☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: THE PATTERN BREAKS — DE-ESCALATION RALLY SURVIVES Q2 OPEN WITHOUT MECHANICAL SUPPORT. WTI DROPS BELOW $100. BREADTH EXPLODES 21→75 IN 3 SESSIONS. VIX BELOW 25. MOST DATA-DENSE SESSION OF THE WAR AHEAD.

The de-escalation breakout from Day 24 is extending into Q2 — and this is the critical development. Q1 rebalancing flows are GONE, and yet futures remain green (ES +0.62%, NQ +0.89%, RTY +0.69%, DAX +2.70%, Nikkei +2.01%). European indices are LEADING at nearly +2.7%, suggesting Europe is pricing disproportionate benefit from any energy supply normalization given its import dependence. WTI has dropped back below $100 to $99.57 (−1.79%) — the first time below that psychologically critical threshold since Day 23. DXY has fallen further below 100 to 99.315 (−0.38%). Gold is surging to $4,768 (+1.91%), now +$392 above the war low — but diverging upward from other metals, suggesting it’s trading on ‘inflation legacy’ demand rather than risk-on. VIX indicative at 24.57 has crossed BELOW the 25 crisis threshold. MOVE at 96.05 is below 100 for the 4th attempt. S5FD has exploded from 21.27 to 75.34 in just 3 sessions — one of the most aggressive breadth recoveries in recent market history. COR1M collapsed from 41.68 (war high) to 28.11 — crisis correlation is definitively broken.

This is the first genuine multi-session sustained rally of the entire war. Six prior relief bounces all reversed within 1-2 sessions. This one has now extended through 3 sessions AND survived the removal of mechanical support. The market microstructure has undergone a structural regime shift: VIX below 25, MOVE below 100, correlation below 30, breadth above 75, all G10 gaining vs USD. These are ALIGNED de-escalation signals across every asset class simultaneously.

The overnight headlines remain contradictory: China and Pakistan issued a joint 5-point peace initiative calling for ‘immediate ceasefire.’ Trump said the war could be ‘done’ in ‘2 or 3 weeks.’ Israel is speeding up targeting over the next 48 hours specifically ‘in case a ceasefire is declared’ — suggesting the military is preparing for an imminent end. But simultaneously, Iran fired THREE WAVES of missiles at Israel within one hour on Passover. Israel killed IRGC Navy commander Alireza Tangsiri in an overnight strike. A missile from Iran hit an oil tanker off Qatar. The fighting is INTENSIFYING even as diplomatic signals point toward an exit — both sides maximizing damage before any ceasefire locks in the status quo. Nike beat Q3 estimates (EPS $0.35 vs $0.29 est, revenue $11.28B vs $11.24B) but shares fell approximately 8.7% in European trading on weak Q4 guidance — the war’s consumer impact is showing in forward-looking corporate commentary.

The Number That Matters: WTI at $99.57 — back below $100.

WTI crossed above $100 on Day 23 and has now dropped back below in just 2 sessions. This tests Morgan Stanley’s ‘qualitatively different economic damage’ threshold from above. If WTI sustains below $100, the worst-case stagflation scenario de-escalates. If it rebounds above $100, the structural damage continues. Critical caveat from Sparta: ‘A ceasefire does not equal supply restoration. Physical relief is weeks-to-months away.’ Even a ceasefire doesn’t immediately clear Hormuz mines or restore shipping routes.

The Setup: De-Escalation Extends Into Q2 — Multi-Session Rally Confirmed. ADP and Retail Sales Both Beat.

ADP came in at +62K (beat 40K forecast) and Retail Sales at +0.6% (beat −0.2% prior) — the economy entered the war on firmer footing than feared. The de-escalation rally now has BOTH geopolitical AND economic support. The remaining test is ISM Manufacturing at 10:00 AM (consensus 52.3, Prices Paid consensus 73.8) — the first full-month war reading on factory activity and input costs. Yesterday’s session was the best since May: S&P +2.91%, Nasdaq +3.83%, 441/500 stocks gained, VIX −17.51% to 25.25, MOVE −11.33% to 96.05.

2. OVERNIGHT SESSION RECAP

Asia-Pacific

Nikkei +2.01%, TOPIX +0.24%. Japan surging on the ceasefire trajectory — as the most energy-import-dependent major economy, Japan benefits disproportionately from any path toward Hormuz normalization. The Nikkei’s 2-day surge reflects aggressive repricing of the war premium in Japanese equities.

Europe

DAX +2.70%, Euro Stoxx +2.77% — LEADING all global indices. European markets are pricing the ceasefire narrative most aggressively because Europe faces the most severe structural energy damage from the war (Ras Laffan 17% LNG lost, Nord Stream legacy, ECB hawkish hold). Any path toward energy supply normalization generates disproportionate European relief. The DAX at 23,453 has recovered its ENTIRE week’s losses and is now above its Day 22 level. Nike fell approximately 8.7% in Frankfurt despite the Q3 earnings beat — weak Q4 guidance citing ‘dynamic operating environment’ and war-related consumer headwinds drove the selling.

US Pre-Market

Day 33 of Operation Epic Fury. Q2 Day 1. The session is defined by the tension between the extending de-escalation rally and the most data-dense morning of the war.

DE-ESCALATORY CATALYSTS: China and Pakistan issued a joint 5-point peace initiative after hours of engagement — calling for immediate ceasefire, peace talks ‘as soon as possible,’ a lasting UN-backed peace, securing shipping lanes, and ending attacks on civilians. This is Beijing’s most thorough conflict resolution framework to date. Trump said the war could be ‘done’ in 2-3 weeks. Israel speeding up targeting in the next 48 hours ‘in case a ceasefire is declared’ — the military is preparing for an imminent end. Nvidia’s $2B Marvell investment continuing to support semiconductor sentiment. Warren Buffett on CNBC said he’d buy Apple at lower prices.

ESCALATORY CATALYSTS: Iran’s Revolutionary Guards fired THREE WAVES of missiles at Israel within one hour on Passover — the most significant Jewish holiday season. An 11-year-old girl was injured. Israel killed IRGC Navy commander Alireza Tangsiri — a significant military decapitation. Iran’s FM Araghchi said he has ‘no faith’ in talks. A missile from Iran hit an oil tanker off Qatar’s coast. US/Israeli strikes continued in Isfahan and Tehran. The fighting is INTENSIFYING even as diplomatic signals suggest winding down — consistent with ‘fighting to negotiate from strength.’

PRIOR SESSION (Day 24 Close): S&P +2.91% (best since May). Nasdaq +3.83%. VIX −17.51% to 25.25. MOVE −11.33% to 96.05 (below 100). COR1M collapsed from 41.68 to 28.11. S5FD exploded to 75.34 (from 32.40). 441/500 S&P stocks gained. DXY broke below 100 to 99.640. Iran President Pezeshkian reported open to ending war. WSJ Hormuz report continued to drive sentiment. Oil fell. All sectors green except XLE (−2.50%). HIGH confidence.

NIKE Q3 FY2026 (reported after yesterday’s close): Revenue $11.28B (beat $11.24B est), EPS $0.35 (beat $0.29 est). But shares fell ~8.7% in European trading. Revenue flat YoY, down 3% currency-neutral. Gross margin down 130 bps to 40.2%. Net income down 35% to $520M. Nike Direct down 7%. The beat was overshadowed by weak Q4 guidance — CFO Friend noted the ‘dynamic operating environment’ and indicated turnaround efforts would ‘continue to impact results over the balance of the calendar year.’ The war’s consumer spending headwind is now showing up in forward corporate guidance.

This week’s calendar (verified): TODAY 8:15 AM — ADP Employment (March, prior 63K). 8:30 AM — Retail Sales (Feb, rescheduled from March 16 by Census Bureau; prior −0.2%). 10:00 AM — ISM Manufacturing PMI (March, consensus 52.3, prior 52.4; Prices Paid consensus 73.8, prior 70.5). 10:00 AM — Construction Spending (Feb). Fed Vice Chair Barr speaks 8:10 AM. THURSDAY — Jobless Claims, Trade Balance, Factory Orders. FRIDAY — GOOD FRIDAY MARKETS CLOSED. NFP released 8:30 AM (consensus +57K, prior −92K) + ISM Non-Manufacturing to closed markets. Maximum Monday 4/7 gap risk. APRIL 6 — Trump’s energy strike pause deadline.

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 03/31/26. Provided for informational purposes only; not as investment advice.

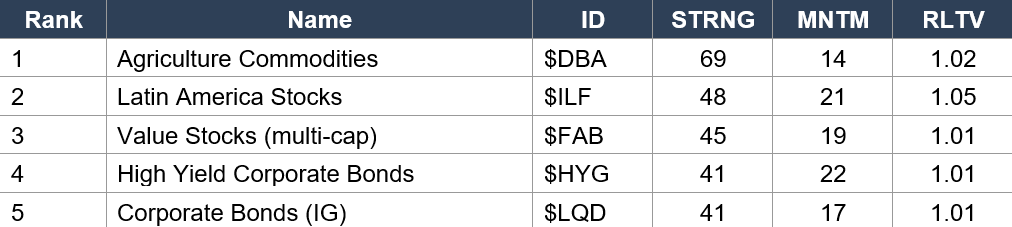

Asset Classes — Top 5

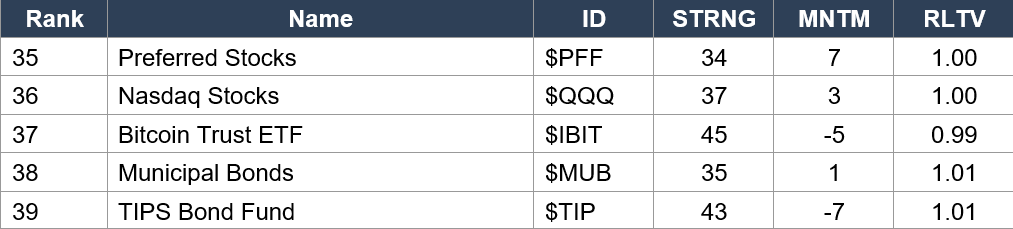

Asset Classes — Bottom 5

Regime signal: The Quiggle rankings have undergone the most dramatic reshuffling of the entire war — reflecting the de-escalation breakout. Agriculture ($DBA rank 1, STRNG 69, MNTM 14) has taken the top position as food inflation persists even as the war de-escalates. Latin America ($ILF rank 2, MNTM 21) is the highest-momentum asset class — commodity-producing EM is the clear winner of the de-escalation trade. Value stocks ($FAB rank 3, MNTM 19) and High Yield ($HYG rank 4, MNTM 22) confirm the risk-on rotation into cyclical and credit-sensitive assets. The CRITICAL shifts: Dollar ($UUP) has PLUNGED from rank 1 to rank 26 (MNTM −14) — the safe-haven trade is unwinding. VIX ($VXX) dropped from rank 2 to rank 19 (MNTM −10) — volatility is no longer the dominant asset. S&P ($SPY rank 30, MNTM 9) and Nasdaq ($QQQ rank 36, MNTM 3) have improved significantly but remain in the bottom half. Gold ($GLD rank 34, MNTM 2, RLTV 1.07) is mid-table with modest positive momentum — the RLTV at 1.07 shows gold OUTPERFORMING the market despite the selloff, reflecting its inflation-hedge role. Crude Oil ($USO rank 7, STRNG 70, MNTM −14, RLTV 1.12) still has the highest RLTV of any asset at 1.12 but momentum has turned deeply negative — the oil de-escalation trade is registering. NOTE: Today’s pre-market moves are NOT yet reflected.

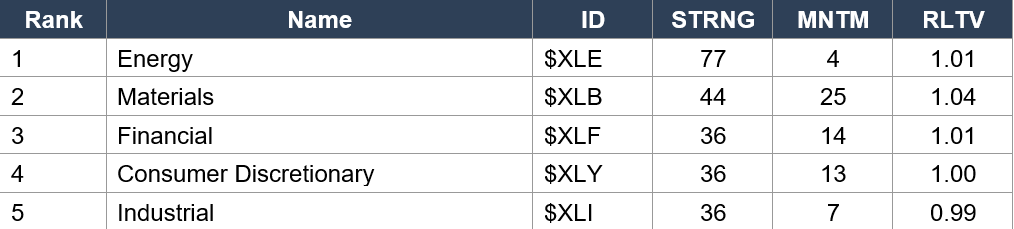

Sector ETFs — Top 5

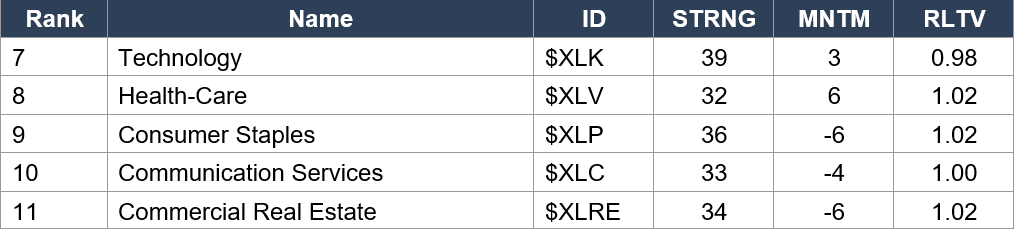

Sector ETFs — Bottom 5

Regime signal: Energy ($XLE rank 1, STRNG 77, MNTM 4) remains dominant on strength but momentum has decelerated sharply from prior sessions — XLE fell 2.50% in after-hours yesterday as oil dropped below $100. Materials ($XLB rank 2, MNTM 25) now has the HIGHEST MOMENTUM of any sector — a dramatic shift reflecting the commodity-inflation trade broadening beyond energy. Financial ($XLF rank 3, MNTM 14) and Consumer Discretionary ($XLY rank 4, MNTM 13) confirm the cyclical rotation. Industrial ($XLI rank 5, MNTM 7) entering the top 5 for the first time. Technology ($XLK rank 7, MNTM 3, RLTV 0.98) remains the only sector with sub-1.00 RLTV — tech continues to underperform the broad market in the war environment. The sector picture tells a clear story: the de-escalation rally is being LED by cyclicals and value (Materials, Financials, Industrials) rather than growth (Tech, Communications). This is a healthy rotation pattern.

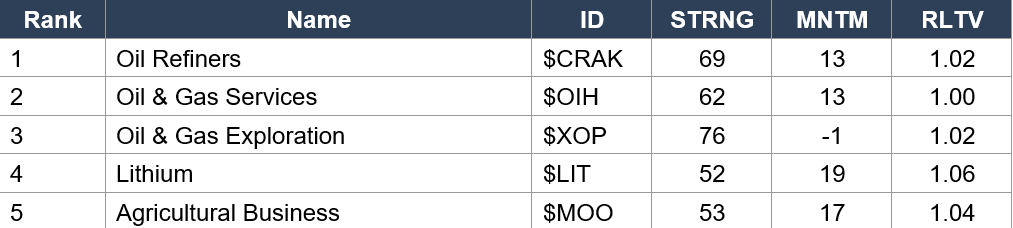

Industry ETFs — Top 5

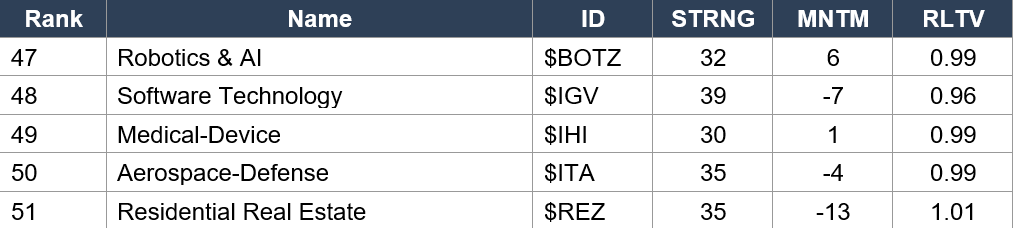

Industry ETFs — Bottom 5

Regime signal: Oil Refiners ($CRAK rank 1, MNTM 13) have overtaken Exploration ($XOP rank 3, MNTM −1) at the top — refiners benefit from both high oil prices AND the crack spread, making them more resilient as crude declines. Lithium ($LIT rank 4, MNTM 19, RLTV 1.06) continues its strong positioning with the highest RLTV of any top-5 industry — battery materials are a structural growth story independent of the war. Gold Miners ($GDX rank 22, MNTM 14, RLTV 1.11) have surged with the highest RLTV of any industry at 1.11 — gold’s recovery from the war low is powering the miners. Regional Banks ($KRE rank 9, MNTM 23), Banking ($KBE rank 10, MNTM 23), and Steel ($SLX rank 8, MNTM 23) share the highest momentum at 23 — the cyclical/value rotation is broad-based. Software Technology ($IGV rank 48, MNTM −7, RLTV 0.96) has the worst RLTV of any industry — growth/tech remains the war’s biggest relative loser. Aerospace-Defense ($ITA rank 50, MNTM −4) still near the bottom despite an active war.

4. MORNING DATA REACTION

ADP Employment: +62,000 (March) — BEAT. Forecast 40K. Prior revised up to 66K from 63K.

Private payrolls added 62,000 jobs in March, solidly beating the 40K consensus and extending the upwardly revised 66,000 in February. The result holds signs of resilience in the labor market despite economic uncertainty and the pullback in labor force growth. Education and health services led with 58,000 jobs. Construction added 30,000. Information added 16,000. Natural resources and mining added 11,000. Pay growth for job-stayers held at 4.5% YoY. The ADP data contradicts the recession narrative: hiring is not collapsing under the war’s weight, at least through mid-March. However, breadth remains a concern — job growth is concentrated in a few sectors rather than broad-based. This is a constructive but not emphatic labor market signal ahead of Friday’s NFP (consensus +57K, prior −92K) to closed markets.

Retail Sales: +0.6% MoM (February) — BEAT. Prior −0.2%. Ex-autos and gas +0.4% (best since August).

US retail sales rebounded sharply in February, rising 0.6% after January’s −0.2% decline — a broad-based advance helped by resurgent auto sales. Excluding motor vehicles and gas, sales rose 0.4%, the strongest reading since August. This data was rescheduled from March 16 and covers the war’s first few days but predates the worst of the consumer confidence collapse (Michigan 53.3 didn’t come until late March). The strength contradicts Nike’s weak Q4 guidance and the survey-based sentiment data — consumers are SPENDING even as they report feeling terrible. This is the classic ‘say one thing, do another’ divergence between soft data (surveys) and hard data (actual spending). The control group strength is a positive GDP input.

Both releases BEAT — the economy entered the war on firmer footing than feared.

ADP +62K and Retail Sales +0.6% together suggest the pre-war economy had more resilience than the recession narrative implied. This supports the de-escalation rally: if the economy was stronger going INTO the war, it has more capacity to absorb the shock and recover as the war winds down. The remaining question is ISM Manufacturing at 10:00 AM — this is the first release that covers a FULL MONTH of war. The Prices Paid component (consensus 73.8, prior 70.5) is the inflation flashpoint. If Prices Paid spikes above 73 while the headline holds above 50, the reading confirms ‘resilient activity with intensifying inflation pressure’ — the stagflation-lite scenario rather than outright contraction.

Still ahead: 10:00 AM — ISM Manufacturing PMI (March, consensus 52.3, Prices Paid consensus 73.8). Construction Spending (Feb). This week remaining (verified): THURSDAY — Jobless Claims, Trade Balance, Factory Orders. FRIDAY — GOOD FRIDAY MARKETS CLOSED. NFP at 8:30 AM (consensus +57K) + ISM Non-Manufacturing to CLOSED markets. Maximum gap risk Monday April 7. APRIL 6 — Trump’s energy strike pause deadline.

5. THE DYRH READ

Regime: De-Escalation Extends Into Q2 — Multi-Session Rally Confirmed. Oil Below $100. Breadth Explodes. Vol Normalizing. ADP +62K and Retail Sales +0.6% both beat — the economy entered the war stronger than feared. The first sustained rally of the war has survived without mechanical support. VIX below 25, MOVE below 100, correlation below 30, breadth at 75. ISM Manufacturing at 10 AM remains the inflation test. Confidence: High.

Yield Curve: Bull Flattener Pausing — Consolidation After Biggest 3-Day Move of the War.

Yields are essentially flat today after a 3-day decline of 10-12.5 bps across the curve. 2Y 3.789% (−0.2 bps), 5Y 3.941% (flat), 10Y 4.313% (−0.6 bps), 30Y 4.905% (−0.5 bps). The aggressive repricing from Powell’s rate hike removal and the WSJ report has been absorbed. The 30Y at 4.905% is now 11.5 bps below its 5.00% intraday high — the 5.00% threshold is being decisively abandoned. The curve is consolidating at new equilibrium levels, which is NORMAL after a move of this magnitude. MOVE at 96.05 below 100 should decline further if the de-escalation continues. The bull flattener regime from Days 23-24 may be exhausting itself as the bond market shifts from ‘crisis de-escalation’ to ‘growth slowdown anticipation.’

WTI Below $100 — The Stagflation Threshold Test.

WTI at $99.57 has dropped back below $100 for the first time since Day 23. Brent continuous at $101.90 (−1.99%). RBOB gasoline −2.27%. The de-escalation trade is now COHERENT for a second session: oil down + equities up + dollar down. This is the alignment the market has been seeking since the war began.

However, the Sparta analyst’s caveat is critical: ‘A ceasefire does not equal supply restoration. Physical relief is weeks-to-months away, even in a best case.’ Hormuz mines need to be cleared. Shipping routes need to be re-established. Iraq’s force majeure needs to be lifted. Qatar’s Ras Laffan damage is 3-5 years from repair. Even in the best diplomatic scenario, oil prices could remain elevated for an extended period. WTI below $100 may reflect ceasefire PRICING rather than supply REALITY.

Gold at $4,768 — The Inflation Legacy Trade.

Gold is surging +1.91% to $4,768 — now +$392 above the $4,376 war low (+8.96% recovery in 5 sessions). GVZ at 38.89 (−8.94% yesterday) means gold volatility is COLLAPSING while gold prices surge — the definitive sign that forced liquidation is over and the recovery is durable. But the OTHER metals are mixed/flat today (silver +0.38%, copper −0.14%, palladium −0.30%), breaking the 5-session ‘all 5 green’ streak. Gold diverging upward from silver/copper suggests gold is trading on INFLATION-HEDGE demand rather than risk-on industrial demand. The war may end, but the inflation it created doesn’t disappear overnight. Gold at $4,768 is pricing ‘the damage is done’ regardless of ceasefire timing.

Equities: The Pattern Break — First Multi-Session Sustained Rally.

ES at 6,611.75 (+0.62%) continues the rally with REDUCED momentum versus yesterday’s +2.91% — this is healthy. European indices leading at +2.7% suggests the rotation is broadening geographically. All 7 Mag 7 green in after-hours (TSLA +2.03% leading, AAPL +0.28% lagging). Sector rotation shows cyclicals leading (XLI +0.95%, XLY +0.97%, XLK +1.17%) while XLE is being CRUSHED (−2.50%) as oil drops below $100 — this is the de-escalation trade in its purest form: the equity rally is NOT driven by energy.

The breadth recovery is the session’s most constructive signal. S5FD’s move from 21.27 to 75.34 in 3 sessions means 75% of S&P stocks are now above their 5-day MA, compared to only 21% three days ago. The 200-day breadth (S5TH 47.31, R2TH 47.93) finally turned positive after declining for weeks — the first sign that medium-term structural damage may be stabilizing. COR1M at 28.11 (from 41.68 war high) means crisis correlation is broken and individual stock selection matters again.

The Analytical Paradox — Fighting Intensifies as Markets Rally.

The military tempo is INCREASING even as diplomatic signals point toward an exit. Iran fired 3 missile waves at Israel on Passover. Israel killed IRGC Navy commander Tangsiri. An oil tanker was hit off Qatar. This is consistent with ‘fighting to negotiate from strength’ — both sides want to maximize damage before any ceasefire locks in the status quo. The market is pricing the DIPLOMATIC trajectory (equities up, oil down) rather than the MILITARY trajectory (missiles flying, tankers burning). This divergence resolves when either a ceasefire materializes or an escalation overrides the diplomatic signals. Netanyahu’s framing — ‘beyond the halfway point in terms of missions, not necessarily time’ — supports the ceasefire timeline.

6. THE GAME PLAN

Today’s Key Events: ADP 8:15 AM (labor market test). Retail Sales 8:30 AM (consumer spending reality). ISM Manufacturing 10:00 AM (activity + inflation — Prices Paid 73.8 consensus is the flashpoint). Construction Spending 10:00 AM. Fed Vice Chair Barr 8:10 AM. Thursday: Claims, Trade Balance, Factory Orders. Friday: NFP + ISM Non-Mfg to CLOSED markets. April 6: Energy strike deadline.

The Bull Case:

The de-escalation rally has survived Q2’s open without mechanical support — the critical pattern break. ADP +62K and Retail Sales +0.6% both BEAT — the economy is stronger than the recession narrative suggested. Oil below $100. VIX below 25. MOVE below 100. Correlation below 30. Breadth at 75.34 from 21.27 in 3 sessions. 200-day breadth finally improving. All G10 gaining vs USD. China-Pakistan 5-point peace initiative. Trump: ‘2-3 weeks.’ Israel preparing for ceasefire. Powell killed the hike. The 3-day yield decline is the biggest of the war. Gold recovering +$392 from war low — forced liquidation definitively over. Silver surging. XLE −2.50% while everything else green = the war trade is unwinding. Nike beat estimates. Nvidia $2B Marvell investment. Buffett would buy Apple lower. The S&P +2.91% yesterday with 441/500 gainers is the broadest risk-on session of the conflict. The market microstructure has structurally improved across every metric.

The Bear Case:

Iran fired 3 missile waves at Israel on PASSOVER — fighting is intensifying, not ending. Oil tanker hit off Qatar. IRGC commander killed = potential retaliation escalation. ‘Ceasefire does not equal supply restoration’ — oil relief is weeks-to-months away even in best case. MOVE has snapped back above 100 after EVERY prior break below — 4th attempt. Nike shares fell 8.7% despite beating estimates — weak guidance shows war damage in consumer spending. Today’s data could reveal economic damage: if ADP misses AND ISM prints below 50 AND Retail Sales is negative, the recession case hardens regardless of ceasefire timeline. ISM Prices Paid at 73.8 would be the highest since 2022 — stagflation confirmed. NFP Friday to closed markets creates unprecedented gap risk. April 6 energy strike deadline still approaching. Iran’s 5-point counterproposal demands sovereignty over Hormuz — far apart from US position. Grains going red is a potential deflationary signal that demand is weakening. ES +0.62% today vs +2.91% yesterday = momentum decelerating.

Regime: De-Escalation Extends Into Q2 — Multi-Session Rally With Economic Support. The pattern has broken. The microstructure has shifted. The rally has survived without mechanical support. ADP +62K and Retail Sales +0.6% provide the economic foundation the rally was missing — the economy entered the war stronger than feared. ISM Manufacturing at 10 AM is the remaining test. If ISM holds above 50 but Prices Paid spikes above 73, the reading confirms ‘resilient activity with intensifying inflation’ — stagflation-lite rather than contraction. The de-escalation rally now has geopolitical catalysts AND hard economic data behind it. The question shifts from ‘can the rally survive?’ to ‘how much war damage is already embedded in forward earnings and guidance?’

Watch List

ADP +62K — labor market resilient, but narrow

The beat (62K vs 40K forecast) shows hiring held up through mid-March. But job growth remains concentrated in a few sectors (education/health 58K, construction 30K). The breadth concern persists. Friday’s NFP (consensus +57K, prior −92K) to closed markets will confirm or deny whether the BLS data aligns with ADP’s more optimistic reading.

Retail Sales +0.6% — consumers spending despite sentiment collapse

The beat confirms the ‘say one thing, do another’ divergence: Michigan Sentiment at 53.3 (worst since 2022) while actual spending rebounds +0.6%. Ex-autos/gas +0.4% is the best since August. This is constructive for GDP but raises a question: how long can spending hold up if sentiment continues deteriorating and gas stays above $4/gallon? Nike’s weak guidance suggests corporate America sees the headwind coming even if February’s receipts looked fine.

ISM Manufacturing at 10:00 AM — the stagflation verdict

Consensus 52.3. If the headline drops below 50, manufacturing is in contraction. PRICES PAID at consensus 73.8 (from 70.5) is the inflation flashpoint — above 73 would be the highest since the 2022 energy crisis. New Orders (prior 55.8) tells us if demand holds. The combination of sub-50 headline + above-73 Prices Paid would be the purest stagflation signal of the war.

MOVE at 96.05 — 4th attempt below 100

MOVE has broken below 100 and snapped back above it after every prior attempt. If MOVE sustains below 100 through today’s data releases — especially if ISM surprises — it confirms the bond crisis is structurally resolved rather than temporarily suppressed. If MOVE spikes back above 100 on data, the pattern holds and the crisis isn’t over.

Oil below $100 — can it sustain?

WTI at $99.57. If oil holds below $100 through the session despite no ceasefire announcement, the market is pricing supply normalization before it happens. If oil rebounds above $100 on continued military escalation (more tanker hits, Hormuz operations), the ‘permanent premium’ thesis reasserts. Today’s EIA Crude Oil Inventories (10:30 AM) adds a supply data point.

Friday NFP + ISM Non-Mfg to closed markets — gap risk planning

Good Friday means NFP (consensus +57K, prior −92K) and ISM Non-Manufacturing are released to CLOSED US equity and bond markets. This is only the second time in 20+ years. The full reaction defers to Monday April 7. April 6 is also Trump’s energy strike pause deadline. The weekend of April 3-6 may be the highest-risk weekend of the entire war for positioning.

Morning check: the pattern finally breaks — and the economy agrees. Three sessions of sustained rally. No more mechanical support. Oil below $100. VIX below 25. Breadth from 21 to 75. ADP +62K and Retail Sales +0.6% both beat — the labor market is hiring and consumers are spending, even as surveys say the sky is falling. The soft data screams recession; the hard data says not yet. China wants a ceasefire. Trump says 2-3 weeks. Israel is preparing for the end. But three missiles hit Israel on Passover, a tanker burns off Qatar, and an IRGC commander is dead. The war rages even as the market prices its end. ISM Manufacturing at 10:00 AM is the last major test before the session’s direction is set. Prices Paid at 73.8 would confirm the inflation damage is real even if growth holds. The geopolitical story says rally. The economic data so far agrees. The inflation data gets the final word.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.