☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: The hard data now confirms textbook stagflation — and this is all PRE-WAR. Q4 GDP was revised down to 0.7% annualized (from 1.4% advance estimate, consensus expected 1.4% to hold). Core PCE came in at +0.4% MoM / +3.1% YoY — RISING from 3.0% in December. GDP at 0.7% + Core PCE at 3.1% = stagflation in the hard data before the war even started. The economy was already decelerating sharply from Q3’s 4.4% while inflation remained sticky and services-driven (+3.5% YoY). This is the most important data release of the entire series: the war isn’t creating weakness in a strong economy — it’s COMPOUNDING weakness in an already fragile one. Equities are attempting a dead-cat bounce (ES +0.55%) driven entirely by oil pulling back from $100 (Brent −1.08% to $99.38, WTI −2.77% to $93.08). But the bounce is hollow: SPHB still red (−0.22%), IJR flat (0.00%), breadth at THREE metrics below 20 (S5FD 19.48, S5TW 19.68, R2FD 19.82) — APOCALYPTIC. Both S5TH and R2TH below 50 — a majority of S&P 500 AND Russell 2000 stocks are below their 200-day moving average. SKEW crashed from 152 to 140 (−8.2%), the largest single-session move of the series — the tail event is no longer hypothetical, it’s happening. The yield curve executed a 180° reversal in 12 hours: from yesterday’s bear flattener (2Y +8.6 bps, rate cuts priced out) to today’s bull steepener (2Y −4.3 bps, GDP miss reintroduces rate-cut expectations). The Fed’s impossible position: GDP says cut, Core PCE says don’t, oil says can’t. Safe havens surging: CHF +0.88%, JPY +0.85%, BTC +3.30% (biggest move of the series). Gold flat for a fourth session (−3.5% cumulative) — forced liquidation continues. DXY approaching 100. MOVE at 95.30 approaching panic. Michigan Consumer Sentiment at 10:00 AM and JOLTS (January) at 10:00 AM remain as the next catalysts.

The Number That Matters: Q4 GDP at 0.7%. Revised down from 1.4% — a HALVING of growth. The economy was barely growing before the February 28 strikes. With oil now at $93, Hormuz mined and closed, consumer confidence likely cratering, and the labor market already showing cracks (−92K NFP), Q1 GDP is at severe risk of going NEGATIVE. This is the data point that transforms the narrative: this isn’t a strong economy absorbing a geopolitical shock — this is a fragile economy being pushed toward recession while inflation remains sticky at 3.1%.

The Setup: The regime is a confirmed Stagflationary Crisis with hard data. GDP 0.7% + Core PCE 3.1% = textbook. The dead-cat bounce on oil relief is mechanically unsound: SPHB and IJR refuse to participate, breadth is at three metrics below 20, SKEW has crashed, and safe havens are surging despite equities being green. The yield curve’s 180° reversal captures the Fed’s paralysis. Michigan Sentiment at 10:00 AM is the next catalyst: if the first war-shock consumer survey craters below 50 (from 56.6), it completes the stagflation trifecta. JOLTS (January, with annual revisions) also at 10:00 AM — if openings collapse and layoffs surge, the labor market deterioration extends beyond the −92K NFP. The Fed meets next week with no good options.

2. OVERNIGHT SESSION RECAP

Asia-Pacific

Nikkei +0.43%, TOPIX +0.39%. Asia bouncing modestly on oil relief after yesterday’s carnage. But the bounce is muted — Japan remains highly vulnerable to sustained $90+ oil given its energy import dependence.

Europe

Euro Stoxx +0.33%, DAX +0.19%. Europe barely green. The GDP miss is a warning for European economies too — if the US was already at 0.7% growth before the war, Europe’s own slowdown risks are compounding. IMO extraordinary session next week (March 18–19) on maritime threats signals institutional alarm about Hormuz.

US Pre-Market

Day 14 — Continued Escalation Despite Oil Pullback. US military refueling tanker crashed in western Iraq — 4 of 6 crew killed, rescue underway for remaining 2. Kuwait International Airport damaged by drones. Saudi Arabia intercepted drones headed to Shaybah oil field. Bahrain under attack with citizens urged to seek shelter. Iran has reportedly MINED the Strait of Hormuz — a new escalation beyond ship attacks. Hegseth said the US “doesn’t need to worry” about Hormuz. Russia’s UK ambassador called the war a “misadventure.” Iran death toll 1,300+, Lebanon 687, US now 11 killed (including tanker crash).

DATA BOMBS (released today at 8:30 AM): Q4 GDP second estimate: 0.7% annualized — revised DOWN from 1.4%, consensus expected 1.4% to hold. Downward revisions across exports, consumer spending, government spending, AND investment. January PCE headline: +0.3% MoM / +2.8% YoY (slightly below 2.9% consensus). January Core PCE: +0.4% MoM / +3.1% YoY — in-line but RISING from 3.0% in December. Services inflation +3.5% YoY (up from 3.4%). GDP at 0.7% + Core PCE at 3.1% = textbook stagflation in the hard data, all pre-war.

Prior session (March 12 close — WORST SESSION OF THE SERIES): S&P −1.52% to 6,672.62 (lowest since November). Dow −1.56% (−739 pts) below 47,000. Nasdaq −1.78%. Russell −2.11% (below 2,500). 72.8% of US issues declined — broadest selloff. Brent CLOSED above $100 ($100.46) for the first time since August 2022. MOVE +21.25% to 95.30 — largest single-session spike. Morgan Stanley/Cliffwater capped private credit fund withdrawals. Khamenei’s son declared Hormuz should “remain shut.” ALL 7 Mag 7, ALL 12 factors, ALL 11 thematics deep red. Adobe CEO resigned. Dollar General weak forecast.

Today’s data still pending: Michigan Consumer Sentiment (preliminary March) at 10:00 AM — the FIRST consumer survey capturing the war and oil shock (forecast 55.0 vs. 56.6 prior). JOLTS (January, with annual revisions) at 10:00 AM. Atlanta Fed GDPNow (Q1 estimate) at 10:30 AM. Baker Hughes Rig Count at 1:00 PM. NOTE: February PPI remains rescheduled to March 18 per BLS. Next week: FOMC decision (Tue–Wed) — hold universally expected; statement language is what matters.

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 03/12/26. Provided for informational purposes only; not as investment advice.

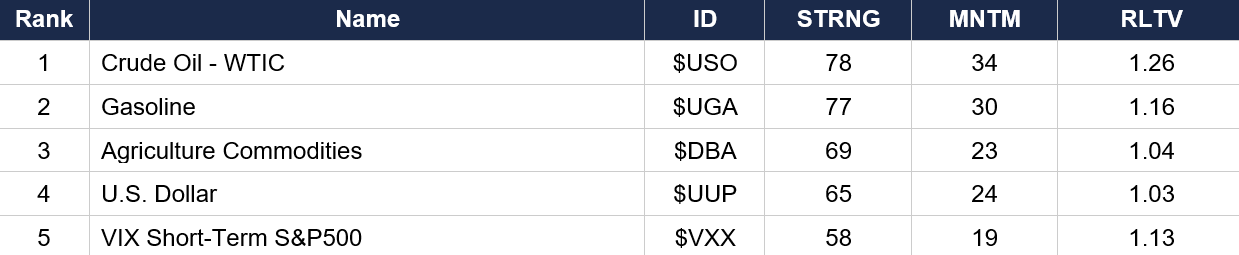

Asset Classes — Top 5

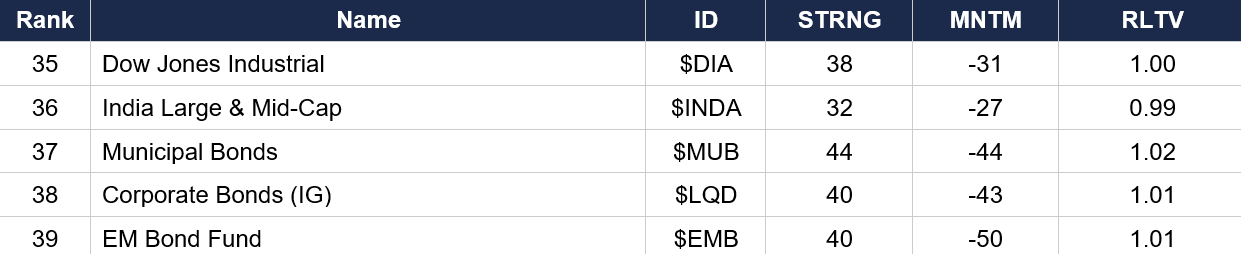

Asset Classes — Bottom 5

Regime signal: Crude oil has reclaimed rank 1 with RLTV 1.26 — the HIGHEST relative strength reading of the entire series for any asset. Oil isn’t just leading, it’s dominating. VIX ($VXX) has returned to rank 5 (MNTM 19) after dropping to rank 14 yesterday. Dollar ($UUP) at rank 4 with MNTM 24 (up from 18) — safe-haven dollar demand accelerating. Natural Gas ($UNG rank 6, MNTM 17) rising as energy complex broadens. Senior Corporate Loans ($BKLN) dropped to rank 7 (from 4) with MNTM 22 — still strong but the credit stress from Morgan Stanley/Cliffwater is beginning to register. Nasdaq ($QQQ rank 14, MNTM −9) has turned NEGATIVE momentum for the first time — tech’s shelter status is eroding. S&P ($SPY rank 17, MNTM −22) deeply negative. EM Bonds ($EMB, MNTM −50) is the worst momentum on the entire board — the first −50 reading of the series. Dow ($DIA, MNTM −31) entering the bottom 5 for the first time.

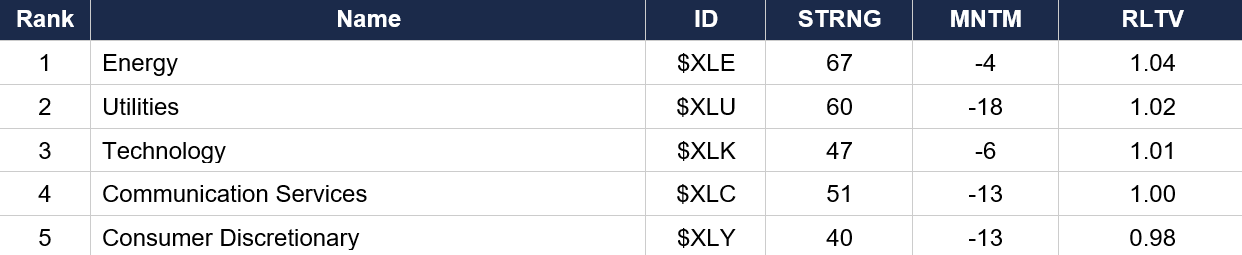

Sector ETFs — Top 5

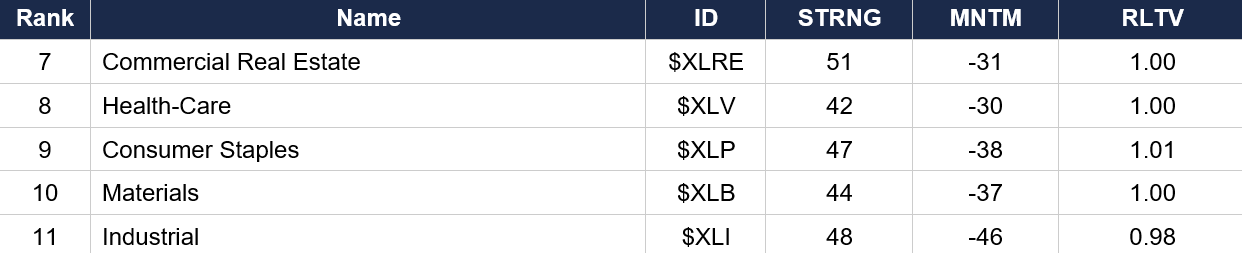

Sector ETFs — Bottom 5

Regime signal: Energy ($XLE) maintains rank 1 but MNTM −4 — even the leading sector has negative momentum. Technology ($XLK) MNTM has flipped to −6 from +10 yesterday — the tech shelter is eroding rapidly. ALL 11 sectors now have NEGATIVE momentum, a first in the series. Industrial ($XLI, MNTM −46) is the worst sector momentum of the entire series — industrial America is being crushed by the oil shock and GDP weakness. Consumer Staples ($XLP, MNTM −38) and Materials ($XLB, MNTM −37) near series lows.

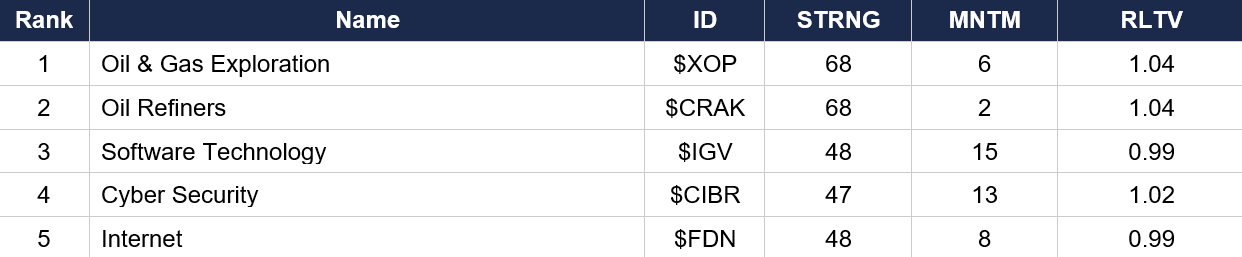

Industry ETFs — Top 5

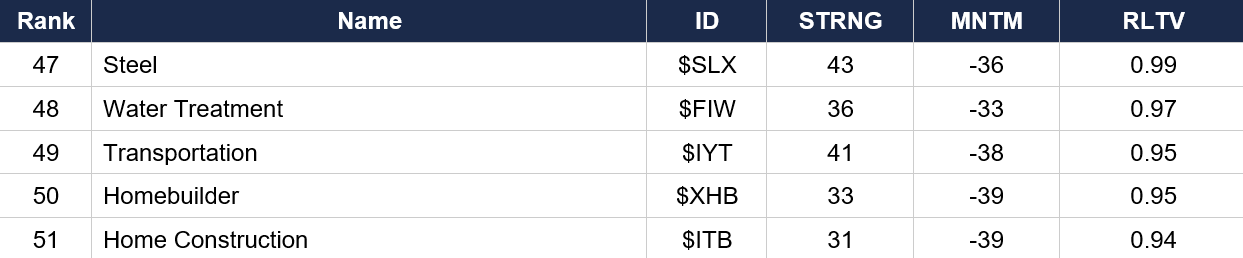

Industry ETFs — Bottom 5

Regime signal: Oil & Gas ($XOP, $CRAK) hold the top 2 but momentum is fading ($XOP MNTM 6, down from 8; $CRAK MNTM 2, down from 5). Software ($IGV) at rank 3 with MNTM 15 (down sharply from 23) — the tech darling is losing steam. Aerospace-Defense ($ITA) has plummeted to rank 36 (MNTM −31) — from rank 17 two days ago. Defense is being destroyed despite an active war. Shipping ($BOAT rank 41, MNTM −51) is the worst industry momentum on the board — the FIRST −50 reading for any industry. Hormuz closure is devastating global shipping. Home Construction ($ITB, MNTM −39) and Homebuilders ($XHB, MNTM −39) remain at the absolute bottom as 30Y yields at 4.88% and mortgage rates at 6.11% crush housing.

4. MORNING DATA REACTION

Q4 GDP Second Estimate (released today at 8:30 AM): 0.7% annualized — revised DOWN from the 1.4% advance estimate. Consensus expected 1.4% to hold. Downward revisions to exports, consumer spending, government spending, AND investment. This is the economy BEFORE the war — already decelerating sharply from Q3’s 4.4%. With oil at $93, Hormuz mined, and the labor market cracking (−92K NFP), Q1 GDP is at severe risk of going negative.

January Core PCE (released today at 8:30 AM): +0.4% MoM / +3.1% YoY — in-line with expectations but RISING from 3.0% in December. The Fed’s preferred inflation gauge is moving in the WRONG direction. Services inflation at +3.5% YoY (up from 3.4%) is the sticky component. Headline PCE: +0.3% MoM / +2.8% YoY. GDP at 0.7% + Core PCE at 3.1% = the textbook stagflation configuration. The Fed meets next week trapped: GDP says cut, PCE says don’t, oil says can’t.

Michigan Consumer Sentiment (10:00 AM today — PENDING): Preliminary March. Forecast 55.0 vs. 56.6 final February. This is the FIRST consumer survey capturing the war and oil shock. If sentiment craters below 50, it completes the stagflation trifecta: weak growth, sticky inflation, collapsing consumer confidence. Watch the inflation expectations components — if 1-year expectations jump above 4% (from 3.4%), the Fed’s hands are tied even tighter.

JOLTS January (10:00 AM today — PENDING, with annual revisions): This release incorporates the annual CES benchmark update that previously triggered large downward revisions to employment. If job openings collapse and layoffs surge, the labor market deterioration extends beyond the −92K NFP. The revision history could also alter the entire 2024–2025 labor market narrative.

Yesterday’s data: Jobless Claims came in at 218K (vs. 215K expected), modestly above estimates but within normal range. Not yet showing clear war disruption in the weekly filing data. Adobe CEO resigned. Dollar General issued weak forward guidance — low-income consumer barometer flashing red as gas surges from $3.00 to $3.61 pre-market.

5. THE DYRH READ

Regime: Stagflationary Crisis — Hard Data Confirms Economic Weakness; Dead Cat Bounce on Oil Relief. GDP 0.7% + Core PCE 3.1% = textbook stagflation in the hard data, all pre-war. Confidence: High on characterization.

Yield Curve: Bull Steepener — 180° Reversal in 12 Hours. Yesterday was a bear flattener (2Y +8.6 bps, rate cuts priced out on $100 Brent + Khamenei Hormuz endorsement). Today is a bull steepener (2Y −4.3 bps, GDP miss reintroduces growth fears). The 30Y at 4.882% (+0.2 bps) REFUSES to rally — inflation expectations and term premium anchor the long end. The 2s30s spread is steepening ~4.5 bps in a single session. This is the stagflationary trap made visible in the curve: the front end says growth is dying, the back end says inflation isn’t going away. The Fed faces an impossible choice. Cumulative: 10Y +29.6 bps from pre-war; 2Y has GIVEN BACK 4.3 of yesterday’s 8.6 bps surge. This is the single most volatile yield curve session of the entire series.

Breadth: Apocalyptic — THREE Metrics Below 20. S5FD 19.48, S5TW 19.68, R2FD 19.82 — three breadth metrics below 20 simultaneously, unprecedented in the series. Only ~20% of stocks are above their 5-day AND 20-day moving averages. S5TH (48.90) and R2TH (48.56) both below 50 — a majority of S&P AND Russell stocks are below their 200-day MA. Bear market by breadth definition, even though the index drawdown is only 3%. The index at 6,714 is a complete fiction held up by mega-cap weights while 80% of the market is in freefall. SKEW crashed from 152 to 140 (−8.2%) — the tail event is no longer hypothetical. COR1M at 35.52 (series high) = pure systematic risk.

Commodity Complex: Oil Retreating From $100, Gold Still Liquidating. WTI −2.77% to $93.08, Brent −1.08% to $99.38 (back below $100 after yesterday’s first close above since August 2022). The pullback is profit-taking, not fundamental — Hormuz is mined, Khamenei endorsed closure, Navy can’t escort until end of month. Gold +0.03% — flat for a FOURTH consecutive session. Cumulative gold: −$184.5 (−3.5%), deepest loss of the series. Forced liquidation confirmed. Platinum −3.06% = industrial demand destruction signal from the GDP miss. Grains flipping red (soybeans −0.79%, oats −0.94%) signals the market shifting focus from supply-side inflation to demand destruction.

Equities: Dead Cat Bounce — Hollow Recovery. ES +0.55% to 6,714.25 recovers only 35% of yesterday’s −1.52% loss. 6 of 7 Mag 7 green but META still −1.33% in pre-market (extending yesterday’s −2.55%). All 11 sectors green but magnitudes tiny (0.12% to 0.76%). SPHB still RED (−0.22%), IJR FLAT (0.00%) — high beta and small caps refuse to participate. The bounce is mechanical mean reversion, not risk appetite. Russell leading at +0.82% is reflexive after −2.11%. When SPHB and IJR don’t bounce on a green day, risk appetite has NOT returned.

FX: Safe Havens Surging Despite Equity Bounce. CHF +0.88%, JPY +0.85% — the two purest safe-haven currencies are surging even as equities bounce. The FX market is NOT buying the equity relief rally. DXY at 99.805 approaching the psychologically significant 100 level despite a massive GDP miss — safe-haven demand overwhelming the rate-differential impact. BTC +3.30% ($72,975) — biggest single-session move of the series. Bitcoin as liquidity escape valve in a stagflationary environment where bonds, equities, and gold are all impaired. AUD −0.41%, GBP −0.49% — commodity/risk currencies weak.

Volatility: VIX Compressing on Bounce, MOVE Approaching Panic. VIX at 25.77 (−5.57%) pulling back on the equity bounce but remains above 25. MOVE at 95.30 (yesterday’s close, +21.25% — largest single-session spike of the series) is approaching the 100 panic threshold. Bond volatility at 95+ with the Fed meeting next week is SYSTEMIC STRESS in the rates market. VIX1D at 24.21 (+27.49%) from yesterday. VVIX at 130.18. The vol picture: equity vol compressing temporarily on the bounce while bond vol remains at crisis levels.

6. THE GAME PLAN

Today’s Key Events: GDP and PCE already released (8:30 AM) — GDP 0.7%, Core PCE 3.1%. Michigan Consumer Sentiment (preliminary March, 10:00 AM) — the FIRST war-shock consumer survey. JOLTS January with annual revisions (10:00 AM). Atlanta Fed GDPNow Q1 estimate (10:30 AM). Baker Hughes Rig Count (1:00 PM). Next week: FOMC decision Tuesday–Wednesday — hold expected, statement language on stagflation is key.

The Bull Case: Oil pulling back from $100 provides temporary relief — Brent back below $100 is a near-term positive. The 35% equity recovery is at least SOMETHING after the worst session of the series. The yield curve’s bull steepener means the front end is pricing in the POSSIBILITY of eventual rate cuts if growth deteriorates further. S5FD at 19.48 and R2FD at 19.82 are extreme oversold — readings this low have historically preceded violent mechanical rebounds if a catalyst emerges. 6 of 7 Mag 7 green. BTC +3.30% shows some risk appetite surviving somewhere. If Michigan beats expectations and Hormuz mine-clearing makes progress, the relief rally could extend. Russia-US energy cooperation discussions could be a wildcard de-escalation path.

The Bear Case: GDP at 0.7% confirms the economy was already fragile BEFORE the war compounded it. Core PCE RISING to 3.1% means the Fed can’t cut even as growth collapses. Three breadth metrics below 20 = 80% of stocks in freefall. SPHB and IJR refuse to participate in the bounce. SKEW crashed from 152 to 140 — the tail event is happening. Safe havens surging (CHF, JPY) despite equity green = the FX market doesn’t believe the bounce. MOVE at 95 approaching panic. Morgan Stanley/Cliffwater private credit fund withdrawals = credit stress spreading. Gold down 3.5% cumulative during a war = forced liquidation continues. Hormuz is MINED, not just blockaded. If Michigan craters below 50, the stagflation trifecta is complete. Q1 GDP may go NEGATIVE. The Fed meets next week with zero good options.

Regime: Stagflationary Crisis — Hard Data Confirms. GDP 0.7% + Core PCE 3.1% = textbook stagflation before the war. The dead-cat bounce on oil relief is hollow: SPHB red, IJR flat, three breadth metrics below 20, SKEW crashed, safe havens surging. The yield curve’s 180° reversal captures the Fed’s paralysis. Michigan Sentiment at 10:00 AM is the next catalyst — if it craters, the trifecta is complete. The index is a fiction. The real market is in a bear market by every breadth definition.

Watch List

Michigan Sentiment 10:00 AM — THE war-shock survey — Forecast 55.0 vs. 56.6 prior. First survey capturing war and oil shock. Below 50 completes the stagflation trifecta. Watch 1-year inflation expectations — above 4% (from 3.4%) would tie the Fed’s hands completely.

JOLTS January 10:00 AM — labor market depth check — Includes annual CES benchmark revisions. If openings collapse or layoffs surge, the −92K NFP wasn’t a one-off. Revision history could alter the entire 2024–2025 labor narrative.

Brent $100 toggle — will it re-cross? — Brent at $99.38, back below $100 after yesterday’s first close above since August 2022. The equity bounce depends ENTIRELY on oil staying below $100. Hormuz is mined, Khamenei endorsed closure, Navy can’t escort until end of month. Re-crossing $100 evaporates the relief rally.

MOVE at 95 — approaching 100 panic — The largest single-session bond vol spike of the series (+21.25%). If MOVE breaches 100 at the open, bond market stress is systemic. With the FOMC meeting next week, rates traders are in crisis mode.

FOMC next week — impossible position — GDP says cut. Core PCE says don’t. Oil says can’t. September rate cut now off the table. Only December priced in. Some desks see NO cuts in 2026. The statement language on stagflation risk is the single most important forward guidance event.

Morning check: the hard data confirms what the market has been pricing in fragments — textbook stagflation. GDP at 0.7% before the war started. Core PCE rising to 3.1%. Oil pulling back from $100 gives a one-day reprieve, but the bounce is hollow: SPHB red, IJR flat, three breadth metrics below 20, SKEW crashed, safe havens surging despite equity green. The yield curve’s 180° reversal in 12 hours is the Fed’s impossible position made visible. Michigan Sentiment at 10:00 AM completes or complicates the picture. The index is a fiction held up by seven stocks. The real market — the other 493 — is already in a bear market.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.