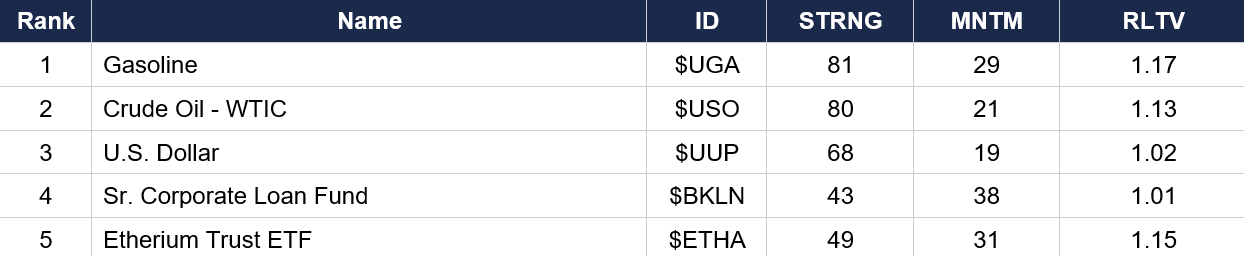

Asset Classes — Top 5

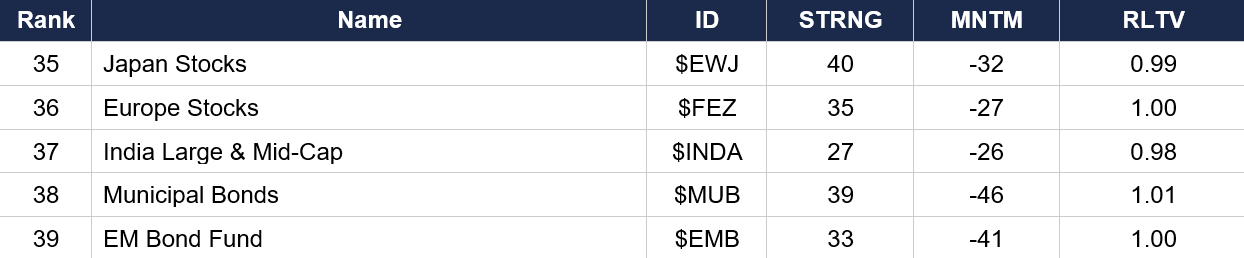

Asset Classes — Bottom 5

Regime signal: Gasoline ($UGA) reclaims rank 1 from crude as refined product tightness leads. Senior Corporate Loans ($BKLN rank 4, MNTM 38) maintains the HIGHEST non-energy/non-crypto momentum — floating-rate credit remains the standout asset in a rising-rate environment. Crypto ($ETHA rank 5, $IBIT rank 6) holding top positions despite today’s BTC −3%. VIX ($VXX rank 8, MNTM −3) has NEGATIVE momentum and dropped further — the fear trade continues unwinding. Gold ($GLD rank 20, MNTM −20) has deteriorated sharply from rank 16 yesterday — the rate repricing is devastating gold’s ranking. Nasdaq ($QQQ rank 11, MNTM 2) barely positive. S&P ($SPY rank 17, MNTM −8) modestly negative. EM Bonds ($EMB, MNTM −41) and Municipal Bonds ($MUB, MNTM −46) remain the worst momentum. Corporate Bonds ($LQD rank 34, MNTM −26) deeply negative as rate repricing hits credit.

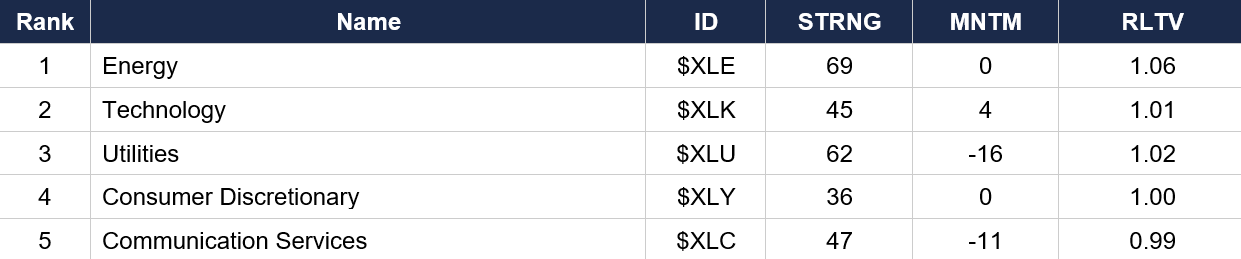

Sector ETFs — Top 5

Sector ETFs — Bottom 5

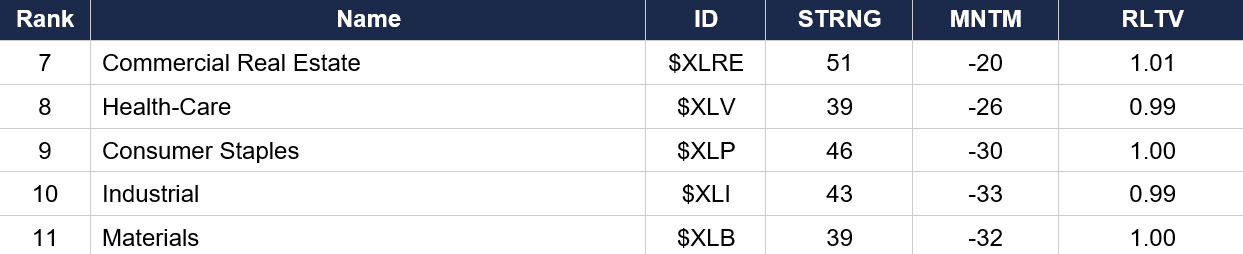

Regime signal: Energy ($XLE rank 1) MNTM has reached exactly 0 — the sector is at a momentum inflection. Despite $106 Brent, energy equities are no longer gaining momentum, suggesting the oil-equity divergence is maturing. Technology ($XLK rank 2, MNTM 4) still positive on GTC momentum. Consumer Discretionary ($XLY rank 4, MNTM 0) at inflection. ALL sectors except Energy and Technology have negative momentum. Health-Care ($XLV rank 8, MNTM −26) and Industrial ($XLI rank 10, MNTM −33) remain deeply weak.

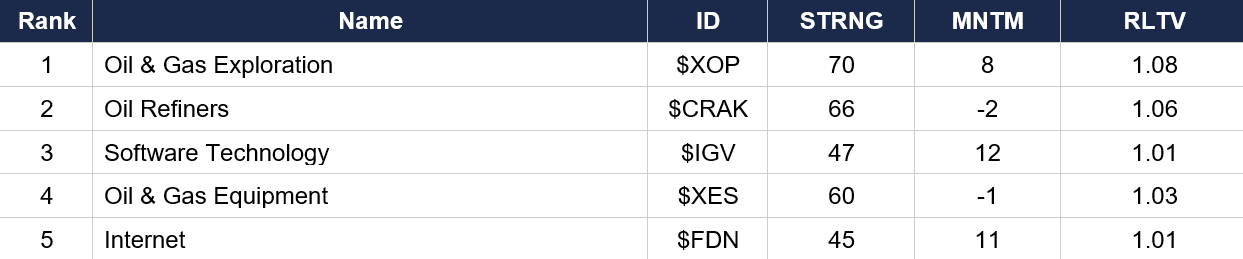

Industry ETFs — Top 5

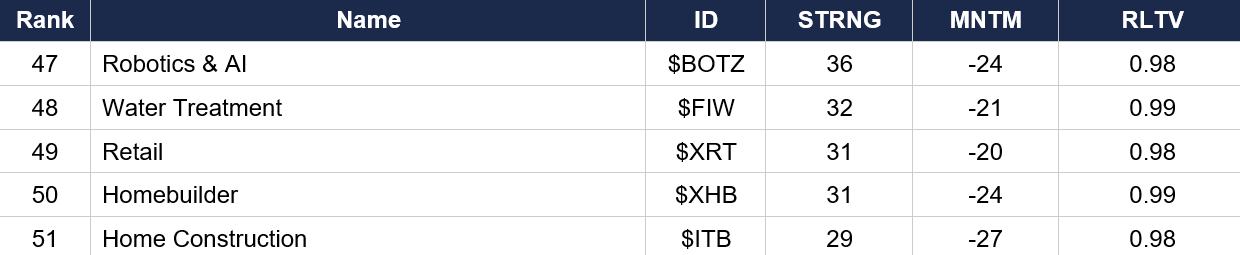

Industry ETFs — Bottom 5

Regime signal: Oil & Gas Equipment ($XES rank 4) has risen into the top 5 — the energy services complex is broadening beyond just exploration and refining. Software ($IGV, MNTM 12) and Internet ($FDN, MNTM 11) maintain positive momentum from GTC. Clean Energy ($ICLN rank 7, MNTM 6) and Solar ($TAN rank 10, MNTM 4) continue benefiting from the $100+ oil alternative energy thesis. Semiconductor ($SMH rank 19, MNTM −6) improving but still negative. Aerospace-Defense ($ITA rank 39, MNTM −26) continues plummeting despite the war. Home Construction ($ITB rank 51, MNTM −27) and Homebuilder ($XHB rank 50, MNTM −24) at the absolute bottom as 30Y at 4.85% and mortgage rates at 6.11% crush housing.

4. MORNING DATA REACTION

February PPI (released today 8:30 AM — delayed from March 12 by government shutdown): Headline +0.7% MoM, +3.4% YoY. HOTTER THAN EXPECTED (consensus was +0.3% headline, +0.3% core). Final demand goods surged +1.1% (war/oil pass-through). Services +0.5% (portfolio management +1%, securities brokerage +4.2%). Core PPI ex food/energy/trade +0.3% MoM (9th consecutive increase). Food +2.4%, Energy +2.3%. Within food, fresh/dry vegetables +48.9%. This is the first hard data confirming that the Hormuz closure’s energy shock is transmitting into producer prices. The data was delayed by the government shutdown, meaning the Fed was “flying blind” until this morning — 5.5 hours before their rate decision.

The PPI confirms the stagflation diagnosis in BOTH consumer and producer data: CPI +0.3%/2.4% YoY (in-line but pre-war), PPI +0.7%/3.4% YoY (accelerating), Core PCE 3.1% (rising), GDP 0.7% (decelerating), NFP −92K, Empire State −0.20. The inflation side is getting WORSE while the growth side is getting WORSE. The Fed meets in 5 hours with zero good options.

FOMC Decision at 2:00 PM: Hold at 3.50–3.75% is universal. The dot plot is the fulcrum — December’s median dot projected two 25bp cuts in 2026. The market has now priced ZERO cuts. If the dots confirm zero or one cut, it validates the repricing. If the dots show a hike discussion, risk-off. Powell’s presser at 2:30 PM: the key phrase is how he characterizes the oil shock. “Transitory supply disruption” = markets stabilize. “Persistent inflationary pressure requiring extended vigilance” = gold crashes further, yields spike.

Micron (MU) earnings after the close (~$9 EPS, $19B+ revenue, +146% YoY). Entire 2026 HBM supply sold out. First major semiconductor earnings of the season and a litmus test for the AI demand narrative. A beat provides post-FOMC support; a miss compounds any hawkish reaction. Tomorrow: ECB, BOE, SNB, BOJ decisions; Jobless Claims; Philly Fed Mfg; New Home Sales.

5. THE DYRH READ

Regime: Post-Crisis Recovery — Fed Day Stagflation Stress Test. The recovery structure is intact beneath the surface noise (breadth, MOVE, correlation all confirming). But the hot PPI has introduced a new problem: hard evidence of war-driven inflationary pass-through arriving 5.5 hours before the Fed decides. Confidence: Moderate-High.

Yield Curve: Bear Flattener — Hawkish Repricing on Hot PPI. The 2Y surged +3.4 bps to 3.712% — more than 4x the 30Y’s +0.7 bp move. This is the market aggressively pricing out any remaining rate cut optionality. The 2Y is now at the lower bound of the fed funds target (3.50–3.75%), compressing the policy premium to zero. 10Y at 4.214% has risen from its 3-session decline. 30Y at 4.850% barely moved. The flattening is coming from front-end HAWKISH repricing, not flight-to-safety. Cumulative: 10Y +26.5 bps from pre-war. The key question: does today’s hot PPI and the dot plot push the 10Y back toward the Day 12 highs (~4.30%)?

Gold Crashed Below $5,000 Again — But the Mechanism Has Changed. Gold −$129 to $4,879 (−2.58%). BACK BELOW $5,000. But this is NOT the forced-liquidation signal from Days 2–11. On those days, gold fell alongside surging MOVE (bond panic) and crashing equities. Today, MOVE is −7% at 79.23 (bond vol crisis OVER), equities are only −0.44%, and the move is driven by a hot PPI driving higher-for-longer rate expectations → higher real rates → non-yielding asset repricing. GVZ (gold vol) collapsing −8.44% while gold crashes means the options market views this as a KNOWN repricing event, not an uncertain risk event. Platinum −4.81% and palladium −4.53% confirm the PGM complex is in a real-rate-driven rout.

Oil at New Series Highs While Equities Ignore It. Brent $105.86 (+2.36%) — new SERIES HIGH. WTI $96.41 (+0.21%). Brent-WTI spread has widened to $9.45 (widest of the series). The equity-oil decoupling has now survived 3+ sessions, overnight war escalation, AND a hot PPI — remarkably resilient. The market has decided: the oil shock is manageable with IEA reserves and partial Hormuz reopening. 8 non-Iranian ships transited Monday. But Brent at $106 with goods PPI +1.1% means the inflation pass-through is REAL and accelerating. If Brent stays above $105 and PPI keeps accelerating, the “transitory” narrative collapses.

Equities: Remarkably Sanguine for a Hot PPI on Fed Day. ES at 6,743.75 (−0.44%) — an orderly pre-FOMC pause well above the 200-day MA floor. Mag 7 pre-market: all 7 red but mostly small moves (−0.11% to −0.84%). Russell −0.11% (outperforming S&P’s −0.44%). The 3-day rally has retraced ~60% of the war drawdown and the market is holding gains despite a +0.7% PPI print. This sanguinity is either justified pricing of a dovish hold or complacency ahead of a potential hawkish surprise. SPHB −0.49% in pre-market after leading factors for 3 straight sessions.

Recovery Structure Intact Beneath Surface Noise. The 5 recovery pillars from Day 14 remain standing: (1) S5FD at 66.60 — fastest breadth recovery of the series, 2/3 of S&P above 5-day MA. (2) MOVE at 79.23 (−7.06%) — bond vol crisis definitively over, 72% of war spike retraced. (3) COR1M at 29.50 — declining from 37.21 peak, stock-specific alpha returning. (4) VIX term structure in healthy contango (VIX1D 17.55 vs VIX 23.08). (5) All other vol measures declining: VXN −6.31%, VVIX −5.33%, GVZ −8.44%. The VIX uptick to 23.08 (+3.17%) is normal Fed Day event premium. S5TH at 50.09 — 200-day breadth holding at the exact bull/bear line (fragile). The hot PPI and gold crash are surface-level stress events driven by rate repricing, not structural deterioration.

6. THE GAME PLAN

Today’s Key Events: PPI released 8:30 AM (+0.7% MoM, +3.4% YoY — HOT). FOMC Decision 2:00 PM + Dot Plot + Summary of Economic Projections. Powell Press Conference 2:30 PM. Micron (MU) Q2 earnings after close. Bank of Canada decision. Tomorrow: ECB, BOE, SNB, BOJ; Jobless Claims; Philly Fed Mfg; New Home Sales.

The Bull Case: The recovery regime’s structural pillars are ALL intact: breadth surging, MOVE at series lows, correlation declining, VIX in contango. ES only −0.44% on a +0.7% PPI is remarkable resilience. The equity-oil decoupling has survived 3+ sessions. Russell outperforming. If Powell characterizes the oil shock as “transitory supply disruption” and the dot plot shows one cut preserved for late 2026, markets stabilize and the rally extends. Micron beat on AI demand could provide post-FOMC tech support. Partial Hormuz reopening (8 ships Monday) continues. Gold’s crash is rate repricing, not forced liquidation (MOVE confirms). The market has absorbed the PPI shock with minimal damage.

The Bear Case: PPI at +0.7% is the smoking gun of inflationary pass-through — goods +1.1%, services +0.5%. Gold crashed below $5,000 again. Brent at $106, new series high. The Fed receives this data 5.5 hours before deciding. If the dot plot shows zero cuts or discusses hikes, the 3-day rally evaporates. Powell calling the oil shock “persistent” rather than “transitory” would be devastating. S5TH at 50.09 — 200-day breadth right at the bull/bear line. Mortgage rates jumped to 6.11%. The war is escalating: Larijani killed, bunker busters on Hormuz, Gulf exports down 60%, EU refusing to help. All rate cut expectations for 2026 have been priced out. The bear flattener means the front end sees NO relief.

Regime: Post-Crisis Recovery — Fed Day Stagflation Stress Test. The recovery’s structural foundation (breadth, MOVE, correlation, decoupling) remains intact, but the hot PPI has made the FOMC decision the highest-stakes event of the series. The regime label will likely need updating by the close depending on the outcome. Hold + dovish = recovery confirmed. Hold + hawkish = recovery tested. Hike discussion = recovery breaks.

Watch List

FOMC 2:00 PM — THE event of the series — Hold universal. Dot plot is the fulcrum: zero cuts vs. one cut vs. hike discussion. Powell’s oil shock characterization (“transitory” vs. “persistent”) determines the post-decision direction. Risk is ASYMMETRIC.

PPI +0.7% — stagflation confirmed in producer data — The first hard evidence of war-driven inflationary pass-through. Goods +1.1%, services +0.5%, core +0.3% (9th consecutive). Arrives at the worst possible time for the Fed.

Gold below $5,000 — rate repricing, not liquidation — The mechanism has CHANGED. MOVE −7% at 79. GVZ −8.4%. This is higher-for-longer rates crushing non-yielding assets, not margin-call forced selling. The distinction matters for forward positioning.

Micron after close — AI demand litmus test — ~$9 EPS, $19B+ revenue, +146% YoY. Entire 2026 HBM sold out. Beat = post-FOMC tech support. Miss = compounds any hawkish reaction. First major semi earnings of the season.

S5TH at 50.09 — the bull/bear line — 200-day breadth at the exact dividing line. A close below 50 today would be the first regression since the recovery and would weaken the thesis. Watch whether the FOMC reaction pushes breadth above or below this critical threshold.

Morning check: the most consequential session of the entire series. Hot PPI (+0.7%) arrived 5.5 hours before the Fed decides — the first hard evidence of war-driven inflationary pass-through. Gold crashed below $5,000 on rate repricing. Oil at series highs. But the recovery’s structural pillars are ALL intact: breadth surging, MOVE at crisis lows, correlation declining. The market has absorbed the PPI with remarkable calm (ES −0.44%). Now everything comes down to 2:00 PM. The dot plot. Powell’s words. The regime either confirms or breaks in the next six hours.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.