☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: The de-escalation trade is dead. Oil has surged +$10 from Tuesday’s $83.45 close back above $93 in 48 hours. Brent at $98.37 (+6.95%) is approaching $100 for the SECOND TIME. Three more commercial ships struck overnight in the Persian Gulf — attacks are SPREADING beyond Hormuz into Iraqi waters for the first time (two oil tankers hit near Basra). Iran’s military warned: “Get ready for $200 oil.” Energy Secretary Wright confirmed the Navy is “NOT YET READY” to escort ships through Hormuz and won’t be until end of month — meaning the strait remains effectively closed for 2–3 more weeks. THE CRITICAL DEVELOPMENT: ALL 7 Mag 7 names are RED in pre-market for the first time in sessions. The tech shield that held up the S&P while breadth collapsed is CRACKING. ES at 6,740.75 (−0.57%) is threatening to break below 6,750 for the first time since the series began. SOXX −1.07% after-hours. SPHB −1.26%. IJR −1.30%. VIX spiking +6.27% to 25.75. Yields have PAUSED their ascent marginally (30Y at 4.872% vs. yesterday’s 4.878% high) but oil surging back toward $100 will reignite the bond selloff. Gold marginally positive (+0.21%) attempting stabilization. Dollar at 99.445 — new series high. The IEA’s historic 400M barrel SPR release yesterday was immediately overwhelmed — oil rose +4.55% on the day of the announcement. Policy intervention has failed. Gas at $3.61/gallon (from $3.00 pre-war).

The Number That Matters: Brent at $98.37. For the second time in this war, oil is approaching $100. The first time (Day 8, $119.50 spike) was treated as a panic overshoot. If $100 is breached AGAIN, it confirms the disruption is STRUCTURAL, not a spike. Energy Secretary Wright’s admission that the Navy can’t escort through Hormuz until end of month means the physical supply disruption has a minimum 2–3 week timeline. Rapidan Energy: IEA drawdowns “can at best only offset a fraction of the ~15M bbl/day net supply loss.” The IEA’s 400M barrel release was historic but insufficient — the market dismissed it in real-time by pushing oil higher. Iran’s $200 warning is hyperbole, but $100–120 is now a realistic range if Hormuz remains closed.

The Setup: This is the session where “stealth stagflation” stops being stealth. For four sessions, the S&P index looked calm (−0.1% to +0.8%) while breadth collapsed to extremes (S5FD hit 16.50, S5TW at 26.24 — series lows). Mega-cap tech masked the damage. Today, ALL 7 Mag 7 are red in pre-market. If tech follows through to the downside, the air pocket materializes — there is no breadth support underneath. ES at 6,740 is testing 6,750 for the first time. Oil is surging back toward $100 with the Navy unable to provide escorts for weeks. The IEA’s 400M barrel release failed. Iran is expanding attacks to Iraqi waters. The regime is unambiguously a Stagflationary Crisis with the equity shield now cracking. NOTE: February PPI has been rescheduled by the BLS to March 18 due to the government shutdown — today’s data is Jobless Claims at 8:30 AM only. Friday is the massive data day: Michigan Sentiment (first war-shock consumer survey), JOLTS, and potentially PCE/GDP.

2. OVERNIGHT SESSION RECAP

Asia-Pacific

TOPIX +0.17% — barely green, the only positive global index. Nikkei −0.53%. Asia showing exhaustion after the volatile week. The oil surge back to $93+ WTI is re-pressuring Asian import-dependent economies.

Europe

DAX essentially flat (−0.01%), Euro Stoxx −0.42%. Europe holding up marginally better than US pre-market but the renewed oil surge toward $100 is a direct threat to the European industrial base. The IEA’s 400M barrel release provided a brief psychological floor yesterday that is now being tested.

US Pre-Market

Day 13 — Major Escalation. Three more commercial ships struck overnight. Two OIL TANKERS hit by projectiles near Iraq’s southern ports at Basra — first oil-related strikes in Iraqi waters since the war began. Iran claimed responsibility for one (US-owned tanker). Container ship struck 35 nautical miles north of Jebel Ali (major port near Dubai). Two drones fell near Dubai International Airport — 4 injured, airspace briefly closed. UAE defense ministry responding to Iranian missile and drone attacks. Iran’s military spokesman warned of $200 oil. Mojtaba Khamenei reportedly giving first public address — was wounded in airstrike, 4 days of silence. Iran death toll 1,200+, Lebanon 634, Israel 12, US 7 killed.

Trump: “we won” but “we’ve got to finish the job” — continued mixed messaging. Energy Secretary Wright told CNBC the Navy is “not yet ready” to escort ships through Hormuz and won’t be until end of month. All military assets focused on destroying Iran’s offensive capabilities. Kremlin said Russia-US energy cooperation discussions are “being discussed” — potential Russia sanction relief to ease oil markets.

Prior session (March 11 close): S&P −0.08%, Dow −0.61%, Nasdaq +0.08%. IEA announced historic 400M barrel release — oil STILL rose +4.55% (market dismissed the policy intervention). ZB −1.13% (worst bond move of the series). 30Y 4.878% (4th consecutive new high). MOVE 78.59 (+2.96%). Gold −1.20%. XLE +2.48% (back to #1 sector). CPI in-line at +0.3%/2.4% YoY (pre-war data, analytically stale).

Today’s data: Jobless Claims at 8:30 AM — first weekly claims capturing the war period more fully. NOTE: February PPI has been RESCHEDULED by the BLS to March 18 due to the government shutdown delay. Earnings: Adobe (ADBE) after close — software demand durability test. Dollar General (DG) before open — low-income consumer barometer. Lennar (LEN) — housing under rising rates. Dick’s Sporting Goods (DKS). Friday is MASSIVE: Michigan Consumer Sentiment (first war-shock survey), JOLTS (January), and potentially PCE/GDP second estimate.

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 03/11/26. Provided for informational purposes only; not as investment advice.

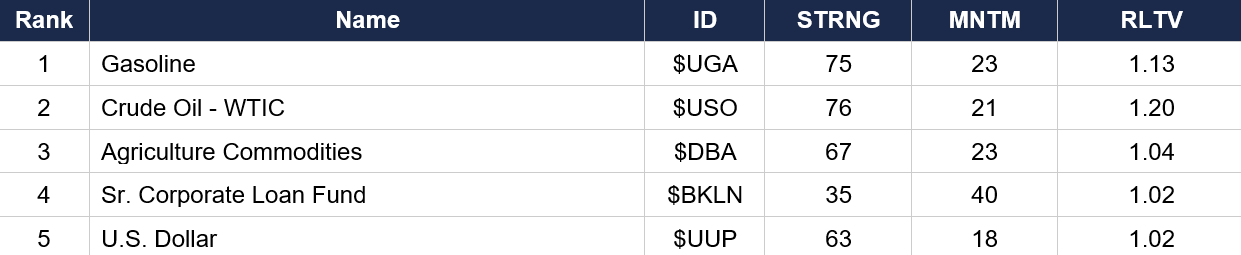

Asset Classes — Top 5

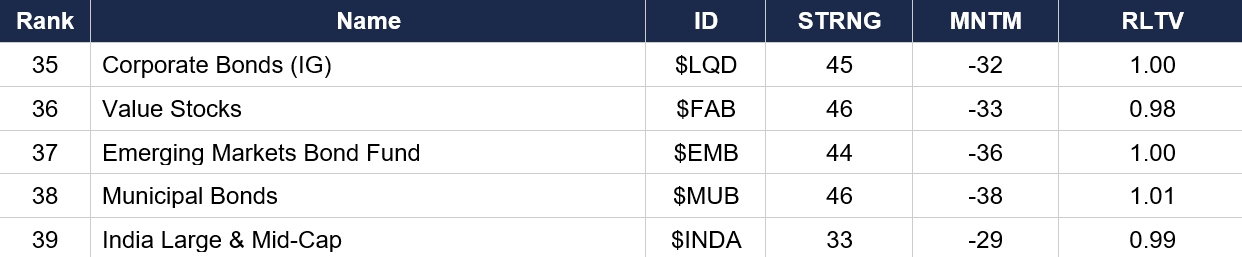

Asset Classes — Bottom 5

Regime signal: Gasoline ($UGA) retakes rank 1 from crude — the refined products tightness continues to lead. Senior Corporate Loans ($BKLN) has surged to rank 4 with MNTM 40 — the HIGHEST momentum reading of any non-energy asset class in the series. Floating-rate credit is the standout asset in a rising-rate, rising-oil environment. VIX ($VXX) at rank 14 with MNTM −4 — vol has dropped out of the top 5 despite today’s +6.27% spike, reflecting the prior session’s compression. Bitcoin ($IBIT rank 6, MNTM 23) and Ethereum ($ETHA rank 7, MNTM 23) both holding strong — crypto as alternative haven. Gold at rank 13 (MNTM −4) still negative. Nasdaq ($QQQ rank 9, MNTM 9) diverging sharply from S&P ($SPY rank 16, MNTM −4) — the tech-vs-broad-market divide. Value ($FAB, MNTM −33) among the worst momentum — value stocks being destroyed. EM Bonds ($EMB, MNTM −36) and Munis ($MUB, MNTM −38) remain extreme negative.

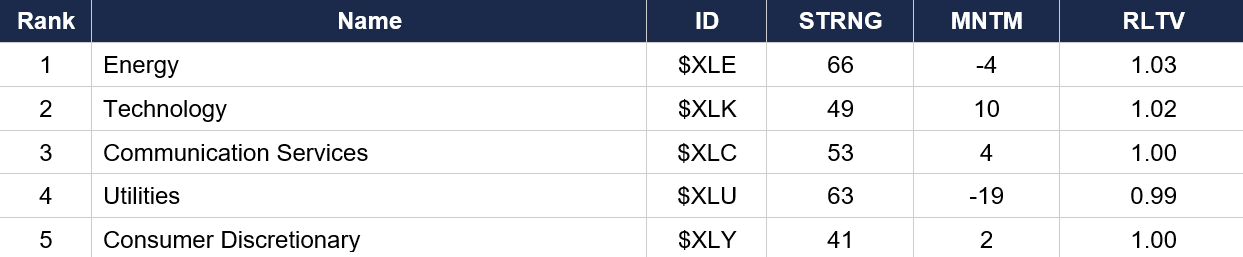

Sector ETFs — Top 5

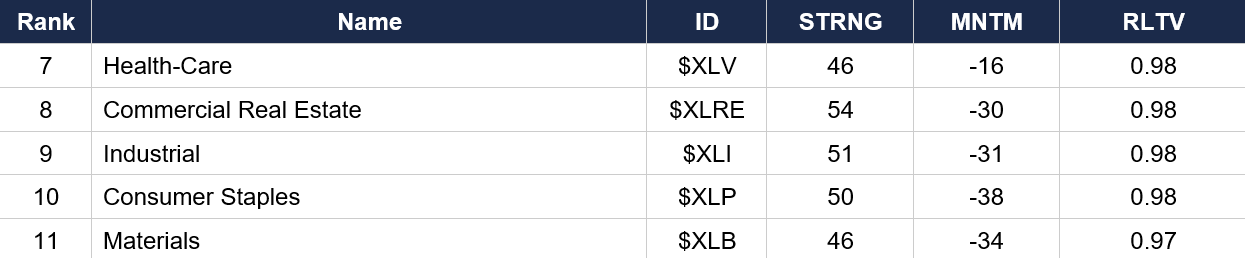

Sector ETFs — Bottom 5

Regime signal: Energy ($XLE) has RECLAIMED rank 1 — XLE was +2.48% yesterday as the only green sector. The energy trade is BACK as oil surges toward $100. Technology ($XLK) at rank 2 with MNTM 10 — the strongest positive sector momentum. But ALL 7 Mag 7 are red pre-market today, testing whether this tech momentum can survive. Commercial Real Estate ($XLRE) collapsed to rank 8 (MNTM −30) from rank 5 yesterday — rate sensitivity devastating the sector as 10Y approaches 4.23%. Consumer Staples ($XLP, MNTM −38) and Materials ($XLB, MNTM −34) remain the worst sectors.

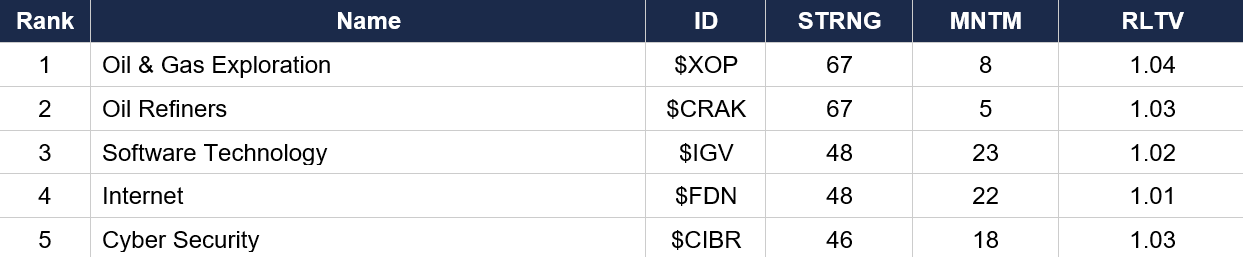

Industry ETFs — Top 5

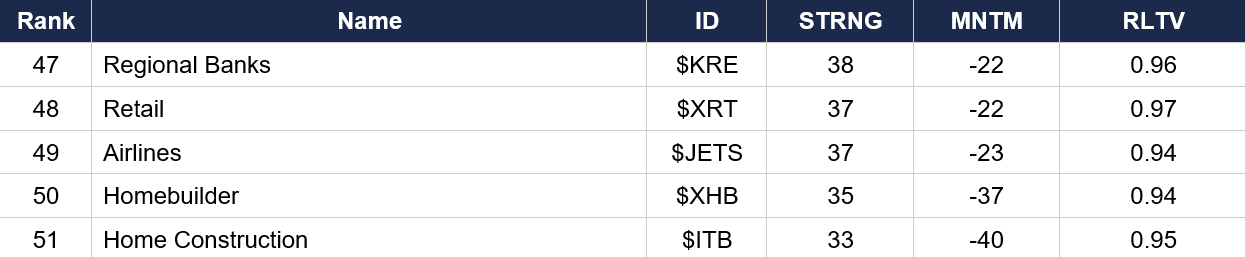

Industry ETFs — Bottom 5

Regime signal: Oil & Gas Exploration ($XOP) and Oil Refiners ($CRAK) have seized the top 2 industry ranks — the energy complex is fully re-asserting dominance as oil surges back toward $100. Software ($IGV, MNTM 23) and Internet ($FDN, MNTM 22) continue to show strong momentum but SOXX −1.07% in after-hours suggests the tech rally is under threat. Clean Energy ($PBW rank 10, MNTM 5) still showing positive momentum as $100 oil accelerates the alternative energy investment thesis. Aerospace-Defense ($ITA rank 24, MNTM −15) continues selling for the FIFTH session despite war escalation — the de-escalation pricing is stubbornly baked in even as events contradict it. Home Construction ($ITB, MNTM −40) is the worst industry momentum on the entire board.

4. MORNING DATA REACTION

NOTE: February PPI has been RESCHEDULED by the BLS to March 18, 2026 due to the government shutdown delay. The DYRH referenced PPI for today but it is NOT releasing. Today’s only data release is Initial Jobless Claims at 8:30 AM.

Jobless Claims context: Prior week was 213K (unchanged from the week before), below expectations of 215K — labor market remained stable through late February. Today’s claims will be the first to more fully capture the war period. A spike above 225K could signal early war-related disruption (supply chain layoffs, energy-sector adjustments). At/below 215K confirms the labor market is resilient despite the oil shock — for now.

Yesterday’s CPI recap (released Wednesday March 11): Headline +0.3% MoM, +2.4% YoY. Core +0.2% MoM, +2.5% YoY. Both in-line. Pre-war February data — inflation was contained at 2.4% before the strikes. The bond market IGNORED it, pushing yields to new series highs. The real inflation story is being written in the March/April data that will capture $80–120 oil.

Friday is a MASSIVE data day: Michigan Consumer Sentiment (preliminary March) — the FIRST consumer survey capturing the war and oil shock. If sentiment craters, recession fears intensify dramatically. JOLTS (January, rescheduled to March 13). Potentially PCE and GDP second estimate. This week’s full data recap: ISM Manufacturing (Mon 3/2): 52.4, Prices Paid 70.5. ISM Services (Wed 3/4): 56.1. ADP (Wed 3/4): +63K. NFP (Fri 3/6): −92K. CPI (Wed 3/11): +0.3%/2.4% (in-line). The data arc: the pre-war economy was bifurcated, inflation was contained, and then the oil shock hit.

5. THE DYRH READ

Regime: Stagflationary Crisis — Equity Shield Cracking. Oil surging back toward $100 with the Navy unable to provide Hormuz escorts for weeks. All 7 Mag 7 red in pre-market. The tech shield that masked the breadth catastrophe is breaking. Confidence: High on characterization.

Yield Curve: Bear Steepener Pausing Briefly. After four consecutive sessions of new 30Y highs, yields are MARGINALLY lower on the long end: 30Y at 4.872% (−0.6 bps from yesterday’s 4.878%). 10Y at 4.226% (−0.2 bps). But the front end is still rising: 2Y +0.2 bps to 3.655%. The bond selloff may be exhausting itself temporarily. However, with oil surging back toward $100, any respite will be short-lived. Cumulative: 10Y at +27.7 bps from pre-war. ZB still red (−0.30%) — selling pressure hasn’t fully abated. If Brent breaches $100 again, the long end resumes its climb.

Oil Approaching $100 — For the Second Time. WTI +6.76% to $93.15. Brent +6.95% to $98.37. The IEA’s 400M barrel SPR release was immediately overwhelmed — policy intervention has failed. The physical supply disruption is structural: Navy can’t escort until end of month, Hormuz remains closed, attacks spreading to Iraqi waters. Iran warning of $200 oil. Cumulative: WTI +39.0% from pre-war; Brent +35.0%. If Brent breaches $100 for the second time, it confirms the disruption is not a spike but a structural reality. Gold +0.21% attempting marginal stabilization after two days of selling.

THE EQUITY AIR POCKET RISK — ALL MAG 7 RED. For the first time in sessions, ALL seven mega-cap names are red in pre-market: NVDA −0.77%, META −0.69%, AMZN −0.60%, GOOG −0.53%, MSFT −0.34%, AAPL −0.22%, TSLA −0.02%. SOXX −1.07% after-hours. SPHB −1.26%, IJR −1.30%. For four sessions, 5–6 of 7 Mag 7 stocks were green, propping up the index while breadth collapsed (S5FD hit 16.50). If tech follows through today, the air pocket materializes — there is no breadth support underneath. ES at 6,740.75 is testing the 6,750 level. This is potentially the session where the index finally REFLECTS the underlying breadth catastrophe.

Breadth: Series Lows Continue Deepening. S5FD bounced from 16.50 to 25.44 (+54%) but S5TW (20-day) made a NEW series low at 26.24 — only 26.2% of S&P stocks above their 20-day MA. S5FI at 38.17, S5OH breaking below 50 (48.70). The medium-term and long-term breadth continues to deteriorate even as the 5-day reading bounced. The structural damage is compounding. COR1M at 29.18 approaching 30 — macro driving virtually everything.

FX: Dollar at Series Highs. DXY at 99.445 — the highest of the entire war series. Every G10 currency red except JPY (barely green at +0.02%). CHF −0.30%, EUR −0.25%. The dollar is the only shelter again. BTC −0.30% — crypto not providing haven. The dollar’s persistent strength at series highs reflects continued global capital flight to USD as the war disruption intensifies.

6. THE GAME PLAN

Today’s Key Events: Jobless Claims 8:30 AM (NOTE: February PPI rescheduled to March 18 by BLS). Mojtaba Khamenei’s first public address. Russia-US energy cooperation discussions. Earnings: Dollar General (DG) before open, Adobe (ADBE) after close, Lennar (LEN), Dick’s Sporting Goods (DKS). Friday: Michigan Consumer Sentiment (FIRST war-shock survey), JOLTS (January). War headlines continuous.

The Bull Case: The 30Y yield paused after four consecutive new highs — the bond selloff may be exhausting itself. S5FD bounced from 16.50 to 25.44 — the 5-day breadth washout is mean-reverting. Gold marginally stabilizing (+0.21%). The Kremlin signaling Russia-US energy cooperation could ease oil supply concerns. Mojtaba Khamenei reportedly wounded — leadership instability could accelerate negotiation. Trump continues saying “we won” — de-escalation rhetoric hasn’t fully died. If Hormuz mine-clearing succeeds and even partial transit resumes, oil collapses. Adobe beat could reinforce the software-as-shelter narrative.

The Bear Case: ALL 7 Mag 7 red pre-market — the tech shield is cracking. Oil surging back toward $100 for the SECOND time. IEA’s 400M barrel release was immediately overwhelmed. Navy “not ready” for Hormuz escorts until end of month. Three more ships struck overnight including first-ever attacks in Iraqi waters. Iran warning of $200 oil. ES breaking below 6,750 for the first time. SOXX, SPHB, IJR all crashing in after-hours. VIX +6.27%. S5TW at series low (26.24). The air pocket beneath the mega-cap shell is about to be tested. If Brent breaches $100 again, it confirms structural disruption. Dollar at series highs confirms global capital flight. Gas at $3.61/gallon crushing consumers.

Regime: Stagflationary Crisis — Equity Shield Cracking. Oil surging back toward $100 with no escort capability for weeks. Policy intervention (IEA 400M barrels) failed. All 7 Mag 7 red for the first time. The tech-driven illusion of index stability is breaking. Beneath the surface, breadth is at series lows, yields at series highs, and the only things working are oil, the dollar, and cash. If ES closes below 6,750 today, the index finally reflects what breadth has been screaming for days.

Watch List

Brent $100 — second breach — At $98.37, Brent is within striking distance. First time was treated as a spike. Second time = STRUCTURAL. Would confirm the IEA release failed and Hormuz closure is the defining market reality until the Navy can escort (end of month at earliest).

All 7 Mag 7 red — air pocket test — First time in sessions. If tech follows through, ES breaks below 6,750 with no breadth support underneath. The four-session divergence between calm indexes and crushed breadth resolves to the downside.

Jobless Claims 8:30 AM — First weekly claims more fully capturing the war period. Above 225K = early war-related disruption signal. Below 215K = labor market resilient for now. NOTE: PPI rescheduled to March 18.

Key Earnings — Dollar General (DG) before open — low-income consumer barometer as gas surges past $3.61. Adobe (ADBE) after close — software demand under stagflation; does Oracle’s cloud strength translate? Lennar (LEN) — housing under 4.87% 30Y yields and rising mortgage rates.

Friday’s massive data day — Michigan Consumer Sentiment (first war-shock survey — if sentiment craters, recession fears compound). JOLTS (January). This will set the tone for next week’s FOMC meeting (March 17–18).

Morning check: the equity shield is cracking. All 7 Mag 7 red for the first time. Oil surging back toward $100 with the Navy unable to escort through Hormuz for weeks. The IEA’s 400M barrel release was immediately overwhelmed. Iran is expanding attacks to Iraqi waters and warning of $200 oil. S5TW at series lows. The four-session illusion of index stability is breaking. If ES closes below 6,750, the breadth catastrophe finally becomes an index reality. The regime is a Stagflationary Crisis — and the last line of defense is giving way.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.