☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: NFP +178K BLOWOUT ABSORBED OVER 3-DAY WEEKEND. TRUMP EXTENDS DEADLINE (3RD TIME). MOVE CRASHES TO 81.78 — NEW WAR LOW. ISM SERVICES MISSES AT 10 AM. OIL-EQUITY DECOUPLING CONFIRMED.

Markets reopen after the most consequential 3-day weekend of the war. NFP +178,000 — three times consensus — was released to closed equity markets on Good Friday and the market has absorbed it CONSTRUCTIVELY: ES +0.39%, NQ +0.78%, all 7 Mag 7 green, gold recovering, oil pulling back. Trump extended the April 6 energy strike deadline to Tuesday 8 PM ET — his 3rd extension of the same deadline. The market reads this as confirmation that energy strike threats are negotiating tools, not military plans. Iran formally rejected a temporary ceasefire, but Pakistan/Egypt/Turkey mediators are pushing a ~45-day ceasefire framework.

MOVE has crashed to 81.78 — a NEW WAR LOW and the 7th consecutive session of decline. The trajectory from 115.02 (Day 21 war high) to 81.78 in 6 sessions (−28.9%) represents the most aggressive bond volatility normalization of the conflict. MOVE is now only 8.6 points above the pre-war 73.21. The bond market is approaching FULL NORMALIZATION despite $110 oil. This is the most structurally bullish signal of the entire war.

ISM Services just released at 10:00 AM: 54.0 — MISSED the 55.0 consensus and DOWN from February’s 56.1. This is the first sign that the war’s economic damage is reaching the services sector, which represents ~80% of the US economy. The miss is significant because services had been the resilient pillar — ISM Manufacturing showed expansion with surging prices (78.3 Prices Paid), but services was expected to hold strong. A deceleration from 56.1 to 54.0 (still in expansion, but the slowest pace since January) suggests the oil shock and war anxiety are now filtering into the broader economy. The miss partially offsets the NFP blowout — the labor market added 178K jobs in a month where services activity was decelerating.

European banks are CLOSED for Easter Monday — the full European reaction to the NFP, the deadline extension, and the ISM miss comes Tuesday. Additional weekend developments: Trump’s Truth Social post (’Open the Fuckin’ Strait, you crazy bastards’) was maximally aggressive in tone but the deadline EXTENSION itself is dovish. Israeli-US strikes continued — overnight strikes killed children in Tehran. Iran struck a residential building in Haifa (2 killed) and missiles hit a Tel Aviv school. The war continues at full intensity even as the market prices post-war normalization.

The Number That Matters: MOVE at 81.78 — new war low, 7th consecutive decline, only 8.6 points above pre-war.

This is the session’s structural anchor. MOVE’s decline from 115.02 to 81.78 in 6 sessions means the bond market has nearly FULLY normalized despite WTI at $110, Brent near $109, ISM Prices Paid at 78.3, and an active war. The bond market is telling you: the FINANCIAL CRISIS component of the war is over. What remains is the INFLATION LEGACY — and that’s a different, slower-burning problem that doesn’t require crisis-level volatility premiums. MOVE approaching pre-war levels with $110 oil is the single most powerful signal that the market has structurally repriced the war from ‘crisis’ to ‘elevated risk environment.’

The Setup: NFP Blowout Absorbed — Post-War Repricing Accelerates. ISM Services Miss Adds Complexity. Oil-Equity Decoupling Confirmed.

The oil-equity decoupling from Day 26 is CONFIRMED and extending. Thursday’s session showed S&P +0.11% with WTI +11.41% — equities have structurally stopped trading inversely with oil. Today continues the pattern: ES +0.39% while WTI −1.03%. The market has decoupled oil’s level from equity valuations, instead pricing the war’s END as the dominant equity driver regardless of where oil trades. The ISM Services miss at 54.0 adds nuance — if services decelerate further toward 50, the ‘Goldilocks with inflation sting’ narrative shifts toward outright stagflation in the services economy. Tuesday’s deadline is the next binary catalyst.

2. OVERNIGHT SESSION RECAP

Asia-Pacific

Nikkei +0.86%, TOPIX +0.44%. Japan absorbed the NFP blowout constructively — the +178K headline is bullish for global risk appetite, and AHE cooling to 3.5% reduces the tightening scare. Asian markets opened after digesting 3 days of catalysts and chose to price the NFP beat + deadline extension as net positive.

Europe

European banks CLOSED for Easter Monday. DAX and Euro Stoxx futures showing −0.72% (stale delayed data from Thursday). The full European reaction — to the NFP blowout, the deadline extension, and today’s ISM Services miss — will arrive Tuesday. European markets have additional sensitivity to the war’s energy dimension given import dependence.

US Pre-Market

Day 38 of Operation Epic Fury. Q2 Day 4. Markets reopen after the maximum gap risk weekend that was flagged in every report last week.

NFP DETAIL: +178,000 jobs in March — the most since December 2024 and three times the 57-60K consensus. Healthcare +76K (Kaiser strike reversal drove ~35K as nurses returned). Construction +26K. Transportation/warehousing +21K. Manufacturing +15K. Federal government −18K (continuing decline). Financial activities −15K. Unemployment rate 4.3% (unchanged). Average Hourly Earnings +3.5% YoY — DOWN from 3.8%, the lowest since August 2024. This is the Goldilocks read: hot headline employment + cooling wages = the Fed can stay on hold without fearing a wage-price spiral. January revised UP +34K to +160K. February revised DOWN −41K to −133K (net −7K).

ISM SERVICES (Released 10:00 AM today): 54.0 — MISSED 55.0 consensus. DOWN from 56.1 in February. The services sector decelerated to its slowest expansion since January. This is the first ISM Services print covering a full month of war. The miss matters because services are ~80% of GDP — if the oil shock and war anxiety are pulling services down from 56 to 54, the deceleration trend could accelerate in April as $110+ oil and $4+/gallon gas continue to squeeze consumer budgets. The NFP showed 178K jobs created in March, but ISM Services shows the sector those jobs serve is losing momentum.

TRUMP DEADLINE EXTENSION: The April 6 energy strike deadline has been pushed to TUESDAY April 8, 8 PM ET — his 3rd extension. His Truth Social rhetoric remained maximally aggressive (’Open the Fuckin’ Strait, you crazy bastards,’ ‘Tuesday will be Power Plant Day’), but the pattern of threats followed by extensions is now established. Iran formally rejected a temporary ceasefire but mediators (Pakistan/Egypt/Turkey) are pushing a ~45-day ceasefire framework. An Iran-Oman Hormuz transit protocol is still developing. The market has learned to discount Trump’s deadlines.

PRIOR SESSION (Day 26 Close, Thursday): S&P +0.11% with WTI +11.41% — the session that confirmed the oil-equity decoupling. MOVE fell to 84.41 (6th consecutive decline). VIX 23.87. The market absorbed Trump’s ‘stone ages’ speech by decoupling equities from oil for the first time in the war.

This week’s calendar (verified): TODAY — ISM Services (released, 54.0 miss). TUESDAY — Trump deadline 8 PM. DAL, STZ, APLD earnings. WEDNESDAY — GDP Q4 Third Estimate + PCE February + LEVI earnings. THURSDAY — CPI March (THE inflation test) + Factory Orders (rescheduled from April 2).

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 04/02/26. Provided for informational purposes only; not as investment advice.

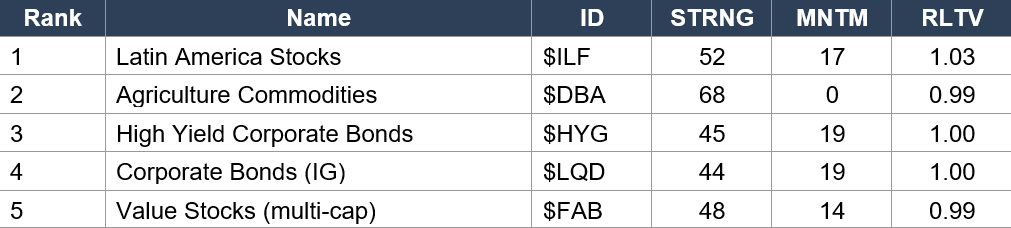

Asset Classes — Top 5

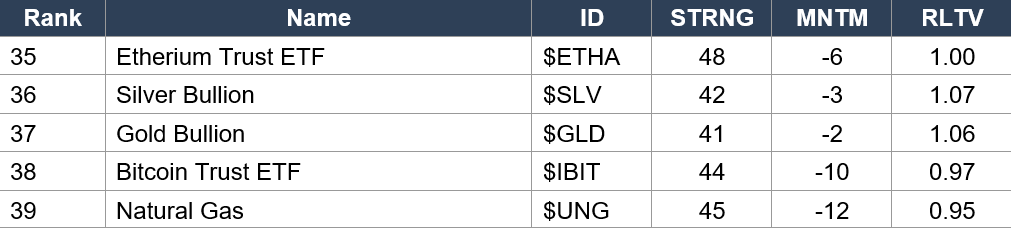

Asset Classes — Bottom 5

Regime signal: Latin America ($ILF rank 1, MNTM 17) holds the top position for a 3rd consecutive data set — commodity-producing EM remains the structural winner. High Yield ($HYG rank 3, MNTM 19) and Investment Grade ($LQD rank 4, MNTM 19) credit have the HIGHEST MOMENTUM of any asset class — credit markets are pricing de-escalation aggressively. The CRITICAL shift: Oil ($USO rank 6, STRNG 68, MNTM −7, RLTV 1.16) still has the highest RLTV at 1.16 but momentum has turned negative as the de-escalation trade pulls oil lower. VIX ($VXX rank 29, MNTM −8, RLTV 0.94) has COLLAPSED from rank 2 to rank 29 — the panic trade is dead. Dollar ($UUP rank 26, MNTM −10) plunged from rank 1 to rank 26 over the last two data sets. Gold ($GLD rank 37, MNTM −2, RLTV 1.06) and Silver ($SLV rank 36, MNTM −3, RLTV 1.07) remain near the bottom with negative momentum but elevated RLTV — precious metals still outperform the broad market despite the forced liquidation episodes. S&P ($SPY rank 24, MNTM 9) has recovered to mid-table. Nasdaq ($QQQ rank 33, MNTM 3) still underperforming. NOTE: The Quiggle data captures Thursday’s close — the NFP, ISM Services miss, and weekend developments are NOT reflected.

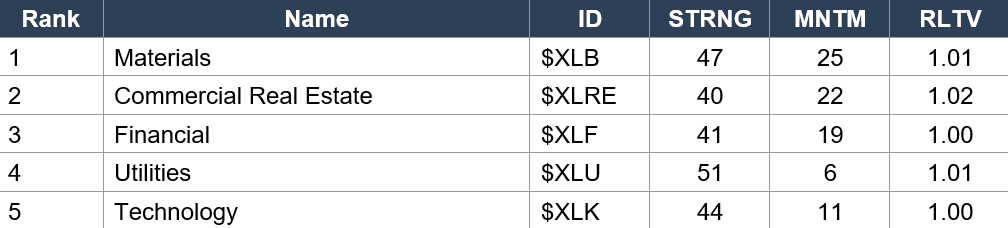

Sector ETFs — Top 5

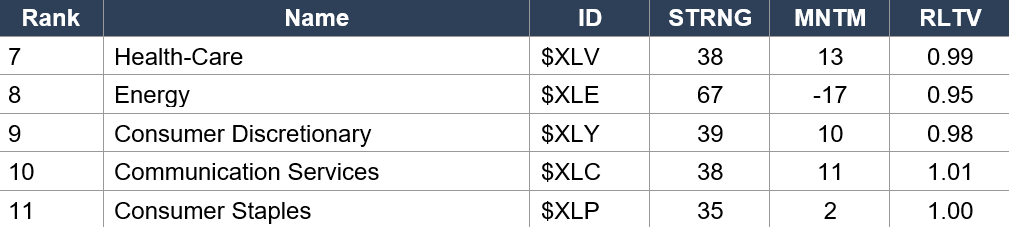

Sector ETFs — Bottom 5

Regime signal: The sector rankings have undergone the most dramatic reshuffling of the entire war. Materials ($XLB rank 1, MNTM 25) now LEADS — surpassing Energy for the first time. Commercial Real Estate ($XLRE rank 2, MNTM 22) has SURGED from rank 10-11 to #2 — the most dramatic single-session sector move of the series, driven by the bond rally and MOVE normalization. Energy ($XLE rank 8, MNTM −17, RLTV 0.95) has PLUNGED from perennial #1 to #8 with the worst momentum AND worst RLTV of any sector — the de-escalation and oil-equity decoupling are destroying Energy’s relative positioning. This is a HISTORIC regime shift in the Quiggle data: for the entire war, Energy led every data set. Its fall to #8 with negative momentum and sub-1.00 RLTV signals the market has STRUCTURALLY rotated away from the war trade. Technology ($XLK rank 5, MNTM 11) has recovered into the top 5 for the first time since early in the war — the post-crisis normalization benefits growth/duration assets.

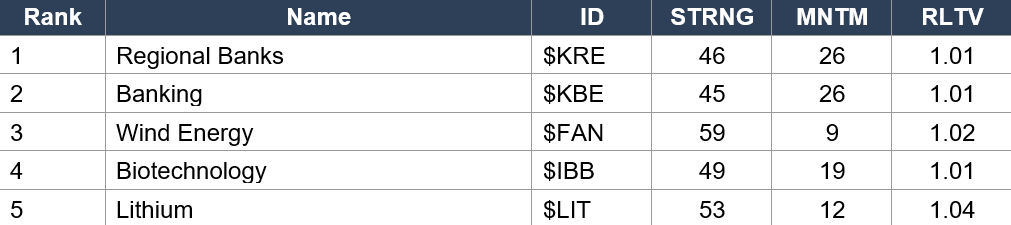

Industry ETFs — Top 5

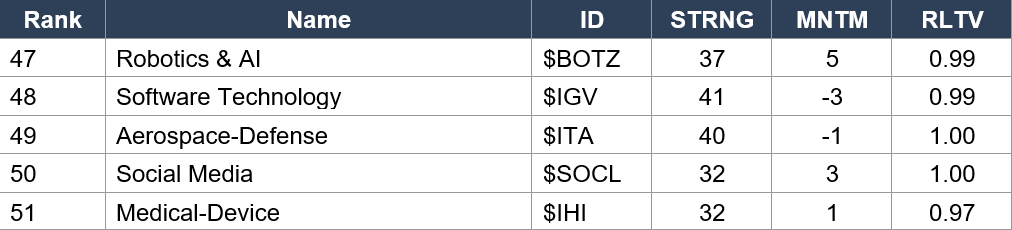

Industry ETFs — Bottom 5

Regime signal: Regional Banks ($KRE rank 1, MNTM 26) and Banking ($KBE rank 2, MNTM 26) have the highest momentum of ANY industry — the steeper yield curve and MOVE normalization are powering bank earnings expectations. Gold Miners ($GDX rank 20, MNTM 14, RLTV 1.13) still has the HIGHEST RLTV of any industry at 1.13 — gold miners structurally outperform despite the metal’s volatility. Oil & Gas Exploration ($XOP rank 26, STRNG 69, MNTM −13, RLTV 0.95) has plunged with the worst RLTV of any top-20 industry — the oil-equity decoupling is devastating the energy complex in relative terms. Alerian MLP ($AMLP rank 46, MNTM −25) worst momentum. Medical-Device ($IHI rank 51, RLTV 0.97) has the worst RLTV of any industry. Software Technology ($IGV rank 48, MNTM −3) remains a relative laggard despite tech’s broader recovery.

4. MORNING DATA REACTION

NFP March: +178,000 — MASSIVE BEAT. Consensus +57-60K. Prior revised to −133K from −92K.

Released to closed markets Good Friday — absorbed over 3-day weekend. The most since December 2024. Healthcare +76K (Kaiser strike reversal). Construction +26K. Transportation +21K. Manufacturing +15K. Federal government −18K. Unemployment 4.3% (unchanged). Average Hourly Earnings +3.5% YoY — DOWN from 3.8%, lowest since August 2024. January revised up +34K to +160K; February revised down −41K to −133K (net −7K). The market’s read: Goldilocks. Hot headline jobs show the economy can absorb the war shock. Cooling wages remove the wage-price spiral fear and keep the Fed comfortably on hold. But 76K of the 178K was healthcare strike reversal — the underlying pace is closer to ~100K, which is solid but not exceptional.

ISM Services March: 54.0 — MISS. Forecast 55.0. Prior 56.1. Slowest expansion since January.

The first ISM Services reading covering a full month of war. The deceleration from 56.1 to 54.0 (−2.1 points) is the largest single-month drop since the war began. Services represent ~80% of the US economy. The miss matters for three reasons: (1) it’s the first hard evidence that the oil shock and war anxiety are reaching the broader economy beyond manufacturing; (2) the NFP +178K was generated in a month where services activity was slowing — hiring held up even as the sector decelerated, which is an unsustainable divergence if ISM continues falling; (3) combined with ISM Manufacturing Prices Paid at 78.3, the picture is ‘activity slowing + inflation surging’ — the stagflation signature in both the goods AND services economy.

The pairing of NFP +178K with ISM Services 54.0 creates a MIXED signal: the labor market is strong but the economy it serves is losing momentum. If services decelerate further toward 50 in April — plausible given $110+ oil, $4+/gallon gas, and Michigan Sentiment at 53.3 — the next NFP may not be able to repeat this strength.

Jobless Claims from Thursday: 202,000 — beat 212K. Near 2-year low. Labor market remains resilient.

The week’s data arc tells a clear story: ADP +62K (beat). Retail Sales +0.6% (beat). ISM Manufacturing 52.7 (beat, but Prices Paid 78.3 surging). Claims 202K (beat). NFP +178K (massive beat). ISM Services 54.0 (MISS). Five beats and one miss — but the miss is in the sector that drives 80% of the economy.

This week ahead (verified): TUESDAY — Trump energy strike deadline 8 PM ET. DAL, STZ, APLD earnings. WEDNESDAY — GDP Q4 Third Estimate + PCE February (the Fed’s preferred inflation gauge). LEVI earnings. THURSDAY — CPI March (THE inflation test — will capture the war’s first full month of price impact) + Factory Orders (rescheduled).

5. THE DYRH READ

Regime: NFP Blowout Absorbed — Post-War Repricing Accelerates. MOVE New War Low. Deadline Extended. Oil-Equity Decoupling Confirmed. ISM Services Miss Adds the First Services-Sector Warning. The war’s MARKET crisis is over — MOVE at 81.78 is 8.6 points from pre-war. What remains is inflation legacy, geopolitical noise, and whether services deceleration becomes a trend. Confidence: High.

Yield Curve: Bear Flattener — NFP Beat Reprices the Front End.

All yields rising with the front end leading: 2Y +5.5 bps to 3.860%, 5Y +4.9 bps to 3.999%, 10Y +3.8 bps to 4.347%, 30Y +2.3 bps to 4.903%. The front end is repricing rate expectations higher on the NFP beat — +178K jobs means the Fed has zero urgency to cut. The 2Y at 3.860% is pricing the Fed firmly on hold through year-end. The long end rising less (+2.3 bps) reflects the de-escalation anchor — the market believes the war’s worst inflation impulse is behind it even if oil stays at $110.

MOVE at 81.78 is the session’s structural anchor. The 7-session decline from 115.02 to 81.78 (−28.9%) means the bond market has nearly fully normalized. Only 8.6 points of war premium remain versus the pre-war 73.21. This level of bond market calm with $110 oil is unprecedented in the war’s history — the market has structurally repriced from ‘bond crisis’ to ‘elevated but manageable inflation environment.’

Oil-Equity Decoupling — The War’s Most Important Structural Shift.

WTI at $110.39 (−1.03%) while ES at +0.39%. Thursday’s session was the confirmation: S&P +0.11% with WTI +11.41%. For the first 33 days of the war, oil up = equities down. That relationship has BROKEN. The market is no longer trading equities as a function of oil prices — it’s trading them as a function of war TRAJECTORY. If the war is ending (deadline extensions, mediator frameworks, ceasefire talk), equities can rally regardless of where oil is. XLE at −0.54% today (with WTI −1.03%) confirms the energy sector is being sold even as equities rally — the ‘war trade’ is being unwound.

The oil-equity decoupling also explains the Quiggle data: Energy (XLE)fellfromperennialrank1torank8withtheworstRLTV(0.95)ofanysector.Materials(XLE) fell from perennial rank 1 to rank 8 with the worst RLTV (0.95) of any sector. Materials ( XLE)fellfromperennialrank1torank8withtheworstRLTV(0.95)ofanysector.Materials(XLB) and Commercial Real Estate ($XLRE) have taken the top positions. The market is rotating FROM war beneficiaries TO post-war recovery plays.

ISM Services Miss — The First Warning Shot for the Broader Economy.

ISM Services at 54.0 (miss 55.0, down from 56.1) is the first sign that the war’s economic damage is migrating from goods/manufacturing into services — the 80% of GDP that has been resilient. Manufacturing showed expansion with surging input costs (ISM Mfg 52.7, Prices Paid 78.3). Services is now showing deceleration without the offsetting inflation component being visible yet. If April’s services data shows further deceleration AND services Prices Paid surges (mirroring manufacturing’s 78.3), the stagflation narrative extends from factories to the entire economy.

The NFP +178K creates a temporary buffer — the labor market is strong enough to sustain services activity even as the sector slows. But the divergence between ‘strong hiring’ and ‘weakening activity’ is historically temporary. Either activity recovers (hiring justified) or hiring slows to match (the NFP was a lagging indicator). Wednesday’s PCE and Thursday’s CPI will determine which narrative prevails.

Gold Recovery and Forced Liquidation Over.

Gold at $4,700.4 (+0.44%, +$20.7) has recovered from Thursday’s forced liquidation. All metals green except palladium (flat). The Day 26 forced liquidation (gold −3.56%, silver −7.22%) was a ONE-SESSION event — not the start of a new cascade. Gold is now $324.4 above the $4,376 war low. GVZ at 37.85 (Thursday) will determine whether gold’s recovery continues or stalls. The Quiggle data shows gold’s RLTV at 1.06 — still outperforming the broad market despite three forced liquidation episodes.

6. THE GAME PLAN

Today’s Key Events: ISM Services 54.0 MISS already digested. Tuesday — Trump energy strike deadline 8 PM (3rd extension — will he extend again or follow through?). DAL earnings (airline in a war zone). STZ earnings. Wednesday — GDP Q4 Third Estimate + PCE February (Fed’s preferred inflation gauge). Thursday — CPI March (THE inflation test — first full month of war price impact).

The Bull Case:

MOVE at 81.78 is the most structurally bullish signal of the entire war — the bond market has nearly fully normalized. NFP +178K shows the economy can absorb the war shock and keep hiring. AHE cooling to 3.5% removes the wage-price spiral fear. Trump’s 3rd deadline extension confirms ‘he will keep extending’ — the market has learned to discount the threats. Oil-equity decoupling means equities can rally regardless of oil levels. All 7 Mag 7 green. SOXX +0.99% (5th session of recovery). XLK leading sectors (+0.59%). All correlations at war lows (COR1M 25.00). Breadth healthy (S5TW 52.48 above 50, S5FD 77.13). Pakistan/Egypt/Turkey pushing 45-day ceasefire framework. ISM Services at 54.0 is still in expansion — it missed expectations but the economy is NOT contracting. The Quiggle data shows the market has structurally rotated from war trades to post-war recovery plays.

The Bear Case:

ISM Services 54.0 is the first evidence that the oil shock is reaching the 80% of GDP that had been resilient — if this deceleration continues, the ‘Goldilocks’ narrative breaks. The NFP-ISM divergence (strong hiring + weakening activity) is historically unsustainable. Tuesday’s deadline could be the one Trump follows through on — 3rd extension doesn’t guarantee a 4th. Iran rejected the ceasefire — fighting INTENSIFYING (children killed in Tehran, missiles hitting Tel Aviv schools, Haifa residential building struck). Oil at $110 is still above the $100 damage threshold. ISM Manufacturing Prices Paid at 78.3 + services deceleration = stagflation spreading. CPI March on Thursday could show the war’s inflation arriving in consumer prices. European reaction delayed to Tuesday — could be negative. AHE at 3.5% may cool further if services weaken — deflation risk in wages alongside inflation in goods. BofA projects inflation to ~4% YoY. The 5-beat, 1-miss data arc this week shows the economy is resilient but NOT immune.

Regime: NFP Blowout Absorbed — Post-War Repricing Accelerates With Services Sector Warning. MOVE at 81.78 says the bond crisis is over. The oil-equity decoupling says equities have stopped pricing oil. The ISM Services miss at 54.0 says the damage is reaching the broader economy. Three different stories, three different timeframes. The bond market is pricing ‘crisis over.’ Equities are pricing ‘war ending.’ Services data is pricing ‘damage spreading.’ This week’s GDP/PCE/CPI sequence will determine which story dominates Q2.

Watch List

Tuesday 8 PM — Trump energy strike deadline (3rd extension — 4th?)

The market is pricing another extension. If Trump follows through and strikes power plants, every de-escalation position built over the last week gets destroyed. If he extends again, the ‘boy who cried wolf’ dynamic deepens and the market further discounts future deadlines. The binary nature of this catalyst with less than 36 hours remaining makes position sizing critical.

ISM Services 54.0 — trend or noise?

A single miss doesn’t make a trend. But the 2.1-point deceleration (56.1 → 54.0) in a single month is notable. April’s services data will be the tiebreaker — if it drops toward 52 or below, the war’s damage to the services economy is real and the NFP strength won’t persist. Watch the services Prices Paid component when the full subcomponents are available.

Wednesday — GDP Q4 Third Estimate + PCE February

GDP is ancient pre-war data but PCE February is critical — the Fed’s preferred inflation gauge covering the war’s opening days. If PCE shows inflation accelerating before the worst of the oil shock hit, it implies the April/May readings will be significantly worse. BofA’s projection of headline inflation approaching 4% YoY would be confirmed by an upside PCE surprise.

Thursday — CPI March (THE inflation test)

The first CPI reading covering a full month of war. This is the data point the Fed, the bond market, and the equity market are all watching. A hot CPI print with $110 oil, $4+/gallon gas, and ISM Prices Paid at 78.3 would confirm the inflation pass-through that the survey data has been signaling. The market’s ability to maintain the ‘crisis over’ narrative depends on CPI not delivering a shock.

MOVE trajectory — can it reach pre-war levels?

81.78 is 8.6 points above pre-war 73.21. If MOVE continues declining to ~75-78, the bond market will have FULLY normalized during an active shooting war with $110 oil. This would be one of the most remarkable risk repricing events in modern market history. If MOVE reverses and spikes back above 90 on Tuesday’s deadline or Thursday’s CPI, the normalization was premature.

Morning check: Day 38. The war rages — children killed in Tehran, missiles hitting schools in Tel Aviv, an IRGC commander dead, Houthis firing at Israel. And the bond market is 8.6 points from pre-war. MOVE at 81.78 says the crisis is over. NFP +178K says the economy is hiring. ISM Services at 54.0 says the damage is spreading. Oil at $110 says the energy shock persists. Trump says ‘stone ages’ but extends every deadline. Iran says ‘no ceasefire’ but mediators keep pushing. Five data releases beat last week. One missed — and it was the one that covers 80% of the economy. The market has decoupled equities from oil, normalized bonds despite inflation, and rotated from war trades to recovery plays. The crisis IS over. The question now is whether the inflation it created — Prices Paid 78.3, CPI on Thursday, PCE on Wednesday — will force the crisis back. Tuesday’s deadline. Wednesday’s PCE. Thursday’s CPI. The war’s market chapter may be closing. The inflation chapter is just opening.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.