☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: Gold bounces. Oil pulls back. The bond market refuses to believe it. Day 21 of the war and the cross-asset picture is splitting in two. Gold is GREEN for the first time since the forced liquidation began (+1.46% to $4,673) — after a $638 cumulative crash (−12%) during an active war, the precious metals complex is finally bouncing (silver +1.35%, platinum +1.53%). Oil is pulling BACK despite Kuwait’s Mina Al-Ahmadi refinery being hit AGAIN overnight by Iranian drones: Brent −1.65% to $106.86 (down from $119 intraday Thursday), WTI −1.00% to $94.59. The reason: de-escalation SIGNALS. Netanyahu pledged to hold off further South Pars attacks at Trump’s request and said the war may “end sooner than people think.” Treasury Secretary Bessent told Fox Business the US may “unsanction” ~140M barrels of Iranian oil on water to ease prices. Axios reports Trump considering occupying Kharg Island to force Hormuz open. BUT — yields are RISING across the entire curve. The 30Y is at 4.875%, approaching the critical 5.00% barrier. Yesterday’s bull steepener lasted exactly ONE SESSION before reverting to a bear steepener. The 2Y at 3.856% is climbing back toward the fed funds upper bound. MOVE at 84.88 is 0.37 points from its war high. The bond market sees permanent inflation damage regardless of war outcome — hot PPI (+0.7%), core PCE revised to 2.7%, and market pricing NO rate cuts until 2027. US futures mildly red (ES −0.28%) — a massive improvement from yesterday’s apocalyptic pre-market. DAX +0.98% recovering from −2.18%. All four European central banks held yesterday: ECB at 2%, BoE at 3.75% (unanimous), SNB at 0% — all hawkish-leaning. The ECB raised its 2026 inflation forecast to 2.6%. BoE members hinted at possible hikes. VIX at 24.77, edging back toward the 25 crisis line. No major US data today.

The Number That Matters: Gold at $4,673.1 (+1.46%) — the first green session since the forced-liquidation massacre began. After crashing $638 (−12%) from pre-war levels during an active shooting war — including a $342 single-session collapse on Day 19 (the largest since the January 30 crash) — gold is finally bouncing. If this holds through the session, it signals the leveraged-fund margin-call cycle is EXHAUSTING. Silver +1.35%, platinum +1.53%. The metals complex bouncing while oil pulls back is the most constructive cross-asset signal since Day 14’s recovery. But gold at $4,673 is still $638 below pre-war — the damage is massive and the recovery, if it continues, will be slow.

The Setup: Bifurcated Stagflation with tentative stabilization. The market is splitting: gold bouncing + oil pulling back + de-escalation rhetoric says the crisis intensity is fading. Bear steepener + 30Y approaching 5% + MOVE near war highs says the inflation damage is permanent. US futures only mildly red. International indices recovering (DAX +0.98%). Russell breadth surged +43% yesterday while S&P breadth barely moved. The size-factor divergence is the widest of the war: small caps improving while large caps remain stressed. No major data today — the session trades on war headlines, the gold/oil signal, and whether bonds can stabilize. Week 4 of the war begins Monday.

2. OVERNIGHT SESSION RECAP

Asia-Pacific

Nikkei +0.29%, TOPIX +0.34%. Japan green for the first time in 3 sessions. The oil pullback from $119 to $107 is providing relief for energy-import-dependent economies. BOJ held rates yesterday as expected.

Europe

DAX +0.98% — recovering from yesterday’s −2.18%. Euro Stoxx −0.89% (lagging). European central bank results from yesterday: ECB held at 2.0% (deposit), raised 2026 inflation forecast to 2.6%, said Middle East conflict will have “material impact on near-term inflation.” BoE held at 3.75% (unanimous) but MPC member Mann shifted toward “considering a longer hold, or even a hike.” SNB held at 0%, stressed willingness to intervene in FX markets. All hawkish-leaning. Markets pricing >2 ECB hikes and ~40bp BoE tightening in 2026. Natural gas surged 20%+ intraday Thursday on Ras Laffan/South Pars fears before settling.

US Pre-Market

Day 21 — De-escalation Rhetoric vs. Physical Escalation. Netanyahu pledged to hold off South Pars attacks at Trump’s request, said Israel “acted alone,” and said the war may “end sooner than people think.” Bessent: US may “unsanction” ~140M barrels of Iranian oil on water in next 10–14 days. Axios: Trump considering occupying or blockading Kharg Island to force Hormuz open. BUT: Kuwait’s Mina Al-Ahmadi refinery (730K bpd) hit AGAIN by Iranian drones, fires at multiple units. Iran’s IRGC spokesperson killed. Israel struck Tehran during Nowruz. Iran’s Supreme Leader warned of “zero restraint” if energy infrastructure attacked again. Qatar Energy Minister: Ras Laffan damage cuts 17% of LNG capacity, $20B annual revenue loss, 3–5 YEAR repair timeline. IMO negotiating humanitarian corridor for ~20,000 stranded seafarers. Pentagon requesting additional $200B for the war. Death toll: 2,200+ (Iran 1,444, Lebanon 1,000+, Israel 15+, Gulf states 21, US military 13).

Yesterday’s massive intraday reversal (Day 19 close): Pre-market was apocalyptic (gold −7%, silver −13%, Brent $113). But the session reversed: VIX fell below 25 (to 24.06), Russell closed green +0.67%, SPHB led factors, 7 of 11 thematics green. The equity market stabilized at the 200-day MA for the second time. BUT metals crisis continued: gold closed −5.93%, silver −8.22%. MOVE surged to 84.88 near war highs. DXY crashed −1.03% (largest of war) back below 100. Long bond rallied (bull steepener). The session defined “bifurcation”: equities stabilizing while metals/bonds remain in crisis.

FOMC recap (Wednesday March 18): Held 3.50–3.75%, vote 11-1 (Miran dissented wanting 25bp cut). Dot plot: ONE cut in 2026 (median 3.4%, unchanged from Dec). 7 of 19 see no cuts (up from 6). GDP forecast raised to 2.4%. PCE inflation forecast RAISED to 2.7% (headline and core). Powell: “not as much progress on inflation as hoped.” “Bar is higher for cuts.” Market now pricing NO cuts until 2027.

Today: No major US economic data. Light earnings (13 reports, no major names). FedEx +1.82% pre-market on beat + raised FY26 guidance. Michigan Sentiment FINAL releases March 27. Next FOMC: May 6–7.

3. THE PRIOR DAY’S REGIME (Jeff Quiggle Data)

Data from JeffQuiggle.com as of 03/19/26. Provided for informational purposes only; not as investment advice.

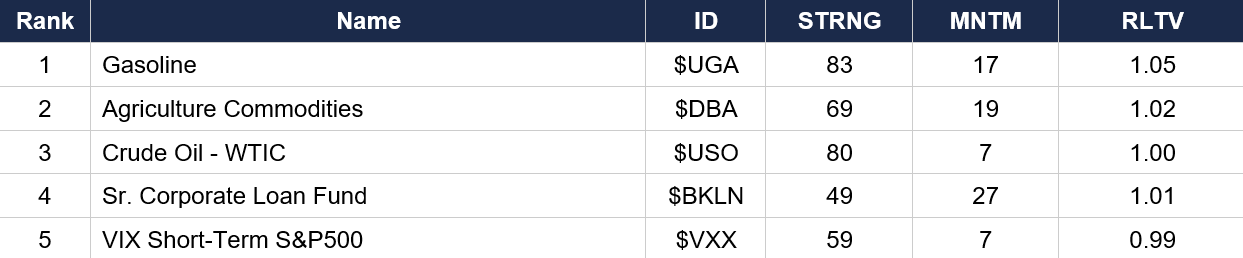

Asset Classes — Top 5

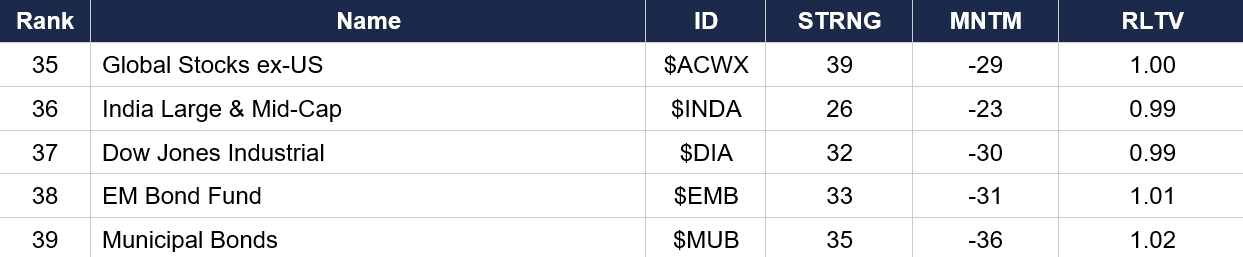

Asset Classes — Bottom 5

Regime signal: Agriculture ($DBA rank 2, MNTM 19) has SURGED to rank 2 for the first time in the series — the food inflation trade is intensifying as Gulf disruption threatens fertilizer supply chains and Hormuz closure impacts grain shipping. VIX ($VXX rank 5, MNTM 7) has returned to the top 5 with POSITIVE momentum — the fear trade is back. Dollar ($UUP rank 6, MNTM −5) has dropped out of the top 5 with NEGATIVE momentum for the first time — the DXY crash below 100 is registering. Crude ($USO rank 3, MNTM 7) momentum has faded sharply from 21 two sessions ago as oil pulls back from $119. Gold ($GLD rank 32, MNTM −31) has PLUMMETED to its lowest ranking of the series despite today’s bounce — the cumulative damage is devastating. S&P ($SPY rank 28, MNTM −22) deeply negative. NOTE: Today’s gold bounce and oil pullback are NOT yet reflected in this data which captures yesterday’s close.

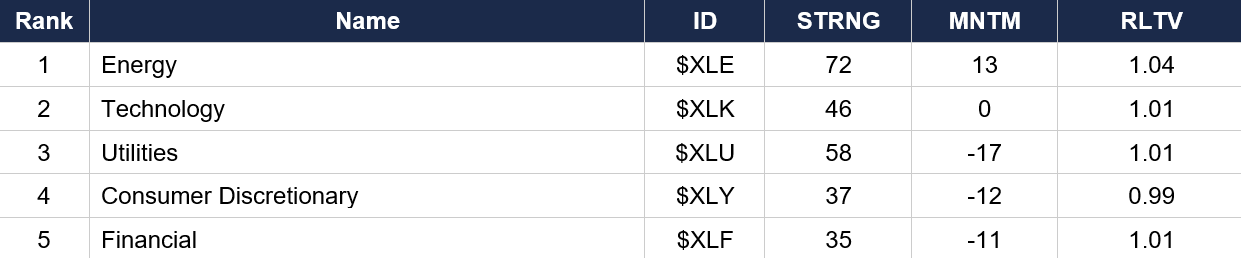

Sector ETFs — Top 5

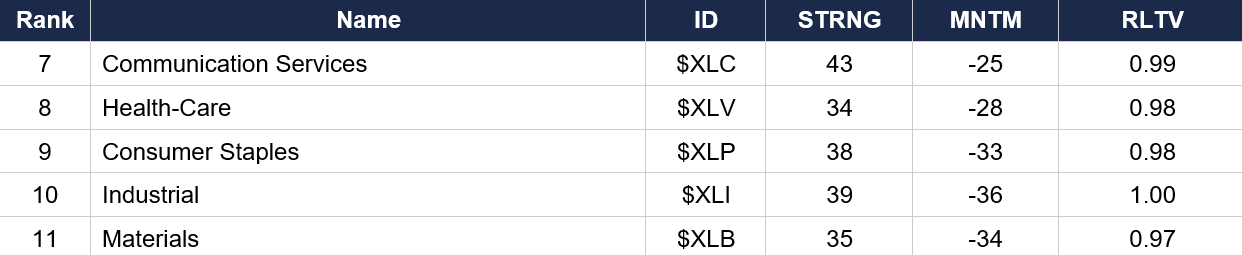

Sector ETFs — Bottom 5

Regime signal: Energy ($XLE, MNTM 13) has SURGED to the highest sector momentum of the entire series — the Brent $100–119 range has been transformative for energy equities. Technology ($XLK, MNTM 0) is at ZERO momentum — the exact inflection point. Financial ($XLF rank 5, MNTM −11) has risen to the top 5 for the first time as banks benefit from higher rates and steeper curves. Communication Services ($XLC rank 7, MNTM −25) has dropped sharply from rank 4. Materials ($XLB, MNTM −34) and Industrial ($XLI, MNTM −36) remain the weakest sectors. Consumer Staples ($XLP rank 9, MNTM −33) continues deteriorating — even defensives provide no shelter.

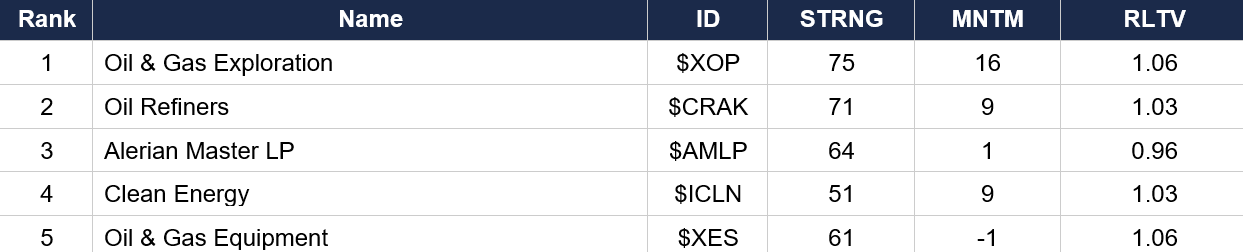

Industry ETFs — Top 5

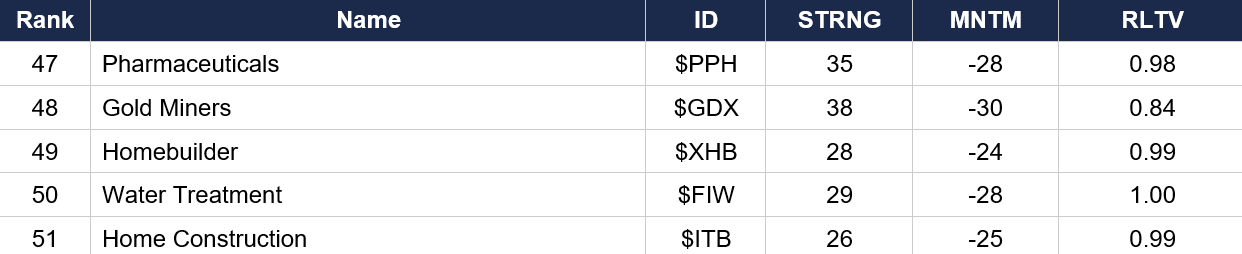

Industry ETFs — Bottom 5

Regime signal: Oil & Gas Exploration ($XOP, MNTM 16) at the highest industry momentum of the series. Clean Energy ($ICLN rank 4, MNTM 9) continues its rise as $100+ oil accelerates the alternative energy thesis. Gold Miners ($GDX rank 48, MNTM −30, RLTV 0.84) is being DEVASTATED by the gold crash — the lowest RLTV in the entire industry table. Semiconductor ($SMH rank 18, MNTM −5) slightly improved but still negative despite Micron’s historic beat. Aerospace-Defense ($ITA rank 46, MNTM −33) continues plummeting despite the war escalation. Home Construction ($ITB) and Homebuilder ($XHB) at the absolute bottom.

4. MORNING DATA REACTION

No major US economic data releases today. This is a light-calendar Friday at the end of the most intense week of the entire series: PPI (+0.7%, hot), FOMC (hold, one cut preserved but bar raised), four European central bank decisions (all held, all hawkish-leaning), Micron’s historic beat (ignored), gold’s $342 single-session crash, and the South Pars energy infrastructure escalation.

Yesterday’s central bank results: ECB held at 2.0% (deposit facility), raised 2026 inflation forecast to 2.6% from 2.0%, said the war will have “material impact on near-term inflation through higher energy prices.” BoE held at 3.75% (unanimous), but MPC member Catherine Mann shifted from considering a cut to “considering a longer hold, or even a hike.” The BoE now expects inflation could reach 3.5% by Q3 2026 (from 2.0% February forecast). SNB held at 0%, stressed willingness to intervene in FX markets. Riksbank held. All four signaled the war has fundamentally altered the inflation outlook. Markets pricing >2 ECB hikes and ~40bp BoE tightening in 2026 — a dramatic reversal from pre-war cut expectations across the board.

The data arc for the week: PPI +0.7%/3.4% YoY (goods +1.1%, war pass-through confirmed). FOMC: one cut 2026, core PCE raised to 2.7%. Jobless Claims 205K (tight labor). Michigan Sentiment prelim March was 55.5 (2nd percentile, released March 13). Micron: EPS $12.20 vs $9.31, Q3 guide $33.5B (ignored). FedEx: beat + raised FY26 guidance. The pattern: inflation data is getting WORSE while growth data is mixed-to-weak. The stagflation diagnosis is now confirmed across consumer prices (CPI 2.4%), producer prices (PPI 3.4%), the Fed’s preferred gauge (core PCE 3.1%), GDP (0.7%), labor (−92K NFP), and consumer confidence (Michigan 55.5).

Next key dates: Michigan Sentiment FINAL March 27. Next FOMC May 6–7. PPI March releases April 14. The market is now in a data desert until late March — war headlines will dominate.

5. THE DYRH READ

Regime: Bifurcated Stagflation — Tentative Stabilization with Bear Steepener Complication. Gold bouncing and oil pulling back are the most constructive signals since Day 14. But the bond market refuses to validate the de-escalation narrative. Confidence: Moderate.

Yield Curve: Bear Steepener — Yesterday’s Bull Steepener Lasted One Session. The entire curve is selling again: 2Y +6.1 bps to 3.856%, 5Y +5.8 bps, 10Y +5.1 bps to 4.300%, 30Y +3.4 bps to 4.875%. The front end is leading in absolute terms — the 2Y is climbing back toward the fed funds upper bound (3.75%). The 30Y at 4.875% is approaching the psychologically critical 5.00% barrier — 12.5 bps away. MOVE at 84.88 is 0.37 points from its war high (85.24). Market pricing: NO rate cuts until 2027. Powell’s “bar is higher for cuts” has cemented the hawkish hold. The bond market sees the inflation damage as DONE regardless of how the war resolves — hot PPI, core PCE 2.7%, and $95+ oil are structural, not transitory. The bond market is the one asset class NOT buying the de-escalation narrative.

Gold Bouncing — Forced Liquidation Exhausting? Gold +1.46% to 4,673.1—theFIRSTgreensessionsincetheforced−liquidationcascadebegan.Silver+1.354,673.1 — the FIRST green session since the forced-liquidation cascade began. Silver +1.35%, platinum +1.53%. After crashing $638 (−12%) from pre-war during an active war, the precious metals complex is finally finding a floor. If gold closes green today, the leveraged-fund margin-call cycle is exhausting. But gold at $4,673 is still $638 below pre-war — the damage is massive. Gold Miners ( 4,673.1—theFIRSTgreensessionsincetheforced−liquidationcascadebegan.Silver+1.35GDX) at RLTV 0.84, the lowest in the entire industry table, shows the carnage in the equity expression.

Oil Pulling Back Despite Ongoing Attacks. Brent −1.65% to $106.86 (down from $119 intraday Thursday). WTI −1.00% to $94.59. Kuwait’s refinery hit AGAIN overnight but oil is falling. The market is pricing de-escalation signals: Netanyahu’s South Pars pledge, Bessent’s unsanction hint, and Netanyahu saying the war may “end sooner than people think.” Natural gas −3.10% reverses the South Pars/Qatar fear. The Brent pullback from $119 to $107 in ~18 hours is a $12 swing — the market is trying to price a ceiling. But Brent is still $34 above pre-war (+46.6%). Saudi officials told the WSJ prices could hit $180/bbl if disruptions last through late April. Qatar’s Ras Laffan: 17% LNG capacity lost, 3–5 year repair.

Equities: Tentatively Stabilizing at 200-Day MA. ES at 6,641.50 (−0.28% pre-market) — “mildly negative” is constructive relative to yesterday’s apocalypse. DAX +0.98% recovering. Nikkei +0.29%. The 200-day MA (~6,619 on S&P cash) has held on Days 12 and 16 — a third test today would have lower odds. Russell breadth surged +43% yesterday (R2FD from 28.34 to 40.65) while S&P breadth barely moved (31.80) — the widest Russell/S&P breadth divergence of the war. Small caps improving while large caps remain stressed = size-factor bifurcation. Mag 7 all red pre-market but modest moves. FedEx +1.82% on beat/raise is the single-stock catalyst.

FX and Volatility: Dollar Below 100, VIX Oscillating Around 25. DXY at 99.130 (+0.10%) consolidating below 100 after yesterday’s −1.03% crash (largest of the war). The dollar crash below 100 + JPY +1.29% yesterday was the purest flight-to-safety signal since Day 8. Today JPY is reversing (−0.56%) as panic fades. VIX at 24.77 (+2.95%) is edging back toward the 25 crisis threshold — third session of testing this line from both sides. BTC +0.21%. MOVE at 84.88 near war highs. The vol picture: equity vol oscillating around crisis, bond vol near war peaks.

6. THE GAME PLAN

Today’s Key Events: No major US economic data. Light earnings calendar. War headlines dominate. Ongoing: Bessent “unsanction” Iranian oil timeline (10–14 days); Kharg Island occupation consideration; Kuwait refinery fires. March 27: Michigan Sentiment FINAL. Next FOMC: May 6–7.

The Bull Case: Gold bouncing (+1.46%) while oil pulls back (Brent −1.65%) is the most constructive cross-asset signal since Day 14. De-escalation rhetoric (Netanyahu, Bessent) is being priced. The 200-day MA has held twice. Russell breadth surged +43%. DAX +0.98% recovering. COR1M falling (stock-specific alpha returning). Bessent’s 140M barrel unsanction could ease prices in 10–14 days. Netanyahu said the war may “end sooner than people think.” If gold sustains above $4,650 and oil stabilizes $105–110, the bifurcated regime transitions to broad recovery. FedEx beat/raise shows corporate earnings can survive the shock.

The Bear Case: The bear steepener returned after one session — the bond market sees permanent inflation damage. 30Y at 4.875%, approaching 5.00%. MOVE at 84.88 near war highs. S&P breadth still at 31.80 (extreme washout). VIX edging back toward 25. Market pricing NO cuts until 2027. Physical attacks continue (Kuwait refinery). Qatar’s Ras Laffan: 3–5 year repair, 17% LNG lost. Iran warned “zero restraint.” Saudi officials see $180 oil if disruptions last. Gold at $4,673 is still $638 below pre-war — the bounce is marginal vs. the damage. SPHB worst in pre-market = factor rotation flipping defensive. The gap between de-escalation rhetoric and physical reality is where the risk lives.

Regime: Bifurcated Stagflation — Tentative Stabilization with Bear Steepener Complication. Gold and oil sending constructive signals. Equities holding the 200-day MA. But the bond market refuses to validate — the 30Y approaches 5%, MOVE near war highs, and no rate cuts priced until 2027. The market is bifurcated: equities and small caps improving, bonds and precious metals still in crisis. Week 4 of the war begins Monday.

Watch List

Gold bounce durability — the forced liquidation test — First green in 3 sessions after $638 crash. If gold closes above $4,700, the margin-call cycle is exhausting. If it reverses below $4,600, a second liquidation wave is possible. The single most important cross-asset signal.

30Y approaching 5.00% — At 4.875%, only 12.5 bps from the psychologically critical level. MOVE at 84.88 near war highs. A breach of 5.00% would represent a new regime — “bond market crisis” layered on stagflation. Yesterday’s bull steepener lasted one session.

200-day MA — third test — ES cash ~6,619. The MA held on Days 12 and 16. A third test has lower odds of holding. If it breaks, systematic trend-following selling triggers. This is the last major technical support.

De-escalation rhetoric vs. physical reality — Netanyahu pledges restraint, Bessent hints at oil release, but Kuwait refinery hit AGAIN, Iran warns “zero restraint,” Qatar faces 3–5 year repair. The gap between words and actions is the market’s biggest risk.

Week 4 begins Monday — The war enters its fourth week. The data desert means war headlines dominate. Michigan Sentiment FINAL March 27. Next FOMC May 6–7. Bessent’s unsanction timeline (10–14 days) means potential oil supply relief by late March/early April.

Morning check: the end of the most intense week since the war began. Gold is bouncing for the first time since the liquidation. Oil is pulling back from $119 despite continued attacks. De-escalation signals are being priced. But the bond market is the skeptic — the 30Y approaches 5%, MOVE is near war highs, and no rate cuts are priced until 2027. The market is bifurcated: one half stabilizing, the other in structural repricing. The 200-day MA has held twice. Gold’s bounce and the bond market’s rejection will determine whether Week 4 brings recovery or another wave down.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.