☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: RISK-ON — ES 7,145.00 (+0.63%). TRUMP EXTENDED THE CEASEFIRE INDEFINITELY TUESDAY AFTERNOON — HOURS BEFORE EXPIRATION. IRAN REFUSED TO SEND DELEGATION. VANCE TRIP POSTPONED. BLOCKADE CONTINUES. THE WAR DID NOT RE-ESCALATE. WTI $90.80 (+1.26%) RISING AS HORMUZ REMAINS CONTESTED. MOVE 70.78 (+4.23%) EXPANDING TOWARD BASELINE — THE BOND MARKET’S CAPITULATION IS BEING TESTED. BTC $78,740 (+4.90%) SURGING. NIKKEI +1.77%. RUSSELL +0.86% OUTPERFORMING. BULL STEEPENER — ALL YIELDS FALLING. TSLA REPORTS AFTER CLOSE TONIGHT. GOOGL / MSFT / META / CAT TOMORROW. ITA −3.78% DEFENSE CRATER. XLRE −1.93% CRATERING.

The ceasefire did not expire. In the most significant diplomatic development since the April 8 original ceasefire announcement, President Trump extended the ceasefire indefinitely on Tuesday afternoon — just hours before it was set to expire at approximately 8 PM ET. Trump wrote on Truth Social that he was acting at Pakistan’s request, citing Iran’s ‘seriously fractured’ government needing time to develop a ‘unified proposal.’ The US military blockade of Iranian ports CONTINUES. VP Vance’s planned trip to Islamabad was postponed indefinitely — Iran had refused to send a delegation, notifying Pakistan it would not participate in talks and citing the US blockade as an ‘act of war’ and ceasefire violation. Pakistani PM Sharif thanked Trump and expressed hope for ‘a comprehensive Peace Deal during the second round of talks scheduled at Islamabad.’ No date for those talks has been set.

The market read is clear: NO IMMEDIATE RESUMPTION OF COMBAT (bullish) + NO CLEAR PATH TO PEACE (vol-expanding) + BLOCKADE CONTINUES WITH HORMUZ CONTESTED (oil-rising). This is the ‘frozen conflict’ scenario — hostilities suspended but unresolved, with the blockade as the primary pressure mechanism. The equity tape loved it: ES +0.63%, Russell +0.86% outperforming, Nikkei +1.77% (Japan’s largest single-session rally in over a week). BTC surged +4.90% to $78,740 — the largest single-session crypto move since the war’s early days. But MOVE expanded +4.23% to 70.78, approaching the 73.21 pre-war baseline from below — the bond market is NOT comfortable with the ambiguity even as equities celebrate. The MOVE trajectory: 65.70 (Friday floor) → 65.70 → 67.90 → 70.78 — three consecutive sessions of expansion after four sessions of capitulation-level compression. If MOVE crosses back above 73.21, the capitulation thesis from last week formally reverses.

The equity tape structure has shifted dramatically. XLRE −1.93% is the worst sector, cratering from its seven-session #1 perch. XLE +1.45% leads all sectors — the energy-defense trade is alive as the blockade continues and Hormuz remains contested. ITA −3.78% (defense CRATERING for the second consecutive session — the ceasefire extension removes the combat-resumption premium). Mag 7 at 2 green / 5 red: MSFT +1.46% leading (into tomorrow’s earnings), AMZN +0.66%. AAPL −2.52% is the worst Mag 7 name (now decisively the weakest over the past two weeks). TSLA −1.55% positioning cautiously into tonight’s earnings. GOOG −1.47% and NVDA −1.08% soft. The index is green on breadth — Russell outperforming, Dow bid — not on Mag 7.

The Number That Matters: MOVE 70.78 (+4.23%). The Bond Market’s Capitulation Is Being Tested. Three Consecutive Sessions Of Expansion From The 65.70 Floor. The 73.21 Pre-War Baseline Is Now 2.43 Points Away.

MOVE has expanded from the 65.70 post-ceasefire-extension floor to 70.78 in three sessions. The 73.21 pre-war baseline is now only 2.43 points above. If MOVE crosses 73.21 this week — during TSLA tonight, GOOGL/MSFT/META tomorrow, or on any geopolitical catalyst — the bond market’s capitulation thesis from Days 35-37 formally reverses and the war’s rates-vol overhang returns. The MOVE expansion is happening DESPITE the ceasefire extension (which should be rates-vol-compressing) because: (1) The extension is ambiguous — no talks scheduled, Iran not participating, blockade continues; (2) The Warsh confirmation hearing introduced governance uncertainty (Tillis blocking, Powell investigation, contested succession); (3) The front end repriced hawkishly on the Retail Sales beat. MOVE vs ES is the week’s defining divergence: equities at +0.63% while rates-vol expands +4.23% is unsustainable. One will capitulate.

The Setup: Bull Steepener — Risk-On — Energy Steady. Ceasefire Extended Indefinitely. TSLA Tonight. GOOGL/MSFT/META Tomorrow. MOVE Approaching Baseline. The Market Is Pricing ‘Frozen Conflict’ — Hostilities Suspended But Unresolved.

2. OVERNIGHT SESSION RECAP

Tuesday Cash Session (Day 38 Close)

Tuesday’s cash session was defined by the ceasefire-extension announcement in the afternoon. The morning opened with the UNH beat and Retail Sales blowout providing a strong fundamentals floor. The Warsh confirmation hearing at 10 AM proceeded without major fireworks — Warsh emphasized a ‘leaner, more disciplined Fed’ and signaled he would not pre-commit to rate cuts, consistent with his hawkish reputation. The Tillis block remains unresolved. The curve settled in a BEAR FLATTENER with the front end rising sharply (2Y +5.8 bps — the largest single-session 2Y move of the post-ceasefire period) on the strong Retail Sales data + Warsh hawkish tone. Then Trump’s ceasefire extension announcement in the afternoon reversed some of the bear-flattener dynamics — the war not re-escalating removed the tail risk and allowed the long end to stabilize.

Overnight — Ceasefire Extended, Iran Refused Talks

TUESDAY AFTERNOON: Trump announced on Truth Social that he was extending the ceasefire indefinitely at Pakistan’s request, citing Iran’s ‘fractured’ government. The extension came hours before the deadline. TUESDAY EVENING: The White House confirmed Vance would NOT travel to Islamabad. Iran’s state television confirmed NO Iranian delegation had visited Islamabad. Iran’s FM Araghchi called the blockade an ‘act of war’ and a ceasefire violation. Pakistan’s PM Sharif thanked Trump and called for continued diplomatic efforts. The extension is open-ended with no scheduled talks — this is a ‘frozen conflict’ framework with the blockade as the primary pressure mechanism. WTI stabilized at $90.80 (+1.26%) — the oil market is pricing the blockade continuing without combat escalation.

Asia-Pacific

Nikkei +1.77% to 59,555 — Japan’s LARGEST single-session rally in over a week, driven by the ceasefire extension removing overnight combat-resumption risk. Topix −0.40% diverging (domestic Japan weakness vs export-sector strength). The Nikkei-Topix divergence reflects concentrated buying in large-cap export/tech names on the de-escalation read rather than broad domestic risk appetite.

Europe

DAX −0.17% to 24,402. EuroStoxx 50 −0.19% to 5,880. Europe SOFT despite the ceasefire extension — the European tape is pricing the ‘frozen conflict’ scenario as net-negative for European energy costs and industrial margins. The blockade continuing with Hormuz contested means European refineries face sustained supply-chain premium. UK CPI at 2 AM printed 3.1% vs 3.3% consensus — the UK inflation undershoot is a modest positive for BoE easing expectations but didn’t move European equities.

US Pre-Market

Day 55 of Operation Epic Fury. Q2 Day 16. Wednesday — TSLA earnings day. FOMC blackout active.

US FUTURES BROADLY GREEN: ES 7,145.00 (+0.63%), NQ 26,848.25 (+0.80% — LEADING for the first time this week), RTY 2,799.00 (+0.86% — OUTPERFORMING), YM 49,656 (+0.64%). The NQ leading ES is the MSFT +1.46% pre-earnings bid driving Nasdaq outperformance. Russell at +0.86% leading all indices — the third session of small-cap outperformance in four days. The ‘frozen conflict’ scenario is being read as: lower tail risk = higher small-cap/cyclical risk appetite.

MAG 7 TWO GREEN / FIVE RED: MSFT +1.46% leading (cumulative multi-day software reflation into tomorrow’s earnings — MSFT has been the strongest Mag 7 name over the past two weeks). AMZN +0.66%. META −0.31% (consolidating into tomorrow’s earnings). NVDA −1.08%. GOOG −1.47% (positioning cautiously into tomorrow’s earnings). TSLA −1.55% (cautious into TONIGHT’s earnings — Q1 deliveries missed, the AI5/AI6 narrative is the bull case). AAPL −2.52% (WORST Mag 7 — Apple is now the structural weak link, red in 5 of the past 7 sessions). The MSFT-AAPL divergence (+1.46% vs −2.52% = 398 bp spread) is the widest single-session Mag 7 spread of the past week and signals the software-over-hardware rotation is intensifying.

SECTORS — XLE LEADING, XLRE CRATERING: XLE +1.45% (energy leading on blockade-continues/oil-rising narrative). XLK +0.08% flat. Everything else RED. XLF −0.63%. XLP −0.67%. XLY −0.75%. XLB −0.88%. XLV −1.02% (despite yesterday’s UNH beat — sell-the-news confirmed). XLC −1.34%. XLI −1.41% (industrial weakness — defense read-through). XLU −1.75%. XLRE −1.93% (the WORST sector, cratering from the seven-session #1 position). ITA −3.78% (defense CRATERING for the second straight session — the ceasefire extension removes the combat-resumption premium that had supported defense names). Only XLE and XLK in the green — the narrowest sector leadership of the week.

FACTORS 1/12 GREEN: VLUE +0.08% the only green factor. Everything else red: SPHB −0.33%, USMV −0.69%, SPLV −1.10%, MTUM −0.72%. USMV-SPHB spread −0.35% (still risk-on technically, but barely). The factor tape is the weakest since Monday’s defensive rotation. The narrow leadership (only 2 sectors green, only 1 factor green) while the index is +0.63% tells you this is a futures-driven overnight bid that hasn’t been confirmed by broad cash-session internals.

3. THE PRIOR DAY’S REGIME (34 Macro Price, Strength & Momentum Rankings)

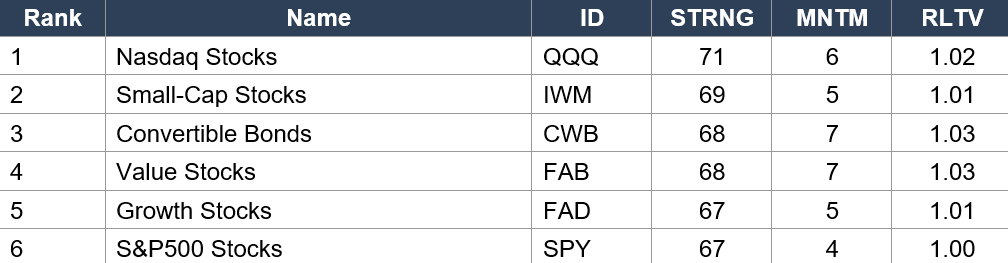

34 Macro Price, Strength & Momentum Rankings — Daily Close, Tuesday April 21. SPY Baseline: STRNG 67 | MNTM +4 | RLTV 1.00.

Asset Classes — Leaders

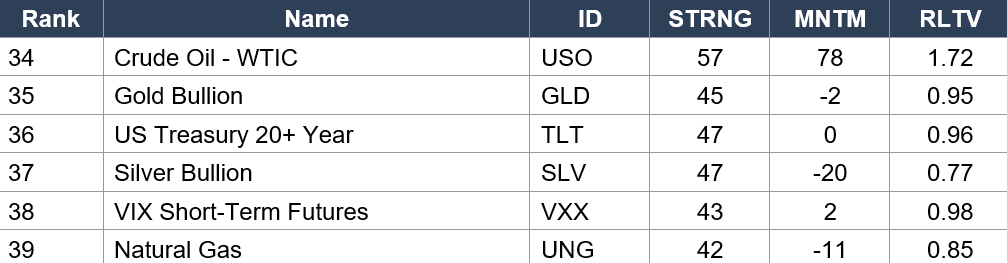

Asset Classes — Laggers

Regime signal: THE STRUCTURAL ROTATION DEEPENS. QQQ (rank 1, STRNG 71) holds #1 for a third consecutive data set. Small-Cap (IWM rank 2, STRNG 69) holds rank 2 — small-cap leadership now firmly embedded in three consecutive data sets. Value Stocks (FAB rank 4, MNTM +7, RLTV 1.03) enters the top 5 ahead of Growth (FAD rank 5) — value-over-growth rotation captured. CRITICAL ENERGY: Crude Oil (USO rank 34, MNTM +78, RLTV 1.72!!!) — momentum ACCELERATED further from +69 to +78, RLTV from 1.65 to 1.72. This is the most extreme single-asset momentum reading of the ENTIRE war in ANY data set. Gasoline (UGA rank 10 — ENTERED Leaders category, MNTM +60, RLTV 1.54). The energy complex’s relative strength is now so extreme it is distorting the data. PRECIOUS METALS COLLAPSE: Silver (SLV rank 37, MNTM −20, RLTV 0.77) crashed from 1.01 to 0.77. Gold (GLD rank 35, MNTM −2, RLTV 0.95) weak. Platinum (PPLT rank 33, MNTM −18, RLTV 0.79). The entire precious metals complex is being liquidated as the ceasefire extension removes safe-haven urgency. CRYPTO CONTINUES WEAK: Bitcoin (IBIT rank 15 — moved to Middle from Leaders, MNTM −16, RLTV 0.81) despite today’s +4.90% pre-market surge. Ethereum (ETHA rank 25, MNTM −23, RLTV 0.74) remains the weakest major asset class by RLTV.

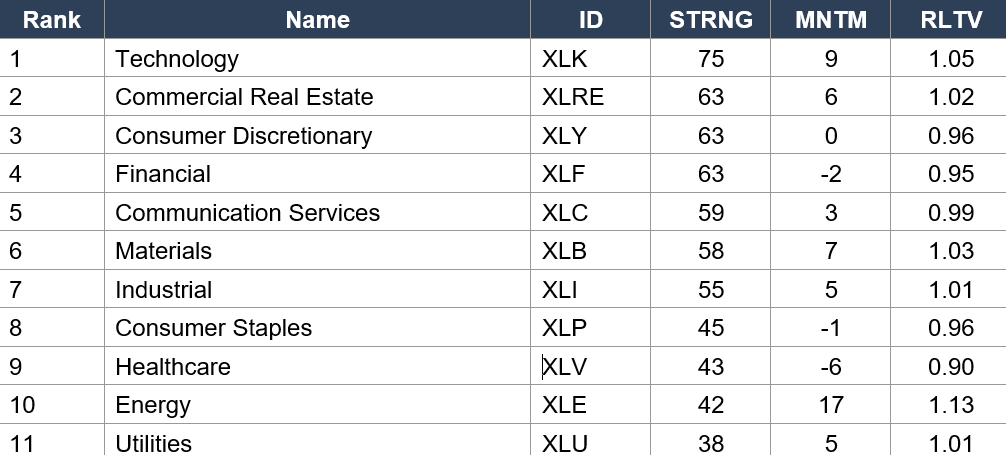

Sector ETFs — Full Ranking

Regime signal: TECHNOLOGY (XLK rank 1, STRNG 75, MNTM +9, RLTV 1.05) has DETHRONED Commercial Real Estate for the #1 sector spot. This ends XLRE’s SEVEN consecutive data-set leadership streak — the longest of the war. The catalyst: MSFT’s multi-day software reflation + SOXX semis broadening + the ceasefire extension removing rate-sensitive REIT demand (XLRE at −1.93% today confirms the rotation). XLRE (rank 2, STRNG 63) dropped 13 STRNG points in a single session (76 → 63) — the steepest single-session STRNG decline of any sector in the war. XLY (rank 3 — entered Leaders) and XLF (rank 4) are now both below 1.00 RLTV — the consumer/financial rotation is stalling. CRITICAL: Energy (XLE rank 10, MNTM +17, RLTV 1.13 — HIGHEST RLTV of any sector for the THIRD consecutive data set). Energy remains the paradox: weakest absolute strength (STRNG 37→42), strongest relative momentum. Health-Care (XLV rank 9, MNTM −6, RLTV 0.90 — LOWEST sector RLTV) despite UNH’s 9.4% beat yesterday — the sell-the-news dynamic confirmed in the data. Utilities (XLU rank 11 — FELL to last place below Energy for the first time) with STRNG cratering to 38.

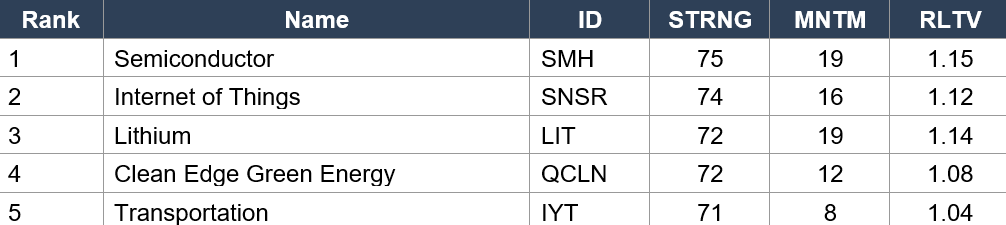

Industry ETFs — Top Leaders

Industry ETFs — Notable Shifts

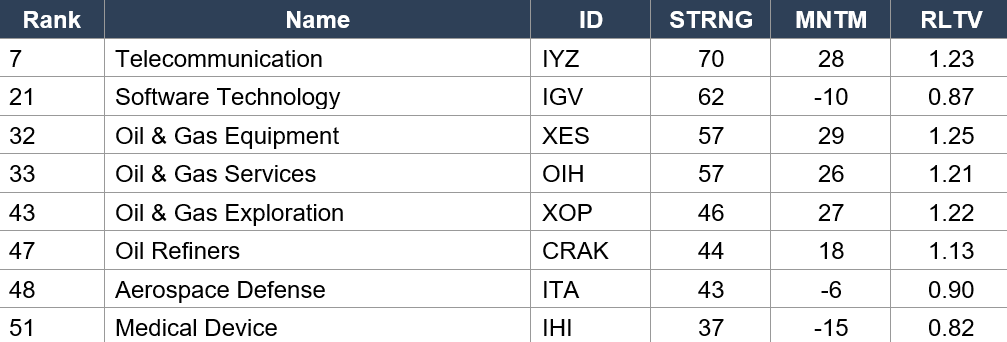

Regime signal: Semiconductor (SMH rank 1, STRNG 75, MNTM +19, RLTV 1.15) holds #1 industry for the FOURTH consecutive data set — the most dominant industry-leadership streak of the war. RLTV at 1.15 is the highest of any industry. Lithium (LIT rank 3, MNTM +19, RLTV 1.14) ties SMH for highest MNTM in the Leaders group — battery materials leadership structural. Telecom (IYZ rank 7, MNTM +28, RLTV 1.23 — highest RLTV of any industry) continues its surge. CRITICAL SOFTWARE: IGV (rank 21, MNTM −10, RLTV 0.87) remains broken — the recovery that peaked at RLTV 1.09 has fully reversed. IGV is now in the Middle tier, not Leaders. MSFT’s +1.46% pre-market today has not yet been captured in this data. ENERGY INDUSTRY COMPLEX: The entire energy value chain has RLTV above 1.10: XES 1.25, OIH 1.21, XOP 1.22, CRAK 1.13, BOAT (Shipping) 1.16. The frozen-conflict scenario with sustained blockade is the most bullish possible configuration for energy-service companies. DEFENSE CRATER: Aerospace-Defense (ITA rank 48, MNTM −6, RLTV 0.90) fell from rank 39 as the ceasefire extension removes combat-resumption premium. Medical Device (IHI rank 51, MNTM −15, RLTV 0.82 — LOWEST RLTV of any industry) is the structural healthcare laggard.

4. MORNING DATA REACTION

No US Morning Economic Data Scheduled. Only Event: Lagarde 1:30 PM.

No US economic data is scheduled today. UK CPI at 2 AM printed 3.1% vs 3.3% consensus — a miss that supports BoE easing expectations but is not directly material to the US regime. The only scheduled event is ECB President Lagarde speaking at 1:30 PM — her interpretation of the frozen-conflict scenario and its implications for European energy inflation will be the macro catalyst. TSLA earnings after close are the session’s dominant event.

Tuesday Afternoon — Trump Extended Ceasefire Indefinitely. Iran Refused Talks. Vance Postponed. Blockade Continues.

The most significant diplomatic development since the April 8 original ceasefire announcement. Trump cited Iran’s ‘seriously fractured’ government and Pakistan’s request. The extension is open-ended with NO scheduled talks, NO Iranian delegation confirmed, and the US blockade CONTINUING. Iran’s FM Araghchi called the blockade ‘an act of war’ and a ceasefire violation. Iran signaled it will not negotiate while the blockade persists — a deadlock. Vance remained in Washington for White House meetings instead of flying to Islamabad. The ‘frozen conflict’ framework is now the operative scenario: hostilities suspended, blockade active, Hormuz contested, no diplomatic timeline. For markets: the tail risk of combat resumption is removed (bullish for equities, bearish for defense), but the supply-chain disruption from the blockade persists (bullish for energy, bearish for European industrials), and the governance uncertainty from the ambiguous terms expands rates volatility (MOVE rising).

Tuesday Pre-Market Recap — UNH +9.4% Beat, Retail Sales Core +1.9% vs +1.4%, Warsh Hearing Proceeded Without Market-Moving Surprises.

Yesterday’s Morning Bell covered these in full. UNH’s raised guidance to >$18.25 and Retail Sales core +1.9% established the strongest consumer/corporate fundamentals floor of the war. The Warsh hearing at 10 AM proceeded as expected — Warsh signaled a ‘leaner’ Fed, did not pre-commit to rate cuts, and the Tillis block remained unresolved. Powell’s term expires May 15. The hearing did not produce a market-moving headline but sustained the governance-uncertainty premium that is contributing to MOVE expansion.

5. THE DYRH READ

Regime: Bull Steepener — Risk-On — Energy Steady. Ceasefire extended indefinitely. No immediate combat resumption (bullish). No clear path to peace (vol-expanding). Blockade continues with Hormuz contested (energy-rising). MOVE expanding toward 73.21 baseline — the bond market’s capitulation is being tested. ES +0.63% with Russell +0.86% outperforming. BTC +4.90%. Factor tape 1/12 green — the narrowest of the week. Only XLE and XLK in green sectors. The equity rally is futures-driven overnight, not confirmed by broad internals. TSLA tonight. GOOGL/MSFT/META tomorrow. Confidence: MODERATE — ceasefire extension removes tail risk but MOVE expansion + narrow internals + two consecutive mega-earnings nights create elevated single-name event risk.

Yield Curve: BULL STEEPENER — All Yields Falling. The Ceasefire Extension Removed The Long-End Tail Risk.

All yields falling: 2Y −1.2 bps to 3.773%, 5Y −1.6 bps to 3.901%, 10Y −1.7 bps to 4.282%, 30Y −1.8 bps to 4.888%. The long end is falling faster than the front on a proportional basis — the ceasefire extension removed the combat-resumption tail that had sustained the long-end premium. The bull steepener is constructive for equities (falling rates support multiples) but is being offset by MOVE expansion (falling rates WITH rising rates-vol is a divergence that typically resolves to the vol side). The 2Y at 3.773% is 1.5 bps ABOVE Friday’s 3.758% — the front-end hawkish repricing from the Retail Sales beat + Warsh hearing is being partially retained even as the long end eases.

MOVE 70.78 (+4.23%) — Three Consecutive Sessions Of Expansion. Approaching 73.21 Baseline. The Capitulation Is Being Tested.

MOVE trajectory: 65.70 (Friday floor, post-Hormuz-opening crash) → 65.70 (Monday) → 67.90 (Tuesday morning) → 70.78 (Wednesday). Three consecutive sessions of expansion totaling +5.08 points from the floor. The 73.21 pre-war baseline is now 2.43 points above. The expansion is happening despite: (1) Ceasefire extended (should compress rates-vol), (2) No combat resumption (should compress rates-vol), (3) All yields falling (should compress rates-vol). The fact that MOVE is expanding INTO these normally-compressing catalysts says the bond market is pricing: Warsh governance uncertainty + Retail Sales hawkish front-end repricing + ambiguous frozen-conflict terms + TSLA/GOOGL/MSFT/META earnings binary. If MOVE crosses 73.21 this week, the entire post-Day-35 capitulation narrative reverses. If MOVE holds below 73.21 through Thursday’s mega-earnings, the capitulation is intact and merely being tested.

ES 7,145.00 (+0.63%) — Constructive But Below The 7,165.50 Tuesday Intraday High. +3.8% Above Pre-War Baseline.

ES at 7,145.00 is green but notably BELOW Tuesday’s 7,165.50 close that was reached on the UNH/Retail Sales/ceasefire-extension triple catalyst. The overnight futures have not extended Tuesday’s rally — they’ve pulled back $20.50 from the session high. This is consistent with the narrow internals (1/12 factors green, 2/11 sectors green) — the futures bid is being driven by the ceasefire-extension headline rather than broad risk appetite. Russell at +0.86% outperforming is the bull case: small-caps are treating the frozen-conflict scenario as lower-tail-risk = higher risk appetite. Nikkei +1.77% confirms the global read. But DAX −0.17% and EuroStoxx −0.19% say European markets disagree — the blockade continuing is net-negative for European energy costs.

BTC $78,740 (+4.90%) — The Largest Single-Session Crypto Move Since The War’s Early Days.

BTC surged from $75,015 to $78,740 — a +$3,725 / +4.90% move that is the largest single-session crypto gain since the early weeks of the conflict. The catalyst: the ceasefire extension removing the tail risk that had been pressuring crypto alongside all risk assets over the weekend. BTC is now +$18,940 / +31.7% from the ~$59,800 pre-war level — the best-performing major asset class of the entire war on a cumulative basis. But the 34 Macro rankings show IBIT at RLTV 0.81 and ETHA at 0.74 — the data has not yet captured today’s rally and the prior data set reflected the weekend crash. Tomorrow’s data will show whether the crypto rally is real or a dead-cat bounce.

WTI $90.80 (+1.26%) — Oil Rising As Blockade Continues. The Frozen-Conflict Scenario Is Bullish For Energy.

WTI at $90.80 (+1.26%) with Brent at $99.75 (+1.29%). The frozen-conflict scenario with the US blockade continuing and Hormuz contested is the most bullish possible oil-market outcome short of full Hormuz closure: supply remains constrained, no diplomatic timeline for resolution, but no combat escalation that would produce a demand-destruction spiral. Cumulative WTI from pre-war $67.02 is +$23.78 / +35.5% — oil premium has re-expanded from Friday’s $81 crash back toward the mid-war range. Brent approaching $100 — if Brent clears $100, the narrative shifts from ‘war premium’ to ‘sustained supply constraint.’ XLE at +1.45% leading sectors — the energy-sector bid is tracking the oil-market read of the frozen-conflict scenario.

6. THE GAME PLAN

Today’s Key Events: No US data. Lagarde 1:30 PM. TSLA Q1 AFTER CLOSE — tonight’s dominant event. TOMORROW: GOOGL / MSFT / META / CAT after close — the MEGA earnings day. FRIDAY: PG, Colgate-Palmolive. FOMC blackout active through April 29. Ceasefire extended indefinitely — no scheduled talks.

The Bull Case:

Ceasefire extended indefinitely — no immediate combat resumption. ES +0.63% with Russell +0.86% outperforming and Nikkei +1.77%. Bull steepener — all yields falling. BTC +4.90% surging. Small-cap outperformance for third session in four. 34 Macro rankings show QQQ #1, IWM #2, XLK dethroned XLRE for #1 sector, SMH holds #1 industry for fourth straight set. UNH beat + Retail Sales blowout established the strongest fundamentals floor of the war (six consecutive data beats). MSFT +1.46% into tomorrow’s earnings — if MSFT delivers, the software reflation extends. The frozen-conflict scenario removes tail risk while preserving the reflation trade. Energy RLTV 1.13-1.72 across the complex — energy equities positioned for sustained outperformance if blockade continues.

The Bear Case:

MOVE expanding three consecutive sessions to 70.78 — only 2.43 points from reversing the capitulation at 73.21 baseline. Factor tape 1/12 green — the weakest of the week. Only 2/11 sectors green — narrowest leadership. The ES +0.63% is futures-driven, not confirmed by broad internals. Europe soft (DAX −0.17%) — the frozen-conflict scenario is net-negative for European energy costs. XLRE −1.93% — the seven-session sector leader is cratering. ITA −3.78% — defense cratering removes the geopolitical-hedge support. AAPL −2.52% is the worst Mag 7 (5 of 7 sessions red) — Apple is the structural weak link. TSLA −1.55% cautious into tonight’s earnings after Q1 delivery miss. IGV at RLTV 0.87 — software recovery broke. Iran refused to negotiate and called the blockade an ‘act of war’ — the diplomatic deadlock could persist indefinitely, gradually re-escalating through proxy actions. The 34 Macro rankings show precious metals collapsing (SLV 0.77, PPLT 0.79) — the safe-haven bid is being liquidated, meaning there’s no natural hedge if the frozen conflict thaws into hot conflict.

Regime: Bull Steepener — Risk-On — Energy Steady. The ceasefire extension created a ‘frozen conflict’ framework that removes combat tail risk while preserving supply-chain disruption. Equities love it (ES +0.63%, Russell +0.86%), energy loves it (XLE +1.45%, oil +1.26%), defense hates it (ITA −3.78%), and the bond market is uncertain (MOVE +4.23%). The resolution of this tension depends on: (1) Whether MOVE crosses back above 73.21 — if yes, the capitulation reverses; (2) TSLA tonight and GOOGL/MSFT/META tomorrow — if earnings deliver, the narrow internals broaden; if earnings disappoint, the MOVE expansion accelerates; (3) Whether Iran re-engages diplomatically or the frozen conflict hardens into permanent blockade. The market enters TSLA earnings tonight at maximal divergence: bullish headline (ceasefire extended, ES green, BTC surging) vs bearish internals (1/12 factors green, 2/11 sectors green, MOVE expanding). The earnings resolution determines which side wins.

Watch List

TSLA Q1 After Close Tonight — The Session’s Dominant Binary

Tesla reports Q1 after close. TSLA at $386.42 (−1.55%). Q1 deliveries missed expectations. The bull case is AI5/AI6 chip development + autonomous vehicle progress + Optimus robot timeline. The bear case is production miss + margin pressure + Musk distraction. Street consensus ~$0.37 EPS. Tonight is both TSLA earnings AND the first full trading session in the frozen-conflict framework — positioning complexity is elevated.

GOOGL / MSFT / META / CAT Thursday After Close — The Mega Earnings Day

Three Mag 7 names + the bellwether industrial report on the same evening. MSFT at +1.46% today is the pre-earnings bid; META at −0.31% and GOOG at −1.47% are cautious. This is the most concentrated Mag 7 earnings event of the war. If all three deliver: the equity re-rating extends with definitive corporate validation. If any disappoints: the MOVE expansion above 73.21 becomes the dominant narrative.

MOVE 73.21 Baseline — The Week’s Defining Technical Level

MOVE at 70.78, three consecutive sessions of expansion, 2.43 points from the pre-war baseline. If MOVE crosses 73.21 this week, the post-Day-35 bond-market capitulation formally reverses. If MOVE holds below through mega-earnings, the capitulation is tested and confirmed. Every cross-asset positioning decision this week is downstream of this single metric.

Frozen Conflict Duration — The New Structural Question

The ceasefire extension creates an indefinite ‘frozen conflict’ with no diplomatic timeline. The longer the frozen state persists, the more the blockade becomes the ‘new normal’ and oil prices embed the supply constraint permanently. Goldman’s pre-conflict Brent average forecast was $85 — current Brent at $99.75 says the market is pricing ~$15/b of permanent blockade premium. If Iran re-engages diplomatically, that premium compresses. If Iran escalates through proxy or direct action, the premium expands above $100.

Morning check: Day 55. The war is fifty-five days old. Trump extended the ceasefire indefinitely yesterday — the war did not re-escalate. Iran refused to talk. The blockade continues. The ‘frozen conflict’ framework is now the operative scenario. Equities love it: ES +0.63%, Russell +0.86%, BTC +4.90%, Nikkei +1.77%. Energy loves it: XLE +1.45%, WTI $90.80. Defense hates it: ITA −3.78%. The bond market is uncertain: MOVE +4.23% to 70.78, approaching the 73.21 baseline that — if crossed — reverses the capitulation thesis. The 34 Macro rankings show XLK dethroned XLRE for #1 sector after seven sessions of XLRE dominance. SMH holds #1 industry for the fourth set. Energy RLTV continues to surge (USO 1.72, XES 1.25, OIH 1.21). Software remains broken (IGV 0.87). The factor tape is 1/12 green — the weakest of the week. Only two sectors green. The equity rally is futures-driven, not confirmed by broad internals. Tonight: TSLA. Tomorrow: GOOGL, MSFT, META, CAT. The earnings determine whether the frozen-conflict equity rally has corporate-fundamentals support or is a positioning trade into binaries. MOVE is the arbiter. Take the ceasefire extension as the floor. Watch the 73.21 level as the ceiling. Let the earnings resolve the divergence.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.