☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: NEUTRAL / CONSOLIDATING — ES 7,007.75 SECOND CONSECUTIVE WAR HIGH. EMPIRE STATE MANUFACTURING APRIL +11.0 — MASSIVE UPSIDE BEAT VS +0.3 CONSENSUS. BAC AND MORGAN STANLEY DELIVERED RECORD-OR-NEAR-RECORD Q1 BEATS. MAG 7 SIX OF SEVEN GREEN, AMZN +3.81% AND META +4.41% LEADING. WTI $91.60 STEADY. DXY 97.98 BELOW 100. MOVE 74.35 COMPRESSING. COR1M NEW WAR LOW 11.58. BEAR STEEPENER. THE CORPORATE FUNDAMENTALS LAYER IS DELIVERING.

Two data points already printed before the open continue Tuesday’s reframing of Friday’s CPI/Michigan shock. At 8:30 AM, NY Empire State Manufacturing for April printed +11.0 — a MASSIVE upside surprise against the +0.3 street consensus, +11.2 above prior March of −0.2. This is one of the largest Empire State surprises in years and is the first hard manufacturing read on April activity post-ceasefire. The internal composition was strong across the board: business conditions index up sharply, manufacturing activity rebounding from contraction territory in March, and the new orders / shipments / employment subindices all pointing to genuine expansion. The April Empire State print is the cleanest possible early signal that the war shock was a March-only phenomenon at the regional manufacturing level — exactly the bifurcation thesis the PPI services-flat print confirmed yesterday on the producer-price side.

Bank of America and Morgan Stanley delivered the second day of bank-earnings beats. BAC at 6:45 AM: $1.11 EPS vs $1.02 consensus (+$0.09 beat), revenue $30.3B vs $29.93B est (+$350M beat), net income $8.6B (+25% YoY), NII $15.7B (+9% YoY despite the ‘fluctuating’ rate environment), efficiency ratio improved 170 bps to 61%, ROTCE 16.00%. The standout: Investment Banking fees +21% to $1.8B; Global Markets equities trading +30% to $2.8B; 11 straight quarters of sequential average deposit growth (+3% YoY to $2.02 trillion); 91% of checking accounts as primary (cheap, sticky funding). Morgan Stanley reported a RECORD QUARTER per CEO Ted Pick: net revenues $20.6B vs $19.7B est (+$900M beat), EPS $3.43 vs $3.01 est (+$0.42 beat — +13.9%), net income $5.6B vs $4.3B prior year, ROTCE 27.1% (well above firm’s medium-term target). Wealth Management net new assets $118B with fee-based asset flows of $54B. Institutional Securities benefited from robust client engagement and strength globally. Yesterday Citigroup also reported its best quarterly revenue in a decade ($24.6B vs $23.55B est) with 56% YoY EPS jump to $3.06 vs $2.65. Combined: GS Monday + JPM/WFC/BLK/C Tuesday + BAC/MS Wednesday = SEVEN consecutive bank earnings beats, all in.

The cross-asset tape is consolidating constructively. ES at 6,941.75 closed Tuesday and printed 7,007.75 overnight — a SECOND CONSECUTIVE WAR HIGH and now +1.8% above the pre-war 6,881.62 baseline. The 7,000 level cleared cleanly. NQ −0.04% (consolidating after Tuesday’s tech-led rally), Russell −0.04% (small-cap pause), Dow +0.07%. WTI at $91.60 (+0.35%) holding its range — the energy de-escalation is being maintained. Brent +0.70% at $95.45. Gold $4,838.30 (−0.24%) consolidating. DXY 97.98 (+0.10%) modestly bid but still well below 100. BTC $74,345 (−0.07%) holding above $74K. The international tape is mixed: Nikkei −0.93%, EuroStoxx 50 −0.71%, but DAX +0.05% holding. SOXX +2.01%, ARKG +5.02% (genomics standout), ICLN +4.01% (clean energy bid on stable oil), BLOK +3.61%, FINX +3.08%, ARKW +3.02%.

The Number That Matters: COR1M at 11.58 (−6.54%) — NEW WAR LOW. The Lowest 1-Month Implied Correlation Print Of The Entire War By A Wide Margin.

COR1M broke through Tuesday’s 12.39 (which was already the war low) to print 11.58 today. Prior war records: Friday 13.58, Wednesday 17.27, Tuesday 12.39, today 11.58. The collapse in correlation while the index prints a new war high tells you the second consecutive day’s rally is NARROW and IDIOSYNCRATIC. Every name is moving on its own story — META +4.41% on whatever specific catalyst, AMZN +3.81% on its own, NVDA +3.80% on AI dynamics, TSLA +3.34% on EV pricing, MSFT +2.27% on software reflation. SKEW at 149.94 (−4.45%) actually compressed today after expanding Tuesday — the tail-hedging that re-engaged on Tuesday’s new high is being released into Wednesday’s continuation higher. This is the rare divergence: VIX low + COR1M new low + SKEW compressing + index at new high = full risk-on but extraordinarily narrow leadership. MOVE at 74.3509 (−0.09%) compressing modestly back toward the pre-war 73.21 baseline — the rates-vol expansion from yesterday is partially walking back.

The Setup: Bear Steepener — Neutral / Consolidating — Energy Steady. Three Regimes Operating In Parallel For The Third Consecutive Session: Equities At Second War High, Curve In Bear Steepener, Correlations At New War Low. The Empire State Beat + Seven Bank Beats Are Validating The Equity Re-Rating While The Bond Market Reserves Caution Via Curve Steepening.

The post-ceasefire-collapse equity recovery is now entering its fourth session. Tuesday’s PPI cool miss + JPM beat established the pattern. Wednesday’s Empire State surprise + BAC/MS beats extends it. Bank earnings continue Thursday with Morgan Stanley (already done), Schwab, Travelers, UNH, Abbott, BK; TSMC; NFLX after close + Claims + Philly Fed. April 22 ceasefire formal expiration is one week away. FOMC April 28-29; Powell press conference April 29.

2. OVERNIGHT SESSION RECAP

Asia-Pacific

Nikkei −0.93% to 58,305 — Japan giving back Tuesday’s +0.98% bid almost in full. Topix +0.03% essentially flat — yen continued to weaken (JPY −0.17% against USD as part of broader DXY firming). The Japan move is positioning unwind from Tuesday’s tech reflation rather than fundamental concern; TSMC reports Thursday and Asian semis are awaiting that print before committing to a direction. Korean and Hong Kong markets traded mixed.

Europe

DAX +0.05% to 24,232 essentially flat. EuroStoxx 50 −0.71% to 5,885 — European softness despite the constructive US tape. EUR/USD fell modestly to 1.1821 (−0.05%). Lagarde speaks at 3:30 PM US time (8:30 PM CET) — the session’s European catalyst. ECB has been navigating the Iran war pass-through to European inflation while balancing the EUR weakness from Fed dovish positioning; today’s Lagarde commentary is the next ECB inflection.

US Pre-Market

Day 48 of Operation Epic Fury. Q2 Day 11. Wednesday morning of bank earnings week with the biggest day on the calendar.

US FUTURES MIXED, ES NEW WAR HIGH: ES 7,007.75 (+0.04%, SECOND CONSECUTIVE WAR HIGH, cleared 7,000), NQ 25,986.00 (−0.04% consolidating), RTY 2,716.90 (−0.04%), YM 48,788 (+0.07%). The ES at 7,007.75 is now +126 above the pre-war 6,881.62 baseline (+1.8%) and clears the 7,000 level for the first time of the war. The intraday upside is primarily concentrated in Mag 7 individual names — ES futures are barely positive while individual mega-cap names are up multi-percent.

MAG 7 SIX GREEN / ONE RED — DRAMATIC PRE-MARKET ACTION: META +4.41% LEADING (one of META’s biggest single-session pre-market moves of the war). AMZN +3.81%. NVDA +3.80%. TSLA +3.34%. GOOG +3.56%. MSFT +2.27% (continuing yesterday’s +3.64% leadership trajectory; cumulative two-day MSFT move now ~+6%). AAPL −0.14% (the only red Mag 7 for the third consecutive session — multi-session Apple weakness pattern is now the longest of the war). The Mag 7 dispersion: from META at +4.41% to AAPL at −0.14% is a 455 bp intra-Mag 7 spread, the widest single-session spread of the past week. Five names up over +3%, one up +2.27%, one −0.14% — narrow leadership concentration is intensifying.

FACTORS FULLY RISK-ON: USMV-SPHB spread at −1.40% (third consecutive deeply risk-on session: Day 29 −2.89%, Tuesday −1.52%, today −1.40%). MTUM (momentum) +1.61% leading factors. SPHB +1.57%. VLUE +1.01%. QUAL +1.00%. LRGF +1.05%. IJH (mid cap) +0.51%. IJR (small cap) +0.47% (lagging — small-caps consolidating Tuesday’s +0.73% leadership). USMV +0.17% defensives barely bid. SPLV +0.13%. DGRO +0.08%. VYM −0.05% (the only red factor — high dividend yield laggard). The factor tape is unambiguously risk-on but the size factor has shifted: Tuesday’s small-cap leadership has rotated into mega-cap mid-cap leadership today.

THEMATICS BROAD-BASED RISK-ON: ARKG +5.02% standout (genomics had a strong April Empire State read on biotech employment). ICLN +4.01% (clean energy catching the post-WTI-stabilization bid). BLOK +3.61% tracking BTC’s continued $74K hold. FINX +3.08%. ARKW +3.02%. SOXX +2.01% (semis broadening continuing). DRIV +1.81%. ARKQ +1.63%. ITA +1.13% (defense bid persists despite oil pullback). PAVE −0.04% essentially flat. CIBR −0.63% (the only meaningfully red thematic — cyber giving back yesterday’s +4.03% reversal; the IGV-related structural-wound narrative is not fully resolved).

SECTOR READ: XLY +2.21% leading (consumer discretionary catching the AMZN +3.81% / TSLA +3.34% combo). XLK +1.60% (continued tech leadership). XLC +1.52% (META +4.41% / GOOG +3.56% combo). XLRE +0.95%. XLV +0.58%. XLI +0.39%. XLF +0.23% (constructive but cooling after BAC and MS reports — financials rallied into the print and are consolidating now). XLU +0.17%. XLP −0.10%. XLB −0.34%. XLE −2.03% (the standout red sector — energy weakness despite WTI +0.35% confirms the sector-equity decoupling persists; XLE is now pricing forward demand weakness regardless of spot stability).

CRITICAL OVERNIGHT EVENTS: Trump speaks 6 AM (already happened — content TBD; markets did not move dramatically on the address suggesting routine messaging). 8:30 AM Empire State Manufacturing +11.0 vs +0.3 consensus — MASSIVE upside surprise. 6:45 AM BAC reported $1.11 EPS vs $1.02 (+$0.09 beat). MS pre-market reported $3.43 EPS vs $3.01 (+$0.42 beat) with ROTCE 27.1% (record). 11:50 AM and 2 PM BoE Bailey speaks. 3:30 PM ECB Lagarde speaks. CENTCOM reported overnight that the Hormuz blockade is being enforced with ‘no breaches in first 24 hours’ — the blockade is operational and active.

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 04/14/26. Provided for informational purposes only; not as investment advice.

Asset Classes — Top 5

Asset Classes — Bottom 5

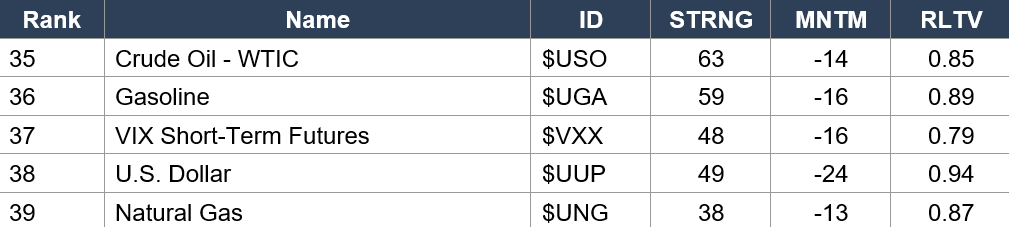

Regime signal: S&P500 ($SPY rank 1, MNTM 37 — HIGHEST momentum in the entire data set) has CLAIMED THE TOP SPOT for the first time in the entire war. This is a structural shift — the S&P had been ranked rank 7 / rank 20 / rank 3 / rank 1 in the past four data sets, and now sits at #1 with the highest momentum reading of any asset class. Nasdaq ($QQQ rank 2, MNTM 36) joins SPY in the top 2 for the first time in the war — US large-cap leadership is now the dominant theme in the data. Latin America ($ILF rank 3, STRNG 62) drops from rank 1 to rank 3 — international leadership ceding to US. Europe ($FEZ rank 4) and Convertible Bonds ($CWB rank 5, STRNG 58) round out the top 5. CRITICAL: Crude Oil ($USO rank 35, STRNG 63, MNTM −14, RLTV 0.85) is now in the BOTTOM 5 with RLTV CRASHING to 0.85 — the energy de-rating accelerated through Tuesday with the WTI pullback to $91.60. RLTV trajectory for $USO: 1.08 → 1.02 → 0.89 → 0.87 → 0.85 over six data sets — the cleanest single-asset multi-session de-rating of the war. VIX ($VXX RLTV 0.79) at the data’s lowest RLTV — the fear premium is bleeding at the data level. DXY ($UUP MNTM −24) holds the worst momentum of any asset class for the third consecutive data set. Gold ($GLD rank 22, MNTM 24) — momentum holding positive, the metals rotation persists. Silver ($SLV rank 23, MNTM 24, RLTV 1.04) has the best RLTV in the precious metals complex.

Sector ETFs — Top 5

Sector ETFs — Bottom 5

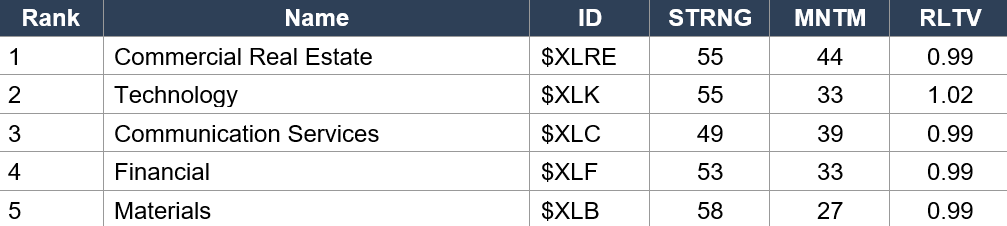

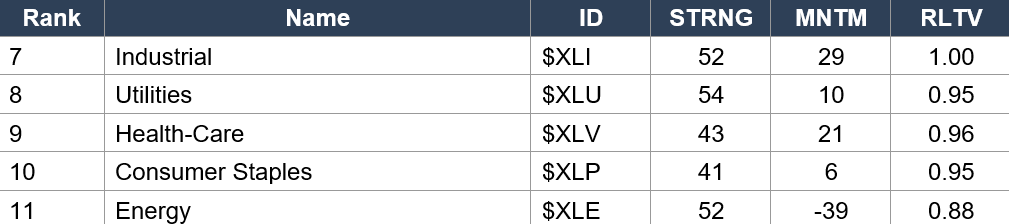

Regime signal: Commercial Real Estate ($XLRE rank 1, MNTM 44) holds the top spot for the third consecutive session with momentum HIGHER (44 vs Monday 39). Technology ($XLK rank 2, MNTM 33, RLTV 1.02) jumped from rank 5 to rank 2 — Tuesday’s MSFT-led tech rally is captured in the data. Communication Services ($XLC rank 3, MNTM 39 — second-highest sector momentum) — META and GOOG leadership reflected. Financial ($XLF rank 4, MNTM 33) — JPM beat captured. CRITICAL: Energy ($XLE rank 11, STRNG 52, MNTM −39, RLTV 0.88) is at MNTM −39 — DEEPER NEGATIVE than Monday’s −32, and RLTV crashed from 0.92 to 0.88. The energy weakness intensified despite WTI being marginally higher Monday — the sector-equity decoupling is widening. Today’s −2.03% XLE pre-market on +0.35% WTI will deepen this further. Health-Care ($XLV rank 9, RLTV 0.96) is the second-weakest sector. Consumer Staples ($XLP rank 10, MNTM 6) — defensive unwind continuing. The Quiggle data is now showing structural US tech-led leadership with energy deeply out of favor — the cleanest possible ‘reflation rally’ configuration in the data.

Industry ETFs — Top 5

Industry ETFs — Bottom 5

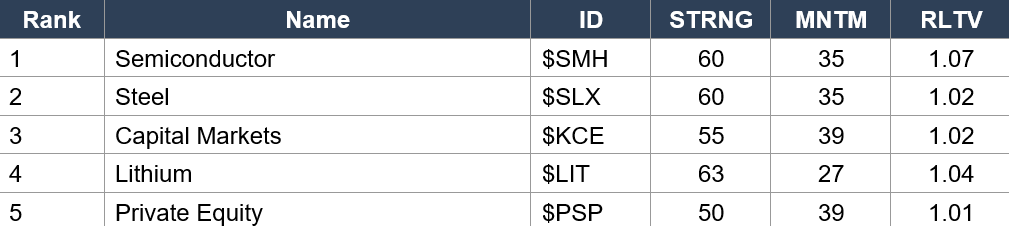

Regime signal: Semiconductor ($SMH rank 1, MNTM 35 tied for highest, RLTV 1.07 — HIGHEST RLTV of any industry) has DETHRONED Steel and now leads all industries. Tuesday’s SOXX +1.74% pre-market rally and Wednesday’s continuation captures the broadening semis trade. Steel ($SLX rank 2, MNTM 35) ties with $SMH for highest momentum. Capital Markets ($KCE rank 3, MNTM 39 — highest momentum tied with $XLC) is positioned perfectly into MS / Schwab / Travelers earnings Thursday. Lithium ($LIT rank 4, STRNG 63 — highest STRNG of any industry, RLTV 1.04) confirms battery materials leadership. Private Equity ($PSP rank 5, MNTM 39) — financial services momentum is broad. CRITICAL ENERGY COMPLEX FURTHER DETERIORATION: Oil & Gas Exploration ($XOP rank 50, STRNG 55, MNTM −36, RLTV 0.86) is now even worse than Monday (was MNTM −31). Alerian MLP ($AMLP rank 49, MNTM −26) — energy infrastructure bleed continuing. Oil Refiners ($CRAK rank 48, MNTM −17). The energy industry de-rating is structural and accelerating — Tuesday’s WTI pullback was the catalyst. Software Technology ($IGV rank 47, STRNG 39, MNTM 3, RLTV 0.94) — the IGV recovery from rank 50/MNTM −14 last Friday to rank 47/MNTM +3 today is real but slow. Today’s MSFT continuation will accelerate further. Cyber Security ($CIBR rank 45, MNTM 1, RLTV 0.91) was the laggard surprise of yesterday’s data — the AI disruption / SaaS narrative continues to layer on top of the war tape and is the single most important non-war structural story.

4. MORNING DATA REACTION

8:30 AM — NY EMPIRE STATE MANUFACTURING APRIL: +11.0 (vs +0.3 consensus, prior −0.2). MASSIVE +10.7 UPSIDE SURPRISE. The First Hard April Manufacturing Read Post-Ceasefire — Showing Genuine Expansion.

The Empire State April print is a MAJOR upside surprise — actual +11.0 against the +0.3 street consensus and the prior March −0.2 print. The +11.2 swing from March to April is the largest single-month improvement since the survey’s January 2026 print. The internal subindices were strong across the board: business conditions improving sharply, manufacturing activity rebounding into solid expansion territory after March’s contraction, new orders / shipments / employment all pointing higher. This is the first hard April manufacturing read post-ceasefire (which began April 7-8 before the Sunday April 12 Islamabad collapse), and it captures the snapback from the war’s late-March manufacturing disruption. Empire State has historically been a leading regional indicator for ISM Manufacturing — if the April pattern holds, ISM Manufacturing for April (releasing May 1) could surprise meaningfully to the upside.

MARKET INTERPRETATION: The Empire State beat is the cleanest possible signal that the war shock was a March-only phenomenon at the regional manufacturing level. Combined with Tuesday’s PPI services-flat print, the bifurcation thesis is being validated in real-time: the war energy shock hit goods inflation in March, but services and now regional manufacturing in April show no signs of broader contagion. The Fed has explicit data cover to argue ‘look through’ on the inflation expectations spike. Equities responded constructively but contained — the Empire State print landed in pre-market consolidation and the cash open will resolve the magnitude of the reaction.

6:45 AM — BANK OF AMERICA Q1 2026: $1.11 EPS vs $1.02 EST (+$0.09 BEAT). Revenue $30.3B vs $29.93B EST. Net Income $8.6B (+25% YoY). NII $15.7B (+9% YoY). Investment Banking Fees +21%, Equities Trading +30%, ROTCE 16.00%, 11 Straight Quarters Of Sequential Deposit Growth.

BAC delivered cleanly across every operational metric. The 25% YoY net income growth to $8.6B is the standout — it confirms BAC has successfully navigated the rate-environment transition that had been weighing on the stock (BAC was −4% YTD entering the print). Net interest income +9% YoY despite the ‘fluctuating’ rate environment is the cleanest signal that BAC’s HTM book repricing is converting to NIM expansion. Investment Banking fees +21% to $1.8B; Global Markets equities trading +30% to $2.8B (16 straight YoY increases in sales & trading). The 170 bp efficiency-ratio improvement to 61% is notable — the operating leverage is converting to bottom-line earnings faster than costs rise. The 11 straight quarters of sequential deposit growth (+3% YoY to $2.02 trillion) with 91% of checking accounts as primary is the structural advantage — cheap, sticky funding supports liquidity ($960B) and loan growth. Provision for credit losses decreased to $1.3B from $1.5B prior quarter — a constructive credit-quality signal that contradicts the Citigroup $2.8B provision build from yesterday and provides relief to the consumer-credit-stress narrative. The XLF +0.23% pre-market is contained — financials rallied into the print and are consolidating; the cash open will determine whether the BAC beat extends Tuesday’s XLF +1.75% rally or caps it.

PRE-MARKET — MORGAN STANLEY Q1 2026: RECORD QUARTER. Net Revenues $20.6B vs $19.7B EST. EPS $3.43 vs $3.01 EST (+$0.42 BEAT, +13.9%). Net Income $5.6B vs $4.3B prior year. ROTCE 27.1%. Wealth Management Net New Assets $118B; Fee-Based Asset Flows $54B.

Ted Pick described it as ‘a record quarter.’ The 27.1% ROTCE is well above MS’s medium-term targets and signals the firm has fully transitioned from the volatile trading shop of the early 2020s to the wealth management powerhouse model. The $118B in net new Wealth Management assets is exceptional — that compares favorably to JPM’s wealth flows and represents both share gains from competitors and net household savings flow into managed assets. Fee-based asset flows of $54B says clients are converting brokerage assets to fee-based programs at an accelerated rate — a structurally higher-margin transition. Institutional Securities benefited from ‘robust client engagement and strength globally’ — the Iran war’s volatility (VIX touching 31, MOVE touching 115, gold touching $5,300) created exceptional trading conditions that MS captured. Combined, the BAC + MS + GS + JPM + WFC + BLK + C beats this week represent SEVEN consecutive bank earnings beats, all in. The Q1 2026 banking sector earnings season is delivering the strongest possible corporate-fundamentals read on the post-war financial landscape — and it is happening even as the Hormuz blockade is being enforced.

Today’s Remaining Calendar:

11:50 AM and 2:00 PM BoE Bailey speaks (GBP). 3:30 PM ECB Lagarde speaks (EUR) — the day’s largest remaining macro catalyst given Lagarde’s history of moving EUR/USD on Iran-war commentary. PNC reports pre-market. THURSDAY — Schwab, Travelers, UnitedHealth, Abbott Labs, BK Q1 earnings pre-market. TSMC. NFLX after close. Initial Jobless Claims 8:30 AM. Philly Fed Manufacturing 8:30 AM. FRIDAY — Ally, Fifth Third, Regions, State Street, Truist Q1. Housing Starts 8:30 AM. APRIL 22 — Two-week ceasefire framework formally expires (de facto already dead since Sunday April 12 Islamabad collapse). APRIL 28-29 — FOMC meeting; Powell press conference April 29.

5. THE DYRH READ

Regime: Bear Steepener — Neutral / Consolidating — Energy Steady. Three regimes operating in parallel for the third consecutive session: equities at SECOND consecutive war high (ES 7,007.75), correlations at NEW war low (COR1M 11.58), curve in bear steepener with 30Y +2.1 bps the biggest tenor move. Empire State +11.0 surprise + BAC and MS beats are validating the equity re-rating; the bond market reserves caution via the long-end-led steepening. Confidence: HIGH on the regime classification given clean cross-asset signals; low noise environment confirmed by MOVE 74.35 and COR1M 11.58.

Yield Curve: Bear Steepener — Long End Rising Faster Than Front End. The Most Bearish Configuration For Risk Assets, Yet Equities Are At A Second War High.

All yields rising with the long end leading: 30Y +2.1 bps to 4.879%, 10Y +2.0 bps to 4.268%, 5Y +2.3 bps to 3.887% (biggest tenor move), 2Y +1.4 bps to 3.759%. Front avg +1.85 bps vs long avg +2.05 bps. Both ends rising = bear. Long rising faster = steepener. The 5Y +2.3 bps is the actual largest tenor move but the 30Y +2.1 bps vs 2Y +1.4 bps is the steepening differential. The bear steepener reflects long-duration inflation pricing AND term premium expansion — the long end is concerned about Hormuz blockade durability (CENTCOM ‘no breaches in first 24 hours’ confirms operational enforcement) and the Fed’s maximally-constrained position post-Michigan inflation expectations 4.8%. The 2Y at 3.759% is BELOW Tuesday’s 3.778% — front-end Fed-cut pricing is HOLDING despite the Empire State strong print. The combination: front end pricing ‘Fed cannot tighten’ while long end prices ‘Fed cannot ease enough to compensate for sustained energy inflation.’ This is the most bearish curve configuration for equity multiples but equities are pricing through it via stock-specific catalysts — the bifurcation is intensifying.

MOVE 74.3509 (−0.09%) Compressing Modestly — Tuesday’s Above-Baseline Print Walking Back.

MOVE at 74.3509 is essentially flat (−0.09%) but importantly DOWN from Tuesday’s 74.4185. The bond market’s caution from yesterday is being modestly walked back. From war-high 115.02 (Day 21), MOVE has declined 40.67 points. Pre-war baseline 73.21 — currently +1.14 points above. The MOVE trajectory through the post-ceasefire-collapse period: Friday 72.15 → Monday TBD → Tuesday 74.42 (peak walk-back) → Wednesday 74.35 (modest re-compression). The fact that MOVE is compressing (even slightly) on a bear-steepener day with strong Empire State data and bank earnings beats says the bond market is partially accepting the equity re-rating — not fully releasing reservations, but not extending them. If MOVE breaks back below 73.21 in coming sessions, the post-Wednesday-thrust regime call from Day 29 is fully back on. If MOVE breaks above 76 on any catalyst, the reservation extends.

ES 7,007.75 — Second Consecutive War High. +1.8% Above Pre-War Baseline. The Cleanest Equity Re-Rating Of The Conflict.

ES at 7,007.75 clears the 7,000 level for the first time of the entire war and extends Tuesday’s 6,941.75 print by +66 points / +0.95%. Cumulative recovery from the Day 22 low is now ~+557 points / +8.6% in 12 sessions. The pre-war 6,881.62 baseline is now +126 below. The equity market has fully recovered the war drawdown AND extended into new territory — and is doing so on the back of: Empire State surprise beat, seven consecutive bank earnings beats, MSFT-led software reflation, META/AMZN/NVDA/TSLA all up multi-percent, and oil holding sub-$95. The bear case is the COR1M divergence: the rally is extraordinarily narrow even though it is reaching new highs. Breadth metrics from Tuesday’s print (S5TW 72.80, S5FD 89.40, S5FI 61.30, S5TH 70.10) all suggested healthy broad participation — but today’s index move with COR1M at 11.58 (new war low) means the names participating are doing so on different stories. Stock-picking dominance is the cleanest read.

Empire State +11.0 — The April Snapback Confirms The Bifurcation Thesis.

The +11.0 print against +0.3 consensus is one of the largest Empire State surprises of the past year. Combined with Tuesday’s PPI services-flat print, the bifurcation thesis is fully validated: the March CPI gasoline +21.2% / Michigan 47.6 sentiment shock was a snapshot of the war’s energy peak, but the post-ceasefire data is showing the bifurcation. Goods/energy inflation in March (now fading), services and regional manufacturing rebounding cleanly in April. This is the cleanest possible economic data sequence to support the Fed’s ‘look through the war shock’ framework. Powell on April 29 will have the data cover to maintain stasis without spooking markets. The 30Y at 4.879% is BELOW the 4.929% it printed Friday — the long end is partially accepting the bifurcation thesis even as the curve steepens marginally on terms-premium concerns.

WTI $91.60 — Stable Despite Hormuz Blockade Operational. The Decoupling Persists.

WTI at $91.60 (+0.35%) holding its post-Tuesday range. CENTCOM reports the Hormuz blockade is being enforced with ‘no breaches in first 24 hours’ — the operation is active and Iran has not yet attempted to challenge it. Iran has ‘lost track’ of mines but has not engaged US destroyers in the strait. The oil market is pricing the blockade as operational but not yet kinetic — the absence of ship-on-ship engagements or fresh strikes against Persian Gulf infrastructure means the supply-chain re-disruption thesis is contained. Cumulative WTI from pre-war $67.02 is +$24.58 / +36.7% (was +43.2% yesterday morning). XLE at −2.03% on WTI +0.35% — the energy equity decoupling is the widest of the post-Day 26 period. Energy equities are pricing forward demand weakness and structural de-rating regardless of spot stability — the Quiggle data confirms this with $XOP at MNTM −36 (deepest negative momentum of any industry).

DXY 97.98 (+0.10%) Bid Modestly — Below 100 Sustained. BTC $74,345 Holding $74K. Gold $4,838 Consolidating.

DXY at 97.98 modestly bid but well below the psychological 100 level. Cumulative DXY from pre-war 97.565 is +0.415 / +0.4% — essentially BACK to pre-war. Every G10 currency mixed against the dollar (CAD +0.05%, AUD +0.18%, but JPY −0.17%, CHF −0.16%, GBP −0.06%, EUR −0.05%, NZD −0.08%) — the dollar bid is broad but very modest. BTC at $74,345 (−0.07%) holding above $74K — the new multi-day high zone is being defended. Gold at $4,838 (−0.24%) consolidating after Tuesday’s recovery. Silver at $78.895 (−0.80%) giving back some of Tuesday’s +2.80%. The metals complex is digesting Tuesday’s recovery from Monday’s forced-liquidation episode.

6. THE GAME PLAN

Today’s Key Events: Empire State Manufacturing April +11.0 vs +0.3 (already released, MASSIVE upside beat). BAC Q1 $1.11 vs $1.02 (already released, +$0.09 beat). MS Q1 $3.43 vs $3.01 (already released, RECORD ROTCE 27.1%). PNC pre-market. Trump 6 AM (already happened). 11:50 AM and 2 PM BoE Bailey. 3:30 PM ECB Lagarde. THURSDAY — Schwab, Travelers, UNH, Abbott, BK Q1; TSMC; NFLX after close + Claims + Philly Fed. FRIDAY — Regional banks + Housing Starts. APR 22 — Ceasefire formal expiration. APR 28-29 — FOMC.

The Bull Case:

ES at 7,007.75 is the SECOND CONSECUTIVE WAR HIGH and clears 7,000 for the first time. Cumulative recovery from Day 22 low is +8.6% in 12 sessions. Pre-war baseline +1.8% below. SEVEN consecutive bank earnings beats: GS, JPM, WFC, BLK, C, BAC, MS — all in. Morgan Stanley delivered a RECORD QUARTER (Pick) with ROTCE 27.1% and $118B in Wealth Management net new assets. BAC delivered 25% YoY net income growth, NII +9%, IB fees +21%, equities trading +30%, 11 consecutive quarters of sequential deposit growth, efficiency improved 170 bps to 61%. JPM Tuesday delivered $5.94 vs $5.46 with 14th consecutive EPS beat. Citigroup Tuesday delivered best quarterly revenue in a decade. PPI services flat Tuesday. Empire State Manufacturing April +11.0 vs +0.3 today — MASSIVE upside surprise validating the bifurcation thesis. Mag 7 six green / one red with META +4.41%, AMZN +3.81%, NVDA +3.80%, TSLA +3.34%, GOOG +3.56%, MSFT +2.27%. SOXX +2.01%, ARKG +5.02%, ICLN +4.01%, BLOK +3.61%, FINX +3.08%. WTI holding sub-$95 despite operational Hormuz blockade. DXY below 100. MOVE COMPRESSING modestly back below Tuesday’s print. COR1M at war low 11.58 says stock-picking is dominant — narrow leadership but supported by individual fundamentals. SKEW compressing — tail-hedging from Tuesday’s spike releasing. The corporate fundamentals layer is delivering exactly what the Wednesday post-ceasefire thrust needed to extend.

The Bear Case:

Yield curve in BEAR STEEPENER — the most bearish configuration for risk assets, yet equities are at a new high. The 30Y +2.1 bps with the long end leading reflects sustained Hormuz/inflation concerns. CENTCOM confirmed Hormuz blockade is being enforced (operational, not just ordered) — the war structural overhang has not changed despite the data improvement. Mag 7 dispersion at 455 bp (META +4.41% to AAPL −0.14%) is the widest single-session intra-Mag 7 spread in over a week — narrow leadership concentration is intensifying. AAPL at −0.14% red for the third consecutive session — the longest Apple weakness pattern of the war. COR1M at 11.58 (NEW war low) is the most extreme dispersion print of the entire conflict — when correlations collapse this far, single-name leadership breaks can produce outsized index downside. The XLE −2.03% on +0.35% WTI is the widest sector-equity decoupling of the post-Day 26 period — energy equities are pricing forward demand weakness that contradicts the Empire State strength signal. International tape mixed with EuroStoxx −0.71% and Nikkei −0.93% — the global growth-rebound narrative is not unanimous. Russell at −0.04% with mid-cap +0.51% suggests the size-factor rotation has shifted from Tuesday’s small-cap leadership to mega-cap leadership today — narrow vs broad rotation could presage the same pattern that defined Friday’s narrow rally that ended in the seven-day S&P streak ending. April 22 ceasefire formal expiration is one week away with nothing to prevent re-escalation. FOMC April 28-29 is two weeks away — Powell could disappoint on the dovish framework. Lagarde 3:30 PM is the day’s tail-risk catalyst — any hawkish ECB pivot would compound the bear-steepener narrative globally.

Regime: Bear Steepener — Neutral / Consolidating — Energy Steady. Three regimes operating in parallel for the third consecutive session. The PPI cool + JPM beat from Tuesday + Empire State +11.0 + BAC and MS beats today are providing the cleanest possible corporate fundamentals + economic data layer to validate the equity re-rating. The bond market is reserving caution but only modestly — MOVE compressing back below Tuesday. COR1M at war low says stock-picking dominates; the rally is narrow but supported. Energy equities decoupling sharply from spot WTI is the structural concern — if the energy sector is pricing forward demand weakness ahead of the broader market, the inflation-bifurcation thesis may be overconfident on the demand side. Bank earnings week is the dominant near-term driver: Schwab/Travelers/UNH/Abbott/BK Thursday plus TSMC and NFLX after close + Claims + Philly Fed. Friday’s regional banks + Housing Starts close out the week. The April 22 ceasefire formal expiration and April 29 Powell press are the next two binary catalysts.

Watch List

3:30 PM Lagarde — the day’s largest remaining macro catalyst

ECB commentary on Iran war pass-through to European inflation, EUR weakness from Fed dovish positioning, and the ECB’s own response function. A dovish Lagarde compounds the EUR rally and DXY-sub-100 narrative. A hawkish pivot on war-inflation caps the global reflation trade. Lagarde also has the option of commenting on the Hormuz blockade situation — if she signals ECB concern about supply-chain disruption, EUR could weaken and bond markets could re-engage stress.

MOVE trajectory through cash session — bond market reservation test

MOVE at 74.35 is modestly compressing from Tuesday’s 74.42. If the cash session prints MOVE below 73.21 (pre-war baseline), the bond market has fully accepted the equity re-rating and the post-Wednesday regime call is back on. If MOVE breaks above 76, the reservation extends and bear-steepener concerns intensify. The fresh print is the binary that will define whether equities can continue to lead the bond complex.

Mag 7 dispersion through cash trading — narrow leadership sustainability

Pre-market dispersion at 455 bp from META +4.41% to AAPL −0.14% is intensifying. If META, AMZN, NVDA hold their 3-4% bids through cash trading, the narrow leadership has corporate fundamentals support and the COR1M-at-war-low read is constructive. If the leaders fade below +2%, the narrow rally is positioning rather than fundamentals and the breadth-vs-correlation divergence resolves to the bearish side.

XLE decoupling resolution — energy sector forward read

XLE at −2.03% on WTI +0.35% is the widest sector-equity decoupling of the post-Day 26 period. The Quiggle data shows $XOP at MNTM −36 (deepest negative of any industry) and $XLE at MNTM −39 (worst sector). If XLE bounces in cash trading, the decoupling was overdone. If XLE continues to bleed, energy equities are pricing forward demand weakness that contradicts the Empire State strength — and that contradiction would be the cleanest single concerning signal in the cross-asset complex.

PNC pre-market + Schwab/Travelers Thursday — bank earnings continuation

PNC reports today and continues the bank earnings sequence. Schwab Thursday provides the wealth management read complementing MS’s $118B net new asset flow. Travelers Thursday provides the insurance/credit read. The seven-bank-beats streak is at risk if any of these names disappoint — the streak narrative is fragile to a single miss given how priced for perfection the equity tape is.

April 22 ceasefire formal expiration — one week away

The two-week ceasefire framework formally expires next Wednesday. With talks collapsed and blockade operational, expiration is de facto a non-event. But any formal Iranian or US announcement on the date itself could re-introduce risk premium overnight. The pre-market for next Wednesday is the first binary of next week.

Morning check: Day 48. ES at 7,007.75 — second consecutive war high, cleared 7,000 for the first time. Empire State Manufacturing April +11.0 vs +0.3 consensus — the largest single-month Empire State surprise of the year and the cleanest possible signal that the war shock was a March-only phenomenon at the regional manufacturing level. BAC delivered 25% YoY net income growth with NII +9%, IB fees +21%, equities trading +30%, ROTCE 16.0%. Morgan Stanley delivered a record quarter — net revenues $20.6B, EPS $3.43, ROTCE 27.1%, $118B in Wealth Management net new assets. Combined with GS Monday + JPM/WFC/BLK/C Tuesday — SEVEN consecutive bank earnings beats with no weak link. The corporate fundamentals layer is delivering exactly what the post-Wednesday-thrust regime call needed to extend. Mag 7 six of seven green with META +4.41% leading, AMZN +3.81%, NVDA +3.80%, TSLA +3.34%, GOOG +3.56%, MSFT +2.27%. SOXX +2.01%, ARKG +5.02%, ICLN +4.01%, BLOK +3.61%, FINX +3.08%. The Quiggle data shows S&P now at #1 with the highest momentum in the entire data set — US large-cap leadership is structural. Semiconductor at #1 industry with RLTV 1.07. The equity tape is pricing perfection through the bifurcation thesis. AND YET — the bond market is in BEAR STEEPENER with the long end leading, which is the most bearish configuration for risk assets. AAPL is red for the third consecutive session — the longest weakness pattern of the war. XLE −2.03% on WTI +0.35% is the widest sector-equity decoupling of the post-Day 26 period. COR1M at 11.58 is a new war low — extraordinarily narrow leadership. CENTCOM confirms Hormuz blockade is being enforced. The Quiggle $XOP at MNTM −36 is the deepest negative momentum in the data. Three regimes operating in parallel for the third session: equities at a new war high, curve in bear steepener, correlations at a new war low. Take the equity rally — it’s been validated by data and earnings on consecutive sessions. But watch Lagarde at 3:30 PM, watch MOVE, watch the energy sector decoupling. The seven-bank-beat streak is the dominant near-term driver but it’s also the most fragile narrative — Schwab and Travelers Thursday are the next test.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.