☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: RISK-ON DESPITE RATES CRISIS. ES 7,263.00 (+0.45%). MOVE EXPLODED TO 77.86 (+10.58%) — NOW 4.65 POINTS ABOVE THE 73.21 BASELINE. THE 30Y CROSSED 5.005% — THE DAY 22 CRISIS THRESHOLD BREACHED FOR THE FIRST TIME SINCE MARCH. AND YET THE EQUITY MARKET IS RALLYING. NQ +0.75%. RUSSELL +0.81% OUTPERFORMING. DAX +1.38%. NIKKEI +1.07%. WTI $102.96 (−3.25%) PULLING BACK — OIL RELIEF PROVIDING THE COUNTERWEIGHT TO THE RATES STRESS. BULL FLATTENER — ALL YIELDS FALLING. GOLD +1.05% RALLYING — HAVEN DEMAND RETURNING. BTC $81,670 (+1.59%). ISM SERVICES + JOLTS 10 AM TODAY. NFP FRIDAY AT 64K.

The cross-asset complex is presenting the most extreme divergence of the entire war. MOVE at 77.8630 (+10.58%) has EXPLODED above the pre-war baseline and is now at its highest level since the post-ceasefire compression began — the third-highest MOVE reading of the entire post-Day-22 period. The 30-year yield crossed 5.005%, breaching the 5.00% threshold that marked the Day 22 bond crisis peak for the first time since then. Monday’s session produced a massive bear flattener: 2Y +6.6 bps to 3.946%, 5Y +6.5 bps, 10Y +6.0 bps, 30Y +5.2 bps to 5.013% — the broadest single-session yield expansion since the war’s acute phase. The trigger: post-FOMC repricing + Warsh transition uncertainty + $100+ oil sustained + ISM Prices Paid at 84.6 (highest since 2022) all converging into a rates-stress event.

AND YET — equities are rallying. ES at +0.45%, NQ at +0.75%, Russell at +0.81% OUTPERFORMING (small-cap leadership returning for the first time since mid-April). DAX +1.38%, EuroStoxx +1.59%, Nikkei +1.07% — global risk-on. The catalyst: WTI crude is pulling back −3.25% to $102.96, providing the oil-relief trade that has been the war’s most consistent equity-bullish catalyst. Brent −2.25% to $111.86. The oil pullback from the $108 Brent peak gives equities room to price the FOMC fracture as an institutional event rather than an economic threat. The market is saying: ‘the rates-vol stress is about Fed governance and positioning, not about the real economy — and the oil pullback proves it.’

The bull flattener on Tuesday (all yields falling: 2Y −1.2 bps to 3.934%, 5Y −1.4 bps, 10Y −1.0 bps, 30Y −0.8 bps to 5.005%) is the market’s attempt to walk back Monday’s massive bear flattener. But the 30Y at 5.005% — EXACTLY at the crisis threshold even after the walkback — is the canary. The bond market has NOT resolved the 5.00% question. It has parked directly on the line.

Gold at $4,580.80 (+1.05%) is RALLYING — the first meaningful gold bid in over a week. Palladium +3.17%, Copper +2.44%, Platinum +1.89%, Silver +0.71% — the entire metals complex is catching a bid. The metals recovery reverses the multi-week liquidation that drove gold down 13.8% from pre-war levels. If gold sustains this rally into ISM Services and JOLTS today, it signals the market is re-engaging safe-haven demand despite the equity rally — the classic ‘everything rally’ configuration where both risk and haven assets bid simultaneously on liquidity concerns.

The Number That Matters: MOVE 77.86 (+10.58%) — The Largest Single-Session MOVE Expansion Since Day 21-22. Now 4.65 Points Above Baseline. The Bond Market Is In Crisis Posture While Equities Rally. This Divergence Is Unsustainable — One Will Capitulate.

The MOVE-equity divergence is the defining tension of the session: MOVE at 77.86 (rates-vol crisis) + ES at +0.45% (equity risk-on) + 30Y at 5.005% (bond crisis threshold) + WTI −3.25% (oil relief) + gold +1.05% (haven demand) + BTC +1.59% (risk-on). Every asset class is moving simultaneously — this is a LIQUIDITY event, not a directional event. The market cannot sustain MOVE above 77 with equities at +5.5% above pre-war indefinitely. Either MOVE compresses back below 73.21 (equities confirmed right) or equities de-rate to match the rates-vol stress (MOVE confirmed right). ISM Services at 10 AM and JOLTS at 10 AM provide the first data tests. NFP Friday is the definitive resolution.

The Setup: Bull Flattener — Risk-On — Oil Relief Emerging. MOVE Crisis-Level Above Baseline. 30Y At 5.00%. Equities Rallying On Oil Pullback. Metals Recovering. ISM Services + JOLTS 10 AM. NFP Friday. The Most Extreme Cross-Asset Divergence Of The War.

2. OVERNIGHT SESSION RECAP

Monday Cash Session — The Bear Flattener Shock

Monday produced the most aggressive single-session yield expansion of the post-ceasefire period: 2Y +6.6 bps to 3.946%, 5Y +6.5 bps to 4.079%, 10Y +6.0 bps to 4.432%, 30Y +5.2 bps to 5.013%. The 30Y CROSSING 5.00% for the first time since Day 22 (when VIX hit 31.05 and the bond crisis peaked) is the session’s defining event. The catalysts: (1) Post-FOMC hawkish repricing solidifying — the 8-4 split with three members wanting to remove easing bias is settling into the rates complex; (2) Warsh transition uncertainty — he inherits a fractured committee with no rate-cut path; (3) ISM Prices Paid at 84.6 lingering — manufacturing input-cost inflation at 2022 highs; (4) Oil sustained above $100 for over a week. MOVE exploded +10.58% to 77.86 — the largest single-session expansion since the Day 21-22 bond crisis. The S&P closed −0.07% — essentially flat as equities absorbed the rates shock without selling.

Overnight / Tuesday Pre-Market

The overnight recovery is dramatic. Every global index green: DAX +1.38%, EuroStoxx +1.59%, Nikkei +1.07%, ES +0.45%, NQ +0.75%, Russell +0.81%. The catalyst: WTI crude pulling back −3.25% to $102.96. The oil relief provides the fundamental offset to the rates stress — lower oil eases near-term inflation expectations (reducing the urgency for the Fed to act hawkishly) while the 30Y at 5.005% is seen as a positioning event rather than a fundamental repricing. Bull flattener with all yields falling modestly confirms the market is walking back Monday’s overshoot.

BTC at $81,670 (+1.59%) — new multi-week high, now +$21,870 / +36.6% from pre-war. The crypto bid on a day with MOVE at 77.86 and 30Y at 5.00% is the clearest ‘liquidity event’ signal in the cross-asset tape. Gold +1.05%, Palladium +3.17%, Copper +2.44% — the metals recovery confirms haven + industrial demand returning simultaneously.

US Pre-Market Detail

Day 68 of Operation Epic Fury. Q2 Day 25. Tuesday — ISM Services + JOLTS day.

Mag 7 FOUR GREEN / THREE RED: AMZN +1.41% leading (continuing post-earnings momentum). TSLA +0.43%. META +0.27%. NVDA +0.02%. MSFT −0.20%. GOOG −0.93% (giving back from the +9.97% earnings surge). AAPL −1.18% (profit-taking after the +6% post-earnings rally — Apple rotating from ‘strongest’ back to ‘consolidating’).

SECTORS: XLE +0.92% LEADING (energy bid on the oil pullback — the positive XLE/WTI decoupling returns as oil drops). XLK +0.11%. Only 2/11 sectors green. XLB −1.36% worst (materials selling on commodity rotation). XLI −1.14%. XLY −0.77%. XLP −0.75%. The sector tape is narrow — energy and tech green, everything else red. This is NOT a broad risk-on despite the index +0.45%.

FACTORS: SPHB +0.08% (barely green, only green factor). USMV −0.23%. SPLV −0.65% (LOW-VOL AT THE BOTTOM). MTUM −0.28%. USMV-SPHB spread −0.31% (modestly risk-on but barely). Factor tape 1/12 green — the NARROWEST of the week. The equity rally is being driven by index-level futures bidding and individual Mag 7 names, NOT by broad factor participation. This is a positioning-driven session ahead of 10 AM data.

3. THE PRIOR DAY’S REGIME (34 Macro Price, Strength & Momentum Rankings)

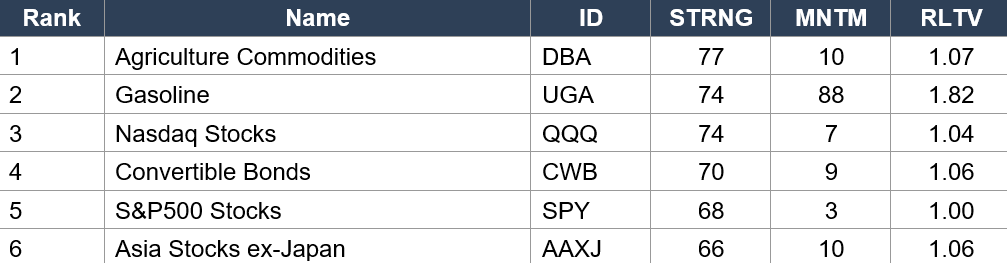

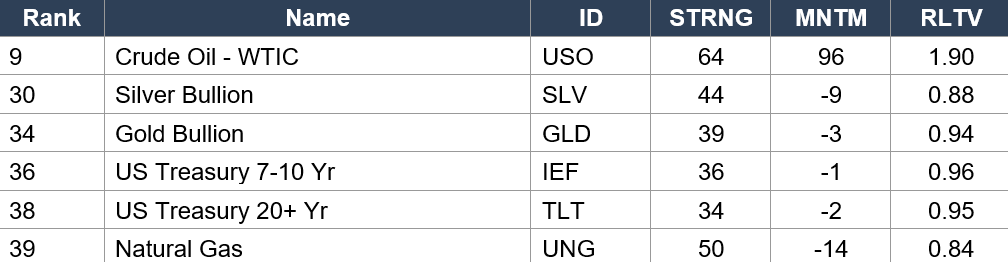

34 Macro Price, Strength & Momentum Rankings — Daily Close, Monday May 4. SPY Baseline: STRNG 68 | MNTM +3 | RLTV 1.00.

Asset Classes — Leaders

Asset Classes — Notable / Laggers

Regime signal: Agriculture (DBA rank 1, STRNG 77) holds #1 for a fourth consecutive data set — the inflationary-commodity leadership is now the war’s most durable asset-class trend. Gasoline (UGA rank 2, MNTM +88, RLTV 1.82) continues to carry extreme energy momentum. Crude Oil (USO rank 9, MNTM +96, RLTV 1.90) DROPPED further from the Leaders category (was rank 5 last set, now rank 9 in the Middle). Energy momentum is normalizing in relative terms even as the absolute MNTM reading (+96) remains near the all-time +97 peak. Today’s −3.25% WTI will accelerate this normalization. Bitcoin (IBIT rank 8, STRNG 65, MNTM +3, RLTV 0.99) improved from rank 12/RLTV 0.90 — the BTC rally is being captured. Ethereum (ETHA rank 13, MNTM +2, RLTV 0.98) also recovering. FIXED INCOME STRUCTURAL WEAKNESS: US Treasury 20+ Year (TLT rank 39, STRNG 34 — LOWEST STRNG of any asset class, RLTV 0.95). The 30Y at 5.005% is fully reflected — long bonds are the weakest asset class in the entire data set. US Treasury 7-10 Year (IEF rank 38, STRNG 36). The bond complex’s weakness is structural and reflects the war’s sustained term-premium expansion.

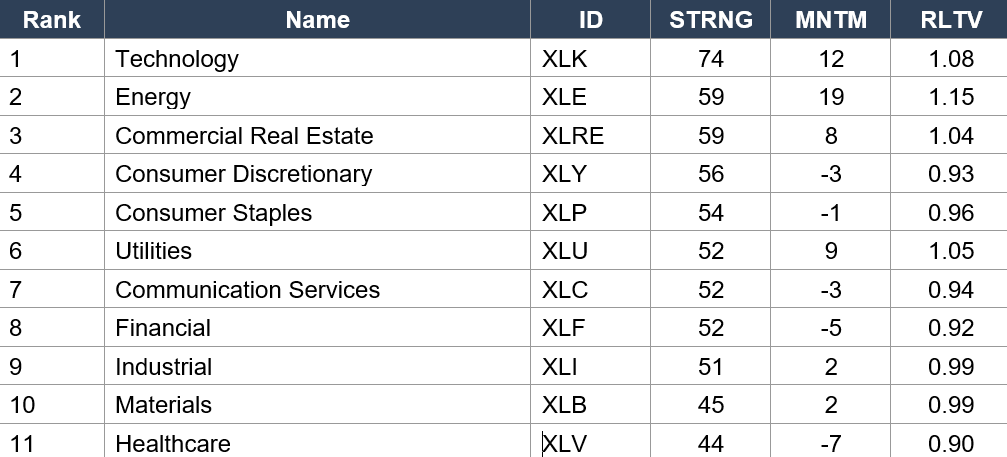

Sector ETFs

Regime signal: XLK (rank 1, STRNG 74, RLTV 1.08) holds #1 sector for a NINTH consecutive data set. ENERGY (XLE rank 2, MNTM +19, RLTV 1.15 — TENTH consecutive data set as a top-3-RLTV sector, now in Leaders for the third set). The energy sector has been the war’s single most consistent relative-strength story across all 10+ weeks of data — no other sector has maintained above-1.10 RLTV for this duration. Today’s XLE +0.92% on WTI −3.25% confirms the positive decoupling: energy equities are pricing earnings leverage, not spot crude. Financial (XLF rank 8, MNTM −5, RLTV 0.92) deepening weakness — the bank-beat trade from April is now fully unwound and financials are a Lagger on a relative basis. Health-Care (XLV rank 11, STRNG 44, RLTV 0.90 — structural laggard, 11th consecutive set at rank 11).

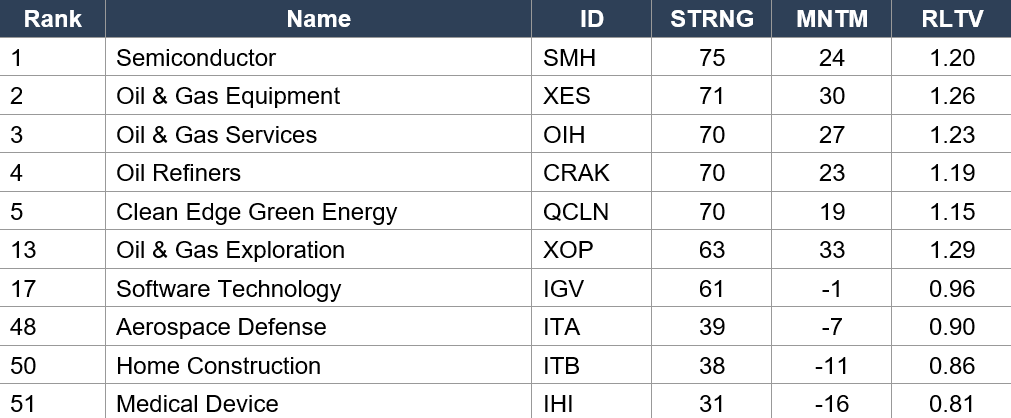

Industry ETFs — Top Leaders + Notable

Regime signal: Semiconductor (SMH rank 1, STRNG 75, RLTV 1.20) holds #1 industry — stabilized after the STRNG crash from 84 to 73 two weeks ago. Energy value chain occupies ranks 2, 3, 4, and 13 with XES (1.26), OIH (1.23), CRAK (1.19), XOP (1.29 — HIGHEST RLTV of any industry). The Oil & Gas Exploration RLTV of 1.29 is the most extreme of any industry in the data — E&P companies are outperforming the market by 29% on a relative basis. SOFTWARE RECOVERY ACCELERATING: IGV (rank 17, MNTM −1, RLTV 0.96) has improved dramatically from the 0.84 trough — the recovery trajectory: 0.84 → 0.85 → 0.88 → 0.92 → 0.96. IGV is approaching baseline and is now in the Leaders category for the first time since early April. The MSFT Azure 40% beat is flowing through. Rare Earth Minerals (REMX rank 26, MNTM +20, RLTV 1.17) — the defense-supply-chain and clean-energy-materials trade. Cannabis (MSOS rank 24, MNTM +18, RLTV 1.15). Medical Device (IHI rank 51, STRNG 31 — NEW ALL-TIME LOW, RLTV 0.81) continues its structural decline. Home Construction (ITB rank 50, MNTM −11, RLTV 0.86) — the 30Y at 5.00% is crushing the housing complex.

4. MORNING DATA REACTION

10:00 AM — ISM SERVICES PMI APRIL (Consensus 53.7, Prior 54.0). The Services-Sector Activity Test Into The Oil Shock.

ISM Services for April is the session’s dominant data event. The consensus at 53.7 implies a modest deceleration from March’s 54.0. The key internals: Prices Paid (if it surges like manufacturing’s 84.6, the inflation-broadening thesis from goods to services is confirmed — the most hawkish possible outcome for the Fed). Employment (if it weakens like manufacturing’s crash to 46.4, the labor-market concern broadens beyond manufacturing). New Orders (if they hold above 55, services demand is absorbing the oil shock). A ‘services strong / prices hot’ combination would mirror the manufacturing ISM and confirm the soft-landing-with-elevated-inflation regime. A ‘services weak / prices hot’ would be the stagflation confirmation the market has been pricing against.

10:00 AM — JOLTS JOB OPENINGS MARCH (Consensus 6.86M, Prior 6.88M). The Labor Demand Pre-Read For NFP Friday.

JOLTS at 6.86M consensus implies essentially flat labor demand. The openings-to-unemployed ratio has been the Fed’s preferred measure of labor market tightness. A meaningful decline below 6.5M would signal demand softening ahead of NFP. A hold near 6.9M would confirm demand resilience. The quits rate and hires rate subcomponents are the secondary reads — declining quits signal workers feel less confident about finding new jobs, which is a leading indicator of labor market cooling.

Monday’s Bear Flattener — 30Y Crossed 5.00% For The First Time Since Day 22. MOVE +10.58% To 77.86. The Bond Market Is In Crisis Posture.

Monday’s yield expansion was the broadest since the war’s acute phase: 2Y +6.6 bps, 5Y +6.5 bps, 10Y +6.0 bps, 30Y +5.2 bps. The 30Y at 5.013% crossed the 5.00% threshold that marked the Day 22 bond crisis peak. On Day 22, the combination was VIX 31.05, MOVE 115.02, 30Y at 5.00%, gold in forced liquidation — the war’s worst cross-asset moment. Today, 30Y is at 5.005%, but VIX is at 17.64 (vs 31.05), MOVE is at 77.86 (vs 115.02), and gold is RALLYING (+1.05%). The bond market is at crisis levels while every other risk metric says ‘no crisis.’ This is unprecedented in the war’s history — and one of these signals is wrong.

5. THE DYRH READ

Regime: Bull Flattener — Risk-On — Oil Relief Emerging. The most extreme cross-asset divergence of the war: MOVE at 77.86 (crisis-level, 4.65 above baseline) while ES +0.45% and global equities rally broadly. 30Y at 5.005% — the Day 22 crisis threshold. Bull flattener walking back Monday’s bear flattener shock. WTI −3.25% providing the oil-relief counterweight. Gold +1.05% — haven demand returning. ISM Services + JOLTS at 10 AM. NFP Friday at 64K consensus. Confidence: MODERATE — the MOVE-equity divergence is unsustainable and one will capitulate this week.

Yield Curve: Bull Flattener — All Yields Falling. Walking Back Monday’s Bear Flattener. But 30Y Still At 5.005%.

All yields falling: 2Y −1.2 bps to 3.934%, 5Y −1.4 bps to 4.065%, 10Y −1.0 bps to 4.422%, 30Y −0.8 bps to 5.005%. The front end falling fastest is the classic bull-flattener driven by the oil pullback easing near-term inflation expectations. But the declines are MODEST — the 30Y has fallen only 0.8 bps from the 5.013% close, leaving it parked on the 5.00% threshold. The market is tentatively walking back Monday’s shock rather than decisively reversing it. If ISM Services confirms strong activity at 10 AM, the bull flattener extends. If ISM Services Prices Paid surges (like manufacturing’s 84.6), the bear flattener returns immediately.

MOVE 77.86 (+10.58%) — 4.65 Points Above Baseline. The Largest Single-Session Expansion Since Day 21-22. The Bond Market Is In Crisis Posture.

MOVE at 77.8630 is the third-highest reading of the entire post-Day-22 period. The trajectory since the post-war low: 66.97 (Apr 24 floor) → 68.42 → 68.68 → 74.33 (FOMC spike) → 72.07 (recovered below baseline) → 70.41 (Friday) → 77.86 (Monday explosion). The Monday MOVE expansion erased all of the post-FOMC compression in a single session. The capitulation thesis that held from Day 35 through Day 63 is now FORMALLY BROKEN — MOVE is not just above baseline, it is SUBSTANTIALLY above at 77.86. The question: is this a positioning event (resolved by ISM/JOLTS/NFP data) or a fundamental regime shift (sustained above baseline through the Warsh transition)? The answer determines the war’s final chapter.

ES 7,263.00 (+0.45%) — Rallying Into MOVE Crisis. +5.5% Above Pre-War Baseline. The Oil Pullback Is The Equity Lifeline.

The equity market at +0.45% with MOVE at 77.86 and 30Y at 5.005% is the war’s most extreme regime divergence. The lifeline is WTI −3.25%: the oil pullback eases the inflation-expectations channel that feeds through to rates stress. If oil continues to pull back toward $100, equities can sustain their rally even with elevated MOVE because the near-term inflation input softens. If oil reverses and re-approaches $105+, the MOVE crisis level compresses the equity multiple.

COR1M 14.17 (+16.82%) — Correlations Rising Sharply. Macro Risk Is Re-Entering The Tape.

COR1M surged from 12.13 to 14.17 — the largest single-session correlation increase in weeks. The 5.00% 30Y level + MOVE at 77.86 is pulling names back into correlated movement as the rates-stress macro headline dominates individual stock stories. The idiosyncratic stock-picking regime from the AAPL/GOOGL earnings week is giving way to macro-driven trading. This is consistent with only 1/12 factors green and 2/11 sectors green — the market is increasingly systematic rather than idiosyncratic.

6. THE GAME PLAN

Today: ISM Services 10 AM (53.7 consensus, 54.0 prior) + JOLTS 10 AM (6.86M consensus). Lagarde 8:30 AM. New Home Sales 10 AM (652K consensus). FRIDAY: NFP 8:30 AM (64K consensus vs 178K prior) + Avg Hourly Earnings (0.3%) + Unemployment Rate (4.3%). WARSH CONFIRMATION VOTE EXPECTED THIS WEEK — takes the chair May 15.

The Bull Case:

ES +0.45%, NQ +0.75%, Russell +0.81% OUTPERFORMING — risk-on with small-cap leadership returning. DAX +1.38%, Nikkei +1.07% — global risk-on. Bull flattener — all yields falling. WTI −3.25% — oil relief providing the inflation counterweight. Gold +1.05% — haven demand returning (the forced-liquidation episode is over). BTC $81,670 (+1.59%) — new multi-week high. 34 Macro shows QQQ at rank 3 (STRNG 74), XLK #1 sector (RLTV 1.08 — highest of the war), SMH #1 industry (RLTV 1.20). IGV improving to 0.96 — software recovery accelerating toward baseline. The oil pullback is the lifeline: if WTI drifts below $100 this week, the inflation-expectations channel eases, MOVE compresses toward baseline, and the equity re-rating extends. If ISM Services holds above 53 and JOLTS near 6.9M, the services economy is absorbing the oil shock.

The Bear Case:

MOVE at 77.86 — 4.65 points ABOVE baseline. The largest expansion since Day 21-22. The capitulation thesis is FORMALLY BROKEN. 30Y at 5.005% — the Day 22 crisis threshold BREACHED. Monday’s bear flattener (2Y +6.6, 30Y +5.2) was the broadest yield expansion of the post-ceasefire period. The MOVE-equity divergence is unsustainable. Only 1/12 factors green. Only 2/11 sectors green. COR1M +16.82% — correlations surging as macro risk returns. The equity rally is narrow (futures-driven, Mag 7 concentrated, not confirmed by breadth). ISM Manufacturing Employment crashed to 46.4 — if ISM Services Employment also weakens, the labor deterioration is broadening beyond manufacturing. NFP at 64K consensus would be the weakest since January 2020. Home Construction (ITB) at rank 50 / RLTV 0.86 — the 5.00% 30Y is crushing housing. TLT at rank 39 / STRNG 34 — long bonds are the weakest asset class. The Warsh transition introduces governance uncertainty into a rates-vol-stressed environment. If ISM Services Prices Paid surges above 80 (matching manufacturing), the inflation-broadening thesis is confirmed and MOVE could push toward 80+.

Regime: Bull Flattener — Risk-On — Oil Relief Emerging. The war’s most extreme cross-asset divergence: MOVE in crisis posture while equities rally on oil relief. One will capitulate this week. ISM Services and JOLTS at 10 AM are the first tests. NFP Friday is the definitive resolution. The 30Y at 5.005% is the canary — if it stays above 5.00% through Friday, the bond crisis is structural. If it falls below 5.00% on the oil pullback, it was a positioning overshoot. Sixty-eight days. The war’s final chapter is being written in real time.

Watch List

ISM Services + JOLTS 10 AM — The Dual Data Test

ISM Services (53.7 consensus) — the services-sector counterpart to manufacturing’s stagflationary print. If Services Prices Paid surges like manufacturing’s 84.6, inflation is broadening beyond goods. If Services Employment weakens, the labor concern broadens. JOLTS (6.86M) — labor demand resilience. A decline below 6.5M would signal demand softening ahead of NFP. Both prints land simultaneously at 10 AM — the combined reaction will set the tone through Friday.

MOVE 77.86 — Will The Bull Flattener Compress It?

If the bull flattener extends through the session and MOVE compresses below 75, the Monday explosion was a positioning overshoot. If MOVE holds above 77 through ISM/JOLTS, the rates stress is structural and the equity-MOVE divergence intensifies into NFP.

30Y At 5.005% — The Crisis Threshold Test

The 30Y is parked on the 5.00% line. On Day 22, 30Y at 5.00% + VIX at 31.05 + MOVE at 115.02 produced the war’s worst cross-asset moment. Today, 30Y at 5.00% + VIX at 17.64 + MOVE at 77.86 is a completely different configuration — rates stress without equity stress. If 30Y holds above 5.00% with VIX below 20, it establishes a new regime: elevated rates as the permanent cost of the frozen conflict’s energy premium.

NFP Friday 64K — The Labor Market Resolution

Consensus now 64K (revised from 60K). Prior 178K. ISM Employment at 46.4 (manufacturing) is the leading indicator. If NFP confirms labor weakness: the war’s damage extends from prices to jobs, the soft-landing thesis evolves into recession concern, and the Fed faces a dual-mandate challenge. If NFP surprises above 100K: the labor market absorbs the oil shock and the S&P maintains its +5.5% premium.

Morning check: Day 68. The war is sixty-eight days old. MOVE exploded to 77.86 — the largest expansion since Day 21-22 — and the 30-year yield crossed 5.00% for the first time since the bond crisis. The capitulation thesis that held from Day 35 through Day 63 is formally broken. And yet: ES +0.45%. NQ +0.75%. Russell +0.81% outperforming. DAX +1.38%. Nikkei +1.07%. BTC $81,670. Gold +1.05% — haven demand returning. The oil pullback (WTI −3.25%) is the equity lifeline — the only thing preventing the MOVE crisis from becoming an equity crisis. The MOVE-equity divergence is the most extreme of the war and one will capitulate this week. ISM Services + JOLTS at 10 AM are the first tests. NFP Friday is the resolution. The 34 Macro data shows energy at #2 sector (RLTV 1.15, 10th consecutive top-3 set), software recovering (IGV 0.96, up from 0.84 trough), long bonds at the bottom of the asset class rankings (TLT STRNG 34), and medical device at the bottom of all industries (IHI STRNG 31). The market is pricing two realities simultaneously: equities say the war is absorbed, bonds say it is not. Sixty-eight days in, and for the first time, the bond market and the equity market fundamentally disagree. This week determines who is right.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.