☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: The market has fully decoupled from the war. ES at 6,770.75 (+2.03%) is the HIGHEST level since the war began on February 28 — 55% of the entire war drawdown has been retraced in two sessions. Meanwhile, the war is escalating on every front: Israel killed Iran’s security chief Larijani and Basij commander Soleimani, Iran’s new Supreme Leader REJECTED peace proposals (“not the right time”), the Fujairah oil zone was struck by drone (attacking the critical Hormuz BYPASS route), Israel expanded ground operations in Lebanon, and Gulf oil exports are down 60% (week to March 15, from 25.13M to 9.71M bpd per Kpler). The market has decided: the war is priced, GTC provides a counter-narrative, and the Fed will deliver a dovish hold tomorrow. Gold is FINALLY green (+0.30% to $5,017) after a 7-day losing streak (−$309, −5.8% cumulative) — the $5,000 floor held. This is the missing piece — if gold sustains above $5,000, the forced-liquidation cycle is over. But oil is reversing HIGHER: WTI +2.35% to $95.70, Brent +2.17% to $102.38, driven by the Fujairah strike and parliamentary speaker Qalibaf’s hawkish comments that Hormuz “cannot return to previous conditions.” The market is currently running equities and oil BOTH higher — a divergence that cannot persist. Yields falling for a second consecutive session (10Y 4.208%, −1.2 bps). VIX at 22.71 (lowest since Day 8). MOVE at 85.25 (bond panic over). Breadth repaired massively Monday (S5FD doubled to 45.72). COR1M crashed from 37.21 to 29.56 — stock-specific alpha returning. The Fed tomorrow is the fulcrum.

The Number That Matters: ES at 6,770.75 — the highest since February 28. The S&P has retraced 55% of the war drawdown (6,881.62 → 6,636 trough → 6,770.75) in just TWO sessions, even as the war intensifies. The market is now only ~111 points (−1.6%) from pre-war levels. This speed of recovery — 135 points in two days — signals that the equity market has decided the war’s financial market impact has peaked. Whether this is justified or complacent is the defining question going forward. The Fed’s statement tomorrow will either validate this bet or expose it as premature.

The Setup: Fed Eve. The entire market is positioned for a dovish hold: bonds rallying for two consecutive sessions, VIX at 22.71, MOVE at 85.25, DXY retreating from 100, breadth repairing, gold stabilizing. The risk is ASYMMETRIC — a dovish hold extends the rally incrementally; a hawkish surprise reverses it violently. Today’s data is light (Pending Home Sales 10 AM, Nvidia Analyst Q&A noon). The market is in pre-Fed holding pattern with a strong upward bias from GTC momentum. The key warning sign: RTY at +0.24% vs. ES at +2.03% — the rally is beginning to NARROW back toward mega-cap tech. Oil reversing higher despite the equity rally creates a divergence that must resolve.

2. OVERNIGHT SESSION RECAP

Asia-Pacific

TOPIX +1.21% — Japan extending gains for a second session. Nikkei −0.46% (only red index, profit-taking after +2.37% Monday). The Hormuz tanker transit narrative is supporting Asian risk appetite but the Fujairah strike overnight is a reminder the conflict is not de-escalating.

Europe

Euro Stoxx +0.68%, DAX +0.55%. Europe modestly green, continuing Monday’s recovery. EU foreign ministers decided AGAINST expanding naval operations around Hormuz despite Trump pressure. Australia and Japan also declined to send ships. Germany: “not NATO’s war.” The international isolation of the US military position is growing.

US Pre-Market

Day 16 — War Escalating, Market Ignoring. Israel claims it killed Ali Larijani (security chief, close to slain Supreme Leader) and Basij force commander Soleimani. Iran has not confirmed — Tasnim posted a purported handwritten note from Larijani dated March 17. Iran’s new leader Mojtaba Khamenei REJECTED peace proposals: “not the right time for peace.” Parliamentary speaker Qalibaf: Hormuz “cannot return to previous conditions.” Fujairah Oil Industry Zone struck by drone — fire at petroleum facility (Fujairah is the vital BYPASS route around Hormuz). Drone hit Al-Rasheed Hotel in Baghdad’s Green Zone near US Embassy. USS Gerald Ford fire burned 30+ hours. Gulf exports down 60% in the week to March 15. Israel expanded ground operations in southern Lebanon. Death toll 2,200+. Gas $3.79/gallon (+26% since war began).

Nvidia GTC — the counter-narrative that won: Jensen Huang keynote delivered — $1 TRILLION in AI chip revenue through 2027 (up from $500B prior guidance). Vera Rubin platform revealed. DLSS 5 previewed. NemoClaw open-source agentic AI. $27B AI infrastructure deal with Meta/Nebius. NVDA Analyst Q&A today at 12 PM ET. SOXX +1.96% Monday, extending in after-hours to +0.42%. The AI narrative has given the market a reason to buy independent of the war.

Prior session (March 16 close — THE RALLY THAT HELD): S&P +1.01%, Nasdaq +1.22%, Dow +0.83%, Russell +0.94%. The rally held all day — categorically different from Friday’s dead cat. All 11 sectors, all 12 factors, all 7 Mag 7 green. VIX −13.53% to 23.51 (largest decline of the series). MOVE −6.50% to 85.25 (bond panic over). COR1M −20.56% to 29.56 (stock-specific alpha returning). S5FD +115% (doubled from 21 to 46). WTI −5.28% to $93.50 (largest oil decline of the series). Gold −1.18% to $5,002.2 (seventh consecutive decline, $2 above $5,000). Empire State Manufacturing −0.20 (first contraction since December).

This week: TODAY 10:00 AM: Pending Home Sales (February). TODAY 12:00 PM ET: Nvidia Analyst Q&A. TOMORROW (THE MAIN EVENT): PPI (February) 8:30 AM; FOMC Decision 2:00 PM + Dot Plot + Economic Projections; Powell Press Conference 2:30 PM; Bank of Canada. Thursday: BOJ (tentative), SNB, BOE, ECB decisions; Jobless Claims; Philly Fed Manufacturing; New Home Sales. SIX central bank decisions in 48 hours (Wed–Thu).

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 03/16/26. Provided for informational purposes only; not as investment advice.

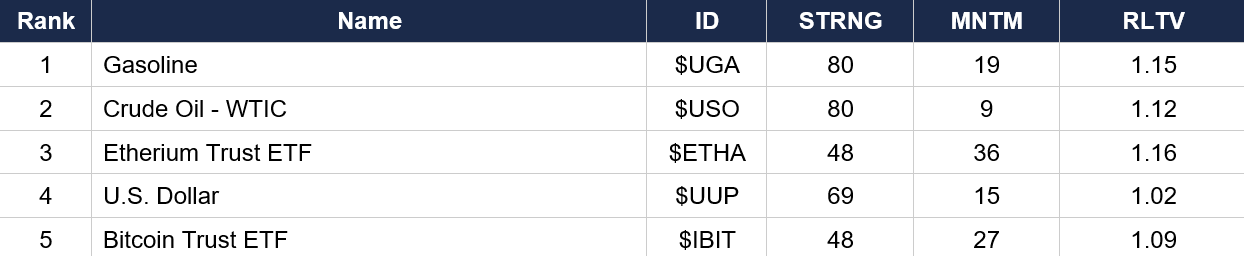

Asset Classes — Top 5

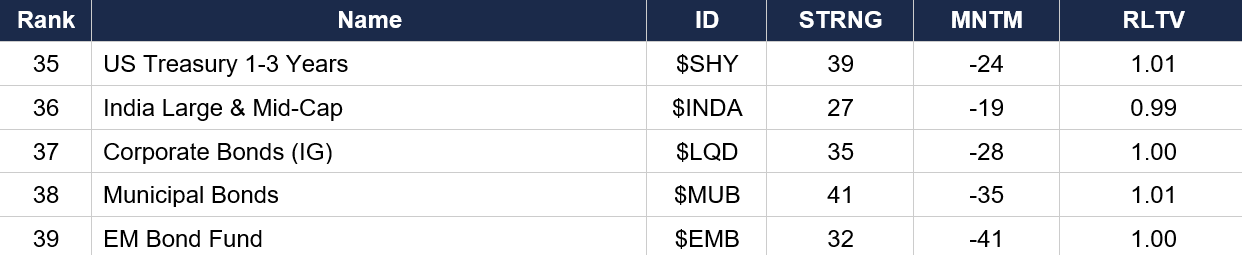

Asset Classes — Bottom 5

Regime signal: Crypto has SURGED into the top 5 — Ethereum ($ETHA rank 3, MNTM 36) and Bitcoin ($IBIT rank 5, MNTM 27) are now the highest-momentum non-energy assets. This is the clearest signal that speculative risk appetite has returned. Dollar ($UUP rank 4, MNTM 15) has moderated from its peak MNTM of 31 as DXY retreats from 100. VIX ($VXX rank 10, MNTM −10) has dropped out of the top 5 and momentum flipped NEGATIVE for the first time in the series — the fear trade is unwinding. Gold ($GLD rank 16, MNTM −13) remains deeply negative but stabilizing above $5,000. Nasdaq ($QQQ rank 11, MNTM 4) has turned POSITIVE momentum for the first time since the crisis — confirming the GTC-driven tech revival. S&P ($SPY rank 17, MNTM −3) is approaching neutral. EM Bonds ($EMB, MNTM −41) remains the worst momentum. Senior Corporate Loans ($BKLN rank 6, MNTM 29) still strong in the floating-rate credit space.

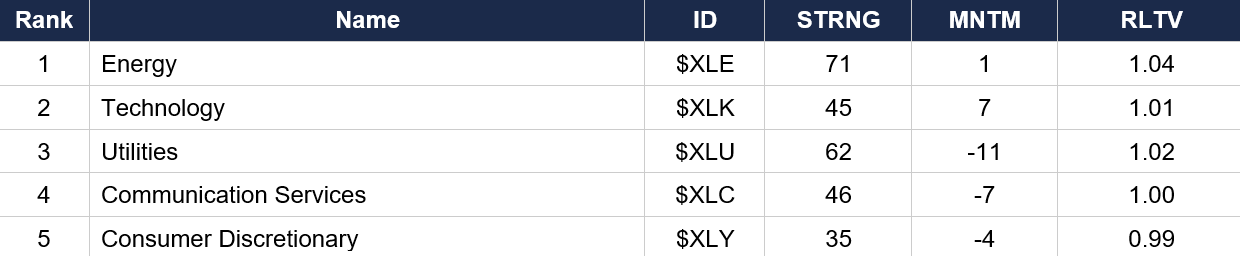

Sector ETFs — Top 5

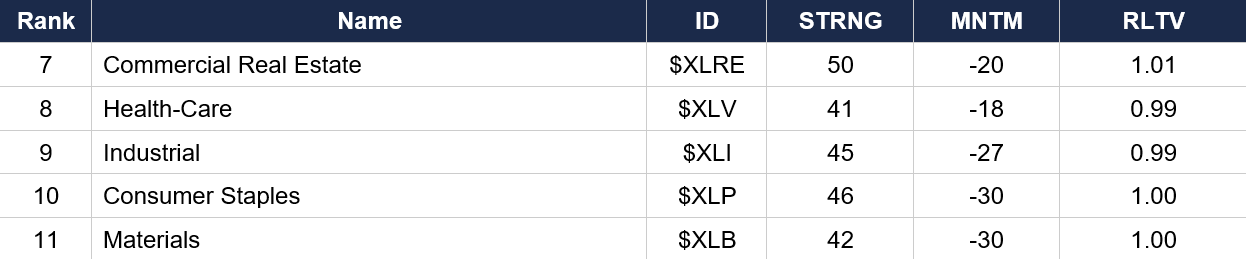

Sector ETFs — Bottom 5

Regime signal: Technology ($XLK, MNTM 7) has turned POSITIVE momentum — the GTC catalyst is showing up in the sector rankings. Energy ($XLE, MNTM 1) is essentially flat-momentum despite being rank 1 by strength — the oil trade is mature. Consumer Discretionary ($XLY, MNTM −4) has improved dramatically from −18, reflecting the consumer resilience narrative. Industrial ($XLI, MNTM −27) and Consumer Staples ($XLP, MNTM −30) remain the weakest sectors. The sector picture is IMPROVING across the board but still dominated by negative momentum in most sectors.

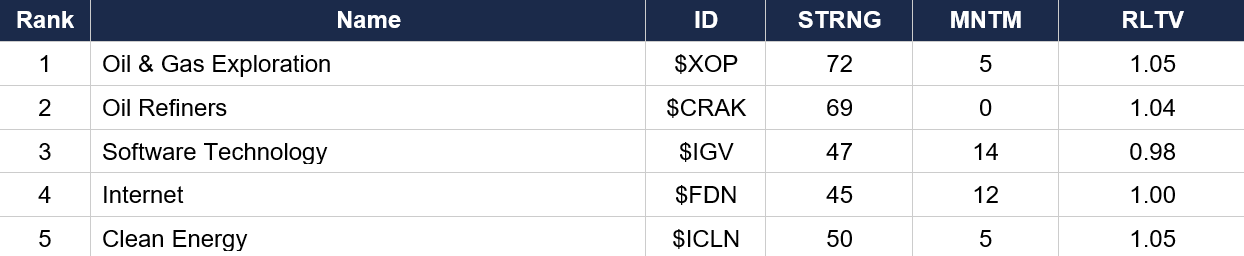

Industry ETFs — Top 5

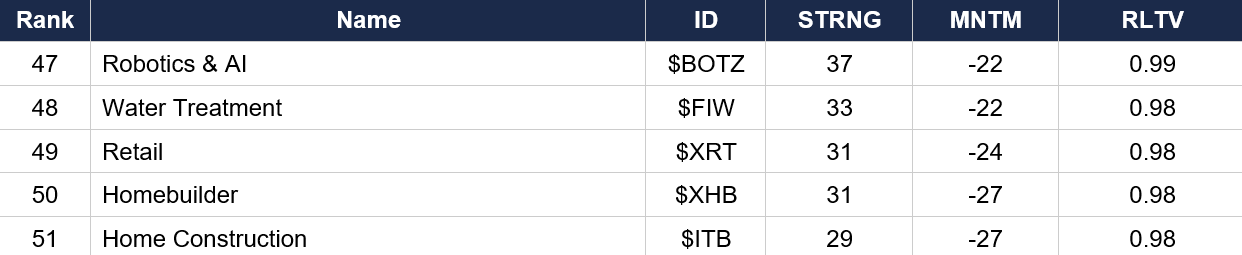

Industry ETFs — Bottom 5

Regime signal: Clean Energy ($ICLN rank 5, MNTM 5) has entered the top 5 for the first time in the series — $100+ oil is accelerating the alternative energy investment thesis. Software ($IGV, MNTM 14) and Internet ($FDN, MNTM 12) maintain strong positive momentum from the GTC catalyst. Semiconductor ($SMH rank 20, MNTM −4) is improving from rank 25 but still negative. Aerospace-Defense ($ITA rank 28, MNTM −16) remains weak despite the war. Shipping ($BOAT rank 32, MNTM −29) devastated by Hormuz. Home Construction ($ITB, MNTM −27) and Homebuilder ($XHB, MNTM −27) at the absolute bottom as 30Y yields at 4.86% and mortgage rates above 6% crush housing.

4. MORNING DATA REACTION

No major economic data before the open today. This is Fed Eve — the market is in pre-positioning mode. Pending Home Sales (February) at 10:00 AM is the only data point, and it is secondary to tomorrow’s FOMC event.

Monday’s data recap: Empire State Manufacturing −0.20 (first contraction since December). The first hard manufacturing survey capturing the war’s impact confirmed that activity has slipped into contraction. Industrial Production +0.7% beat expectations. NAHB Housing Index slipped to 42 from 44. The mixed picture: manufacturing contracting, industrial production still expanding on pre-war momentum, housing weakening under rate pressure.

Tomorrow is THE MAIN EVENT: PPI (February, rescheduled from March 12 due to government shutdown) at 8:30 AM — the last inflation data before the Fed. FOMC Decision at 2:00 PM with Dot Plot, Economic Projections, and Statement. Powell Press Conference at 2:30 PM. The Fed faces an impossible mandate: GDP 0.7%, Core PCE 3.1%, oil above $95, Michigan at 55.5 (2nd percentile). Hold universally expected. The dot plot revisions and Powell’s language on energy-driven inflation (“transitory supply shock” vs. “persistent price pressure”) will determine whether this rally extends or reverses.

Thursday delivers FOUR more central bank decisions: Bank of Japan (tentative), Swiss National Bank, Bank of England, ECB — plus Jobless Claims, Philly Fed Manufacturing, and New Home Sales. Six central bank decisions in 48 hours — a global monetary policy reset moment as every major central bank addresses the stagflationary oil shock simultaneously.

5. THE DYRH READ

Regime: Post-Crisis Recovery — Rally Accelerating Into the Fed; Market Decoupled from War Escalation. Confidence: High on characterization.

Yield Curve: Bull Flattener — Second Consecutive Session. Yields falling across the entire curve: 5Y −1.2 bps, 10Y −1.2 bps (4.208%), 30Y −1.0 bps (4.858%, now 5.0 bps below the 4.908% series high). Two consecutive sessions of falling yields confirm the bond selloff is definitively OVER. The market is pre-positioning for a dovish Fed hold. The 10Y has now retraced 7.5 bps of its 33.4 bp war premium (22% retracement). MOVE at 85.25 is 10 full points below its 95.30 peak — the bond market is no longer in any form of crisis. If Powell delivers tomorrow, yields could fall further toward 4.15–4.20% on the 10Y. The “approaching 5%” 30Y crisis has been averted.

Gold Finally Green — The Missing Piece. Gold at $5,017 (+0.30%) ends a 7-day forced-liquidation streak that was the single most alarming cross-asset signal of the series. Cumulative: −$294.6 (−5.5%) — still deeply negative but the DIRECTION has changed. The $5,000 floor held — barely. If gold sustains above $5,000 through tomorrow’s Fed, the forced-liquidation cycle is OVER and the regime transition from crisis to recovery is complete. Platinum +1.75% and Palladium +1.75% confirm industrial metals are stabilizing. Copper −0.84% is the lone negative, reflecting continued demand destruction concerns.

Oil Reversing Higher — The Key Risk. WTI +2.35% to $95.70, Brent +2.17% to $102.38. Monday’s −5.28% WTI crash was the CATALYST for the equity bounce. Today’s reversal is driven by: Fujairah oil zone drone strike (attacking the Hormuz bypass), Qalibaf’s hawkish Hormuz comments, 60% Gulf export decline confirmed, Larijani killing reducing diplomatic prospects. Brent-WTI spread widened to ~$7.41 (widest of the series). ES +2.03% and WTI +2.35% simultaneously = unsustainable divergence. Either oil fades (rally continues) or oil surges past $103–105 (rally tests). The market is currently IGNORING the oil bounce — the first true decoupling of the series.

Equities: 55% of War Drawdown Retraced in Two Sessions. ES at 6,770.75 — only 111 points (−1.6%) from pre-war levels. All 7 Mag 7 were green Monday; pre-market today shows 5 green, 2 flat. NVDA +0.53% (GTC continuing). META flat (profit-taking after +2.24%). The KEY WARNING: RTY at +0.24% vs. ES +2.03% — the rally is beginning to NARROW back toward mega-cap tech. Mid-caps (IJH −0.49% AH), value (VLUE −0.32% AH), and defensives (USMV −0.42% AH) are all fading. If this persists, it risks recreating the Days 9–10 “stealth stagflation” pattern. Breadth repaired massively Monday (S5FD doubled to 45.72, ALL measures improving), but medium-term breadth (S5TH 49.30) remains just below the critical 50 bull/bear line.

Volatility: Fear Regime Broken. VIX at 22.71 (−3.40%) — lowest since Day 8, well below the 25 fear threshold. Two consecutive sessions below 24 confirms the fear regime has broken. MOVE at 85.25 — 10 points below the 95.30 peak; bond panic over. COR1M crashed from 37.21 to 29.56 (−20.56%) — the largest correlation move of the series. Stock-specific alpha is returning. VXN −11.88% confirms Nasdaq-specific vol has normalized. SKEW at 141.49 (normalizing from 137.76 crash). The vol/breadth/correlation configuration is the most constructive since the war began.

6. THE GAME PLAN

Today’s Key Events: Pending Home Sales (February) 10:00 AM. Nvidia Analyst Q&A 12:00 PM ET. Light data day — Fed Eve pre-positioning. Tomorrow: PPI (February) 8:30 AM; FOMC Decision 2:00 PM + Dot Plot + Projections; Powell presser 2:30 PM; Bank of Canada. Thursday: BOJ, SNB, BOE, ECB; Jobless Claims; Philly Fed Manufacturing; New Home Sales.

The Bull Case: ES has retraced 55% of the war drawdown in two sessions. All structural signals improving: VIX below 23, MOVE at 85, yields falling, breadth repairing across ALL timeframes, COR1M crashed, gold finally green above $5,000. The market has given a clear signal it wants to rally. GTC ($1T AI revenue) provides a fundamental catalyst independent of the war. A dovish Fed hold tomorrow extends the rally and confirms the floor at the 200-day MA area. First non-Iranian tanker transited Hormuz with AIS on. Two-year yield has given back half its war surge. S5FD doubled in one session. All 11 sectors, 12 factors, 7 Mag 7 were green Monday.

The Bear Case: The market has decoupled from a war that is ESCALATING — Larijani killed, peace rejected, Fujairah struck, Lebanon invaded, Gulf exports down 60%. Oil reversing +2.35% on genuine escalation while equities surge = unsustainable divergence. RTY lagging at +0.24% vs. ES +2.03% signals the rally is narrowing back to mega-cap. Gold at +0.30% is marginal — the forced-liquidation signal needs more sessions to confirm it’s over. The Fed tomorrow is asymmetric: dovish = incremental extension; hawkish = violent reversal. Core PCE at 3.1% and oil above $95 give Powell ammunition to sound hawkish on inflation. Brent still above $100. Qalibaf’s “Hormuz cannot return” challenges the reopening narrative. If Brent recrosses $105, the stagflation trade re-engages.

Regime: Post-Crisis Recovery — Rally Accelerating Into the Fed. The market has decoupled from war escalation and is pricing the AI/Fed narrative. ES at the highest since the war began. Gold finally green. Yields falling. Vol crushed. Breadth repairing. But the Fed tomorrow is the ultimate test. The market’s bet is clear — now Powell must validate it.

Watch List

FOMC tomorrow — THE fulcrum — Hold universally expected. Dot plot revisions, statement language on energy/inflation, and Powell’s presser determine everything. Dovish (“transitory supply shock” + growth concern) = rally extends. Hawkish (PCE 3.1% + no cuts) = reversal. The risk is asymmetric.

Oil + equities BOTH up — unsustainable — WTI +2.35% and ES +2.03% simultaneously. This divergence must resolve. Watch Brent $103–105 as the trigger level. If oil fades, rally continues. If oil surges, the stagflation trade re-engages.

Gold above $5,000 — confirmation needed — First green session in 8 days. $5,000 floor held — barely. A close above $5,020 confirms the forced-liquidation cycle is over. A close below $5,000 negates the stabilization. This is the single most important cross-asset signal to monitor.

RTY lagging — rally narrowing? — Russell +0.24% vs. ES +2.03%. IJH −0.49% AH. VLUE −0.32% AH. The broad risk-on from Monday is showing signs of concentration back into mega-cap/tech. If this persists, it recreates the stealth stagflation pattern.

PPI tomorrow 8:30 AM — February PPI (rescheduled from March 12). The last inflation data before the Fed statement at 2:00 PM. A hot print would complicate the dovish narrative. An in-line or soft print keeps the door open for a growth-focused Fed statement.

Morning check: Fed Eve with the strongest risk-on signal of the entire series. ES at the highest since the war began. Gold finally green. Yields falling. Vol crushed. Breadth repairing. The market has decided the war is priced and the AI narrative is dominant. But the war is escalating on every front while the market ignores it — and Powell speaks tomorrow. The rally’s bet is clear: a dovish hold. If Powell validates it, the floor is confirmed. If he doesn’t, two days of gains evaporate. The market has cast its vote. Now we wait for the Fed.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.