☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: The post-panic consolidation lasted exactly one session. CPI came in-line (+0.3% MoM, +2.4% YoY, core +0.2% MoM) but is analytically irrelevant — it’s pre-war February data collected before the strikes began. The real story is underneath: S5FD collapsed to 16.50 (−39.85% in a single session) — the LOWEST breadth reading of the entire war series. Only 16.5% of S&P stocks are above their 5-day moving average while the INDEX was down just 0.21% yesterday. The market is being completely hollowed out — held up by a handful of mega-caps while 83.5% of S&P components are in freefall. Meanwhile, the war is re-escalating: the US sunk 16 Iranian minelayers near Hormuz, a Thai vessel and a commercial cargo ship were struck in the strait, and Iran vowed it won’t allow “ONE LITER OF OIL” to leave the Middle East until attacks cease. Oil is bouncing +5.26% to $87.84 WTI, $91.10 Brent. Yields surging to new series highs: 30Y at 4.830% (third consecutive new high). Gold selling again (−1.08%) — the two-day precious metals rally has been completely reversed, suggesting forced liquidation may be RETURNING. Dollar back above 99. All global indices red. TOPIX −2.00% worst. The bond market has IGNORED the benign CPI, continuing to price forward to March/April inflation data that will capture $80–120 oil. Oracle’s +8% after-hours beat on massive cloud numbers is providing NO pre-market follow-through. G7 decision on IEA’s 400M barrel SPR release proposal expected TODAY — the binary catalyst.

The Number That Matters: S5FD at 16.50. This breadth reading is more important than any single data release including CPI. Only 16.5% of S&P 500 stocks are above their 5-day moving average — yet the index itself was down just 0.21% yesterday. The S&P 500 is a fiction held up by 7–10 mega-cap names while the other 490 stocks are in a bear market. S5TW at 26.83 (only 26.8% above 20-day MA) is also a new series low. When the index is calm but breadth collapses, it creates extreme STRUCTURAL FRAGILITY — if the mega-cap pillars crack, there is no breadth support underneath and the market air-pockets lower. This is the most dangerous internal market structure of the entire series.

The Setup: The regime has shifted to Stealth Stagflation: the S&P looks calm while the real market beneath it is in its most distressed state of the war. Three forces are compounding simultaneously: (1) oil bouncing +5% on Hormuz re-escalation, driving yields to new highs and re-introducing the inflation impulse; (2) gold selling again while oil surges = the forced-liquidation signature from Days 2–7 may be RETURNING; (3) breadth at 16.50 means the index is structurally hollow. CPI was in-line but the bond market ignored it — the market is pricing forward to March/April CPI that will capture $80–120 oil. The G7 SPR decision today is the binary catalyst: a credible 400M barrel release caps oil at $75–80; delay or insufficient volume lets oil re-accelerate toward $100.

2. OVERNIGHT SESSION RECAP

Asia-Pacific

TOPIX −2.00% — Japan the worst global index, with energy import dependence devastating. Nikkei −1.08%. The brief Asian recovery from Monday has completely reversed. Oil bouncing +5% overnight is crushing import-dependent economies.

Europe

DAX −1.41%, Euro Stoxx 50 −1.06%. Monday’s +2.05% European bounce has been erased. The Hormuz re-escalation and Iran’s “not one liter” threat are hitting European equities directly given energy supply chain dependence. UK PM Starmer working with Germany and Italy on options to support commercial shipping through Hormuz.

US Pre-Market

Day 12 — War Re-Escalating. US forces sunk 16 Iranian minelayers near the Strait of Hormuz overnight. A Thai vessel (Mayuree Naree) was hit by an unknown projectile near Hormuz — 3 crew unaccounted for, 20 rescued. Another commercial cargo vessel struck while crossing the strait — fire onboard, crew evacuating. Trump on Truth Social threatened “death, fire and fury” if Iran blocks Hormuz shipping. Iran vowed it won’t allow “ONE LITER OF OIL” to leave the Middle East until attacks cease — the most aggressive Hormuz threat yet. Death toll: Iran 1,200+, Lebanon 570 (83 children), Israel 12, US 7 killed / 140 injured.

CPI (released today, March 11 at 8:30 AM): Headline +0.3% MoM, +2.4% YoY (in-line). Core +0.2% MoM, +2.5% YoY (in-line to slightly below expectations). Shelter +0.2% (moderating). Food +0.4%. Energy +0.6%. CRITICAL CONTEXT: this is pre-war February data, collected before February 28 strikes. The March CPI (released April 10) will capture the oil shock. Today’s print sets the BASELINE — inflation was contained at 2.4% before the war. But the bond market has ignored it, continuing to sell the long end to new series highs.

Oracle (ORCL) Q3 earnings (released yesterday after close): EPS $1.79 vs. $1.70 est. Revenue $17.19B vs. $16.91B. Cloud revenue +44%. RPO $553B (+325% YoY). FY27 guidance raised to $90B (vs. $86.6B consensus). Stock closed +8% after hours. But pre-market shows NO follow-through into broader indices — the war re-escalation is overwhelming the positive tech signal.

Prior session (March 10 close): S&P −0.21%, Dow −0.07%, Nasdaq +0.01% — flat consolidation. WTI crashed to $83.45 (−11.94%), Brent to $87.80 (−11.28%) on continued Trump de-escalation pricing. Gold +2.71% to $5,242.1, Silver +6.00%. 30Y yield at 4.794% (new series high then). VIX 24.93.

This week: TODAY — G7 decision on IEA’s 400M barrel SPR release; Japan plans independent stockpile release as early as Monday. Thursday — PPI (February) 8:30 AM; Jobless Claims; Adobe (ADBE) earnings after close. Friday — Michigan Consumer Sentiment (preliminary March, FIRST survey capturing war/oil shock); JOLTS (January, rescheduled to March 13).

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 03/10/26. Provided for informational purposes only; not as investment advice.

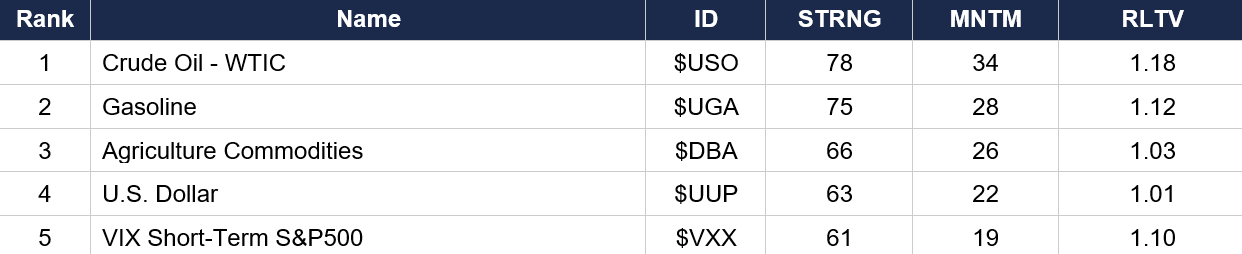

Asset Classes — Top 5

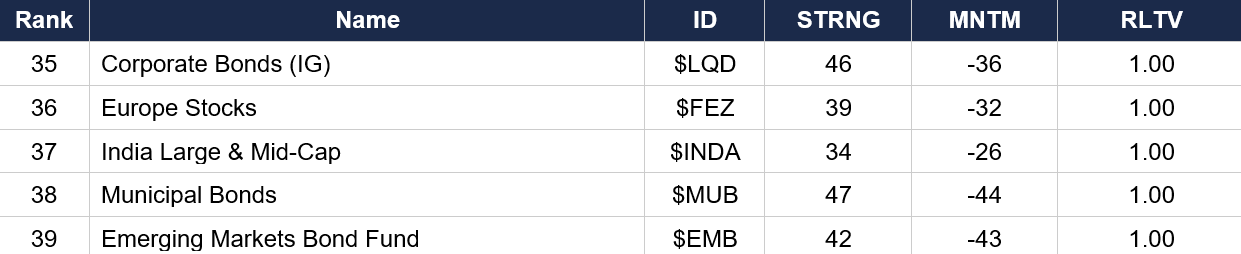

Asset Classes — Bottom 5

Regime signal: Crude oil holds rank 1 with MNTM 34 (up from 27 yesterday). Agriculture ($DBA) has risen to rank 3 with MNTM 26 (from 13) — the food-inflation impulse is intensifying sharply as Hormuz disruption hits fertilizer and grain shipping corridors. VIX ($VXX) at rank 5 with MNTM 19 (up from 1) — the volatility trade is BACK after one session of compression. Gold at rank 11 (MNTM −4) — deteriorating again after the brief bounce. Senior Corporate Loans ($BKLN) at rank 7 with MNTM 23 confirms floating-rate credit as a safe haven in the rising-rate environment. Silver at rank 9 (MNTM 3) slipping. Nasdaq ($QQQ rank 13, MNTM 3) and S&P ($SPY rank 16, MNTM −10) diverging — tech holding while the broad market deteriorates. EM Bond Fund ($EMB, MNTM −43) and Municipal Bonds ($MUB, MNTM −44) remain the worst momentum on the board — the bond complex outside of floating-rate is being devastated

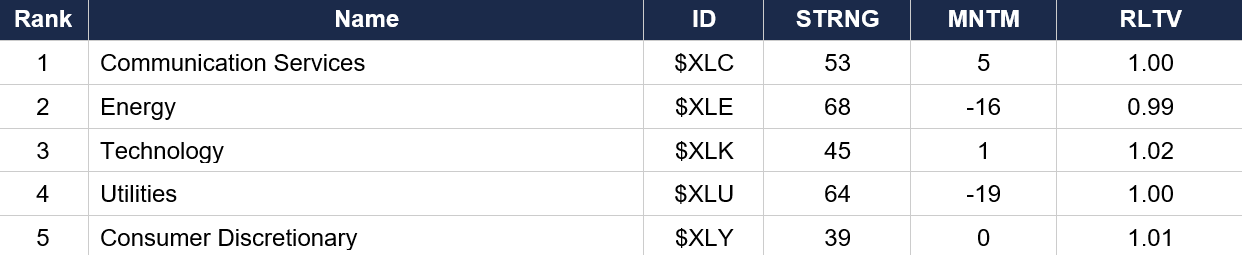

Sector ETFs — Top 5

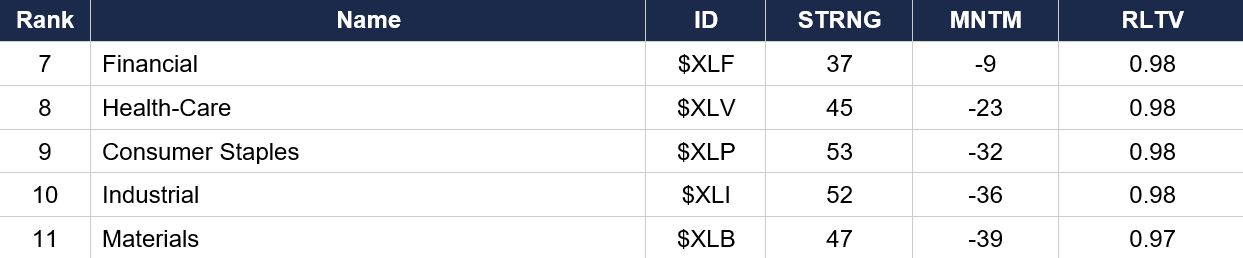

Sector ETFs — Bottom 5

Regime signal: Energy ($XLE) MNTM has deteriorated sharply to −16 from −4 yesterday — even though oil is bouncing +5%, energy equities are STILL losing momentum. The energy-equity divergence from crude prices is widening to extreme levels. Technology ($XLK) at rank 3 with MNTM 1 confirms tech as a relative haven. Consumer Discretionary ($XLY) MNTM at 0 — flat, the cyclical recovery stalled entirely. Materials ($XLB, MNTM −39) and Industrial ($XLI, MNTM −36) remain the worst sector momentum. Consumer Staples ($XLP, MNTM −32) being destroyed. The leadership is now Communication Services and Technology — the only sectors with positive or zero momentum.

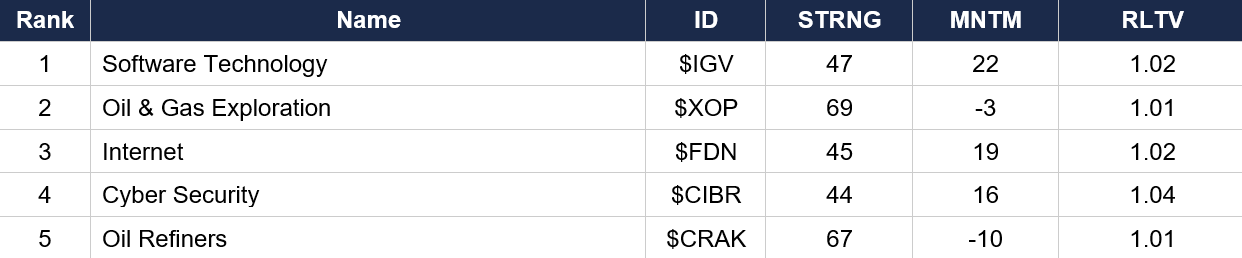

Industry ETFs — Top 5

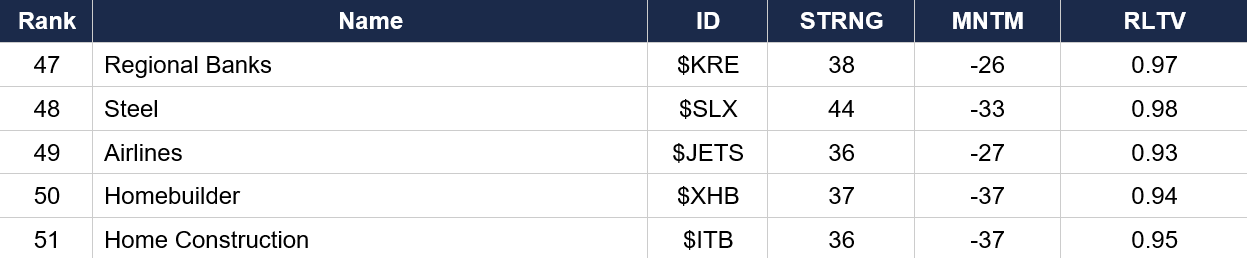

Industry ETFs — Bottom 5

Regime signal: Software ($IGV) has SEIZED rank 1 for the first time in the series (MNTM 22) — software is now the strongest industry in the entire market. Internet ($FDN, MNTM 19) and Cyber Security ($CIBR, MNTM 16) round out a tech/digital top 4. The technology complex has completely decoupled from the rest of the market. Oil & Gas Exploration ($XOP) at rank 2 but MNTM turned negative (−3) — even energy equities are losing momentum despite $88 oil. Aerospace-Defense ($ITA) has plummeted to rank 17 (MNTM −16) — defense selling for the THIRD consecutive session despite war escalation. Home Construction ($ITB, MNTM −37) and Homebuilders ($XHB, MNTM −37) remain the absolute worst industries.

4. MORNING DATA REACTION

February CPI (released today, March 11 at 8:30 AM): Headline +0.3% MoM, +2.4% YoY. Core +0.2% MoM, +2.5% YoY. Both in-line with consensus. Shelter +0.2% (moderating, largest factor). Food +0.4% (food at home +0.4%, food away from home +0.3%). Energy +0.6%. This is PRE-WAR data — February, collected before the February 28 strikes. It confirms inflation was contained at 2.4% before the war disrupted everything. The March CPI (released April 10) will capture the oil shock.

The bond market’s verdict: IGNORED. Despite CPI matching consensus, yields are surging to new series highs. 30Y at 4.830% (+4.3 bps), 10Y at 4.191% (+3.5 bps). ZB −0.75% — the most aggressive long bond selling since Day 8. The market is forward-looking at March/April CPI which will capture $80–120 oil. Pre-war CPI is analytically stale. The bear steepener is in its third consecutive session.

Oracle earnings (released Tuesday March 10 after close): Beat across the board. EPS $1.79 vs. $1.70 est. Revenue $17.19B (+23% YoY). Cloud +44%. RPO $553B (+325% YoY). FY27 guidance raised to $90B. Stock closed +8% after hours. But NO pre-market follow-through into the broader market — the Hormuz re-escalation is overwhelming the positive tech signal.

Prior week’s data recap: PPI (released Friday February 27): Final demand +0.5% MoM. ISM Manufacturing (released Monday March 2): 52.4, Prices Paid 70.5. ISM Services (released Wednesday March 4): 56.1. ADP (released Wednesday March 4): +63K. NFP (released Friday March 6): −92K. The data arc showed a bifurcated economy — strong services, weak manufacturing, collapsing payrolls — and now today’s CPI confirms inflation was contained before the war. The question going forward: how fast does $80–120 oil feed through into CPI?

5. THE DYRH READ

Regime: Stealth Stagflation — Index Calm Masks Breadth Catastrophe. The S&P looks calm (−0.28% pre-market) while the real market beneath is in its most distressed state of the entire war series. Confidence: Moderate on characterization.

Yield Curve: Bear Steepener — Third Consecutive Session, New Series Highs. 30Y at 4.830% — the THIRD consecutive new series high. 10Y at 4.191% — new cumulative high (+24.2 bps from pre-war). ZB −0.75% is the most aggressive long bond selling since Day 8. The CPI was in-line but the bond market IGNORED it because this is pre-war data. The market is pricing forward: March/April CPI will capture the oil shock. The bear steepener is the dominant curve regime — long end leading higher on structural inflation expectations while the front end rises slower on growth-scare rate-cut hopes. This configuration gives equities NO relief: inflation won’t resolve quickly AND the Fed can’t cut aggressively.

Breadth Catastrophe — THE Defining Signal. S5FD collapsed from 27.43 to 16.50 (−39.85% in one session) while the S&P was down just 0.21%. Only 16.5% of S&P stocks are above their 5-day MA — the LOWEST reading of the entire war series. S5TW at 26.83 (only 26.8% above 20-day MA) is also a new series low. The market is being held up entirely by mega-cap tech while 83.5% of components are in freefall. If the mega-cap pillars crack, there is no breadth support underneath — the market air-pockets lower. This is the most dangerous internal structure of the series.

Commodity Complex — Oil Bouncing, Gold Selling Again. WTI +5.26% to $87.84, Brent +3.85% to $91.10 — oil bouncing on Hormuz vessel attacks and Iran’s “not one liter” threat. The $30 crash from $120 has partially reversed. Gold −1.08% to $5,185.4 — the two-day rally (Days 9–10) has been completely erased. Silver −4.31%. The precious metals crashing while oil surges and war escalates = the forced-liquidation/margin-call signature from Days 2–7 may be RETURNING. If gold closes red today, the “liquidation is over” call was premature. Grains surging: soybean oil +3.93%, wheat +1.99%, corn +1.55% — agricultural inflation resuming as Hormuz disruption hits fertilizer corridors.

Equities: Index Calm, Internal Damage Severe. ES −0.28%, NQ −0.21% pre-market. All global indices red. TOPIX −2.00% worst. DAX −1.41%. The Oracle +8% beat is providing NO follow-through. Mag 7 pre-market: mostly flat/slightly red (TSLA +0.15% green, GOOG −0.30% worst). XLE barely red (−0.07%) despite oil +5% — the energy equity divergence from crude is widening further. ITA −0.72% — defense selling for the THIRD consecutive session despite war escalation (de-escalation pricing baked in even as the war re-escalates). IJR −0.89% in pre-market — small caps being punished. ICLN +0.44% — clean energy one of the few green thematics.

FX: Dollar Back Above 99, Safe Havens Failing Again. DX at 99.065 (+0.16%). CHF −0.20%, JPY −0.48% — traditional safe havens selling again after briefly working on Monday/Tuesday. The “normal” safe-haven period lasted two sessions. BTC −1.06%. AUD +0.16% the only green G10 currency. The dollar is the only functioning safe haven again.

Volatility: VIX Rising, Sub-25 Window Closed. VIX at 25.48 (+2.21%) — rising back toward 26 after the sub-25 window lasted exactly one session (Tuesday). VVIX 125.36. MOVE 76.33. The vol crush from Monday’s de-escalation narrative has been partially reversed as the war re-escalates. COR1M at 28.97 (still elevated, rising) — macro driving everything. SKEW at 154.46 (−2.23%) declining slightly — tail-risk hedging demand easing marginally as the regime shifts from “panic” to “structural stress.”

6. THE GAME PLAN

Today’s Key Events: CPI (February) released at 8:30 AM — in-line (+0.3% MoM, 2.4% YoY, core +0.2%). G7 decision on IEA’s 400M barrel SPR release expected TODAY — the binary catalyst. Japan plans independent stockpile release as early as Monday. War headlines continuous (Hormuz mine-clearing, vessel attacks). Thursday: PPI 8:30 AM; Jobless Claims; Adobe (ADBE) earnings after close. Friday: Michigan Consumer Sentiment (first survey capturing war/oil shock); JOLTS (January).

The Bull Case: CPI in-line at 2.4% confirms inflation was contained BEFORE the war — the “Fed has room” narrative is alive if the war resolves. Oracle’s +8% beat on massive cloud/AI numbers reinforces tech-as-shelter. S5FD at 16.50 is historically extreme oversold — readings below 20% have preceded violent mechanical rebounds. G7 is expected to announce a 400M barrel SPR release today, which would cap oil at $75–80 and collapse the war premium. Japan independently releasing stockpiles. If G7 delivers and Hormuz mine-clearing succeeds, oil plunges and the entire risk-off trade reverses. Monday’s intraday reversal proved the market CAN rally violently on any de-escalation signal.

The Bear Case: S5FD at 16.50 means 83.5% of S&P stocks are below their 5-day MA while the index is barely down — the most extreme hollowing in the series. Gold selling again (−1.08%) while oil surges (+5%) = forced liquidation may be returning. 30Y at 4.830% for the third consecutive new high — the bond market is pricing structural inflation regardless of today’s benign CPI. Vessels being struck in Hormuz. Iran vowing “not one liter of oil.” The de-escalation narrative from Monday is FAILING as Hegseth’s “most intense strikes” materialized. Oil is bouncing +5% on a day the G7 is expected to announce SPR release — the market is SKEPTICAL the release will be sufficient. The “post-panic consolidation” lasted one session. Breadth hasn’t confirmed any recovery. If mega-cap cracks, the air pocket below is massive.

Regime: Stealth Stagflation — Index Calm Masks Breadth Catastrophe. The S&P looks calm (−0.28%) but underneath, breadth is at its worst of the war (S5FD 16.50), yields are at new highs (30Y 4.830%), oil is bouncing on Hormuz re-escalation, and gold is selling again. CPI was in-line but irrelevant — pre-war data. The G7 SPR decision today is the binary catalyst: a credible 400M barrel release changes everything; delay or insufficient volume lets the stealth stagflation deepen.

Watch List

G7 SPR decision — TODAY — IEA proposed 400M barrels. Japan plans independent release. A credible, large announcement caps oil at $75–80 and triggers relief. Delay or small release = oil re-accelerates toward $100. This is the single most important policy catalyst of the week.

S5FD breadth below 20 — At 16.50, this is extreme oversold territory. Historically precedes either violent mechanical rebounds OR accelerated capitulation. Direction depends entirely on whether the G7 delivers and the war stabilizes. If breadth doesn’t recover above 20 today, the structural damage deepens.

Gold — forced liquidation test — Gold −1.08% after two days of gains. If gold closes red today while oil surges, the forced-liquidation cycle from Days 2–7 is RETURNING. A gold close above $5,200 would suggest the selloff is a one-day reversal, not a regime shift back to liquidation.

Key Earnings — Adobe (ADBE) Thursday after close — software demand durability; will Oracle’s cloud strength translate across the sector? Dollar General (DG) Thursday before open — low-income consumer barometer as gas prices surge past $3.41/gallon. These reports test whether corporate earnings can withstand the oil shock.

Michigan Sentiment Friday — The FIRST consumer survey capturing the war/oil shock. If sentiment craters, recession fears intensify dramatically and the −92K NFP narrative compounds. A resilient reading would suggest the consumer isn’t as damaged as feared.

Morning check: the surface is calm but the foundation is cracking. CPI was in-line but irrelevant — pre-war data that the bond market is ignoring. S5FD at 16.50 is the most extreme breadth reading of the entire series. Gold is selling again while oil bounces. Yields are at new highs. The post-panic consolidation lasted one session. The G7 SPR decision today is the binary catalyst that determines whether the market stabilizes or the stealth stagflation deepens. Beneath the calm index, the real market is in its most distressed state of the war.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.