☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: POST-CEASEFIRE REFLATION RALLY — WTI CRASHES −17.51% TO $93.17 (LARGEST MOVE SINCE APRIL 2020). EQUITIES GAP MAJOR HIGHER. METALS EXPLODE. VIX BELOW 21. USMV-SPHB AT −2.89% — THE DEEPEST RISK-ON FACTOR PRINT OF THE ENTIRE WAR. THE CEASEFIRE IS HERE.

At 6:32 PM ET Tuesday — 88 minutes before the 8 PM deadline expired — President Trump formally announced a 2-week ceasefire on Truth Social: ‘I agree to suspend the bombing and attack of Iran for a period of two weeks.’ Contingent on Iran’s ‘COMPLETE, IMMEDIATE, and SAFE OPENING of the Strait of Hormuz.’ Trump added that Iran’s 10-point proposal is ‘workable’ and ‘almost all of the various points of past contention have been agreed to between the United States and Iran.’ Iran’s Supreme National Security Council formally accepted the 2-week ceasefire later in the evening. Iran SNSC: ‘Good news to the dear nation of Iran! Nearly all the objectives of the war have been achieved.’ But also: ‘It is emphasized that this does not signify the termination of the war. Our hands are on the trigger, and the moment the enemy makes the slightest mistake, it will be met with full force.’ Iran FM Araghchi: ‘For a period of two weeks, safe passage through the Strait of Hormuz will be possible via coordination with Iran’s Armed Forces and with due consideration of technical limitations.’ Formal US-Iran negotiations begin Friday in Islamabad. Pakistan PM Sharif and Army Chief Field Marshal Munir credited as the proximate mediators. Wikipedia is already calling this the ‘Islamabad Accords.’

Every cross-asset signal has gapped decisively in the de-escalation direction in unison — the cleanest ‘regime reset’ pre-market of the entire war. WTI crashed −$19.78 / −17.51% to $93.17 — by some measures the largest single-day WTI move since the April 2020 negative-price demand shock. The 24-hour range from yesterday morning’s war-high $114.87 to this morning’s $93.17 is −$21.70 / −18.9%. Brent at $92.83 is down −15.05%. RBOB Gasoline collapsed −11.11%. Heating Oil −15.22%. ES futures gapped +2.59% to 6,829.25 — now ~218 points above Monday’s cash close, putting the S&P within striking distance of full recovery (pre-war 6,881.62 baseline = +95% recovery of the war’s drawdown in 5 sessions). Nasdaq +3.37%, Russell +3.46% (best US index 3rd consecutive session), Dow +2.60%. The European cash open produced the catch-up rally: DAX +4.87%, EuroStoxx +5.16%, Nikkei +5.85%, Kospi +6.9% — Europe was closed Easter Monday and closed early Tuesday before the ceasefire chatter peaked, so today’s open absorbs 4-5 days of cumulative news in a single session.

The metals complex EXPLODED with the broadest and largest gains of the war: Palladium +10.87% (the standout single print), Silver +7.67%, Platinum +7.28%, Copper +3.59%, Gold +2.92% extending Tuesday’s +1.64% breakout. Gold has now moved from $4,684.7 Monday close to $4,821.6 Wednesday pre = +$136.9 / +2.92% in two sessions — fully resolving the three-session yellow flag from Day 27/28. Bonds rallied hard with the curve in clean bull flattener (5Y −7.4 bps the biggest tenor move; 2Y −6.4 bps to 3.736% new low; 30Y −4.0 bps to 4.838% — essentially back to the pre-war 4.843% baseline). DXY crashed −1.22% to 98.465 — the deepest sub-100 print of the post-Day 22 period and the largest single-session DXY decline of the war. All G10 currencies strongly green. BTC ripped to $72,185 (+4.36%, new multi-day high). USMV-SPHB pre-market spread at −2.89% is the DEEPEST RISK-ON FACTOR PRINT OF THE ENTIRE WAR — five times deeper than the prior war record (−0.55% on Day 27 close).

The Number That Matters: VIX at 20.76 — first sub-21 print since pre-Day 22, largest single-day VIX decline of the war (−19.47%).

The crash from yesterday’s 25.78 to today’s 20.76 in a single overnight is comparable in magnitude to the entire four-session post-Day 22 normalization (which moved VIX from 31.05 to 24.54). VIX at 20.76 puts the equity vol regime back at the 20 fear threshold rather than the 25 crisis threshold — equities are now pricing ‘fear without crisis’ rather than ‘crisis.’ If the cash session prints VIX below 20, the equity vol regime is functionally complete back to pre-war levels. The CRITICAL stale print: MOVE Index is showing the Tuesday close 83.1452 with no fresh Wednesday print yet. The fresh MOVE print is the binary rates-vol signal of the day. Below 80 = bond crisis is functionally OVER. Above 82 = bond market reserving caution about the two-week ceasefire’s durability.

The Setup: Post-Ceasefire Reflation Rally — WTI Crashes, Metals Explode, VIX Below 21, USMV-SPHB Deepest Risk-On of the War. The Cleanest Regime Reset of the Entire Conflict.

Three sectoral regimes in 48 hours: Monday’s stagflationary ISM barbell → Tuesday’s defensive flip on Kharg → Wednesday’s broad reflation cyclical. The post-Day 22 small-cap rate-cut trade is fully reasserted with cyclicals (XLY, XLI, XLF, XLB) bid +2-3.6%. Only XLE is red pre-market at −5.07% — the cleanest possible sector signal that energy is the cohort fully pricing the de-escalation and everything else is bid. The 30Y yield is back below 4.85% essentially at the pre-war 4.843% baseline. ES is within striking distance of full recovery. The session’s binary catalyst is the FOMC Minutes at 2 PM. The week’s data sequence (PCE Thursday, CPI Friday) matters considerably LESS than 24 hours ago because the WTI shock is unwinding in real time.

2. OVERNIGHT SESSION RECAP

Asia-Pacific

Nikkei 225 +5.4% to 56,308 (close +5.85% on futures). Kospi +6.9% to 5,872 (Korea was the day’s biggest single-market move). Topix +3.2%. Hang Seng +3.1%. Shanghai Composite +2.7%. ASX 200 +2.6%. Asian markets digested the ceasefire announcement during their cash session and produced the broadest single-region rally of the war. Korean equities at +6.9% are the standout — Korea has the highest oil-import sensitivity in Asia and the most direct beneficiary of the WTI crash through margin expansion at refiners and chemical exporters. The yen strengthened from 159.52 to 158.39 (USD/JPY) — Japan’s currency is finally catching the de-escalation flow after lagging through the war.

Europe

European cash markets reopened after Easter Monday closure with massive catch-up gains. DAX +4.87% to 23,996. CAC 40 +4.0% to 8,224. FTSE 100 +2.3% to 10,583. EuroStoxx 50 +5.16%. EUR/USD jumped from 1.1597 to 1.1701. Europe was the most exposed major economy to the war’s energy dimension and is now the biggest beneficiary of the WTI crash. The 4-day catch-up gap has produced the largest single-session European move of the war by a wide margin.

US Pre-Market

Day 40 of Operation Epic Fury (Ceasefire Day 1). Q2 Day 6. The morning after the formal ceasefire announcement.

ALL US INDICES STRONGLY GREEN: ES 6,829.25 (+2.59%, +218 above Monday’s cash close), NQ 24,229.50 (+3.37%), YM 48,027 (+2.60%), RTY 2,648.6 (+3.46% — best US index 3rd consecutive session). The Russell leading at +3.46% confirms the small-cap rate-cut trade reasserting in the post-ceasefire reflation. ES at 6,829.25 is +95% recovery of the war’s drawdown — within striking distance of the pre-war 6,881.62 baseline.

ALL 7 MAG 7 GREEN PRE-MARKET. META at +5.07% leads — Meta has been quietly outperforming the cohort during the de-escalation phase. AMZN +4.08%, GOOG +4.03%, TSLA +4.77% (the 4-day bleed broken decisively), NVDA +3.50%, MSFT +3.17%, AAPL +2.08% (smallest Mag 7 gain — yesterday’s worst Mag 7 at −2.07% is today’s smallest bid; the Apple weakness pattern persists even in a broad reflation rally and may compound into Q2 earnings). SOXX +5.39% leading thematics — the cleanest semis broadening of the war confirming NVDA’s leadership reset is broadening to the chip complex. ARKW +5.20%, DRIV +4.92%, ARKG +4.90%, ARKQ +4.58% — the entire ARK/growth complex ripping. ICLN +3.36% catches the clean energy bid as crude crashes (inverse oil-clean energy correlation working). BLOK +3.89% confirms BTC.

CRITICAL OVERNIGHT: Trump 6:32 PM Truth Social formal ceasefire announcement. Iran SNSC formal acceptance. Hormuz to reopen with ‘technical limitations.’ Israel honors ceasefire vs Iran but CONTINUES Lebanon operations (contradicting Pakistan PM Sharif’s claim that Lebanon was included). Israel and UAE BOTH sounded missile alerts shortly after the ceasefire announcement (target/launcher unclear) — partial confirmation that not all combatants immediately stood down. Formal US-Iran negotiations begin Friday in Islamabad. The ‘TACO’ trade sentiment is now mainstream — eToro’s Wong: ‘TACO is becoming less of a joke and more of a trading strategy.’ The 25th Amendment chatter from Tuesday’s ‘civilization will die tonight’ Trump rhetoric has fully dissipated.

STRUCTURAL CAVEATS REMAIN: BofA’s Francisco Blanch (CNBC): ‘Oil market still extremely tight even if futures markets are down.’ Bloomberg: ‘Oil markets will take time to fix’ — months to repair Persian Gulf refineries, weeks to clear shipping backlogs. QatarEnergy CEO: Ras Laffan LNG complex has 17% of Qatar’s export capacity offline; repairs expected to take 3-5 years. KCM Trade’s Tim Waterer: ‘Cautious optimism rather than outright celebration. The ceasefire is only two weeks long.’ Global X’s Billy Leung: ‘Relief rally layered on top of a still fragile macro backdrop... investors are not fully removing hedges.’

This week’s calendar (verified): TODAY 2 PM — FOMC Minutes (March meeting) — the day’s largest single-event risk for the cross-asset rally. Powell’s Harvard speech already killed the rate-hike thesis; the minutes will reveal committee unity. LEVI after close. THURSDAY 8:30 AM — PCE Price Index February (Fed’s preferred inflation gauge — February data will NOT yet reflect the war oil shock). Initial Jobless Claims. STZ if not already reported. CAG. FRIDAY 8:30 AM — CPI March (the FIRST CPI to fully reflect the war oil shock; pre-ceasefire street consensus around +0.9% MoM headline / +0.3% core; POST-CEASEFIRE this print matters considerably less than 24 hours ago). Michigan Sentiment Preliminary.

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 04/07/26. Provided for informational purposes only; not as investment advice.

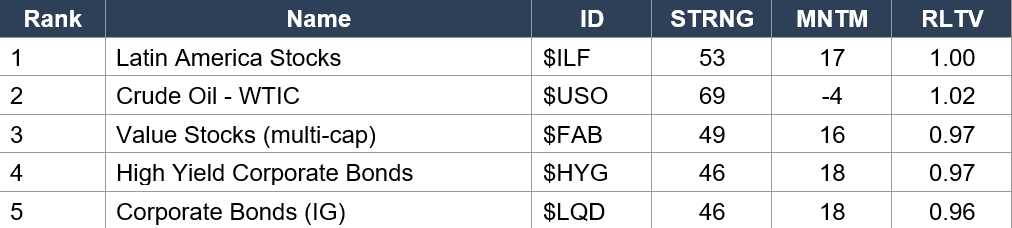

Asset Classes — Top 5

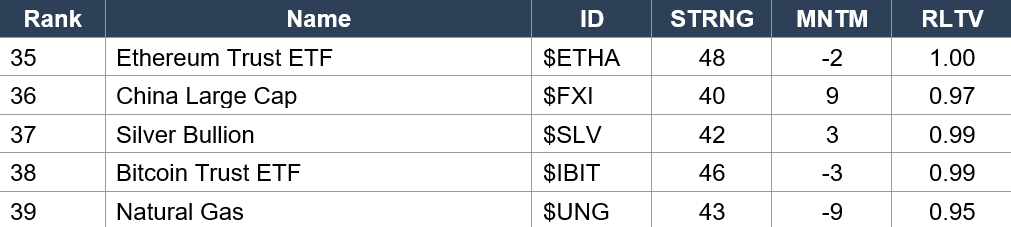

Asset Classes — Bottom 5

Regime signal: Latin America ($ILF rank 1, MNTM 17) holds the top spot for the 4th consecutive data set. Crude Oil ($USO rank 2, STRNG 69, MNTM −4, RLTV 1.02) RLTV has compressed from 1.08 to 1.02 in one session — the energy de-rating is showing up in the data even before today’s −17.51% crash, which will collapse the rankings tomorrow. CRITICAL: Both Investment Grade ($LQD rank 5, MNTM 18) and High Yield ($HYG rank 4, MNTM 18) credit have the SAME momentum (+18) — credit markets are pricing aggressive Fed easing in unison. Value Stocks ($FAB rank 3, MNTM 16) jumped into the top 3 — the value rotation is consolidating ahead of the broad reflation. VIX ($VXX rank 26, MNTM −5, RLTV 0.86) shows the panic trade dying at the data level. Dollar ($UUP rank 30, MNTM −9, RLTV 0.95) collapsed further. Gold ($GLD rank 32, MNTM 8, RLTV 1.00) — momentum has finally turned positive (+8) after multiple sessions of negative scores, captured Tuesday’s breakout. Silver ($SLV rank 37, MNTM 3) and Bitcoin ($IBIT rank 38, MNTM −3) both still in the bottom 5 from Tuesday close — these will move sharply higher in tomorrow’s data. NOTE: Quiggle data captures Tuesday’s close BEFORE the 6:32 PM Trump announcement — the post-ceasefire surge is NOT yet reflected.

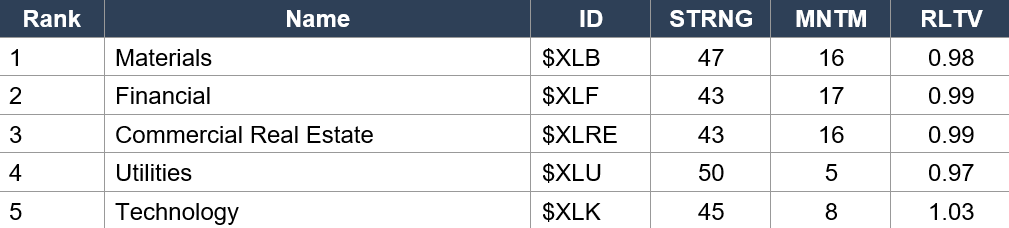

Sector ETFs — Top 5

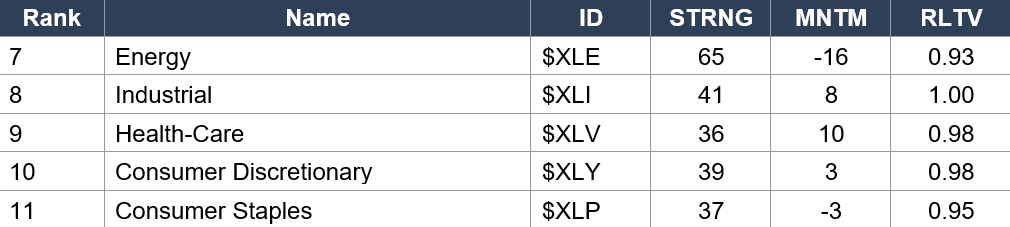

Sector ETFs — Bottom 5

Regime signal: The Energy collapse continues: Energy ($XLE rank 7, STRNG 65, MNTM −16, RLTV 0.93) holds the second-worst position in the data set with deeply negative momentum and sub-1.00 RLTV. After today’s −5.07% pre-market plunge with WTI crashing 17.5%, XLE will collapse further — the structural de-rating from rank 1 throughout most of the war to the bottom-third in three data sets is now complete. Materials ($XLB rank 1) and Financials ($XLF rank 2) have consolidated leadership. Tech ($XLK rank 5, RLTV 1.03) has the HIGHEST RLTV of any sector — the post-war duration trade is the cleanest signal in the data. Consumer Staples ($XLP rank 11, MNTM −3, RLTV 0.95) is now the WORST sector with the worst RLTV — the defensive unwind is complete. Watch tomorrow’s data for the post-ceasefire surge: XLB, XLF, XLK should see momentum acceleration; XLE should print near-zero RLTV.

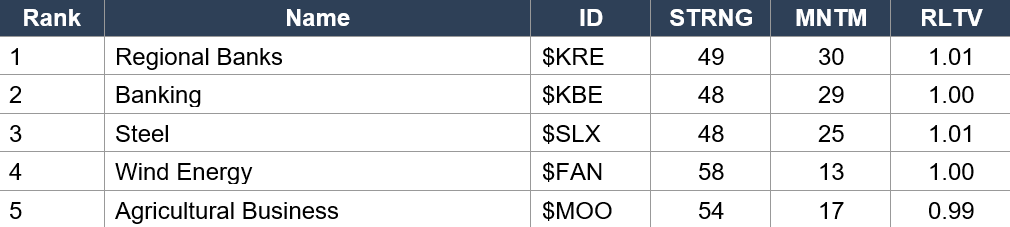

Industry ETFs — Top 5

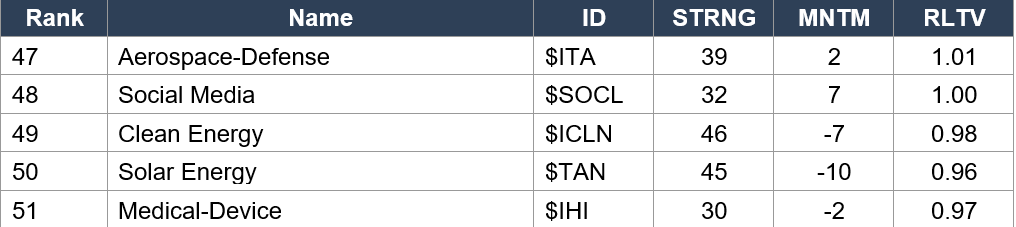

Industry ETFs — Bottom 5

Regime signal: Regional Banks ($KRE rank 1, MNTM 30) and Banking ($KBE rank 2, MNTM 29) have the highest momentum scores of any industry — momentum continues to accelerate as the post-war curve normalization reasserts. Steel ($SLX rank 3, MNTM 25) confirms Materials sector leadership at the industry level. Gold Miners ($GDX rank 8, MNTM 23, RLTV 1.06) have broken into the top 10 with rising momentum — gold’s Tuesday breakout is captured in the data. Cyber Security ($CIBR rank 11, MNTM 17, RLTV 1.03) has surged into the top quartile — the war demonstrated cyber vulnerabilities and the structural bid is real. CRITICAL: Aerospace-Defense ($ITA rank 47, MNTM 2, RLTV 1.01) is in the BOTTOM 5 — the deadline-event positioning unwind I documented yesterday is showing in the data. Today’s +3.34% pre-market bid will reverse this. Oil & Gas Exploration ($XOP rank 36, STRNG 67, MNTM −16, RLTV 0.93) confirms the energy industry de-rating. Alerian MLP ($AMLP rank 40, MNTM −10) — the worst momentum of the energy complex.

4. MORNING DATA REACTION

Quiet US data morning. The main event is FOMC Minutes (March meeting) at 2:00 PM — the day’s largest single-event risk for the cross-asset rally.

Powell’s Harvard speech already killed the rate-hike thesis. The minutes will reveal how unified the committee was on holding rates steady and how much oil-shock concern was discussed. A hawkish surprise (e.g., revealing that more members were leaning toward a rate hike before Powell’s pivot) could stall the equity rally and cause profit-taking in the dollar trade. A dovish confirmation extends the rally. The base case is that the minutes will be consistent with the Powell pivot already absorbed by the market — but the room for surprise is asymmetric given the +2.59% ES gap and the −2.89% USMV-SPHB factor print already pricing dovish-Fed-plus-de-escalation perfection.

This Week’s Data Recalibrated by the Ceasefire:

PCE February tomorrow (8:30 AM) is the Fed’s preferred inflation gauge but covers data BEFORE the war oil shock fully hit. Market consensus around +0.4% headline and +0.3% core MoM. Less market-moving now because the WTI crash is unwinding the inflation impulse the bond market was pricing.

CPI March Friday (8:30 AM) was scheduled to be ‘THE’ inflation test — the FIRST CPI to fully reflect the war-period oil shock. Pre-ceasefire street consensus around +0.9% MoM headline (Barclays) / +0.3% core. POST-CEASEFIRE this print matters considerably LESS than it would have 24 hours ago because (a) the WTI shock is unwinding, (b) Powell’s pivot is already priced, (c) the 30Y is back below 4.85% essentially at the pre-war baseline. The market will read a hot CPI as ‘backward-looking’ rather than predictive.

Michigan Sentiment Preliminary Friday — prior 53.3 with 3.8% inflation expectations. Watch the 1-year inflation expectations component for war pass-through and whether it begins to REVERSE on the ceasefire. A drop in inflation expectations would confirm the post-ceasefire reflation regime.

Last Week’s Data Arc Recapped Through the Ceasefire Lens:

ADP +62K, Retail Sales +0.6%, Claims 202K, NFP +178K with AHE cooling to 3.5% — the labor market resilience that allowed the bond market to price aggressive Fed easing. ISM Manufacturing 52.7 with Prices Paid 78.3 (war high) — the goods-side stagflation print that is now backward-looking. ISM Services 54.0 with Prices 70.7 / Employment 45.2 — the services-side stagflation print that is also now backward-looking. Both ISM Prices subcomponents will likely retreat in April’s data as the WTI crash flows through input costs over the next 4-6 weeks. The ‘data was constructive on top, structurally stagflationary underneath’ narrative gets reframed: the surface was right, the underneath is now obsolete.

5. THE DYRH READ

Regime: Post-Ceasefire Reflation Rally — WTI Crashes, Metals Explode, VIX Below 21, USMV-SPHB Deepest Risk-On of the War. The cleanest ‘regime reset’ pre-market of the entire conflict. Every cross-asset signal has gapped decisively in the de-escalation direction in unison. The ceasefire is two weeks, not permanent — but for today’s tape, the cross-asset confirmation is unanimous. Confidence: High.

Yield Curve: Bull Flattener — 2nd Consecutive Session, 50% Larger Magnitude.

All four tenors falling: 2Y −6.4 bps to 3.736% (new low), 5Y −7.4 bps to 3.864% (biggest tenor move), 10Y −6.5 bps to 4.236%, 30Y −4.0 bps to 4.838%. Front avg −6.9 bps vs long avg −5.25 bps = front falling more = flattener. All falling = bull. The 5Y leading at −7.4 bps is meaningful — the 5Y is the most rate-cut-sensitive part of the curve and the bond market is voting decisively for aggressive Fed easing now that the oil shock is unwinding. The 2Y at 3.736% is a meaningful new low. The 30Y at 4.838% is essentially BACK to the pre-war 4.843% baseline (cumulative −0.5 bps from baseline) — the long end has fully unwound the war’s term premium expansion in two sessions.

CRITICAL UNKNOWN: MOVE Index is showing the stale Tuesday close 83.1452 with no fresh Wednesday print yet — same situation as yesterday morning. The fresh MOVE print is the binary signal of the day. MOVE trajectory: 115.02 (Day 21 war high) → 111.95 → 108.33 → 96.05 → 90.19 → 84.41 → 81.78 → 81.68 → 83.15 (Day 28). The 8-session decline streak broke yesterday but only marginally and stayed below 85. If today’s fresh MOVE prints below 80, the bond crisis is functionally OVER and the rates-vol normalization is complete (matching VIX 20.76 on the equity side). If MOVE stays above 82, the bond market is reserving caution about the durability of the two-week ceasefire and Friday’s Islamabad negotiations.

WTI’s 24-Hour Range: $114.87 → $93.17 = −18.9% — One of the Largest Single-Day Crude Moves on Record.

Cumulative WTI move from the pre-war $67.02 baseline is now +$26.15 / +39.0% — a massive compression from yesterday morning’s +71.4% war high. In two trading days (Day 28 morning to Day 29 morning), WTI has moved from $114.87 to $93.17 = −$21.70 / −18.9%. Heating oil −15.22% and Brent −15.05% confirm the broad-based crude crash. RBOB at −11.11% is the day’s product standout — the gasoline futures crash will translate to retail prices over the coming weeks. The structural caveat from BofA’s Blanch and Eurasia Group remains valid: even with this crash, ‘the oil market is still extremely tight.’ Months are needed to repair Persian Gulf refinery damage and clear shipping backlogs, and Iran’s ‘technical limitations’ caveat on Hormuz transit means actual flows resume gradually. Don’t extrapolate the WTI crash into a sustained move toward pre-war $67. The price gap from $93 toward $67 will likely be slow to close even if the ceasefire holds.

Gold’s Yellow Flag Resolved — The Three-Session Forward-Looking Signal Validated.

Gold at $4,821.6 (+2.92%) extends Tuesday’s +1.64% breakout to a cumulative +4.6% over two sessions, fully resolving the three-session yellow flag from Day 27/28. The thesis from Day 28 close — that gold was pricing peace in advance through its three-session refusal to rally — is now FULLY VALIDATED. Gold was the smartest cross-asset signal in the war’s final 72 hours. The broad metals reflation across precious AND industrial confirms the regime is broadly de-escalating, not just isolated to oil. Palladium +10.87% is the standout — both reflation positioning AND a likely short squeeze in the metal that has been the most beaten-down through the war’s stagflation regime. Copper at +3.59% is the cleanest growth-positive read — the industrial metal responding to both the dollar collapse and the demand-recovery thesis.

USMV-SPHB at −2.89% — The Deepest Risk-On Factor Print of the War by 5x.

The factor tape’s −2.89% USMV-SPHB spread is the deepest risk-on print of the entire war by a wide margin. The prior Day 27 close print of −0.55% was the previous record. Today’s print is more than 5x deeper. SPHB (high beta) at +4.00% leads decisively. USMV at only +1.11% and SPLV at only +0.88% are the conspicuous laggards — defensive low-vol cohorts are barely bid in the broad reflation. MTUM (momentum) at +3.54% confirms positioning is unwinding from defensive momentum back to growth momentum. VLUE +3.07% catches the value bid as cyclicals re-rate. Mid Cap (IJH) +2.76% and Small Cap (IJR) +2.71% confirm the size factor reasserting (smaller = bigger pre-market gain). Three completely different factor regimes in three sessions: Monday’s deeply risk-on (−0.55%) → Tuesday’s defensive flip (+0.23%) → Wednesday’s deepest risk-on of the war (−2.89%). The whipsaw is extreme and positioning is now heavily one-directional.

XLE −5.07% Is The Only Red Sector — The Cleanest Possible Signal.

Energy is the ONLY S&P sector being unwound while every other sector is bid +1-4%. XLK leading at +3.93% confirms the broad reflation tech bid. XLY +3.62% (yesterday’s WORST sector at −1.16%) catches a major bid — the cyclical-consumer rate-cut trade is reasserting now that the oil shock is unwinding (lower gas prices = consumer relief). XLI +3.13% on broad cyclical bid. XLF +2.34%. XLB +2.04% catches the metals reflation. XLP at only +0.64% is the conspicuous laggard non-energy sector — yesterday’s worst sector is only modestly bid today, reflecting that the staples unwind from Monday’s stagflation barbell positioning is still working through. Three completely different sector regimes in three sessions: Monday’s stagflation barbell (defensives + energy bid) → Tuesday’s defensive flip (XLV/XLC/XLE only green) → Wednesday’s broad reflation cyclical (XLE only red). The post-Day 22 small-cap rate-cut trade is fully reasserted.

DXY Crash −1.22% to 98.465 — The Deepest Sub-100 Print of the War.

DXY at 98.465 is the deepest sub-100 print of the post-Day 22 period and a meaningful new low. The −1.22% single-session move is the largest single-day DXY decline since the start of the war and reflects three converging drivers: (1) the dovish-Fed thesis sustained, (2) the geopolitical risk premium fully unwinding, and (3) safe-haven dollar demand evaporating now that the war is paused. NZD at +2.44% leads G10 (highest-beta G10 currency in textbook risk-on print). AUD +1.71%, GBP +1.66%, CHF +1.45% (paradoxical strength), EUR +1.17%, JPY +1.11%. CAD at +0.36% is the laggard — held back by the WTI crash since Canadian heavy crude is highly correlated with WTI demand. BTC at $72,185 (+4.36%) confirms the high-beta tech-proxy regime — BTC has now moved from $68,545 (Tuesday pre) to $72,185 (Wednesday pre), a +5.3% two-session run.

6. THE GAME PLAN

Today’s Key Events: 2:00 PM FOMC MINUTES (the day’s largest single-event risk). Quiet US data morning. LEVI Strauss after close (first major retail/discretionary print of the war period). Friday begins formal US-Iran negotiations in Islamabad. THURSDAY — PCE February + Initial Jobless Claims. FRIDAY — CPI March + Michigan Sentiment Preliminary.

The Bull Case:

The ceasefire is HERE. Trump 6:32 PM Truth Social formal announcement. Iran SNSC formal acceptance. Hormuz reopening with technical limitations. Pakistan/Egypt/Turkey mediation succeeded. Formal negotiations begin Friday. WTI crashed −17.51% — the largest single-day move since April 2020. VIX below 21 for the first time since pre-Day 22 — equity vol normalization functionally complete. Metals exploded across precious AND industrial — broad reflation signal. USMV-SPHB at −2.89% (deepest risk-on of the war by 5x). 30Y essentially back to pre-war baseline. ES within striking distance of full recovery (+95% retraced). All G10 currencies strongly green vs USD. BTC at new highs $72,185. ALL Mag 7 green. SOXX +5.39% (cleanest semis broadening). Bull flattener 2nd consecutive session. ITA finally bid +3.34% (deadline-event positioning resolved, structural defense thesis reasserts). Cocoa +4.52% reversed Tuesday’s −7.05% (clean unwind signal). Powell’s pivot is already priced. PCE/CPI matter less now. The Quiggle data is about to undergo its biggest single-session reshuffling of the war as the post-ceasefire reflation captures into the rankings tomorrow.

The Bear Case:

THE CEASEFIRE IS TWO WEEKS, NOT PERMANENT. Iran SNSC explicitly noted ‘this does not signify the termination of the war.’ Iran will demand sanctions relief, US base withdrawal, frozen asset release, and continued nuclear enrichment. Friday’s Islamabad negotiations could break down within the first session. Any breakdown re-introduces $10-15 of risk premium overnight. The oil market is STILL physically tight per BofA’s Blanch — the WTI crash is repricing geopolitical risk premium, not supply-demand recovery. Persian Gulf refinery damage takes months. QatarEnergy: Ras Laffan LNG 17% offline, 3-5 year repair timeline. Israel and UAE sounded missile alerts shortly after the ceasefire announcement — not all combatants stood down. Israel CONTINUES Lebanon operations (contradicting Pakistan PM Sharif’s ceasefire-includes-Lebanon claim). The FOMC Minutes at 2 PM is the day’s largest single-event risk — a hawkish surprise could stall the entire rally. Positioning is heavily one-directional — USMV-SPHB at −2.89% is 5x deeper than the prior war record, and when positioning extends this far in one direction even small reversals can produce outsized counter-moves. AAPL weakness persists across regimes. Apple is the only Mag 7 still struggling and it’s now a multi-session pattern that may compound into Q2 earnings.

Regime: Post-Ceasefire Reflation Rally — The Cleanest Regime Reset of the Entire War. The bond market is pricing aggressive Fed easing AND ceasefire durability. The equity market is pricing full recovery within striking distance. The FX market is pricing dollar weakness on safe-haven demand evaporating. The metals market is pricing broad reflation. The oil market is repricing the geopolitical premium. Five different markets, five different stories, all pointing in the same direction for the first time since Day 1. The two-week ceasefire window holds the answer. Friday’s Islamabad negotiations are the next binary catalyst.

Watch List

2:00 PM FOMC MINUTES — the day’s largest single-event risk

Powell’s Harvard speech already killed the rate-hike thesis. The minutes will reveal committee unity and how much oil-shock concern dominated the discussion. A hawkish surprise (revealing more members leaning toward a hike before Powell’s pivot) could stall the rally and cause profit-taking. A dovish confirmation extends it. Given the +2.59% ES gap and the −2.89% USMV-SPHB factor print already pricing perfection, the room for surprise is asymmetrically negative.

Fresh MOVE print — bond-market confidence in the ceasefire

MOVE is showing the stale Tuesday 83.1452 carry. If the fresh print breaks below 80, the bond crisis is functionally OVER and matches VIX 20.76 on the equity side — full rates-vol normalization. If MOVE stays above 82, the bond market is reserving caution about the two-week window and Friday’s Islamabad negotiations. CNBC reported overnight 30Y yields fell 7 bps to 4.851% and 10Y fell 9 bps to 4.253% — the bond rally is broad and aggressive, consistent with MOVE compressing further.

Friday’s Islamabad negotiations — the next binary catalyst

Formal US-Iran negotiations begin Friday. Iran will demand sanctions relief, US base withdrawal, frozen asset release, and continued nuclear enrichment. The 10-point proposal Trump called ‘workable’ has not been published. Any breakdown in the first session would re-introduce $10-15 of WTI risk premium overnight. Position-sizing for risk-on into Friday should account for this binary.

LEVI Strauss after close — first retail/discretionary war-period print

Levi’s is a clean read on consumer spending under stagflation pressure. The Q1 results will cover most of the war period. Forward guidance is the key tell — if Levi’s commentary is constructive on Q2 demand recovery, the post-ceasefire reflation thesis gets corporate validation. If it’s defensive, the cyclical bid in XLY pre-market may be premature.

Israel-UAE missile alerts and Lebanon operations — incident risk

Israel and UAE both sounded missile alerts shortly after the ceasefire announcement — partial confirmation that not all combatants immediately stood down. Israel continues Lebanon operations (contradicting Pakistan PM Sharif). Any incident in Lebanon or any post-ceasefire missile attack against Israel/UAE/US assets re-introduces escalation risk.

VIX cash open — sub-20 print would confirm full equity vol reset

VIX at 20.76 pre is the first sub-21 print since pre-Day 22. If the cash session prints VIX below 20, the equity vol regime is functionally complete back to pre-war levels. The 20 threshold is now in clean play for the first time since the war began.

Morning check: Day 40. Ceasefire Day 1. Trump signed at 6:32 PM. Iran’s Supreme National Security Council accepted before midnight. Pakistan brokered it. Hormuz reopens with ‘technical limitations.’ WTI crashed $19.78 in a single overnight — the largest move since April 2020. The metals complex exploded across the board. VIX cracked below 21 for the first time since pre-Day 22. The 30Y yield is essentially back at the pre-war baseline. The factor tape printed −2.89% USMV-SPHB — five times deeper than any prior risk-on signal of the entire war. Every cross-asset signal gapped in the de-escalation direction in unison. ES within striking distance of full recovery — 95% retraced in 5 sessions. The cleanest regime reset of the entire conflict. And yet — the ceasefire is two weeks, not permanent. Iran says ‘this does not signify the termination of the war.’ Israel-UAE sounded missile alerts shortly after the announcement. Israel continues Lebanon operations. The oil market is still physically tight. The Persian Gulf refineries take months. The Ras Laffan LNG complex takes years. Friday’s Islamabad negotiations are the next binary. The FOMC Minutes at 2 PM are the day’s largest single-event risk. Position into the rally, but remember — the war is paused, not ended. The market is pricing perfection. Powell pivoted. Hormuz reopens. Cyclicals lead. Defensives lag. Everything that was working last week is unwinding; everything that was unwinding is working. The cleanest single-session regime reset of the entire war is happening in real time. Take the win. But hedge for Friday.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.