☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: NEUTRAL / CONSOLIDATING — ES 7,148.25 PULLING BACK −0.19% ON WEEKEND HORMUZ RE-CLOSURE AND FIRST SHOTS FIRED IN THE BLOCKADE. WTI $85.89 (+4.00%) BOUNCING FROM FRIDAY’S SPECTACULAR CRASH ON IRAN RE-CLOSING THE STRAIT SATURDAY AND IRANIAN GUNBOATS FIRING ON TANKERS SUNDAY. US NAVY SEIZED IRANIAN SHIP ‘TOUSKA’ — FIRST SEIZURE SINCE BLOCKADE BEGAN. VANCE HEADING TO ISLAMABAD FOR LAST-DITCH TALKS BEFORE CEASEFIRE EXPIRES TUESDAY NIGHT. MOVE 65.70 STILL SUB-BASELINE (THIRD SESSION). VIX +7.78% ON WEEKEND RISK. COR1M REBOUNDING +12.82% FROM WAR LOW. FACTOR TAPE TURNED DEFENSIVE. MEGA EARNINGS WEEK: TSLA WED, GOOGL/MSFT/META THU. WARSH FED CHAIR CONFIRMATION HEARING TUESDAY.

The weekend undid Friday’s de-escalation narrative in dramatic fashion. On FRIDAY, Iran’s Foreign Minister Araqchi declared the Strait of Hormuz open for all commercial vessels for the remaining ceasefire period, and Trump claimed Iran agreed to ‘never close the strait again.’ WTI crashed approximately 14% intraday Friday to $81 — the second-largest single-session oil decline of the war after the Day 29 ceasefire announcement. ES rallied hard through the Friday cash session, closing well above the 7,104.75 pre-market level. The bull flattener deepened: 2Y −7.4 bps, 5Y −7.5 bps, 10Y −6.7 bps, 30Y −5.0 bps — the most bullish yield move of the entire post-ceasefire period.

Then the weekend happened. SATURDAY: Iran re-closed the Strait of Hormuz, blaming the United States for ‘breaches of trust.’ SUNDAY: Iranian gunboats fired on tankers attempting to pass through the strait. The US Navy fired ‘several rounds’ toward an Iranian-flagged ship attempting to violate the US naval blockade, then SEIZED the vessel — the ‘Touska.’ This is the FIRST ship seizure and the FIRST shots fired since the blockade began on April 13. Trump called it a ‘violation’ of the ceasefire. Iran’s military warned it would ‘retaliate against this U.S. act of piracy.’ The ceasefire framework — already stretched to its limits — is now being tested by kinetic engagements for the first time.

The diplomatic picture is in flux. VP JD Vance will lead a US delegation for another round of talks in Islamabad before the ceasefire is scheduled to expire TUESDAY NIGHT. Iran has NOT confirmed participation and is concerned the talks are ‘subterfuge to provide cover for a US surprise attack.’ The ceasefire expiration on April 22 (Wednesday) is no longer a distant calendar item — it is 48 hours away with shots having been fired and a ship seized over the weekend. If Vance secures a framework — even a temporary extension — Wednesday opens with de-escalation re-rating. If talks collapse again (as they did on April 12), the war re-escalates with kinetic precedent now set.

The equity tape is digesting the weekend risk with measured pullback rather than panic. ES at 7,148.25 (−0.19%) represents a modest retreat from Friday’s close but STILL +3.9% above the pre-war 6,881.62 baseline and +266 points from pre-war. The pullback is contained. WTI at $85.89 (+4.00% from Friday’s crash close) has bounced from the ~$81 intraday lows but remains WELL below the pre-weekend $94 level — the market is pricing the Hormuz re-closure as a partial reversal of Friday’s de-escalation, not a full reversal. Brent at $93.32 (+3.25%). International markets are soft: Nikkei −1.14%, DAX −1.09%, EuroStoxx −1.02% — European and Asian risk-off on the weekend kinetic escalation. The US pullback is more contained than international markets, suggesting domestic positioning is more sanguine about Vance’s Islamabad talks.

The Number That Matters: This Is The Most Loaded Week Of The Entire War. Ceasefire Expires Tuesday Night. Warsh Confirmation Hearing Tuesday. UNH Tuesday Pre-Market. Retail Sales Tuesday 8:30 AM. TSLA Wednesday After Close. GOOGL / MSFT / META / CAT Thursday After Close.

Every binary catalyst of the war converges this week. TUESDAY: UNH Q1 before open (the most anticipated healthcare earnings of 2026 — UNH is down 45.5% over the past year and down 15.4% YTD; consensus $6.48-6.76 EPS), Retail Sales 8:30 AM (consensus +1.4% headline, +1.3% core), Kevin Warsh’s Fed Chair-Designate confirmation hearing before the Senate Banking Committee at 10 AM (the most significant Fed-governance event since Powell’s nomination — Warsh wants a ‘leaner, more disciplined Fed’ and has called for ‘regime change’ at the central bank; Tillis blocking complicates passage; Powell’s term expires May 15). TUESDAY NIGHT: Ceasefire formally expires with Vance in Islamabad for last-ditch talks. WEDNESDAY: Tesla Q1 after close (TSLA at $399, +7.62% last Thursday on AI5/AI6), Boeing, ServiceNow. THURSDAY: THE MEGA EARNINGS DAY — Alphabet (GOOGL), Microsoft (MSFT), Meta (META), and Caterpillar (CAT) all report after close. This is the largest single-day concentration of Mag 7 earnings in the entire war. FRIDAY: PG, Colgate-Palmolive. ALSO: FOMC blackout period is active (began April 18) — no Fed communication until the FOMC statement April 29.

The Setup: Flattener Twist — Neutral / Consolidating — Oil Shock Active. Weekend Re-Escalation Reverses Friday’s De-Escalation. MOVE Still Sub-Baseline But VIX Expanding And Factor Tape Turned Defensive. The Market Is In Holding Pattern Ahead Of The Most Binary 48 Hours Of The War.

Monday’s regime is a regime-in-waiting. The weekend re-escalation (Hormuz re-closure + shots fired + ship seizure) reversed Friday’s oil-crash de-escalation, but the equity pullback is measured (−0.19% ES) rather than dramatic. MOVE at 65.70 (−0.30%) still sub-pre-war-baseline for a third consecutive session — the bond market has NOT reversed its capitulation despite the weekend kinetic escalation. This is the single most important signal: if MOVE were above 73.21 this morning, the war would be back in crisis mode. It is not. The bond market is treating the weekend events as diplomatic noise within a framework that is tracking toward resolution, not re-escalation. But VIX at 18.83 (+7.78%) is expanding and the factor tape has turned DEFENSIVE (USMV-SPHB +0.29% — first positive USMV-SPHB spread in six sessions). COR1M rebounded +12.82% to 12.23 — correlations rising from the 10.94 war low as macro risk re-enters the tape. The Mag 7 is 1 green / 6 red with AAPL +0.77% the only green name and META −2.21% the worst. The tape is consolidating ahead of Tuesday’s triple catalyst (UNH + Retail Sales + Warsh hearing) and Tuesday night’s ceasefire expiration with Vance in Islamabad.

2. OVERNIGHT SESSION RECAP

Friday Cash Session Recap (Day 36 Close)

Friday’s cash session was one of the most dramatic of the war — but the price action came AFTER the pre-market report. During the session, Iran’s Foreign Minister Araqchi declared the Strait of Hormuz open for all commercial vessels, and Trump claimed Iran agreed to ‘never close the strait again.’ WTI crashed approximately 14% intraday to $81 — the second-largest single-session oil decline of the entire conflict. ES rallied through the session, closing well above the 7,104.75 pre-market. The curve deepened into a BULL FLATTENER with yields falling dramatically: 2Y −7.4 bps to 3.706%, 5Y −7.5 bps to 3.845%, 10Y −6.7 bps to 4.248%, 30Y −5.0 bps to 4.885%. This was the most bullish single-session yield move of the post-ceasefire-collapse period. Friday closed the best week of the war: four consecutive war highs (Day 33-36), MOVE crashing below pre-war baseline, oil crashing, bull flattener, Russell outperforming, breadth broadening.

Weekend Escalation — Saturday-Sunday

SATURDAY: Iran re-closed the Strait of Hormuz, blaming the United States for ‘breaches of trust.’ The Friday de-escalation narrative was immediately reversed. The Iranian parliament was reportedly preparing legislation to bar vessels from ‘hostile’ countries from the strait. SUNDAY: Iranian gunboats FIRED on tankers attempting to pass through the strait — the first kinetic engagement of the ceasefire period. The US Navy fired ‘several rounds’ toward an Iranian-flagged ship attempting to violate the US naval blockade, then SEIZED the vessel ‘Touska’ in the Gulf of Oman. CENTCOM confirmed the seizure. Trump called it a ‘violation’ of the ceasefire. Iran’s military warned of ‘retaliation against this US act of piracy.’ Defense Secretary Hegseth said forces remain ‘ready to resume combat if ordered.’ VP Vance announced he will lead a US delegation to Islamabad for another round of talks before the ceasefire expires Tuesday night — but Iran has NOT confirmed participation.

Asia-Pacific

Nikkei −1.14% to 59,170 — Japan the largest Asian decliner on the weekend kinetic escalation. Topix +0.15% outperforming the Nikkei — domestic Japan bid vs export-sector weakness. The oil bounce (+4% WTI) hits Japan’s import-cost structure directly. Asian markets broadly soft as the weekend Hormuz re-closure and ship seizure increased geopolitical risk premium across the region.

Europe

DAX −1.09% to 24,596. EuroStoxx 50 −1.02% to 5,940. European markets down sharply — the weekend Hormuz re-closure and shot-firing events hit European markets harder than US because of higher direct oil dependency and proximity to Middle East supply chains. The European re-pricing is more dramatic than the US pullback (−0.19% ES), suggesting US positioning views Vance’s Islamabad talks as the more likely resolution path while European markets are pricing the worst case.

US Pre-Market

Day 53 of Operation Epic Fury. Q2 Day 14. Monday of the most loaded earnings week of the war. FOMC blackout period active.

US FUTURES MODESTLY RED: ES 7,148.25 (−0.19%), NQ 26,754.25 (−0.27%), RTY 2,784.50 (−0.16%), YM 49,638 (−0.01% essentially flat). The Dow holding flat while NQ leads lower tells you this is a tech-led pullback, not a broad risk-off. The Russell at −0.16% outperforming NQ at −0.27% also confirms the pullback is concentrated in large-cap tech / Mag 7 rather than broad market. ES at 7,148.25 is STILL +3.9% above the pre-war 6,881.62 baseline — the pullback from Friday’s highs has not breached any support levels.

MAG 7 ONE GREEN / SIX RED — DEFENSIVE ROTATION: AAPL +0.77% (the ONLY green Mag 7 name — Apple is catching a defensive bid as the safe-haven tech name). TSLA −0.39% (modest giveback). GOOG −0.72%. MSFT −1.03% (giving back some of the 3-day +9% software reflation). NVDA −1.07%. AMZN −1.20%. META −2.21% (the worst Mag 7 performer — highest-beta Mag 7 name giving back the most on the weekend risk-off). The Mag 7 composition flipped from last week’s 6 green / 1 red to this week’s 1 green / 6 red — the weekend kinetic escalation hit positioning hardest in the highest-beta names.

FACTORS TURNED DEFENSIVE — FIRST POSITIVE USMV-SPHB IN SIX SESSIONS: USMV +0.11%. DGRO +0.09%. VYM +0.07%. SPLV −0.06%. Only 3/12 factors green (USMV, DGRO, VYM — all defensive/income names). SPHB −0.19%. MTUM −0.21%. QUAL −0.27%. IJR −0.24%. USMV−SPHB spread +0.29% (POSITIVE for the first time in six sessions — the defensive factor regime returns). This is a clear shift from last week’s five-session risk-on streak.

SECTORS — ENERGY LEADING, TECH LAGGING: XLE +0.67% (energy catching the WTI +4% bounce). XLP +0.48% (defensive staples bid). XLF +0.32% (financials resilient ahead of earnings week). Five sectors green, six red. XLC −0.42% (META drag). XLY −0.66% (TSLA/AMZN drag). XLV −0.36% (healthcare positioning ahead of UNH Tuesday). The sector tape tells you this is an energy-shock-plus-defensive-rotation session, not a broad selloff.

WTI $85.89 (+4.00%) — THE OIL BOUNCE. Friday’s ~14% crash (from ~$94 to ~$81 on Iran declaring Hormuz open) has been partially reversed by Saturday’s re-closure and Sunday’s kinetic events. WTI cumulative from pre-war $67.02 is +$18.87 / +28.2%. Brent at $93.32 (+3.25%). The Brent-WTI spread at ~$7.43 has narrowed from the peak but remains elevated. The oil market is pricing a ‘partial re-closure / partial access’ scenario rather than the full de-escalation Friday priced or the full closure the war’s peak priced.

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 04/17/26. Provided for informational purposes only; not as investment advice.

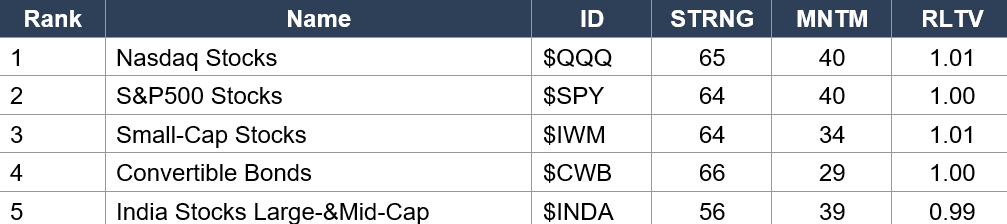

Asset Classes — Top 5

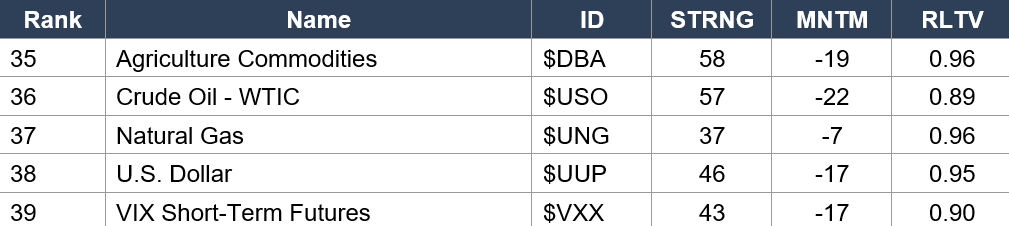

Asset Classes — Bottom 5

Regime signal: Nasdaq ($QQQ rank 1, MNTM 40, STRNG 65 — highest STRNG in the data) holds #1 for a second consecutive data set. MNTM flat at 40 (was 41 yesterday). S&P ($SPY rank 2, MNTM 40) also flat. Small-Cap ($IWM rank 3, MNTM 34, RLTV 1.01) holds top 3 with RLTV ticking above 1.00 — small-cap relative outperformance is now in the data. Convertible Bonds ($CWB rank 4, STRNG 66 — HIGHEST STRNG in the entire data set). India ($INDA rank 5, MNTM 39) enters the top 5 for the first time in the war — the emerging market bid broadening beyond Latin America. CRITICAL: Crude Oil ($USO rank 36, MNTM −22, RLTV 0.89) — RLTV CRASHED from 0.96 yesterday to 0.89 today, the LOWEST RLTV of the entire war for crude. Friday’s 14% oil crash is fully captured. Dollar ($UUP MNTM −17) recovered modestly from −21. VIX ($VXX MNTM −17, RLTV 0.90) — fear premium bleeding despite VIX pop today. Bitcoin ($IBIT rank 15, MNTM 27, RLTV 1.01). Gold ($GLD rank 30, MNTM 17). Gasoline ($UGA rank 34, MNTM −17, RLTV 0.95) — gasoline RLTV also crashed.

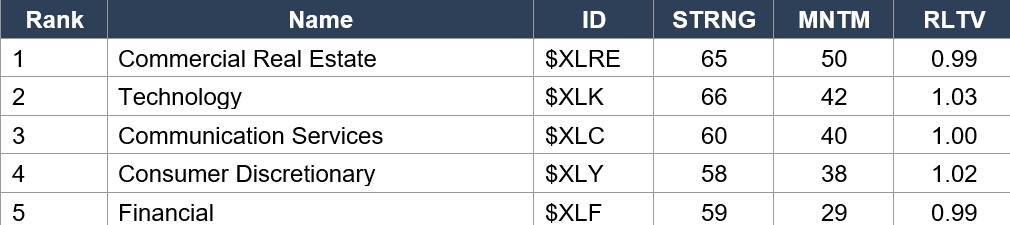

Sector ETFs — Top 5

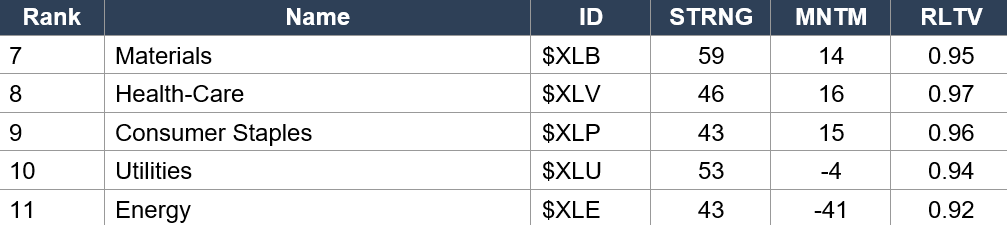

Sector ETFs — Bottom 5

Regime signal: Commercial Real Estate ($XLRE rank 1, MNTM 50 — HIGHEST sector momentum, STRNG 65) holds #1 for a sixth consecutive data set with momentum RISING further (49 → 50). $XLRE is the single most consistent leader of the entire war's data series. Technology ($XLK rank 2, MNTM 42, RLTV 1.03) — tech momentum cooled from 45 to 42 on Thursday's profit-taking. Financial ($XLF rank 5, MNTM 29) continued its decline from the 46 peak — bank-beat trade fully matured. CRITICAL: Utilities ($XLU MNTM −4) still negative and Utilities RLTV 0.94 is the LOWEST of any sector — bond-vol compression removing defensive utility bid entirely. Energy ($XLE rank 11, MNTM −41, RLTV 0.92) — MNTM RECOVERED modestly from −49 to −41 on Friday's oil crash (lower oil = less negative for energy equities via demand-destruction removal). RLTV at 0.92 is still the weakest sector. Today's +4% WTI bounce will partially reverse this recovery in tomorrow's data.

Industry ETFs — Top 5

Industry ETFs — Bottom 5

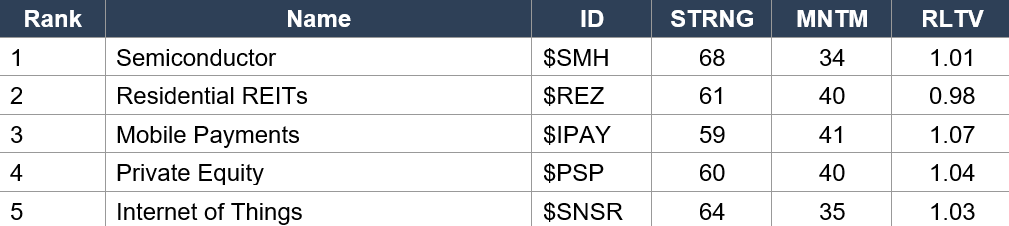

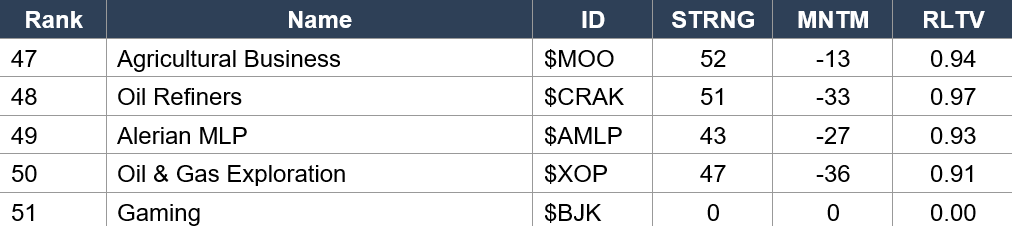

Regime signal: Semiconductor ($SMH rank 1, STRNG 68 — HIGHEST STRNG in any Quiggle table of the war) holds #1 industry for a second consecutive data set. Mobile Payments ($IPAY rank 3, MNTM 41, RLTV 1.07 — tied with $IGV for highest RLTV in the data) — fintech momentum accelerating. Private Equity ($PSP rank 4, MNTM 40, RLTV 1.04). NOTABLE: Software Technology ($IGV rank 33, MNTM 25, RLTV 1.09 — HIGHEST RLTV OF ANY INDUSTRY FOR THE SECOND CONSECUTIVE DATA SET). The IGV recovery is now fully structural: rank 50 (Apr 10) → 47 → 38 → 36 → 33, RLTV 0.94 → 0.94 → 1.01 → 1.07 → 1.09. Software is the strongest relative-strength story in the entire data set. Cyber Security ($CIBR rank 40, MNTM 15, RLTV 1.05). Oil & Gas Exploration ($XOP rank 50, MNTM −36, RLTV 0.91) — MNTM improved slightly from −40 on Friday’s oil crash but remains deeply negative. Today’s +4% WTI bounce will reverse some of this improvement.

4. MORNING DATA REACTION

No US Morning Economic Data Scheduled. Monday Data-Light. Only Catalyst: Lagarde 12:40 PM.

No US economic data is scheduled for Monday morning. Canadian CPI printed at 8:30 AM (0.9% m/m vs 1.1% consensus — miss) but is not directly material to the US regime read. The only scheduled event is ECB President Lagarde speaking at 12:40 PM — her interpretation of the weekend Hormuz re-closure and its implications for European energy inflation will be the macro catalyst. Given the ceasefire expires Tuesday night and Vance is heading to Islamabad, any Lagarde commentary on ECB policy response to sustained energy-price pressure would layer onto the existing rate-vol framework.

Friday Afternoon — Iran’s FM Declared Hormuz Open. WTI Crashed ~14% To $81. ES Rallied. Bull Flattener Deepened.

This happened after Friday’s Morning Bell was generated. During Friday’s cash session, Iran’s Foreign Minister Araqchi declared the Strait of Hormuz open for all commercial vessels during the remaining ceasefire period. Trump stated Iran had agreed to ‘never close the strait again.’ WTI crashed approximately 14% intraday to $81 — Brent fell ~13% to $86.52. This was the largest single-session oil decline since the Day 29 post-ceasefire announcement. ES rallied hard, closing well above the 7,104.75 pre-market. The bull flattener deepened dramatically with 2Y −7.4 bps (the largest single-session front-end move of the post-ceasefire period). Friday’s close was the war’s fifth consecutive session of new highs. The best week of the war.

Weekend — Iran Re-Closed Hormuz Saturday. Gunboats Fired On Tankers Sunday. US Navy Seized Iranian Ship ‘Touska.’ Oil Bounced. The Ceasefire Is Being Tested Kinetically.

Saturday: Iran declared the Strait of Hormuz closed again, citing US ‘breaches of trust.’ The Iranian parliament was reportedly preparing legislation barring vessels from ‘hostile countries.’ Sunday: Iranian gunboats FIRED on tankers attempting transit — the first kinetic engagement of the ceasefire period. The US Navy responded by firing ‘several rounds’ toward an Iranian-flagged ship, then SEIZING it in the Gulf of Oman. The ‘Touska’ seizure is the first ship captured since the blockade began April 13. Trump called it a ‘violation.’ Iran’s military warned of ‘retaliation.’ Defense Secretary Hegseth: ‘forces remain ready to resume combat if ordered.’ WTI bounced from ~$81 Friday close to $85.89 Monday pre-market. VP Vance is leading a US delegation to Islamabad for last-ditch talks, but Iran has NOT confirmed its participation — raising the possibility the ceasefire expires Tuesday night without a framework for extension. The kinetic precedent set this weekend means any post-expiration escalation would start from a HIGHER baseline of hostility.

5. THE DYRH READ

Regime: Flattener Twist — Neutral / Consolidating — Oil Shock Active. Weekend re-escalation reverses Friday’s de-escalation narrative. The Hormuz re-closure, shots fired, and ship seizure are genuine kinetic escalation — the first of the ceasefire period. But MOVE at 65.70 (third session sub-pre-war-baseline) says the bond market has NOT reversed its capitulation. The equity pullback is contained (−0.19% ES vs −1.09% DAX). The factor tape turned defensive (USMV-SPHB +0.29%) for the first time in six sessions. COR1M rebounded +12.82% — macro risk re-entering the tape. The market is in holding pattern ahead of Tuesday’s triple catalyst and Tuesday night’s ceasefire expiration. Confidence: MODERATE — weekend kinetic escalation introduces event-risk uncertainty not present last week.

Yield Curve: FLATTENER TWIST — Front Rising, Long Falling. The Most Complex Regime To Trade.

2Y +1.5 bps to 3.721% (front end RISING — Fed-cut probability being trimmed on the WTI bounce), 5Y +0.7 bps to 3.852%, 10Y +0.2 bps to 4.250% (essentially flat), 30Y −0.2 bps to 4.883% (long end FALLING — the long end retained Friday’s bull move and is not responding to the weekend re-escalation). The flattener twist reflects: (1) Near-term Fed hawkishness re-entering on the oil bounce — the 2Y rising says the market is trimming the rate-cut probability that was added during Friday’s bull flattener; and (2) Long-run growth pessimism — the 30Y falling says the term premium is compressing even as near-term inflation expectations tick higher. This is the most complex regime because the front and long ends are giving contradictory signals. The resolution depends on whether the oil shock extends (in which case the front end keeps rising and the long end eventually follows — converting to a bear regime) or the oil shock fades (in which case the front end reverses and the long end stays compressed — reverting to Friday’s bull regime).

MOVE 65.70 (−0.30%) — Third Session Sub-Pre-War Baseline. The Bond Market Has NOT Reversed Its Capitulation Despite Weekend Kinetic Escalation.

MOVE at 65.6953 is the single most important signal this morning. If the weekend kinetic escalation (shots fired, ship seized, Iran re-closed Hormuz) were material to the bond market’s assessment of macro risk, MOVE would have snapped back above the 73.21 pre-war baseline. It did not. MOVE compressed further (−0.30%). The bond market is treating the weekend events as noise within the existing framework rather than a structural regime change. This is the third consecutive session below the pre-war baseline: Thursday 67.94 → Friday (post-Hormuz-opening crash) → Monday 65.70. The cumulative decline from the 115.02 war high is now 49.33 points (−42.9%). The bond market believes the ceasefire framework — despite the weekend friction — is tracking toward resolution, not re-escalation.

ES 7,148.25 (−0.19%) — Modest Pullback From Five Consecutive War Highs. +3.9% Above Pre-War Baseline.

ES pulled back modestly from Friday’s highs but remains well above any technical support level. The +3.9% above pre-war baseline is the highest cumulative war-to-date gain at any Monday open. The −0.19% pullback is dramatically more contained than the international response (DAX −1.09%, Nikkei −1.14%) — the US market is treating the weekend risk as digestible. Cumulative recovery from Day 22 low is approximately +700 points / +10.8%. Friday’s closing rally extended the four-consecutive-war-high streak to five sessions (Day 33-37).

COR1M 12.23 (+12.82%) — Correlations REBOUNDING From War Low. Macro Risk Re-Entering The Tape.

COR1M bounced from 10.94 (Friday’s war low, the fifth consecutive new low) to 12.23 (+12.82%). The five-session decline in correlations (12.39 → 11.58 → 11.05 → 10.94 → 12.23) has reversed. This tells you the weekend’s macro risk (shots fired, ship seized, ceasefire expiration approaching) is pulling names back into correlated movement — the idiosyncratic-stock-picking regime from last week is giving way to macro-headline-driven trading. This is consistent with the VIX expansion (+7.78%) and the defensive factor rotation (USMV leading). The COR1M rebound is the first since the post-ceasefire-collapse period began and represents a natural position-adjustment ahead of the most binary week of the war.

WTI $85.89 — Bounced From $81 But Below Pre-Weekend $94. The Oil Market Is Pricing A ‘Partial Access’ Scenario.

WTI’s trajectory this weekend: ~$94 (Thursday close) → ~$81 (Friday crash close on Hormuz opening declaration) → $85.89 (Monday open on Iran re-closure + ship seizure). The oil market is pricing neither full Hormuz closure ($95-100+ range) nor full Hormuz opening ($80-85 range) but a partial-access scenario consistent with the US blockade operating alongside sporadic Iranian attempts to reassert control. Cumulative from pre-war $67.02 is +$18.87 / +28.2% — meaningfully below the ~+36.6% war-to-date premium from mid-last-week. Brent-WTI spread at ~$7.43 is narrowing as the supply-chain premium from Hormuz disruption eases. XLE at +0.67% on WTI +4.00% — energy equities underperforming crude again; the demand-destruction discount re-embedded after Friday’s brief positive decoupling.

BTC $75,395 (−2.84%) — Risk-Off Signal. Gold $4,842.30 (−0.76%). Silver −1.79%. Precious Metals Weak.

BTC gave back from the $75,900 war high to $75,395 (−2.84%) — the largest single-session BTC decline in over a week. The crypto weakness is consistent with the broader risk-off positioning (META −2.21%, AMZN −1.20%, factor tape defensive). Gold at $4,842.30 (−0.76%), Silver at $80.38 (−1.79%), Platinum −2.58%, Palladium −2.27% — the entire metals complex is weak. This is unusual for a weekend with kinetic geopolitical escalation — historically, gold rallies on shots-fired headlines. The gold weakness suggests the market is treating the weekend events as positioned-for rather than surprise risk — the ceasefire expiration was widely anticipated and the kinetic escalation is being digested as the opening of negotiating leverage rather than the start of a new war phase.

6. THE GAME PLAN

This Week’s Calendar — The Most Loaded Of The Entire War:

MONDAY APR 20 — No major US data. Lagarde 12:40 PM. Position-management ahead of Tuesday’s triple catalyst. TUESDAY APR 21 — UNH Q1 pre-market ($6.48-6.76 EPS consensus, $109.4-109.8B revenue; UNH is down 45.5% over past year). Retail Sales 8:30 AM (+1.4% headline, +1.3% core consensus). Kevin Warsh Fed Chair-Designate confirmation hearing 10 AM (Senate Banking Committee — most significant Fed-governance event since Powell’s nomination). LMT, COF pre-market. TUESDAY NIGHT — Ceasefire formally expires. VP Vance in Islamabad for last-ditch talks (Iran participation UNCONFIRMED). WEDNESDAY APR 22 — TESLA Q1 after close (TSLA at $399; Q1 deliveries missed expectations). Boeing, ServiceNow after close. THURSDAY APR 23 — ALPHABET (GOOGL), MICROSOFT (MSFT), META (META), CATERPILLAR (CAT) after close — the MEGA earnings day. The largest single-day concentration of Mag 7 earnings in the entire war. FRIDAY APR 25 — PG, Colgate-Palmolive pre-market. FOMC blackout active through April 29.

The Bull Case:

MOVE at 65.70 — third session sub-baseline, the bond market has NOT reversed despite weekend kinetic escalation. ES at 7,148.25 still +3.9% above pre-war baseline — pullback measured not panicked. US equity pullback −0.19% dramatically more contained than Europe −1.09% — suggesting US positioning views Vance talks as credible path to resolution. Friday’s bull flattener (2Y −7.4 bps, 10Y −6.7 bps) was the most constructive yield move of the war — the long-end relief from Friday is being retained (30Y −0.2 bps today). Oil at $85.89 remains WELL below pre-weekend $94 — Friday’s structural repricing of the war premium is partially intact. Quiggle data shows $SPY rank 2 / MNTM 40, $QQQ rank 1 / MNTM 40 — structural US equity leadership maintained. $IGV RLTV 1.09 for the second consecutive data set — software recovery fully confirmed. $SMH STRNG 68 highest of the entire war. Mega earnings week (TSLA/GOOGL/MSFT/META) is the opportunity to validate the equity re-rating via corporate fundamentals. If Vance secures even a temporary extension in Islamabad, Wednesday opens with de-escalation re-rating. Warsh hearing could provide clarity on Fed succession — removal of the governance uncertainty is bullish for risk assets. VIX at 18.83 still well below the 25 crisis threshold.

The Bear Case:

FIRST SHOTS FIRED of the ceasefire period — Iranian gunboats fired on tankers, US Navy fired on and seized an Iranian ship. This is KINETIC ESCALATION, not diplomatic posturing. The ceasefire framework is being tested at its limits 48 hours before expiration. Iran has NOT confirmed participation in Vance’s Islamabad talks — the possibility of ceasefire expiration with no extension framework and kinetic precedent set is REAL. VIX +7.78% — equity vol expanding for the first time in the post-ceasefire period. COR1M rebounded +12.82% — macro risk re-entering the tape. Factor tape turned DEFENSIVE (USMV-SPHB +0.29% positive) for the first time in six sessions. Mag 7 at 1 green / 6 red — risk-off positioning concentrated in highest-beta tech names (META −2.21%). International markets selling harder (DAX −1.09%, Nikkei −1.14%) — global risk-off. BTC −2.84%, Gold −0.76%, Silver −1.79% — even traditional safe havens weak. WTI bounced +4% from Friday crash — if Hormuz closure persists, oil re-escalates toward $95+ and the entire Friday oil-relief narrative unwinds. Flattener twist in the curve is the most complex regime to trade — contradictory front/long signals. The Warsh hearing introduces governance uncertainty — Tillis blocking, Powell investigation, Trump threatening to fire Powell if he stays past May 15 — the Fed succession is the most contested in modern history. UNH earnings Tuesday are a stock that’s fallen 45.5% over the past year reporting into the most loaded macro week of the war. TSLA Q1 after Wednesday’s close reports into the ceasefire-expiration overnight risk. GOOGL/MSFT/META Thursday after close is the most concentrated Mag 7 earnings event of the war — any disappointment could break the narrow-leadership structure that has sustained the 10.8% rally from Day 22 lows.

Regime: Flattener Twist — Neutral / Consolidating — Oil Shock Active. The market is in a holding pattern ahead of the most binary 48 hours of the entire war. The weekend kinetic escalation (shots fired, ship seized, Hormuz re-closed) reversed Friday’s de-escalation narrative but the bond market’s MOVE capitulation has NOT reversed. Equities are pulling back modestly while international markets sell harder — the US market gives Vance’s Islamabad talks the benefit of the doubt. The factor tape turned defensive. Correlations are rebounding. VIX is expanding. The setup into Tuesday’s triple catalyst (UNH + Retail Sales + Warsh hearing) and Tuesday night’s ceasefire expiration is the most risk-laden of the war. The resolution of these events will determine whether the post-ceasefire-collapse rally extends into a structural bull phase (MOVE stays sub-baseline, ceasefire extended, earnings delivered) or reverses into re-escalation (Hormuz fully re-closed, ceasefire collapses, MOVE snaps back above baseline). There is no middle ground this week.

Watch List

Tuesday Night Ceasefire Expiration + Vance Islamabad Talks — THE WEEK’S DEFINING BINARY

The ceasefire formally expires Tuesday night. VP Vance is leading a US delegation to Islamabad. Iran has NOT confirmed participation. If Vance secures even a temporary extension, Wednesday opens with de-escalation re-rating (oil targets $80, equities extend). If talks fail or Iran does not show, the ceasefire expires with kinetic precedent set (ship seizure, shots fired) and the war enters its most dangerous phase since Day 22. Wednesday’s TSLA earnings report after close into this overnight risk makes the positioning extremely complex.

Warsh Confirmation Hearing Tuesday 10 AM — Fed Governance Inflection

Kevin Warsh’s confirmation hearing before the Senate Banking Committee is the most significant Fed-governance event since Powell’s nomination. Warsh has called for ‘regime change’ at the Fed and described the institution as having ‘lost its way.’ Powell’s term expires May 15. Tillis blocking. Trump threatening to fire Powell if he stays as interim chair. The hearing will define market expectations for the Fed’s institutional direction over the next four years. A smooth hearing = governance premium removed. A contentious hearing with no resolution on the Tillis block = governance uncertainty sustained through May 15 expiration.

GOOGL / MSFT / META Thursday After Close — The Largest Mag 7 Earnings Day Of The War

Three of the seven largest companies in the world report on the same day. If all three deliver (as the eight financial earnings beats delivered last week), the equity re-rating extends with definitive corporate-fundamentals validation. If any one disappoints — particularly on AI capex, advertising demand, or cloud growth — the narrow leadership that COR1M at 12.23 says is now re-correlating could break and produce an outsized index-level decline. MSFT’s three-day +9% software reflation is the most stretched entering earnings; META at −2.21% today is the most depressed. GOOG is the swing name.

UNH Tuesday Pre-Market — The Most Anticipated Healthcare Earnings Of 2026

UNH has fallen 45.5% over the past year and 15.4% YTD. Q1 consensus: $6.48-6.76 EPS, $109.4-109.8B revenue. The medical care ratio is the most critical metric — FY26 target 88.8% ±50 bps. UNH’s 2025 was defined by the cyberattack, the CEO departure, and the Q4 charge. Q1 is the quarter where new CEO Stephen Hemsley validates the recovery story. An upside surprise could be one of the largest single-stock moves of earnings season given the extreme negative positioning.

Retail Sales Tuesday 8:30 AM — The Consumer Pulse Into The Oil Shock

Consensus +1.4% headline, +1.3% core. March retail sales will capture the early war-period consumer response to gasoline price spikes. A beat confirms the consumer is absorbing the energy shock without demand destruction — bullish for the bifurcation thesis. A miss signals the energy shock is reaching the consumer — bearish for the ‘look through’ narrative the Fed needs.

Morning check: Day 53. The war is fifty-three days old and the weekend brought its most dramatic escalation since the Islamabad collapse — Iranian gunboats firing on tankers, the US Navy seizing a ship, Iran re-closing the Strait of Hormuz. And yet: MOVE at 65.70, third session below the pre-war baseline. The bond market has not flinched. ES at 7,148.25, pulling back −0.19% while DAX falls −1.09%. The US market gives Vance’s Islamabad talks the benefit of the doubt. The factor tape turned defensive for the first time in six sessions. Correlations are rebounding. VIX is expanding. The setup into Tuesday is the most binary of the entire war: UNH before open, Retail Sales at 8:30, Warsh hearing at 10, ceasefire expires that night with Vance in Islamabad and Iran uncommitted. Then Wednesday: TSLA after close into the ceasefire overnight. Then Thursday: GOOGL, MSFT, META after close — the largest concentration of Mag 7 earnings of the war. Every regime — rates, equities, energy, governance — converges this week. The resolution determines whether the post-ceasefire rally from Day 29 becomes a structural bull market or the war re-escalates with kinetic precedent. There is no middle ground. Position accordingly.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.