☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: THE AFTERMATH. FOMC 8-4 SPLIT — THE MOST DRAMATIC FED DECISION OF THE WAR. POWELL SAID OIL INFLATION ‘HASN’T PEAKED YET.’ THEN ANNOUNCED HE’S STAYING ON — ‘THEY LEFT ME NO CHOICE.’ MSFT BEAT: EPS $4.27 VS $4.06, AZURE RE-ACCELERATED TO 40%, AI RUN RATE $37B (+123%). MOVE EXPLODED TO 74.33 — ABOVE THE 73.21 PRE-WAR BASELINE FOR THE FIRST TIME SINCE DAY 35. THE CAPITULATION HAS REVERSED. AND YET — ES +0.48%. 8:30 AM TODAY: GDP Q1 2.0% VS 2.2% CONSENSUS (MISS). CORE PCE M/M +0.3% (INLINE). PCE YOY 3.5%. AAPL / AMZN / META AFTER CLOSE TONIGHT.

Yesterday was the most consequential session of the entire 62-day war. Three seismic events in three hours fundamentally altered every regime assumption. At 2 PM, the FOMC held rates at 3.50-3.75% as expected — but with a 4-WAY DISSENT that fractured the committee. Stephen Miran (Trump’s appointee) dissented for a 25 bp CUT. Three hawkish members — Beth Hammack, Neel Kashkari, and Lorie Logan — dissented because they wanted to REMOVE the easing bias entirely, effectively slamming the door on any future cuts. The 8-4 split is the most dramatic Fed decision since the war began and signals that Warsh, who passed the Senate Banking Committee earlier that morning, will inherit a deeply divided committee where seven votes for a cut are near-impossible.

At 2:30 PM, Powell delivered his LAST press conference as Fed Chair with two bombshells. First, he stated that the oil-driven inflation shock ‘hasn’t peaked yet’ and that the Fed wants to see the ‘back side’ of the energy shock before considering any return to rate cuts — the most hawkish oil commentary of his tenure. Second, he announced that he will STAY ON at the Fed in a diminished capacity, stating Trump’s legal attacks ‘left me no choice’ — refusing to cede the institutional ground and blocking Trump from installing another loyalist. ‘We’ve been successful so far. But that’s not over,’ Powell said of the court battles. The 2Y surged +10.5 bps to 3.947% on the hawkish dissent combination and the 30Y touched 4.999% — within 1 bp of the Day 22 crisis level.

At approximately 4:15 PM, Microsoft reported fiscal Q3 results that CRUSHED expectations: EPS $4.27 vs $4.06 consensus (+5.2% beat), revenue $82.9B vs $81.39B (+$1.5B beat), Azure growth RE-ACCELERATED to 40% (above the 39% consensus and up from 38% last quarter). AI annual revenue run rate hit $37 billion, up 123% YoY. Copilot seats expanded from 15M to 20M. Q4 Azure guidance of 39-40% constant currency topped the StreetAccount 37% consensus. But capex for calendar year 2026 was guided to approximately $190 billion (up 61% from 2025), including $25 billion from higher component pricing. MSFT at −1.12% pre-market — the market is digesting the capex magnitude despite the operational beat.

The 8:30 AM data dump just landed: GDP Q1 advance at 2.0% vs 2.2% consensus — a MISS but still positive growth. This is the second consecutive GDP miss (Q4 was revised to 0.5%). Core PCE m/m at +0.3%, inline with consensus. PCE YoY at 3.5% (up sharply from 2.9% in Q4 — the war’s energy pass-through is now fully in the inflation data). Core PCE in the GDP release at 4.3% (up from 2.7% — a massive jump). The combination: GDP miss + PCE inline + core PCE in GDP surging = the bifurcation thesis from April is EVOLVING into a soft-landing-with-elevated-inflation configuration rather than the clean ‘activity without inflation’ story from two weeks ago.

The Number That Matters: MOVE 74.33 (+8.22%). ABOVE The 73.21 Pre-War Baseline For The First Time Since Day 35. The Bond Market’s Capitulation Has Formally Reversed. After 12 Sessions Sub-Baseline, The War’s Rates-Vol Overhang Has Returned.

This is the defining cross-asset event of the session. MOVE crossed above the 73.21 pre-war baseline for the first time since the Day 35 capitulation breakthrough on April 16. The trajectory: 66.97 (post-war low, Friday) → 68.42 (Monday) → 68.68 (Tuesday) → 74.33 (Wednesday, +8.22% — single-session explosion). The 8.22% single-session MOVE expansion is the largest since the Day 21-22 bond crisis. The catalysts: Powell’s ‘oil inflation hasn’t peaked’ hawkishness, the 4-way dissent signaling a deeply divided committee, the 2Y surging +10.5 bps, and the governance uncertainty from both Powell’s ‘I’m staying’ and Warsh’s Banking Committee passage. MOVE above baseline means: the rates-vol complex no longer considers the war’s inflation impact resolved. Every equity multiple is now being re-evaluated through the lens of higher-for-longer rates uncertainty.

The Setup: Bull Flattener — Risk-On — Oil Steady. MOVE Above Baseline (Capitulation Reversed). MSFT Beat But Capex Concern. GDP Miss. Core PCE Inline. Powell’s Last Meeting Fractured The FOMC. AAPL / AMZN / META After Close Tonight.

2. OVERNIGHT SESSION RECAP

Wednesday Cash Session — The Most Consequential Of The War

The Wednesday session will be studied for years. The S&P 500 rallied into the FOMC, sold off on the hawkish dissent combination, then rallied again on the MSFT beat after close — net closing higher. The yield curve settled in a BEAR FLATTENER with the most dramatic single-session repricing of the post-ceasefire period: 2Y +10.5 bps to 3.947%, 5Y +9.8 bps to 4.077%, 10Y +8.0 bps to 4.430%, 30Y +6.0 bps to 4.999%. The front end led higher on the hawkish dissent + Powell’s ‘oil hasn’t peaked’ language. The 30Y at 4.999% — within 1 bp of the 5.00% Day 22 crisis threshold — is the most concerning long-end level since the war’s acute phase.

FOMC Recap: 8-4 Split, Powell Staying, Warsh Ascending

RATE DECISION: Hold at 3.50-3.75% (expected). DISSENTS: (1) Miran dissented for 25 bp cut — the lone dovish voice, representing Trump’s preference for lower rates. (2) Hammack, Kashkari, Logan dissented against the easing bias language (’additional adjustments’) — they wanted to remove any forward indication of cuts. STATEMENT: Easing bias retained (’the extent and timing of additional adjustments’) by 8-4 majority. POWELL PRESSER: ‘The oil-driven inflation shock hasn’t peaked yet.’ ‘We want to see the back side of the energy shock before considering rate cuts.’ Growth risks from gas prices acknowledged as a dovish counterbalance. On governance: Powell will STAY at the Fed in a diminished role — ‘the courts have left me no choice.’ He congratulated Warsh but signaled continued institutional resistance. MARKET INTERPRETATION: The three hawkish dissenters signal that Warsh will inherit a committee where cutting rates is near-impossible without replacing multiple members. ‘It’s completely off the table,’ said Claudia Sahm. The rate path is now: hold indefinitely, with the next debate being whether to raise — not cut.

MSFT Fiscal Q3 — Azure Re-Accelerated, But $190B Capex

After close Wednesday: EPS $4.27 vs $4.06 (+5.2% beat, +23% YoY GAAP). Revenue $82.9B vs $81.39B (+18% YoY). Azure grew 40% (above 39% consensus, RE-ACCELERATED from 38% last quarter — this was THE variable the market was watching). Microsoft Cloud revenue $54.5B (+29%). AI annual run rate $37B (+123% YoY). Copilot paid seats reached 20M (up from 15M in January). Q4 guidance: revenue $86.7-87.8B (midpoint slightly below $87.53B consensus), Azure 39-40% constant currency (above 37% consensus). BUT — capital expenditures for CY2026 guided to approximately $190 billion, including $25B from higher component pricing. The capex magnitude is staggering: $190B is 61% above 2025. ‘We expect to remain constrained at least through 2026,’ said CFO Hood. MSFT at −1.12% pre-market despite the beat — the ‘beat and invest forward’ pattern repeating from TSLA.

Overnight / Pre-Market Thursday

ES 7,202.25 (+0.48%) — risk-on overnight despite MOVE above baseline. NQ +0.66%. DAX +0.92%. Nikkei +0.73%. The overnight recovery from Wednesday’s hawkish FOMC shock reflects the MSFT beat absorbing the rate-vol blow. Gold rallied +1.85% to $4,645.70 — the forced-liquidation episode from Monday/Tuesday has REVERSED. Silver +2.83%. Platinum +3.14%. The metals recovery on a session with MOVE above baseline is a CONSTRUCTIVE signal — it means the gold liquidation was margin-call-driven, not fundamental. WTI at $105.47 (−1.32%) — oil easing modestly from its $108 Brent peak. DXY at 98.30 (−0.54%) — dollar weakening on the bull flattener.

3. THE PRIOR DAY’S REGIME (34 Macro Price, Strength & Momentum Rankings)

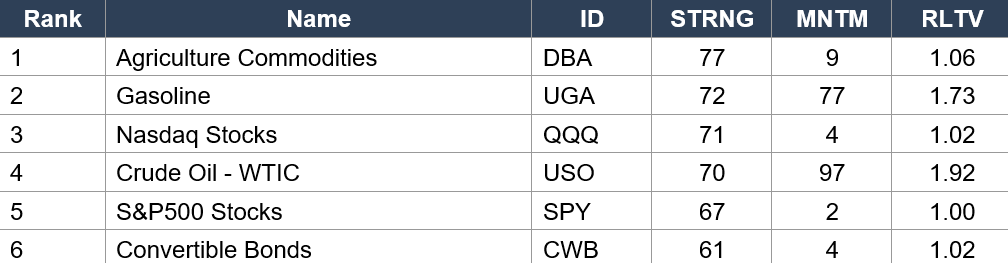

34 Macro Price, Strength & Momentum Rankings — Daily Close, Wednesday April 29. SPY Baseline: STRNG 67 | MNTM +2 | RLTV 1.00.

Asset Classes — Leaders

Asset Classes — Laggers / Extremes

Regime signal: CRUDE OIL (USO rank 4, MNTM +97, RLTV 1.92!!!) has entered the LEADERS category. This is the MOST EXTREME RLTV reading in the HISTORY of the 34 Macro data series — crude is outperforming the market by 92% on a relative basis. MNTM at +97 is also a new all-time high. The $105 oil on the tape is fully captured. Agriculture (DBA rank 1, STRNG 77) holds #1 for the third consecutive data set — the inflationary-commodity leadership is structural. Gasoline (UGA rank 2, MNTM +77, RLTV 1.73). The top 4 asset classes are now: Agriculture, Gasoline, Nasdaq, Crude Oil — the commodity-inflation complex dominates. PRECIOUS METALS DEEPENING TO EXTREMES: Silver (SLV RLTV 0.60 — the LOWEST RLTV of ANY asset class in the ENTIRE war, NEW ALL-TIME LOW). Gold (GLD RLTV 0.82, MNTM −16). Platinum (PPLT 0.68). Natural Gas (UNG 0.68). Today’s gold +1.85% rally will partially reverse these readings. Dollar (UUP rank 13, MNTM +4, RLTV 1.01) — dollar in the Leaders for the first time in the war.

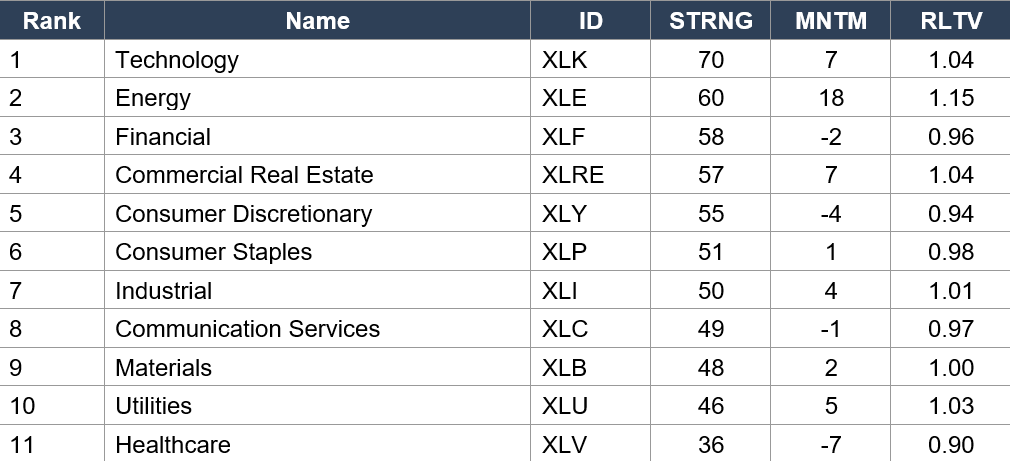

Sector ETFs — Full Ranking

Regime signal: ENERGY (XLE rank 2, MNTM +18, RLTV 1.15) CLIMBED TO THE LEADERS CATEGORY — the first time Energy has been a Leader since the war’s earliest days. XLE’s promotion from rank 10/5/5/5 to rank 2 is the single most dramatic sector re-rating of the post-ceasefire period. The $100+ oil regime has formally converted the Phoenix trade into structural sector leadership. XLK (rank 1, STRNG 70, RLTV 1.04) holds #1 but the gap from #2 has narrowed from 19 to 10 STRNG points — XLE is closing fast. Health-Care (XLV rank 11, STRNG 36 — NEW ALL-TIME WAR LOW for any sector STRNG, RLTV 0.90) has deteriorated further. The STRNG gap between XLK (70) and XLV (36) = 34 points, the widest sector spread in the war.

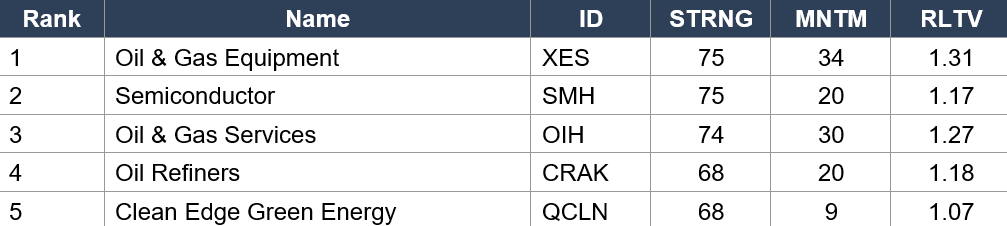

Industry ETFs — Top Leaders

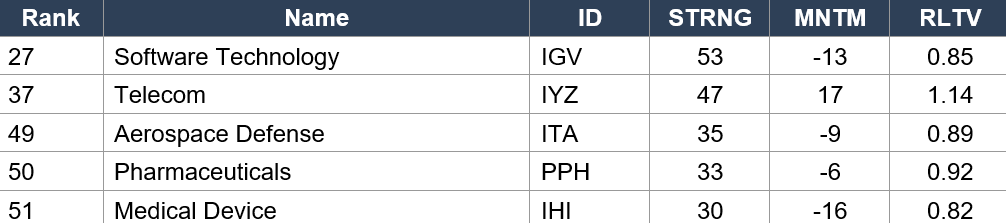

Industry ETFs — Bottom Laggers

Regime signal: OIL & GAS EQUIPMENT (XES rank 1, STRNG 75, MNTM +34, RLTV 1.31 — HIGHEST RLTV of any industry) holds #1 for the third consecutive data set. SMH (rank 2, STRNG 75 — TIED with XES for first time) has stabilized after the STRNG crash from 84. Energy occupies 4 of the top 5 industry positions: XES, OIH, CRAK, plus XOP (rank 12, MNTM +30, RLTV 1.27). The energy value chain’s dominance of the industry landscape is now structural. Software (IGV rank 27, RLTV 0.85) improved one rank but remains broken. Medical Device (IHI rank 51, STRNG 30 — the LOWEST STRNG of any industry in the war’s ENTIRE data history, RLTV 0.82) continues to deteriorate.

4. MORNING DATA REACTION

8:30 AM — GDP Q1 ADVANCE: 2.0% VS 2.2% CONSENSUS (MISS). Second Consecutive GDP Miss. The War’s Growth Drag Is In The Data.

GDP grew at 2.0% annualized in Q1, below the 2.2% consensus and down from the 1.4% Q4 pace (which was itself revised down to 0.5% on the third estimate). The composition: increases in investment, exports, consumer spending, and government spending. Imports (a subtraction) also increased. The GDP Price Index came in at 3.6% vs 3.8% consensus. The miss is modest (−0.2 pp) and 2.0% is still healthy growth — this is not a contraction scare. But the second consecutive miss establishes a DECELERATING trend: Q3 2025 3.1% → Q4 2025 0.5% → Q1 2026 2.0%. The war’s economic drag — via energy costs, supply-chain disruption, and uncertainty — is now visible in the top-line growth data. For the Fed, this is the growth side of the ‘look through’ framework: activity is slowing but not collapsing.

8:30 AM — CORE PCE M/M: +0.3% VS +0.3% CONSENSUS (INLINE). PCE YOY: 3.5%. Core PCE YOY: 3.2%. The War’s Energy Pass-Through Is Fully In The Inflation Data.

Core PCE m/m at +0.3% matched consensus exactly — no surprise. But the annual readings tell the war’s inflation story: headline PCE YoY surged to 3.5% from 2.9% in Q4. Core PCE YoY rose to 3.2% from 3.0%. The quarterly GDP-embedded PCE price index exploded to 4.5% annualized (from 2.9% in Q4) and core PCE in GDP hit 4.3% (from 2.7%). These are the LARGEST quarterly PCE jumps since 2022 and are directly attributable to the war’s energy pass-through. For the Fed, the inline core PCE m/m provides relief — no upside surprise — but the annual trajectory confirms Powell’s statement that the oil inflation ‘hasn’t peaked yet.’ The Fed has explicit data cover to hold and wait for the ‘back side’ of the energy shock, but cutting is off the table until annual PCE trends reverse.

COMBINED INTERPRETATION: GDP 2.0% (miss) + Core PCE 0.3% (inline) = Soft Landing With Elevated Inflation. Not Stagflation (Growth Still Positive). Not Goldilocks (Inflation Elevated). The Middle Path.

The data combination is the middle path between the bull and bear cases: growth is slowing but not contracting (2.0% GDP), inflation is elevated but not accelerating on the core monthly measure (+0.3% inline). This supports the Fed’s hold-and-wait framework — no urgency to cut (inflation too high) and no urgency to hike (growth decelerating). For equities, this is ‘good enough’ — ES at +0.48% confirms the market can live with a GDP miss and inline PCE. The MOVE above-baseline concern from yesterday is being partially offset by the data’s lack of upside inflation surprise.

5. THE DYRH READ

Regime: Bull Flattener — Risk-On — Oil Steady. MOVE above baseline at 74.33 — the capitulation has formally reversed after 12 sessions. But the overnight recovery (ES +0.48%) says equities are absorbing the FOMC shock via the MSFT beat. GDP missed at 2.0% but Core PCE inline at +0.3%. Gold rallying (+1.85%) — forced liquidation reversed. Bull flattener with yields falling across the curve after yesterday’s massive bear flattener repricing. AAPL/AMZN/META after close tonight. Confidence: MODERATE — MOVE above baseline is structurally bearish for equity multiples, but the MSFT beat and inline PCE provide near-term floor.

Yield Curve: BULL FLATTENER — All Yields Falling After Yesterday’s Massive Bear Repricing. The Market Is Walking Back The Hawkish Overshoot.

All yields falling: 2Y −4.5 bps to 3.902%, 5Y −4.0 bps to 4.037%, 10Y −3.2 bps to 4.398%, 30Y −1.7 bps to 4.982%. The front end falling fastest reflects the market walking back yesterday’s +10.5 bps 2Y surge as the GDP miss (2.0% vs 2.2%) provides dovish counterbalance to the hawkish FOMC. The 30Y at 4.982% pulled back from the 4.999% crisis-adjacent level. The bull flattener is the most constructive curve regime for equities: falling rates support multiples, and the front-end pullback suggests the hawkish repricing from yesterday was overdone. BUT — 2Y at 3.902% is still 15+ bps above the pre-FOMC level from last Friday (3.785%) — the hawkish shift from the dissents has been partially retained.

MOVE 74.33 — Above Baseline. The War’s Rates-Vol Overhang Has Returned. But The Overnight Recovery Says The Market Can Function Above Baseline.

MOVE at 74.3273 is 1.11 points ABOVE the 73.21 pre-war baseline. The capitulation from Days 35-44 (12 sessions sub-baseline) has formally ended. But the overnight ES +0.48% / NQ +0.66% / DAX +0.92% tells you the equity market CAN function with MOVE above baseline — it is not the crisis signal that MOVE above 90 or 100 would be. The key question: does MOVE compress back below 73.21 today on the inline PCE / GDP-miss bull flattener? If yes, the capitulation was interrupted but not reversed. If MOVE holds above 73.21 through tonight’s AAPL/AMZN/META earnings, the new regime is: equities rallying DESPITE elevated rates-vol, which is a fundamentally different market structure than the past two weeks.

6. THE GAME PLAN

Today’s Key Events: GDP Q1 2.0% (miss, already released). Core PCE 0.3% (inline, already released). Claims 8:30 AM. ECI 8:30 AM. BOE rate decision 7 AM (consensus hold at 3.75%). ECB rate decision + press 8:15/8:45 AM. AAPL / AMZN / META Q1 AFTER CLOSE — THE MEGA EARNINGS NIGHT. Tomorrow: ISM Manufacturing. Mastercard, Chevron.

The Bull Case:

ES +0.48% absorbing the most hawkish FOMC of the war. MSFT crushed it: Azure 40% RE-ACCELERATED, EPS $4.27 (+5.2% beat), AI $37B run rate (+123%), Copilot 20M seats. Core PCE m/m inline at +0.3% — no upside inflation surprise. Bull flattener — yields falling, walking back yesterday’s hawkish overshoot. Gold +1.85% — forced liquidation reversed. NQ +0.66%, DAX +0.92%, Nikkei +0.73%. AMZN +1.29% positioning into tonight. 34 Macro shows QQQ at #3 asset class, XLK at #1 sector, SMH tied at #1 industry. If AAPL/AMZN/META all deliver tonight: the Mag 7 corporate-fundamentals validation is complete and the equity rally extends into May despite MOVE above baseline and the FOMC fracture.

The Bear Case:

MOVE ABOVE BASELINE — the capitulation has formally reversed after 12 sessions. The bond market no longer considers the war’s inflation impact resolved. Powell: oil inflation ‘hasn’t peaked yet.’ Three FOMC members wanted to remove ALL easing bias. GDP missed at 2.0% — second consecutive miss. PCE YoY surged to 3.5% from 2.9%. Core PCE in GDP at 4.3% (from 2.7%). 2Y at 3.902% still 15+ bps above pre-FOMC levels. 30Y at 4.982% — still crisis-adjacent. MSFT at −1.12% pre-market DESPITE the beat — $190B capex magnitude overwhelms the operational beat. NVDA −1.84% (semis continuing to unwind). AAPL −0.18% barely red into tonight — Apple has been the structural weak link (red 7 of 9 sessions). If AAPL misses: the cap-weighted S&P faces its largest single-name event risk of the war. If any of AAPL/AMZN/META disappoint on AI capex / guidance: the ‘beat and invest forward’ pattern could cascade across all three names on the same evening. The FOMC fracture means Warsh inherits a committee that cannot cut — any expectation of early Warsh-led easing is ‘completely off the table’ per Sahm.

Regime: Bull Flattener — Risk-On — Oil Steady. Yesterday’s FOMC fractured the committee, reversed the MOVE capitulation, and produced the most hawkish Powell commentary of the war. MSFT delivered the cleanest operational beat of earnings season. GDP missed but Core PCE was inline. Tonight: AAPL, AMZN, META — three Mag 7 names in a single evening, the largest concentration of the war. The resolution determines whether the equity market can sustain its rally ABOVE the MOVE baseline — a structurally more difficult environment than the sub-baseline comfort of the past two weeks — or whether the FOMC fracture + MOVE reversal marks the ceiling of the post-ceasefire rally.

Watch List

AAPL / AMZN / META Tonight — The Mega Earnings Night

Three Mag 7 names report after close. AAPL enters as the weakest Mag 7 (red 7 of 9 sessions) — iPhone demand, Services growth, China exposure are the variables. AMZN at +1.29% pre-market is the most aggressively positioned — AWS growth, advertising revenue, and e-commerce margin are the catalysts. META at −0.33% positioning cautiously — Reality Labs losses, advertising pricing, and AI capex are the questions. If all three deliver: the Mag 7 corporate-fundamentals story is complete. If any disappoints: the MOVE-above-baseline environment amplifies the downside.

MOVE 73.21 Level — Does The Capitulation Reverse Or Resume?

If MOVE compresses back below 73.21 today on the inline PCE and bull flattener, the capitulation was interrupted not reversed. If MOVE holds above 73.21 through tonight’s earnings, the new regime is established: equities must rally through elevated rates-vol rather than benefiting from its absence.

Powell’s Legacy + Warsh’s Inheritance

Powell’s decision to stay blocks Trump from another Fed appointment and ensures the hawkish institutional voice persists into the Warsh transition. The three hawkish dissenters (Hammack, Kashkari, Logan) have signaled they will resist rate cuts even under new leadership. Warsh inherits a committee where 7 votes for a cut require replacing or persuading at least 3 hawkish members. The rate path is hold-indefinitely with the next debate being hikes, not cuts.

Morning check: Day 63. Yesterday was the most consequential session of the war. The FOMC fractured 8-4 — the most dramatic split since the conflict began. Powell said oil inflation ‘hasn’t peaked.’ Then said he’s staying. Then MSFT delivered: Azure 40% re-accelerated, EPS $4.27, AI $37B run rate. MOVE exploded above the 73.21 pre-war baseline for the first time in 12 sessions — the capitulation has formally reversed. And yet the market is green: ES +0.48%, gold +1.85%, bull flattener, yields falling. This morning: GDP missed at 2.0%. Core PCE inline at +0.3%. The middle path — not stagflation, not Goldilocks. Tonight: AAPL, AMZN, META — three Mag 7 names in a single evening. The market must now decide whether it can sustain its rally above the MOVE baseline — with a fractured FOMC, $105 oil, and three mega-cap earnings in three hours. The answer comes tonight. Sixty-three days of war. Every regime assumption challenged in a single 24-hour period. And still — the S&P is 4.7% above where it started. Pressure, not panic. Regime, not reaction.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.