☀️THE MORNING BELL

Pre-Market Intelligence Report — 10:30 AM Opening Range Edition

1. THE QUICK SCAN

Overnight Tape Summary: TRUMP PRIMETIME ADDRESS DESTROYS 3-SESSION RALLY. OIL +12.3%. GOLD −3.56%. FORCED LIQUIDATION RETURNS. EVERY DE-ESCALATION TRADE REVERSED IN A SINGLE SESSION.

President Trump addressed the nation at 9 PM Wednesday in a ~19-minute primetime speech that contained NO new information, NO ceasefire timeline, and NO path to ending the war — only escalation rhetoric. The market was pricing de-escalation. The speech delivered escalation. The 3-session rally that represented the first sustained recovery of the entire war has been DESTROYED overnight.

Key quotes: ‘We’re going to hit them extremely hard over the next two to three weeks.’ ‘We’re going to bring them back to the stone ages where they belong.’ Threatened to ‘hit each and every one of their electric generating plants’ and TARGET IRAN’S OIL if no deal is struck. Said other countries should ‘take the lead’ on reopening Hormuz, adding it may ‘open up naturally.’ Iran’s foreign ministry called the ceasefire claim ‘false and baseless.’ The market reaction is VIOLENT and cross-asset complete: WTI exploded +12.33% to $112.46 — the biggest single-session oil move since the war’s opening days. Gold crashed $171 (−3.56%) to $4,641.9, only $266 above the war low — FORCED LIQUIDATION HAS RETURNED. Silver −7.22%. All 5 metals red. Every equity index red globally: Nikkei −3.46%, Kospi −4.47%, Kosdaq −5.36%, DAX −2.27%, ES −1.48%, NQ −1.88%, RTY −1.98%. All 7 Mag 7 red (META −2.97% worst). XLE is the ONLY green sector (+2.71%). VIX surged +12.39% to 27.58 — back above the 25 crisis threshold. DXY surging back toward 100 (99.96). Bear steepener: 30Y at 4.935% approaching the 5.00% crisis zone. Grains bid on food security. The entire de-escalation microstructure improvement from Days 23-25 — VIX below 25, MOVE below 100, correlation below 30, breadth at 77 — is at risk of COMPLETE REVERSAL.

Additional overnight: Houthis entered the war with ballistic missile attacks on Israel. Israel expanding Lebanon ground invasion — 1,300+ killed, 1M+ displaced in 4 weeks. Iran struck Kuwait airport fuel depots with drones, hit another oil tanker off Qatar. Iran IRGC warned 18 US tech companies (including NVDA, AAPL, MSFT, GOOG) could be ‘legitimate targets.’ IEA head Birol: ‘April will be much worse than March’ — 12M bpd supply loss, worst in history. BofA projects headline inflation to nearly 4% YoY; global growth cut 40 bps to 3.1%. The April 6 energy strike deadline is now 4 DAYS away — and Good Friday closes markets tomorrow, meaning the deadline arrives during a 3-day weekend.

The Number That Matters: WTI at $112.46 (+12.33%) — the biggest single-session oil move since the war’s opening days.

This takes WTI WELL ABOVE the $100 ‘qualitatively different economic damage’ threshold that was only just breached to the downside yesterday. The round-trip from $99.57 (yesterday) to $112.46 in a single session is a $12.89 swing. IEA’s warning that the pre-war tanker traffic pipeline has been fully exhausted and ‘April will be much worse than March’ provides FUNDAMENTAL support for $112+ oil. This is not just speech-driven risk premium — it is physical supply crunch meeting re-escalation rhetoric. BofA now projects headline inflation to nearly 4% YoY as the oil shock intensifies.

The Setup: Stagflationary Re-Escalation — Trump Primetime Destroys 3-Session Rally. Forced Liquidation Returns. Last Trading Day Before Maximum Gap Risk Weekend.

This is the last full trading session before Good Friday closes markets tomorrow. NFP releases to closed markets Friday morning (consensus +57K, prior −92K, ADP +62K). The April 6 energy strike deadline expires Sunday/Monday. Markets reopen Monday April 7 absorbing BOTH the jobs report AND the deadline outcome. This creates the MAXIMUM GAP RISK weekend of the entire war — three days of unhedgeable catalysts with no ability to trade.

2. OVERNIGHT SESSION RECAP

Asia-Pacific

Asia-Pacific was devastated — markets had OPENED GREEN before Trump’s speech at 9 PM ET (10 AM Asia) and REVERSED violently. Kospi −4.47%, Kosdaq −5.36% (South Korea led losses). Nikkei −2.38% (−3.46% on futures). ASX 200 −0.48%. The severity of Asia’s reaction reflects the region’s energy import dependence and the abrupt reversal of the ceasefire narrative that had driven Asia’s strongest rally of the war.

Europe

DAX −2.27%, Euro Stoxx −2.05%. European indices that had surged +2.7% yesterday on disproportionate ceasefire benefit are now giving back most of those gains. Europe faces the most severe energy import dependence of any major region, and the speech’s implication — Hormuz stays closed, oil infrastructure targeted, war extends 2-3 weeks — is devastating for European energy costs. Nike shares fell further in European trading on weak Q4 guidance compounding the war selloff.

US Pre-Market

Day 34 of Operation Epic Fury. Q2 Day 2. Last full trading session before the maximum gap risk weekend. The session is defined by the total reversal of every de-escalation trade built over Days 23-25.

TRUMP PRIMETIME ADDRESS — THE CATALYST: The speech was characterized by analysts as a ‘summary of tweets’ repeating ‘nearing completion’ while extending the timeline with threats. No new ceasefire framework. No diplomatic pathway. No Hormuz resolution. Instead: 2-3 more weeks of ‘extremely hard’ strikes, threats against power plants and oil infrastructure, ‘stone ages,’ and a directive to allies to handle Hormuz themselves. Iran’s immediate denial of any ceasefire claim removed the last diplomatic pillar.

ADDITIONAL ESCALATION: Houthis entered the war with ballistic missile attacks on Israel — a new front opening. Israel expanding Lebanon ground invasion (1,300+ killed, 1M+ displaced). Iran struck Kuwait airport fuel depots. Iran IRGC designated 18 US tech companies as potential ‘legitimate targets’ — an unprecedented threat to corporate America. Israel killed IRGC Navy commander Tangsiri responsible for the Hormuz blockade.

PRIOR SESSION (Day 25 Close): S&P +0.72% (3rd straight green). MOVE collapsed to 90.19 (below 100 for the 4th time). VIX 24.54 (below 25). ADP +62K beat. ISM Manufacturing 52.7 beat (highest since Aug 2022). ISM Prices Paid 78.3 (SURGED — highest since June 2022, 17/18 industries reporting higher costs). Retail Sales +0.6% beat. Gold surged to $4,813 (+2.87%). XLE −3.74% (de-escalation trade). COR1M 26.08. S5FD 77.73. Every metric of market microstructure had structurally improved. The ‘bond crisis definitively broken’ call was made. HIGH confidence. All of it reversed in a single speech.

ECONOMIC DATA — Already released today (8:30 AM): Initial Jobless Claims 202,000 (BEAT 212K consensus; prior revised to 211K; −9K week-over-week). Near 2-year low. Labor market resilient — ‘low hire, low fire’ continues. Continuing Claims 1.841M (+25K — people unemployed longer but layoffs remain low). Trade Balance −$57.3B (wider from −$54.5B). Factory Orders POSTPONED from today to April 10 (Census Bureau scheduling).

This week remaining: TOMORROW — GOOD FRIDAY, MARKETS CLOSED. NFP released 8:30 AM (consensus +57K, prior −92K, ADP +62K). ISM Non-Manufacturing also to closed markets. SUNDAY/MONDAY — April 6 energy strike deadline expires. MONDAY 4/7 — Markets reopen absorbing NFP + deadline. Next week: April 8 — DAL, STZ earnings. April 9 — GDP Q4 Third Estimate + PCE February. April 10 — CPI March + Factory Orders (rescheduled).

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 04/01/26. Provided for informational purposes only; not as investment advice.

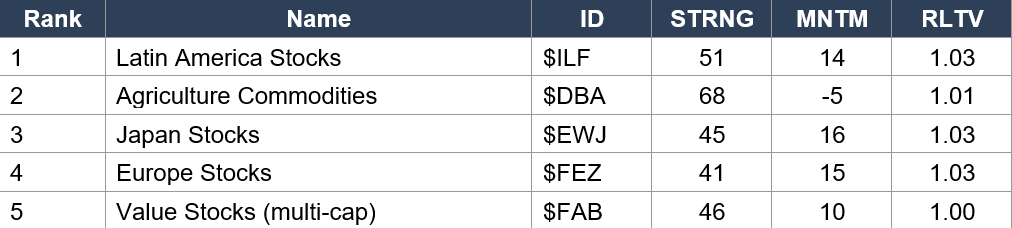

Asset Classes — Top 5

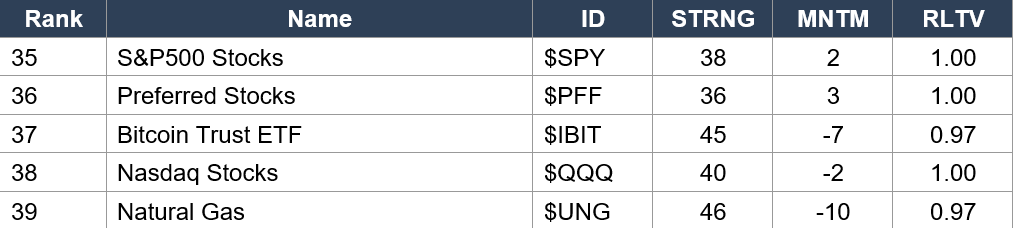

Asset Classes — Bottom 5

Regime signal: The de-escalation rally reshuffled the rankings before Trump’s speech reversed everything. Latin America ($ILF rank 1, MNTM 14) leads — commodity-producing EM remains the structural winner. Japan ($EWJ rank 3, MNTM 16) and Europe ($FEZ rank 4, MNTM 15) surged into the top 5 during the rally — both are now being devastated in pre-market (Nikkei −3.46%, DAX −2.27%). The CRITICAL shift: VIX ($VXX) dropped from rank 2 to rank 6 (MNTM −3) during the de-escalation phase — it will surge back. Dollar ($UUP rank 7, MNTM −7) weakened during the rally — it is now surging back toward 100. Crude Oil ($USO rank 9, STRNG 69, MNTM −16, RLTV 1.10) still has high RLTV at 1.10 and will surge further given WTI +12%. Gold ($GLD rank 27, MNTM 4, RLTV 1.06) had recovered to mid-table — today’s −3.56% crash will destroy that positioning. S&P ($SPY rank 35, MNTM 2) and Nasdaq ($QQQ rank 38, MNTM −2) remain near the bottom. NOTE: Today’s massive reversal is NOT reflected in this data which captures yesterday’s close.

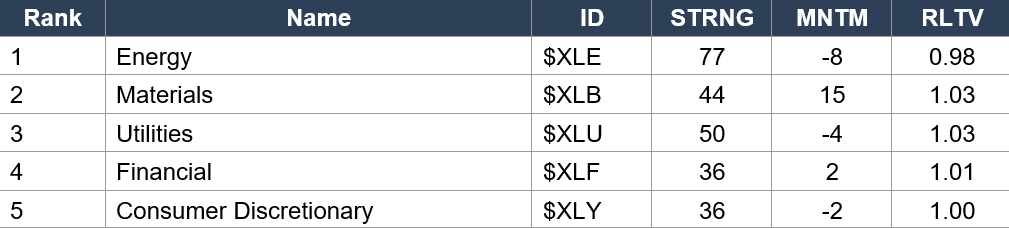

Sector ETFs — Top 5

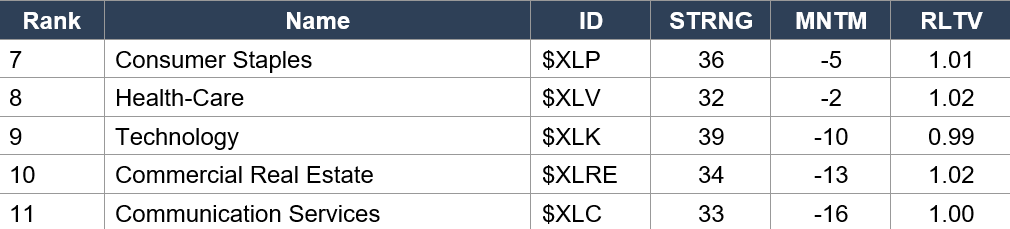

Sector ETFs — Bottom 5

Regime signal: Energy ($XLE rank 1, STRNG 77, MNTM −8, RLTV 0.98) shows a critical divergence: highest STRNG but NEGATIVE momentum and sub-1.00 RLTV. This captured yesterday’s −3.74% XLE selloff during the de-escalation phase. Today’s +2.71% pre-market surge will flip momentum positive again. Materials ($XLB rank 2, MNTM 15) led during the rally. Technology ($XLK rank 9, MNTM −10, RLTV 0.99) remains the only sector with sub-1.00 RLTV — tech continues to be the war’s relative loser. The sector picture is about to undergo ANOTHER complete reversal: XLE was the only red sector yesterday; it is the only green sector today. The ±6.45% XLE swing is the most dramatic sector reversal of the war.

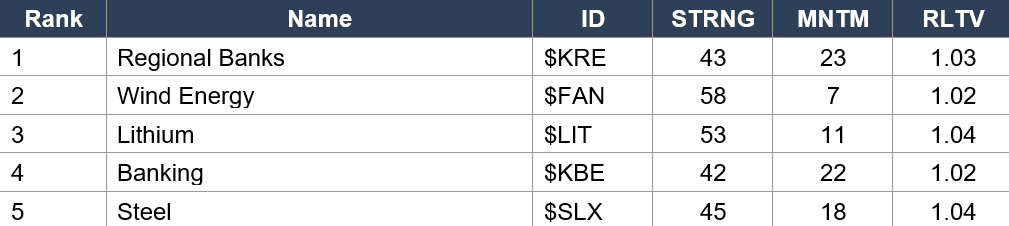

Industry ETFs — Top 5

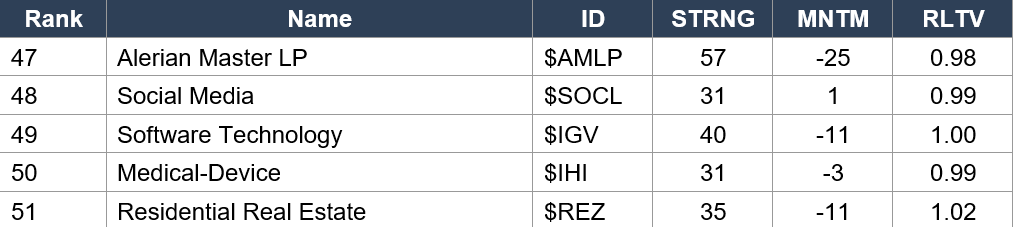

Industry ETFs — Bottom 5

Regime signal: Regional Banks ($KRE rank 1, MNTM 23) and Banking ($KBE rank 4, MNTM 22) lead on momentum — the steeper yield curve during the rally benefited bank NIMs. Today’s bear steepener may paradoxically help banks further if the curve re-steepens on inflation fears. Gold Miners ($GDX rank 9, MNTM 17, RLTV 1.12) had the highest RLTV of any industry at 1.12 — today’s gold crash will devastate the miners. Oil Refiners ($CRAK rank 12, MNTM −13) dropped during the de-escalation but will surge on today’s oil spike. Oil & Gas Exploration ($XOP rank 18, STRNG 71, MNTM −21) had deeply negative momentum from the de-escalation oil drop — today’s +12% WTI move will reverse that entirely. Software Technology ($IGV rank 49, MNTM −11) confirms tech/growth remains the war’s structural loser. Alerian MLP ($AMLP rank 47, MNTM −25) is the worst momentum of any industry — pipeline MLPs were caught in the de-escalation rotation.

4. MORNING DATA REACTION

Initial Jobless Claims: 202,000 — BEAT. Forecast 212K. Prior revised to 211K. Near 2-year low.

Claims fell 9,000 to 202,000, one of the lowest readings in two years. The labor market remains resilient in its most basic measure: companies are NOT laying off workers despite the war, the oil shock, and the financial market volatility. Continuing claims rose modestly to 1.841M (+25K), suggesting those who are unemployed are taking slightly longer to find work, but the overall ‘low hire, low fire’ dynamic persists. This is the third consecutive labor market beat this week (ADP +62K, Retail Sales +0.6% confirming consumer spending, now Claims 202K). The labor data collectively argues against recession — but it does NOT argue against stagflation. You can have a tight labor market WITH rising inflation. That’s exactly what the ISM data showed yesterday.

Yesterday’s ISM Manufacturing Recap: 52.7 (beat 52.3). PRICES PAID 78.3 — SURGING. Highest since June 2022.

The ISM headline at 52.7 was constructive — manufacturing expanded for a 3rd straight month, highest since August 2022. But the Prices Paid component EXPLODED to 78.3 from 70.5, a 7.8-point surge that represents the highest input cost reading since June 2022. ISM Chair Spence: 17 out of 18 industries reported higher costs — ‘very, very concerning’ and ‘going in the wrong direction.’ Employment 48.7 (still contracting). New Orders 53.5 (down from 55.8 — demand sentiment mixed). The ISM delivered the purest STAGFLATION signal of the war: activity expanding BUT inflation SURGING across nearly every industry. Today’s oil surge to $112 means the Prices Paid component will likely accelerate FURTHER in April’s reading.

Trade Balance: −$57.3B (wider from −$54.5B). Factory Orders: POSTPONED to April 10.

The widening trade deficit reflects continued import demand despite the war. Factory Orders rescheduled by Census Bureau.

This week remaining: TOMORROW — GOOD FRIDAY, MARKETS CLOSED. NFP 8:30 AM to closed markets (consensus +57K, prior −92K, ADP +62K). ISM Non-Manufacturing also released. SUNDAY/MONDAY — April 6 energy strike deadline. MONDAY 4/7 — Markets reopen. Next week: April 9 — GDP Q4 Third Estimate + PCE February. April 10 — CPI March (THE inflation test).

5. THE DYRH READ

Regime: Stagflationary Re-Escalation — Trump Primetime Destroys 3-Session Rally. WTI +12.3%. Forced Liquidation Returns. All De-Escalation Trades Reversed. The speech contained nothing new but its tone was unambiguously escalatory. The market had priced ceasefire; it received ‘stone ages.’ Cross-asset confirmation is complete: oil surging, equities selling, bonds selling, gold liquidating, dollar surging, grains bid, energy only green sector. Textbook stagflationary panic. Confidence: High.

Yield Curve: Bear Steepener — 30Y Approaching 5.00% Crisis Zone Again.

All yields rising with the long end leading: 2Y +2.6 bps to 3.831%, 5Y +2.8 bps to 3.986%, 10Y +3.3 bps to 4.354%, 30Y +3.1 bps to 4.935%. The 30Y has retraced HALF of its 4-day decline in a single pre-market session, now approaching the 4.965%–5.00% crisis zone from Day 22. The oil surge is sending inflation expectations directly into the long end. MOVE at 90.19 (yesterday’s close) will gap higher at the open — the critical question is whether it breaks back above 95 or 100. Yesterday’s ‘bond crisis definitively broken’ call is now under DIRECT THREAT. If MOVE recaptures 100, the bond crisis was merely paused, not resolved.

Oil +12.3% — The Biggest Single-Session Surge Since Day 1.

WTI at $112.46 has reversed the entire de-escalation oil trade in a single session. The round-trip from $99.57 to $112.46 is a $12.89 swing. IEA’s Birol warned ‘April will be much worse than March’ because the pre-war tanker pipeline has been fully exhausted — 12M bpd supply loss is ‘more than two oil crises put together.’ Heating oil +13.54% leads the energy complex, meaning distillate supply chain pass-through to consumers and businesses is ACCELERATING. BofA now projects headline inflation to nearly 4% YoY. The $100 ‘qualitatively different damage’ threshold that was just crossed to the downside has been OBLITERATED to the upside.

Gold −$171 to $4,641.9 — Forced Liquidation Returns.

Gold crashing −3.56% while oil surges +12.3% is THE signature forced liquidation signal — margin calls on commodity positions forcing gold sales to cover energy exposure. Silver at −7.22% confirms the liquidation thesis — silver amplifies gold’s moves in liquidation environments due to lower liquidity. The 6-session metals recovery ($4,376 → $4,813, +$437) has been cut nearly in half in a single session. Gold at $4,641.9 is now only $265.9 above the $4,376 war low. If the selloff extends, a retest of the war low is on the table.

Equities: 3-Session Rally Destroyed — The Pattern Holds.

ES at 6,520 (−1.48%) has given back the entire Day 25 gain plus most of the Day 24 breakout. The S&P is now below the Day 24 close of 6,575 and threatening the Day 23 close (6,344 area). Russell −1.98% is the weakest US index — small caps most sensitive to oil/inflation/growth fears. Nikkei −3.46%, Kospi −4.47%. All 7 Mag 7 red (META −2.97% worst — Iran IRGC tech threat). The XLE swing from −3.74% (yesterday) to +2.71% (today) is a ±6.45% reversal — the most dramatic single-session sector reversal of the war. The ‘war trade’ is back: long energy, short everything else. SPHB −2.72% (worst factor), SPLV −0.63% (least damaged) = maximum risk-off. The de-escalation pattern break from Days 24-25 has been invalidated — seven relief bounces have now ALL reversed.

Maximum Gap Risk Weekend — The Most Dangerous 72 Hours of the War.

Good Friday closes markets tomorrow. Three catalysts converge over the weekend with no ability to trade: (1) NFP at 8:30 AM Friday to closed markets — consensus +57K would confirm labor resilience; a miss would amplify recession fear. (2) The April 6 energy strike deadline expires Sunday evening/Monday — if Trump follows through on threatening power plants and oil infrastructure, Monday’s open faces catastrophic escalation. (3) Iran’s response to the IRGC commander assassination and the speech’s ‘stone ages’ rhetoric is unknown. Markets reopen Monday April 7 absorbing ALL of these catalysts simultaneously. This is only the second time in 20+ years that NFP was released to closed US markets. Position sizing into close today is critical — the weekend carries unhedgeable gap risk of potentially historic magnitude.

6. THE GAME PLAN

Today’s Key Events: LAST FULL TRADING SESSION before the maximum gap risk weekend. Claims 202K already released (beat). No remaining scheduled data. The session is entirely driven by: (1) oil price action — does WTI hold $110+? (2) MOVE at the open — does it break back above 95/100? (3) VIX1D — backwardation would signal intraday crash dynamics. (4) positioning for the weekend — risk reduction into close. FRIDAY: Good Friday closed. NFP to closed markets. SUNDAY/MONDAY: April 6 deadline. MONDAY 4/7: Markets reopen.

The Bull Case:

Trump has a pattern of escalatory rhetoric followed by deadline extensions — the April 6 deadline has already been extended twice. The speech contained NO new information; it recycled existing rhetoric. If Trump posts ‘deal is close’ or ‘extending deadline’ on Truth Social, the entire move reverses in minutes. Jobless Claims 202K confirms labor market resilience — the economy is NOT in recession. ADP +62K, Retail Sales +0.6%, ISM 52.7 all beat this week — the economic foundation is stronger than the recession narrative. Pre-market moves can partially retrace at the open as liquidity normalizes. Oil at $112 may trigger demand destruction that self-limits the surge. US crude inventories +5.5M barrels (EIA Wednesday) was a bearish demand signal. Iran has incentives to negotiate before the April 6 deadline. The de-escalation thesis may have been premature but wasn’t wrong — ceasefire dynamics are real, just not imminent.

The Bear Case:

The speech delivered ESCALATION when the market was positioned for de-escalation — maximum pain. WTI +12.3% is the biggest single-session oil move since the war’s opening. Every de-escalation trade built over 3 sessions reversed in hours. Gold −3.56% with silver −7.22% = forced liquidation confirmed — not orderly selling. 30Y at 4.935% approaching 5.00% crisis zone. VIX back above 25. MOVE will gap higher — ‘bond crisis broken’ call threatened. Iran denied ceasefire — ‘false and baseless.’ Houthis entered the war (new front). IRGC threatening 18 US tech companies. IEA: ‘April will be much worse than March.’ BofA: inflation to 4%, global growth cut. ISM Prices Paid 78.3 = stagflation confirmed at the factory level. Good Friday creates 3-day gap risk with NFP + April 6 deadline + potential military escalation. The 7th relief bounce has reversed like all 6 before it. ES at 6,520 threatens to test the Day 23 close at 6,344.

Regime: Stagflationary Re-Escalation. The primetime speech contained nothing new but destroyed a rally built on ceasefire hope. Cross-asset confirmation is textbook: oil surging, equities selling, bonds selling, gold liquidating, dollar surging, energy only green sector, high-beta worst factor. The 3-session de-escalation rally is the 7th relief bounce to reverse. The session’s dominant question is NOT what the data says — the data has been uniformly strong all week. The question is whether Trump will follow through on the April 6 deadline or extend it again. And that question won’t be answered until the market is closed.

Watch List

MOVE at the open — bond crisis reassertion test

MOVE closed at 90.19 yesterday (below 100 for the 4th attempt). If it gaps back above 95 or 100 today, the ‘bond crisis definitively broken’ call is INVALIDATED and every prior break below 100 was a head-fake. The 30Y at 4.935% approaching 5.00% adds urgency. Watch whether the bear steepener accelerates through the session.

WTI above $110 — can it sustain?

$112.46 in pre-market. If oil holds above $110 through the session, the market is pricing Trump’s speech as a genuine escalation (not just rhetoric). If oil partially retraces below $105, the market is treating it as Trump’s typical negotiating bluster. IEA’s supply crunch warning provides fundamental support for elevated prices.

VIX1D at the open — backwardation test

VIX1D closed at 22.95. If it opens above VIX (27.58) = backwardation = intraday crash dynamics. This pattern characterized Days 21-22’s worst sessions. If VIX1D stays below VIX (contango), the selloff is orderly rather than panicked.

Gold — retest of $4,376 war low?

Gold at $4,641.9 is only $266 above the war low. The 6-session recovery ($4,376 → $4,813, +$437) has been cut nearly in half. If forced liquidation continues through the session and the weekend brings escalation, a retest of the war low is on the table. GVZ will surge at the open — watch whether it exceeds the 43.36 war high.

Close positioning — unhedgeable weekend risk

This is the most important close of the war for risk management. Good Friday + NFP to closed markets + April 6 deadline = 72 hours of catalysts with zero ability to trade. Expect aggressive risk reduction into the close. The VIX term structure, put/call ratios, and S&P futures open interest will reveal how the market is positioning for the gap.

Morning check: seven relief bounces. Seven reversals. The market priced ceasefire; Trump delivered stone ages. WTI +12% in a single session. Gold crashing back toward the war low. Silver in freefall. Every metric of de-escalation — VIX below 25, MOVE below 100, breadth at 77, correlation below 30 — built over three careful sessions, destroyed in nineteen minutes of primetime television. The data this week has been uniformly strong: ADP +62K, Retail Sales +0.6%, ISM 52.7, Claims 202K. The economy is holding. But ISM Prices Paid at 78.3 says the inflation damage is accelerating even as activity expands — textbook stagflation at the factory level. And now the market faces its most dangerous weekend: Good Friday, NFP to closed markets, and the April 6 deadline arriving while the trading floor is dark. The hard data says resilience. The speech says stone ages. The gap risk says plan accordingly.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.