☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: WSJ BOMBSHELL — TRUMP WILLING TO END WAR WITHOUT REOPENING HORMUZ. FUTURES SURGE +1.2%. OIL SURGES TO $117 BRENT. YIELDS POST BIGGEST 2-DAY DECLINE OF THE WAR. VIX BELOW 30. Q1 ENDS TODAY.

The Wall Street Journal dropped the most important geopolitical headline since the war began: President Trump told aides he is willing to END the military campaign against Iran even if the Strait of Hormuz REMAINS LARGELY CLOSED. The rationale: reopening Hormuz would push the conflict beyond Trump’s 4-6 week timeline. The US would achieve its core goals — hobbling Iran’s navy and missile stocks — then wind down hostilities. Diplomatic pressure would continue post-ceasefire. If diplomacy fails, Washington would push European and Gulf allies to lead the Hormuz operation. Military options exist but are ‘not his immediate priority.’

The market is treating this as massively de-escalatory: ES +1.18%, NQ +1.15%, RTY +1.55% (small caps leading again), DAX +1.20%, Nikkei +1.40%. All 7 Mag 7 green in after-hours (AMZN +1.72% leading). All sectors green with cyclicals leading (XLI +1.21%, XLY +1.31%, XLF +1.28%) and defensives lagging (XLU +0.35%). SPHB +1.10% vs SPLV +0.52% = risk-on factor rotation. DXY retreating from 100.37 to 100.005 — all G10 currencies gaining vs USD except CAD. VIX at 28.31 is BELOW 30 on a close basis for the first time since Day 21 — the panic threshold has been recaptured. MOVE at 108.33 (below 110). Yields continue falling in a bull flattener for a second session: 2Y −3.5 bps to 3.801%, 5Y −4.7 bps to 3.943%, 10Y −3.9 bps to 4.311%, 30Y −2.4 bps to 4.885%. The cumulative 2-day yield decline (2Y −11.3, 5Y −12.5, 10Y −11.7, 30Y −8.0 bps) is the BIGGEST of the entire war, driven by Powell’s rate hike removal Monday + the WSJ headline.

BUT — and this is the critical analytical nuance — the WSJ headline is a DOUBLE-EDGED SWORD. ‘End the war’ is bullish for equities. ‘Hormuz stays closed’ is bullish for OIL. Brent surged to approximately $117.48 intraday per CNBC (up ~4%), with WTI above $103. Iran’s parliament has simultaneously approved a TOLL PLAN for Hormuz passage — including ‘financial arrangements and rial toll systems’ and ‘prohibition of Americans and the Zionist regime from passing through.’ This is Iran INSTITUTIONALIZING the blockade. A ceasefire without Hormuz reopening transforms a ‘war trade’ into a ‘structural energy crisis trade’ — the $100+ oil environment becomes PERMANENT, not temporary. Gold at $4,611.6 (+1.19%) is extending its recovery for a 4th consecutive session, now +$235.6 from the war low. Silver surging +3.74%. The forced liquidation is definitively over.

Additional overnight: Iran struck a Kuwaiti oil tanker in Dubai waters (Bloomberg) — crew safe, fire reported. Trump on Truth Social told allies to ‘go to the Strait, and just TAKE IT’ and called the UK and France ‘VERY UNHELPFUL.’ Netanyahu told Newsmax the war is ‘definitely beyond the halfway point...in terms of missions, not necessarily in terms of time.’ Nvidia announced a $2B strategic investment in Marvell Technology (+11% pre-market). Defense Secretary Hegseth’s broker reportedly sought defense ETF investments pre-war (Financial Times). Apellis Pharmaceuticals surged 138% (Biogen $5.6B acquisition). Q1 ends today — rebalancing flows + JPM options expiration create mechanical support.

The Number That Matters: Brent at approximately $117.48 — SURGING despite a ‘war-ending’ headline.

This is the market’s most important paradox of the entire conflict. On a day when futures rally +1.2% on ‘end the war,’ oil is surging to near its war high because the WSJ report explicitly states Hormuz stays closed. The Brent price tells you the ECONOMIC damage of the war persists even if the MILITARY dimension ends. A ceasefire with $117 Brent means $4+/gallon gas is permanent, inflation pass-through continues, and the Fed cannot cut. The equity rally and the oil surge are CONTRADICTORY — one of them is wrong over any meaningful time horizon. Either the war actually ends AND Hormuz reopens (oil collapses, equities justified), or the war ends and Hormuz stays closed (oil justified, equities must reprice the permanent energy shock).

The Setup: Ceasefire Hopes Collide With Permanent Oil Premium — Relief Bounce #7 With Q1 Mechanical Support.

This is the 7th relief bounce of the war. The prior 6 have all reversed within 1-2 sessions. What’s different this time: (1) Powell killed the rate hike Monday (FedWatch >50% → 2.2%); (2) the WSJ report is genuinely new — it’s the first indication Trump is willing to end the war; (3) the 2-day yield decline is the biggest of the war; (4) VIX below 30, backwardation resolved, MOVE below 110. What’s the same: (1) oil is surging, not falling; (2) Hormuz is closed and Iran is institutionalizing the blockade; (3) Q1 rebalancing creates artificial support; (4) CB Consumer Confidence at 10 AM may crater. Dense data slate today: Case-Shiller at 9:00 AM, Chicago PMI at 9:45 AM, Consumer Confidence + JOLTS at 10:00 AM. Nike after the close. And this is just the warmup — tomorrow brings ADP, Retail Sales (rescheduled from March 16), and ISM Manufacturing all in one session. Friday: NFP released to CLOSED markets on Good Friday — maximum gap risk Monday 4/7.

2. OVERNIGHT SESSION RECAP

Asia-Pacific

Nikkei +1.40%, TOPIX +1.13%. Japan rallying hard on the WSJ headline — if the war ends, Japan’s energy import dependence makes it the biggest beneficiary. The Nikkei’s +1.40% follows yesterday’s mixed session and represents renewed optimism on the ceasefire timeline.

Europe

DAX +1.20%, Euro Stoxx +1.03%. European markets responding to both the WSJ headline and the broader risk-on rotation. The permanent Hormuz closure implication is less immediately priced in European equities but will weigh on European energy costs — the Ras Laffan damage (17% LNG, 3-5 year repair) combined with a permanently disrupted Hormuz creates a structural energy crisis for Europe that persists post-ceasefire.

US Pre-Market

Day 32 of Operation Epic Fury. Q1 2026 Final Trading Day. The session is defined by the tension between the war-ending headline and the permanent oil premium, layered on top of significant mechanical flows (quarter-end rebalancing, JPM options expiration, window-dressing).

THE WSJ REPORT IN DETAIL: Trump and aides concluded that reopening Hormuz would push the conflict beyond his 4-6 week timeline. The US would achieve its main goals — hobbling Iran’s navy and missile stocks — then wind down. Diplomatic pressure would continue post-ceasefire. If diplomacy fails, Washington would push allies to lead. Trump’s Truth Social posts added combative color: told affected countries to ‘go to the Strait, and just TAKE IT,’ attacked the UK for refusing to ‘get involved in the decapitation of Iran,’ called France ‘VERY UNHELPFUL’ for blocking US military supply flights to Israel.

IRAN’S RESPONSE: Parliament approved a Hormuz TOLL PLAN — ‘financial arrangements and rial toll systems’ with prohibition on American and Israeli vessels. This is Iran institutionalizing the blockade, not a temporary military closure. The toll plan implies Iran sees Hormuz control as a PERMANENT post-war leverage tool, not a negotiating chip to be surrendered. Separately, Iran struck a Kuwaiti oil tanker in Dubai waters (Bloomberg) — demonstrating that kinetic operations continue even as ceasefire negotiations advance.

PRIOR SESSION CONTEXT: Monday’s close was deeply mixed despite the biggest bond rally of the war. Powell at Harvard killed the rate hike (FedWatch >50% → 2.2%), sending yields down 5.6-7.8 bps. But equities couldn’t hold: S&P −0.39%, Nasdaq −0.73%, Russell −1.45% (swung −2.31% from pre-market green). XLE −0.96% vs WTI +3.25% — equity-oil decoupling. SOXX −4.23% (Micron −10%). USMV-SPHB spread +2.51% (maximum risk-off). The session showed that even Powell removing the worst-case rate scenario wasn’t enough to support equities against the stagflationary backdrop.

Netanyahu told Newsmax the war is ‘definitely beyond the halfway point...in terms of missions, not necessarily in terms of time.’ This framing is important — ‘missions complete’ is different from ‘timeline complete.’ It aligns with the WSJ report: the US can declare objectives achieved and exit without resolving the Hormuz question.

This week’s calendar (verified via ForexFactory/MNI/Census Bureau): TODAY 9:00 AM — Case-Shiller Home Prices (Jan). 9:45 AM — Chicago PMI (March). 10:00 AM — CB Consumer Confidence (March) + JOLTS Job Openings (Feb). NKE after close. WEDNESDAY 8:15 AM — ADP Employment (March). 8:30 AM — Retail Sales (Feb, rescheduled from March 16). 10:00 AM — ISM Manufacturing PMI (March, consensus 52.3). THURSDAY — Jobless Claims. FRIDAY — GOOD FRIDAY, MARKETS CLOSED. NFP released at 8:30 AM to CLOSED markets (consensus +57K, prior −92K) — maximum gap risk Monday 4/7.

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 03/30/26. Provided for informational purposes only; not as investment advice.

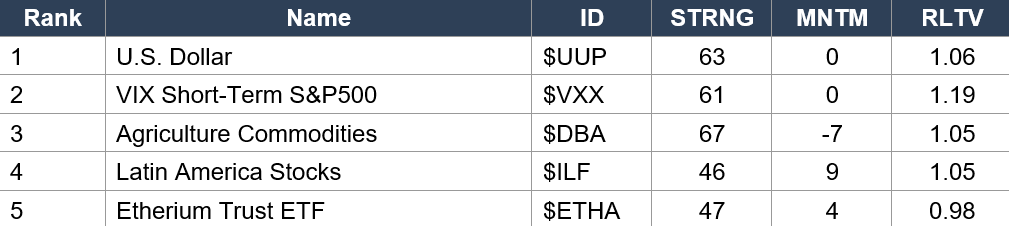

Asset Classes — Top 5

Asset Classes — Bottom 5

Regime signal: The rankings have undergone a DRAMATIC reshuffling. Dollar ($UUP rank 1, STRNG 63, MNTM 0) has vaulted to the top — war-driven safe haven demand has made the dollar the strongest asset of the conflict. VIX ($VXX rank 2, STRNG 61, RLTV 1.19) maintains its elevated position with the highest RLTV of any asset — volatility IS the trade. Agriculture ($DBA rank 3, STRNG 67, MNTM −7) remains strong on food inflation but momentum has turned negative. Latin America ($ILF rank 4, MNTM 9) is a standout — commodity-producing EM benefiting from the energy/materials supercycle. Crude Oil ($USO rank 10, STRNG 68, MNTM −21, RLTV 1.22) has the highest RLTV of any asset at 1.22 despite deeply negative momentum — the oil trade has been volatile but structurally dominant. Gold ($GLD rank 39, MNTM −21, RLTV 1.07) remains DEAD LAST but RLTV has recovered from 0.89 to 1.07 — the forced liquidation damage is healing. S&P ($SPY rank 37, MNTM −11) and Nasdaq ($QQQ rank 38, MNTM −17) at the bottom — US large-cap equities have been the war’s biggest losers. Short-duration bonds ($SHY rank 7, MNTM 10) and MBS ($MBB rank 8, MNTM 8) reflect the rate-hike-removed bull flattener. NOTE: Today’s WSJ-driven equity rally is NOT yet reflected in this data which captures Monday’s close.

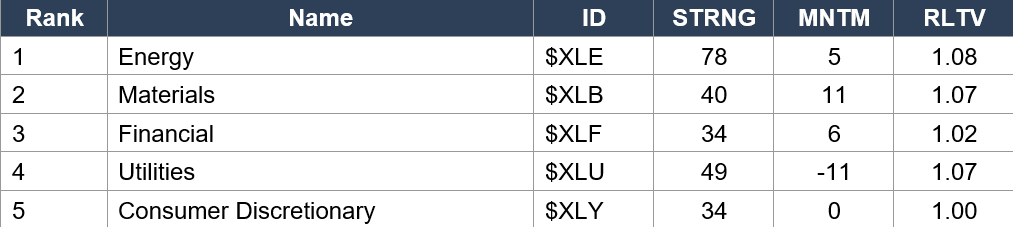

Sector ETFs — Top 5

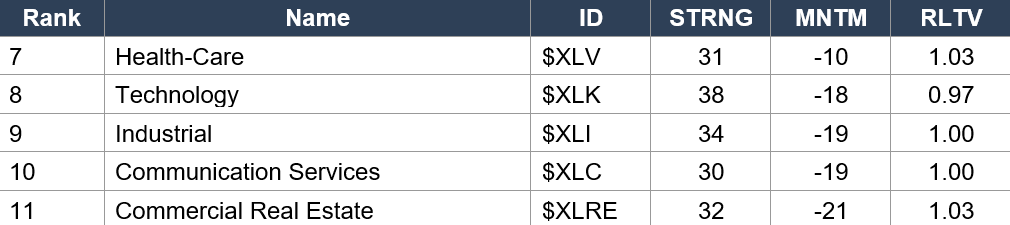

Sector ETFs — Bottom 5

Regime signal: Energy ($XLE rank 1, STRNG 78, MNTM 5, RLTV 1.08) dominates — STRNG 78 is the highest of ANY sector across the entire war series and is 38 points above the next sector. Materials ($XLB rank 2, MNTM 11) has surged to #2 with the strongest momentum of any sector — the commodity inflation trade is broadening beyond just energy. Financial ($XLF rank 3, MNTM 6) remains positive as banks benefit from the steeper curve and higher rates. Technology ($XLK rank 8, MNTM −18, RLTV 0.97) has COLLAPSED — the only sector with sub-1.00 RLTV, meaning tech is underperforming the broad market. This is a profound regime shift: for the first time, tech is a RELATIVE LOSER in the war environment. Commercial Real Estate ($XLRE rank 11, MNTM −21) remains the worst sector — 30Y near 5.00% and 6.38% mortgage rates are devastating. ALL 5 bottom sectors have deeply negative momentum.

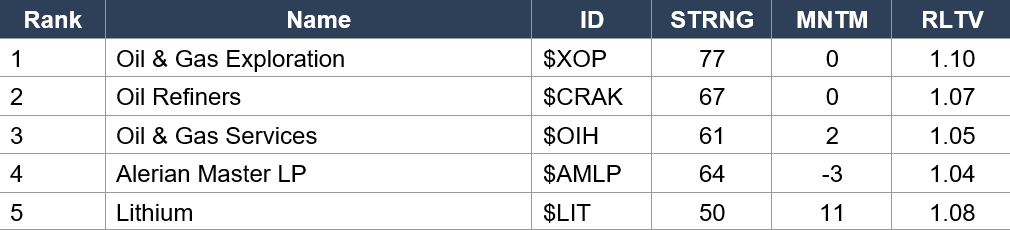

Industry ETFs — Top 5

Industry ETFs — Bottom 5

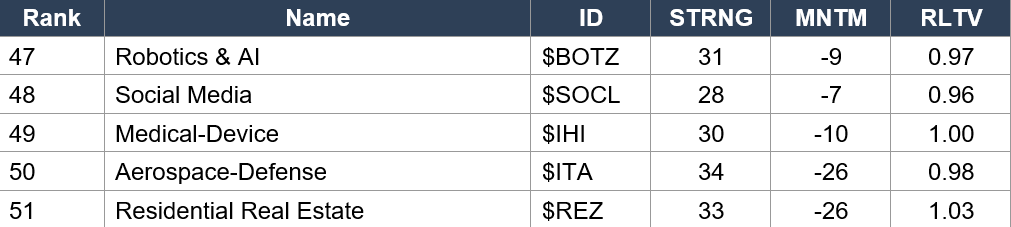

Regime signal: The energy complex still dominates on STRNG ($XOP 77, $CRAK 67, $OIH 61, $AMLP 64) but momentum has flattened to 0 across the top names — the oil trade’s explosive gains have stabilized. Lithium ($LIT rank 5, MNTM 11, RLTV 1.08) is a NEW entrant to the top 5 with the strongest momentum and RLTV of any industry — likely reflecting battery supply chain repricing and war-driven materials demand. Regional Banks ($KRE rank 9, MNTM 11) and Banking ($KBE rank 12, MNTM 10) show strong momentum as the steeper yield curve benefits NIMs. Mortgage REITs ($REM rank 11, MNTM 13) has the highest momentum of any industry — a contrarian signal as rate-sensitive names recover from oversold levels. Aerospace-Defense ($ITA rank 50, MNTM −26) remains one of the worst — the persistent paradox of defense stocks falling during an active war. Residential Real Estate ($REZ rank 51, MNTM −26) again dead last as housing is crushed by 6.38% mortgage rates.

4. MORNING DATA REACTION

No 8:30 AM data releases today. The session’s economic catalysts arrive in a concentrated 60-minute window:

9:00 AM — S&P CoreLogic Case-Shiller Home Price Indices (January).

Housing prices data that predates the war. January data will show the pre-conflict housing market — useful as a baseline but not directly relevant to the war’s current impact. The more important housing signal is mortgage rates at 6.38% (series high, weekly data) and KB Home’s weak earnings guidance from last week.

9:45 AM — Chicago PMI (March).

The Chicago Business Barometer is a composite index that correlates closely with ISM Manufacturing. February’s reading surged to 57.7 (from 54.0), marking the strongest expansion since May 2022. March data will capture the FIRST FULL MONTH of war impact on the Chicago manufacturing region. A drop below 50 would signal that the energy shock is pushing manufacturing into contraction. A hold above 50 with rising Prices Paid would confirm the stagflation thesis. This releases 15 minutes before Consumer Confidence and JOLTS, creating a potential one-two punch at the open.

10:00 AM — CB Consumer Confidence (March) — THE session’s key risk event.

February’s reading was 91.2. The March survey will capture the FULL impact of $4+/gallon gas, the bond market explosion, the stock market crash, the daily war headlines, and inflation anxiety on consumer sentiment. UoM Consumer Sentiment already showed 53.3 (final, Friday) with 1-year inflation expectations at 3.8%. If CB confirms the collapse — particularly a reading below 85 — it reinforces the recessionary narrative even as equities rally on the WSJ headline. A better-than-expected print would suggest consumers are more resilient than surveys indicate.

10:00 AM — JOLTS Job Openings (February).

The Job Openings and Labor Turnover Survey measures labor demand. February data predates the war’s most intense period but provides the baseline labor market health before the March employment shock. The prior reading showed 7.74M openings. A significant decline would signal that hiring was already cooling before the war accelerated the slowdown. JOLTS is particularly important this week because NFP (released to closed markets Friday) will show whether February’s −92K payrolls was a one-off or the start of a trend.

Prior session data context: Powell at Harvard Monday killed the rate hike — FedWatch collapsed from >50% to 2.2%. This was the single most important Fed signal since the FOMC. UoM Consumer Sentiment Final on Friday: 53.3 (lowest reading since late 2022), 1-year inflation expectations 3.8%. The prior week’s data: Durable Goods +0.7% (better than expected), Q4 GDP Final 2.1% (revised up from 0.7%, though this is ancient pre-war data). The cumulative data arc: GDP 2.1% (pre-war), NFP −92K, Empire State −0.20, Michigan 53.3 (worst since 2022), CPI 2.4%, PPI 3.4%, Core PCE 3.1%. Growth collapsing while inflation persisting = textbook stagflation.

This week’s remaining calendar (verified): WEDNESDAY 8:15 AM — ADP Employment. 8:30 AM — Retail Sales (Feb, rescheduled from March 16 by Census Bureau). 10:00 AM — ISM Manufacturing PMI (March, consensus 52.3 — the MOST IMPORTANT data point of the week; Prices Paid component is the inflation flashpoint). THURSDAY — Jobless Claims. FRIDAY — GOOD FRIDAY MARKETS CLOSED. NFP released to closed markets at 8:30 AM (consensus +57K, prior −92K). This creates maximum gap risk for Monday April 7 — the market will have the entire weekend to digest the jobs number without being able to trade it. This is only the second time in 20+ years that NFP was released to closed US markets.

5. THE DYRH READ

Regime: Ceasefire Hopes Collide With Permanent Oil Premium — WSJ Hormuz Report Drives Relief Bounce #7. Q1 Rebalancing Adds Mechanical Support. The most powerful de-escalation catalyst since the war began meets the most contradictory oil signal: war ending = bullish equities, Hormuz closed = bullish oil. The market is pricing the first half. Oil is pricing the second. Confidence: Moderate.

Yield Curve: Bull Flattener Day 2 — Biggest 2-Day Yield Decline of the War.

All yields falling for a second consecutive session. 2Y −3.5 bps to 3.801%, 5Y −4.7 bps to 3.943% (below 4.00%), 10Y −3.9 bps to 4.311%, 30Y −2.4 bps to 4.885%. The cumulative 2-day decline: 2Y −11.3, 5Y −12.5, 10Y −11.7, 30Y −8.0 bps. The 30Y is now 11.5 bps below Friday’s 5.00% intraday high — the 5.00% threshold is being DECISIVELY abandoned. The 2Y at 3.801% has broken below 3.85%, pricing the Fed firmly on hold and moving toward eventual cuts. The 5Y below 3.95% is the belly driving the curve — the market has fully repriced from ‘hike possible’ to ‘hold indefinitely, cut eventually.’

MOVE at 108.33 (below 110) should decline further today given the continued bond rally. The combined impact of Powell removing the hike + WSJ ‘end the war’ has created a bond rally that is transitioning from ‘crisis de-escalation’ to ‘growth slowdown anticipation.’ The 30Y’s retreat from 5.00% to 4.885% in 2 sessions is the most aggressive bond rally of the conflict.

The WSJ Paradox — War Ending + Hormuz Closed = Structural Energy Crisis.

This is the report’s central analytical challenge. The WSJ headline creates a genuine new framework: Trump is willing to declare victory and exit. But the headline’s qualifier — Hormuz stays largely closed — means the war’s ECONOMIC damage persists indefinitely. Iran’s parliamentary approval of a toll plan institutionalizes what was previously a military blockade into a PERMANENT economic lever. The toll plan includes ‘financial arrangements and rial toll systems’ with explicit prohibition on American and Israeli vessels.

The implications cascade: (1) $100+ oil becomes structural, not cyclical — the market can no longer price ‘oil normalizes when the war ends’ because the war ending doesn’t reopen Hormuz; (2) the Fed cannot cut rates into a permanent energy shock — the inflation pass-through from $117 Brent continues regardless of ceasefire; (3) consumer spending remains under pressure from $4+/gallon gas indefinitely; (4) global supply chains built around Gulf transit remain disrupted; (5) IEA’s assessment of ‘worse than 1973 and 1979 combined’ may prove conservative if Hormuz is PERMANENTLY restricted rather than temporarily closed.

The equity market is choosing to price ‘end the war’ and ignore ‘Hormuz stays closed.’ This is rational in the very short term — removing the military tail risk (nuclear escalation, power plant destruction, broader regional war) IS worth a premium. But over any meaningful horizon, equities must reprice the permanent energy shock. The S&P cannot sustain current valuations with $117 Brent, 3.4% PPI, no rate cuts, and Michigan Sentiment at 53.3.

Gold Recovery — Forced Liquidation Definitively Over.

Gold at $4,611.6 (+1.19%) has risen for 4 consecutive sessions after the 5-day forced liquidation that took it from $5,311.6 to the $4,376 war low (−$935.6, −17.6%). The recovery: $4,376 → $4,611.6 (+$235.6, +5.39% in 3 sessions). Silver surging +3.74% — outperforming gold on a risk-on day, which means the metals complex is responding to BOTH safe-haven demand AND industrial/risk appetite. GVZ fell −6.15% yesterday while gold rose — gold volatility declining with gold rising is the definitive signal that the margin-call cascade is over. The Quiggle data confirms: Gold RLTV has recovered from 0.89 to 1.07. Copper +0.78% adds a constructive growth signal.

Equities: Relief Bounce #7 — Can This One Survive?

ES at 6,463.50 (+1.18%), RTY +1.55% (small caps leading = risk-on), NQ +1.15%. All 7 Mag 7 green in after-hours. All sectors green with cyclicals leading. IJR +1.64%, SPHB +1.10% = risk-on factor rotation. SOXX +1.86% (bouncing from −4.23% yesterday — the Nvidia $2B Marvell investment helping sentiment). MTUM +1.14% (recovering from −2.12%). The breadth picture is improving: S5FD recovered to 32.40 from 21.27 capitulation, R2FD to 31.38 from 21.25.

What makes bounce #7 potentially different: (1) Powell killed the rate hike — the worst-case monetary policy outcome is off the table; (2) the WSJ headline is genuinely new information about the war’s trajectory; (3) VIX below 30 with backwardation resolved and MOVE below 110 — the vol mechanics of panic are subsiding; (4) gold’s recovery confirms forced liquidation is over. What makes bounce #7 vulnerable: (1) all 6 prior bounces reversed within 1-2 sessions; (2) oil is surging, not falling — the stagflationary headwind persists; (3) Q1 rebalancing creates artificial support that fades in Q2; (4) Consumer Confidence at 10 AM could crater; (5) tomorrow’s ISM Manufacturing and Friday’s NFP are high-impact risk events.

Q1 Mechanical Flows — Artificial Support That Masks Fundamentals.

Today is the final trading day of Q1 2026. Three significant mechanical flows: (1) quarter-end rebalancing — pension funds and balanced portfolios that are underweight equities after the war drawdown must BUY to restore target allocations; (2) JPM’s massive options position expiration — the ‘collar’ trade has been creating artificial S&P price support through dealer hedging, and its expiry removes that support going forward; (3) window-dressing — fund managers buying winners and selling losers for quarter-end reporting. These flows create BUYING PRESSURE that has nothing to do with the war, oil, or economic fundamentals. If the rally is primarily mechanical, it will fade in early Q2 when these flows reverse. The S&P closed at 6,388.25 yesterday — today’s close determines the Q1 total return that will be reported on every 401(k) statement.

6. THE GAME PLAN

Today’s Key Events: Case-Shiller 9:00 AM. Chicago PMI 9:45 AM (first full month of war impact). CB Consumer Confidence + JOLTS 10:00 AM (sentiment crater test). Nike after close (consumer spending bellwether). Q1 ends — rebalancing flows + JPM options expiration. WEDNESDAY: ADP + Retail Sales (rescheduled from 3/16) + ISM Manufacturing (consensus 52.3 — the week’s most important data). FRIDAY: NFP to CLOSED markets — Good Friday gap risk.

The Bull Case:

The WSJ report is the most significant de-escalation signal of the war — Trump is willing to END the conflict. Powell killed the rate hike Monday. The 2-day yield decline is the biggest of the war. VIX below 30 with backwardation resolved. MOVE below 110. Gold recovering for 4 straight sessions — forced liquidation definitively over. Silver surging +3.74% (risk-on + safe-haven). All 7 Mag 7 green. All sectors green with cyclical leadership. Small caps leading (+1.55%). SOXX bouncing +1.86% from −4.23%. Breadth recovering from capitulation. The bond market is pricing recession/slowdown — if growth stabilizes, equity re-rating is significant. Netanyahu says war ‘beyond halfway point.’ The 30Y retreating from 5.00% to 4.885% removes the bond crisis tail risk. Nvidia $2B Marvell investment shows big tech still deploying capital despite the war.

The Bear Case:

Relief bounce #7 — six prior bounces ALL reversed within 1-2 sessions. Oil surging to 117 Brent DESPITE ‘war-ending’ headline — the Hormuz closure makes the energy crisis PERMANENT, not temporary. Iran institutionalizing the blockade with a toll plan. Iran struck a Kuwaiti tanker in Dubai waters — kinetic operations continue. Consumer Confidence expected to crater (UoM already 53.3). Q1 rebalancing creates artificial support that fades tomorrow. Yesterday’s session showed equities can’t hold: S&P −0.39%, Russell −1.45% DESPITE the biggest bond rally. XLE −0.96% vs WTI +3.25% = equity-oil decoupling. SOXX −4.23% yesterday (Micron −10%). Tomorrow’s ISM Manufacturing could confirm stagflation. Friday’s NFP to closed markets creates unprecedented gap risk. S&P at 6,463 is still −6.1% from pre-war. Quiggle data: tech ( XLK RLTV 0.97) is now a RELATIVE LOSER. Defense Secretary Hegseth’s broker reportedly sought defense investments pre-war (FT) — governance risk. Trump’s combative tone (’go take it’) toward allies creates diplomatic strain.

Regime: Ceasefire Hopes Collide With Permanent Oil Premium. The WSJ headline is the strongest de-escalation signal of the war, but Hormuz staying closed means the economic damage is permanent. The market is pricing ‘end the war’ while oil is pricing ‘Hormuz stays closed.’ One of them is wrong. The Q1 mechanical flows add support today that cannot be trusted as conviction. The session turns on: Does Consumer Confidence confirm or deny recession risk? Does Chicago PMI show war damage in manufacturing? And can the 7th relief bounce break the pattern of failure?

Watch List

CB Consumer Confidence at 10:00 AM — recession confirmation test

February was 91.2. UoM already cratered to 53.3. A CB reading below 85 would be the lowest since late 2024 and could overwhelm the WSJ optimism. The Conference Board survey measures both present conditions and expectations — the expectations component is the leading indicator. If consumers see the economy deteriorating DESPITE a potential ceasefire, the recession narrative hardens regardless of equity price action.

Chicago PMI at 9:45 AM — first full war month

February surged to 57.7. March covers the first complete month of war. A drop toward 50 signals the energy shock is reaching the industrial heartland. The Prices Paid subcomponent is the inflation flashpoint — if input costs are surging while output contracts, it’s textbook stagflation.

JOLTS at 10:00 AM — labor demand baseline

February openings data provides the pre-escalation labor market health. A significant decline from 7.74M would signal hiring was already cooling before March’s −92K NFP. Combined with Friday’s NFP (to closed markets), this builds the labor market picture the Fed is watching.

Nike after close — consumer spending reality check

NKE Q3 FY2026 (EPS est $0.29) is a bellwether for discretionary consumer spending. With $4/gallon gas and Michigan Sentiment at 53.3, Nike’s North America revenue, gross margins, and inventory guidance will reveal whether the consumer is stressed but spending, or pulling back. Weak guidance would reinforce the recessionary narrative.

Oil at $117 Brent — the war’s unresolved contradiction

The equity rally and the oil surge cannot coexist indefinitely. Either Hormuz reopens (oil crashes, equity rally justified) or it doesn’t (oil justified, equities must reprice). Watch whether oil pulls back from $117 intraday — if it HOLDS above $115 on a day when ‘end the war’ is the headline, the ‘permanent oil premium’ thesis is confirmed and the equity rally is on borrowed time.

Wednesday: ADP + Retail Sales + ISM Manufacturing

Tomorrow is the most data-dense session of the week. ADP (8:15 AM) previews Friday’s NFP. Retail Sales (8:30 AM, rescheduled from March 16) shows actual consumer spending behavior versus survey sentiment. ISM Manufacturing (10:00 AM, consensus 52.3) is the week’s single most important data point — the Prices Paid component at consensus 73.6 (from 70.5) would be the highest input cost reading since the 2022 energy crisis.

Morning check: the 7th relief bounce, the biggest headline, the deepest contradiction. Trump is willing to end the war — genuinely the most de-escalatory signal since February 28. But he’s NOT willing to reopen Hormuz. Oil at $117 is pricing that reality. Equities at +1.2% are ignoring it. The bond market — posting its biggest 2-day rally of the war — is pricing something else entirely: recession. Three different markets, three different stories. Consumer Confidence at 10 AM will tell us which one the consumer believes. And tomorrow’s ISM will tell us which one the factories are living. Q1 ends today. The mechanical flows support the bulls. But when the quarter turns, the flows reverse, the options expire, and the market stands on its own. Six relief bounces have all reversed. Is the seventh time the charm — or is it just another trap?

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.