☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: NEUTRAL / CONSOLIDATING — ES 7,187.00 (−0.11%). MOVE COMPRESSED TO 66.97 — NEW POST-WAR LOW, NOW 6.24 POINTS SUB-BASELINE. MICHIGAN REVISED TO 49.8 VS 48.0 CONSENSUS FRIDAY — PEAK CONSUMER STRESS CONFIRMED BEHIND US. BRENT CROSSED $100 FOR THE FIRST TIME IN THE WAR (+1.74% TO $100.85). WTI $96.02 (+1.72%). MAG 7 SIX GREEN / ONE RED WITH NVDA +4.32% LEADING AND SOXX +4.67%. FACTOR TAPE RISK-ON: MTUM +1.82%, SPHB +1.61%, USMV-SPHB −1.86%. COR1M 11.17 (−11.91%) BACK NEAR WAR LOWS. BEAR FLATTENER. GOLD FAILING TO RALLY ON DOLLAR WEAKNESS. AAPL −0.87% THE ONLY RED MAG 7. ITA −1.51% DEFENSE CONTINUES TO BLEED. THE MEGA WEEK: FOMC + MSFT WEDNESDAY. GDP + PCE + AAPL/AMZN/META THURSDAY.

The market enters the most consequential week of the entire war from a position of extraordinary rates-vol comfort. MOVE at 66.9665 (−1.08%) is a NEW POST-WAR LOW — lower than Thursday’s 67.70 and Friday’s floor. From the war high of 115.02, MOVE has now declined 48.05 points (−41.8%). The pre-war baseline of 73.21 is 6.24 points above — the widest sub-baseline margin of the entire conflict. The bond market has never been MORE comfortable with the macro environment than it is at this moment. This is happening despite: Brent crossing $100 for the first time, the frozen conflict continuing with no diplomatic timeline, and the most loaded single-week event calendar of the war ahead (FOMC + mega-earnings + GDP + PCE all in three days).

Friday’s Michigan revised sentiment provided the last piece of the consumer puzzle. The index was revised UP to 49.8 from the 47.6 preliminary — a meaningful +2.2 point revision against consensus of 48.0. The 49.8 final reading is still the weakest on record (comparable to the June 2022 trough) but the DIRECTION of the revision is constructive: the ceasefire extension and the brief oil pullback to $81 helped sentiment recover from early April’s record-low stress. Year-ahead inflation expectations revised to 4.7% from the 4.8% preliminary — a modest improvement. Long-run expectations at 3.5%, highest since October 2025 but below the feared 5%+ threshold. Peak consumer stress is BEHIND us — and the data arc now reads: PPI services flat → Empire State +11.0 → Philly Fed 26.7 → Claims 207K → Retail Sales core +1.9% → UNH raised guidance → Michigan revised UP. SEVEN consecutive constructive data prints.

The pre-market tape is technically risk-on by factor structure despite ES at −0.11%. SOXX at +4.67% is the largest single-session semis bid since the war’s early days. NVDA +4.32% leading the Mag 7 with AMZN +3.49%, META +2.41%, MSFT +2.13%, GOOG +1.35%, TSLA +0.69% all green. AAPL −0.87% remains the lone red Mag 7 name — Apple has been red in 6 of the past 8 sessions, the longest sustained Apple weakness of the war. Factor tape: MTUM +1.82% LEADING (momentum back in favor), SPHB +1.61%, VLUE +1.51%. Defensive names ALL red: USMV −0.24%, DGRO −0.51%, VYM −0.56%, SPLV −0.66%. USMV-SPHB spread −1.86% (DEEPLY risk-on — the most negative since last week’s five-session streak). The Friday defensive rotation (SPLV leading, SPHB lagging) has FULLY reversed into Monday’s risk-on rotation.

Brent crude crossed $100 for the first time in the war at $100.85 (+1.74%). WTI at $96.02 (+1.72%). The oil market is pricing the frozen conflict’s sustained blockade as a structural supply constraint — Brent above $100 shifts the narrative from ‘war premium’ to ‘sustained supply disruption.’ The $100 Brent level is the psychological threshold that historically triggers: (1) Consumer demand-destruction modeling, (2) OPEC+ supply-response debate, (3) Fed inflation-risk recalibration. For the April 29 FOMC, $100 Brent on the tape when Powell speaks is a different backdrop than $86 Brent from last week.

The Number That Matters: MOVE 66.97 — New Post-War Low. 6.24 Points Sub-Baseline. The Bond Market Has Never Been More Comfortable. And Yet — Brent Just Crossed $100.

This is the week’s defining tension: MOVE at a new post-war low says the bond market is fully at ease with the macro environment, while Brent above $100 says the energy-supply constraint from the frozen conflict is intensifying. These two signals cannot coexist indefinitely. Either: (1) Brent above $100 eventually re-engages inflation expectations and pushes MOVE back toward baseline, or (2) MOVE’s compression signals that the bond market has permanently ‘looked through’ the oil shock and Brent’s level is irrelevant to rates-vol. The FOMC on Wednesday resolves which interpretation wins — Powell either validates the ‘look through’ framework (MOVE stays compressed, equities extend) or expresses concern about $100 Brent / 4.7% inflation expectations (MOVE re-expands, equities de-rate).

The Setup: Bear Flattener — Neutral / Consolidating — Energy Steady. MOVE At New War Low. Brent At $100+. Factor Tape Risk-On. Mag 7 Six Green. The Most Loaded Week Of The War: FOMC + MSFT Wednesday, GDP + PCE + AAPL/AMZN/META Thursday.

2. OVERNIGHT SESSION RECAP

Friday Cash Session — Michigan Revised + Bull Flattener

Friday’s cash session closed constructively. Michigan revised sentiment at 10 AM printed 49.8 vs 48.0 consensus — a meaningful upside revision from the 47.6 preliminary. The market read the revision as ‘peak consumer stress behind us’ and the curve responded with a BULL FLATTENER: 2Y −4.7 bps to 3.785% (the largest single-session front-end decline since the Day 37 oil-crash session), 5Y −3.3 bps, 10Y −1.9 bps, 30Y −0.2 bps. The front end falling fastest reflects the market adding back rate-cut probability on the consumer-stress-is-peaking interpretation. Friday closed with strong breadth (S5FD 89.40, R2FD 85.10 both expanding) and the Michigan revision provided a clean close to a constructive week.

Weekend — No Major Escalation

The weekend passed without major kinetic escalation. The frozen-conflict framework continues: ceasefire extended indefinitely, blockade active, Hormuz contested, no diplomatic timeline. Iran’s state media continued to describe the blockade as ‘an act of war’ but no new kinetic events. The Touska seizure from the prior weekend remains the most recent combat event. Vance’s Islamabad trip remains postponed. The market enters Monday with the same geopolitical backdrop as Friday — which means positioning is driven by the FOMC/earnings week ahead rather than war developments.

Asia-Pacific

Nikkei +0.66% to 60,460 — Japan extending its multi-session rally, now at the highest level since before the war’s ceasefire collapse. The semis-led bid from SOXX +4.67% is reading through to Japanese tech exporters. Topix +0.12% — the Nikkei-Topix divergence continues (concentrated export-tech vs domestic). BOJ Policy Rate decision tonight (consensus hold at <0.75%) — if BOJ holds as expected, the yen impact is neutral.

Europe

DAX +0.61% to 24,413. EuroStoxx 50 +0.45% to 5,859. European markets constructive — reversing the soft tone from late last week. The European rally is likely positioning into the FOMC week rather than fundamental European data, though Brent at $100.85 is a headwind for European energy costs. EUR +0.25% to 1.1774.

US Pre-Market

Day 60 of Operation Epic Fury. Q2 Day 19. Monday — position-building day ahead of the mega week. FOMC blackout active.

US FUTURES MIXED: NQ 27,392.50 (−0.15%), ES 7,187.00 (−0.11%), YM 49,339 (−0.11%), RTY 2,797.60 (+0.05%). Futures modestly red but the Mag 7 individual stocks and factor/thematic tapes are strongly risk-on — the disconnect reflects overnight futures positioning vs. the pre-market stock-level bidding that began at 4 AM.

MAG 7 SIX GREEN / ONE RED — NVDA-LED SEMIS BREAKOUT: NVDA +4.32% (the largest single Mag 7 pre-market move of the past week). AMZN +3.49% (positioning into Thursday’s earnings). META +2.41% (positioning into Thursday’s earnings). MSFT +2.13% (positioning into Wednesday’s earnings). GOOG +1.35%. TSLA +0.69% (modest recovery from the −3.56% capex-raise selloff). AAPL −0.87% (still the structural weak link — now red 6 of 8 sessions; AAPL reports Thursday). The NVDA-led move is the catalyst: reports suggest accelerated Blackwell chip delivery schedules and potential new hyperscaler orders that would validate the AI capex cycle.

SECTORS — XLK DOMINATING: XLK +2.81% (technology sector leading by a massive margin — the widest single-session XLK outperformance of the post-ceasefire period). XLY +0.81%. XLB +0.21%. XLU +0.20%. Four sectors green. XLE −0.19% (energy lagging WTI +1.72% — the demand-destruction discount re-embedded). XLRE −0.30%. XLP −0.30%. XLF −0.73%. XLI −0.92% (industrial giving back Friday’s defensive bid). XLV −1.41% (healthcare structural laggard). XLC −1.58% (communication services the worst sector — the META/GOOG individual stock bids are NOT translating to the sector-ETF level, meaning non-Mag-7 XLC components are selling).

FACTORS RISK-ON — MOMENTUM LEADING: MTUM +1.82% LEADING (momentum back in favor for the first time since mid-April). SPHB +1.61%. VLUE +1.51%. LRGF +0.77%. QUAL +0.73%. IJR +0.54%. 7/12 factors green with all greens being risk-seeking/momentum names. USMV −0.24%. DGRO −0.51%. VYM −0.56%. SPLV −0.66%. All defensives red. USMV-SPHB spread −1.86% (DEEPLY risk-on). The Friday defensive rotation has FULLY reversed — Monday’s factor tape is the cleanest risk-on configuration since the four-consecutive-war-high streak two weeks ago.

SOXX +4.67% — THE SESSION’S STANDOUT THEMATIC. The most aggressive single-session semis bid in weeks. ARKW +2.23%. DRIV +1.71%. FINX +0.98%. CIBR +0.98%. PAVE −0.44% (infrastructure giving back). ICLN −0.74%. ARKG −0.87%. ITA −1.51% (defense continues to bleed in the frozen-conflict framework). The thematic tape is split: tech/semis/AI rallying hard while energy/defense/infrastructure/genomics sell. This is the ‘AI capex cycle’ trade in its purest form.

3. THE PRIOR DAY’S REGIME (34 Macro Price, Strength & Momentum Rankings)

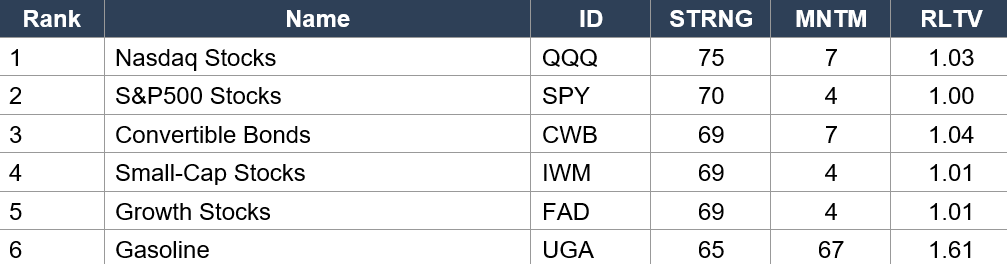

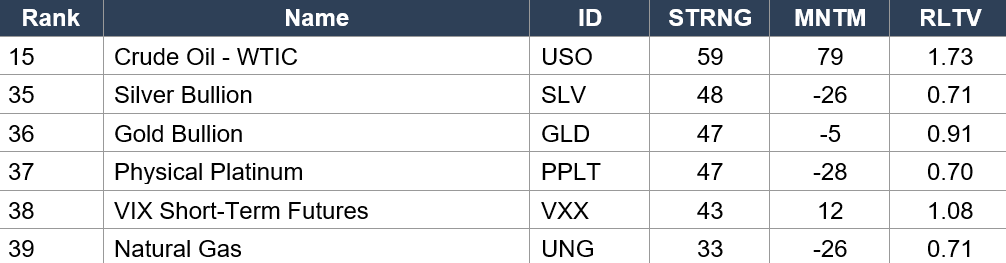

34 Macro Price, Strength & Momentum Rankings — Daily Close, Friday April 24. SPY Baseline: STRNG 70 | MNTM +4 | RLTV 1.00.

Asset Classes — Leaders

Asset Classes — Laggers / Extremes

Regime signal: QQQ (rank 1, STRNG 75 — HIGHEST STRNG of any asset class) extends its #1 position for a fifth consecutive data set. STRNG rose from 71 to 75 — Nasdaq momentum accelerating. SPY (rank 2, STRNG 70) holds. CWB (rank 3, RLTV 1.04) — credit risk-appetite persists. IWM (rank 4, RLTV 1.01) — small-cap outperformance confirmed. ENERGY: Crude Oil (USO rank 15, MNTM +79, RLTV 1.73) — momentum slowed from +88 to +79 but RLTV TICKED DOWN from 1.82 to 1.73. The energy momentum extreme is beginning to NORMALIZE, even as WTI rose to $96. Gasoline (UGA MNTM +67, RLTV 1.61) also normalizing. The Friday oil stabilization + Michigan upside revision allowed the energy complex’s relative strength to begin mean-reverting. PRECIOUS METALS DEEPENING COLLAPSE: Platinum (PPLT RLTV 0.70 — the LOWEST RLTV of any asset class in the entire war), Silver (SLV 0.71), Natural Gas (UNG 0.71). The precious-metals liquidation is now at extreme readings. Gold (GLD 0.91) — gold underperforming the market by 9% on a relative basis. VIX (VXX MNTM +12, RLTV 1.08) — fear momentum remains positive but stabilizing.

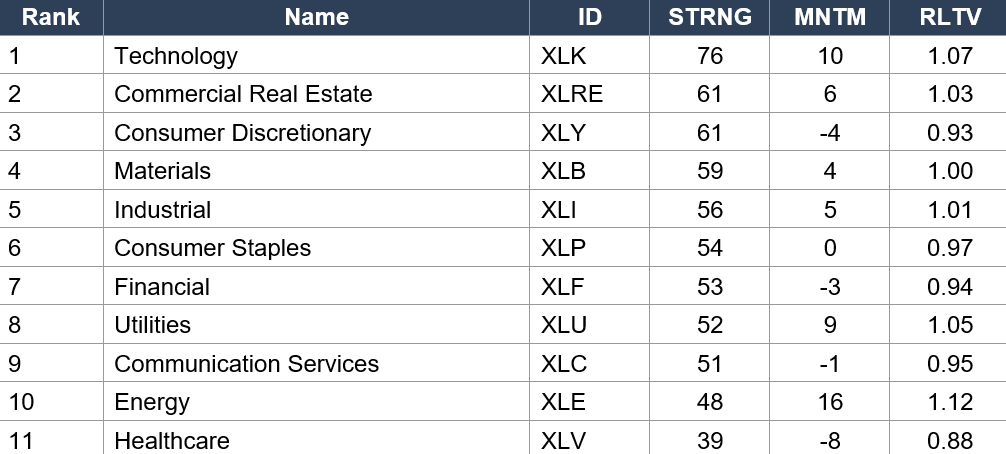

Sector ETFs — Full Ranking

Regime signal: Technology (XLK rank 1, STRNG 76, MNTM +10, RLTV 1.07 — HIGHEST sector RLTV) holds #1 for a fourth consecutive data set with STRNG rising from 72 to 76 and RLTV from 1.05 to 1.07. Tech leadership is accelerating. Today’s +2.81% XLK pre-market will extend this further. XLRE (rank 2, STRNG 61, RLTV 1.03) stabilized but the gap from XLK has widened to 15 STRNG points (76 vs 61) — the largest sector-gap of the war. Utilities (XLU rank 8, MNTM +9, RLTV 1.05) remains the second-highest RLTV sector — the Friday defensive bid captured. Energy (XLE rank 10, MNTM +16, RLTV 1.12 — FIFTH consecutive data set as highest-RLTV sector). The energy Phoenix trade continues structurally. Health-Care (XLV rank 11, STRNG 39 — LOWEST of any sector by far, RLTV 0.88 — weakest relative strength). Healthcare is the war’s structural laggard. Financial (XLF rank 7, MNTM −3, RLTV 0.94) — financial momentum remains negative, the bank-beat trade fully unwound.

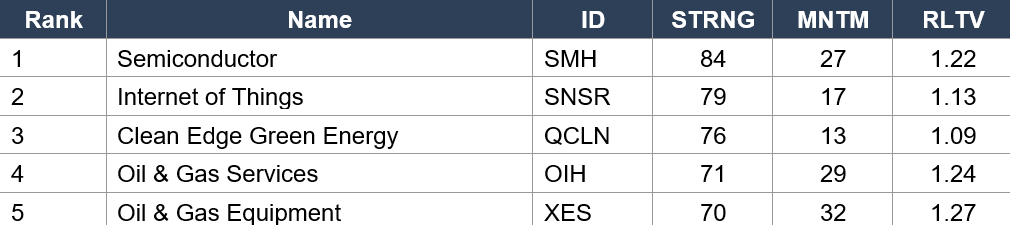

Industry ETFs — Top Leaders

Industry ETFs — Notable Shifts

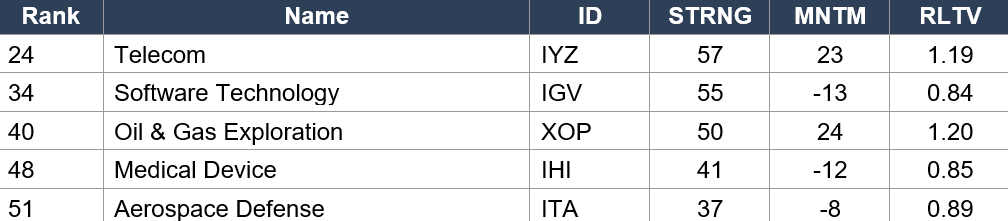

Regime signal: Semiconductor (SMH rank 1, STRNG 84 — NEW ALL-TIME WAR HIGH, MNTM +27, RLTV 1.22) holds #1 industry for the SIXTH consecutive data set. STRNG at 84 is the highest reading for ANY asset in ANY table in the ENTIRE war. RLTV at 1.22 means semis are outperforming the market by 22% on a relative basis. Today’s SOXX +4.67% will extend this dominance further. Oil & Gas Services (OIH rank 4, MNTM +29, RLTV 1.24) and Equipment (XES rank 5, MNTM +32, RLTV 1.27 — HIGHEST RLTV of any industry) — the energy value chain joins the Leaders category for the first time. CRITICAL: Software Technology (IGV rank 34, MNTM −13, RLTV 0.84) remains broken at the SAME level as Thursday — the recovery has stalled at Laggers/Middle boundary. Aerospace-Defense (ITA rank 51, STRNG 37 — LOWEST of any industry, RLTV 0.89) — defense at the absolute bottom of all 51 industries for the second consecutive set. The frozen-conflict framework is devastating for defense names.

4. MORNING DATA REACTION

Friday 10 AM — REVISED MICHIGAN CONSUMER SENTIMENT APRIL: 49.8 (vs 48.0 consensus, preliminary 47.6). UPSIDE REVISION. STILL RECORD LOW BUT PEAK STRESS CONFIRMED BEHIND US.

The Michigan revision landed constructively. The 49.8 final reading is +2.2 points above the 47.6 preliminary — the second-largest upside revision in the survey’s history. Consensus had expected 48.0, so the 49.8 beat by 1.8 points. The index is still the weakest on record, comparable to the June 2022 trough, but the direction matters: the revision captured the ceasefire extension and the brief oil pullback to $81 mid-month. Year-ahead inflation expectations revised DOWN to 4.7% from 4.8% preliminary — a modest improvement. Long-run expectations at 3.5% are elevated (highest since October 2025) but below the feared 5%+ threshold that would have forced the Fed’s hand.

MARKET INTERPRETATION: The Michigan revision is the seventh consecutive constructive data print (PPI/Empire/Philly/Claims/Retail/UNH/Michigan). The consumer-stress narrative from early April has been systematically dismantled. For Wednesday’s FOMC: the revised Michigan gives the Fed cover to maintain the ‘look through’ framework — sentiment is at record lows but REVISING HIGHER, which means the acute stress is fading. Powell can point to the revision direction rather than the absolute level. The Friday bull flattener (2Y −4.7 bps) reflects the market adding back rate-cut probability on this interpretation.

No US Data Scheduled Today. BOJ Decision Overnight (Consensus Hold <0.75%).

Monday is a clean positioning day ahead of the mega week. No US economic data. BOJ policy decision tonight — consensus hold. The only catalyst is the pre-market Mag 7 positioning and the WTI/Brent oil dynamics. The market has two more sessions (Monday, Tuesday) to position before Wednesday’s FOMC + MSFT convergence.

5. THE DYRH READ

Regime: Bear Flattener — Neutral / Consolidating — Energy Steady. MOVE at a new post-war low of 66.97 — the bond market has NEVER been more comfortable. Brent crossed $100 for the first time. Factor tape risk-on with MTUM leading and USMV-SPHB −1.86%. COR1M 11.17 back near war lows — stock-picking dominant, macro in the background. Mag 7 six green / one red with NVDA +4.32% leading a SOXX +4.67% semis breakout. ES −0.11% modestly red on overnight futures but pre-market stock-level action is strongly risk-on. Gold failing to rally on dollar weakness is the session’s most important divergence — safe-haven demand being liquidated. Confidence: HIGH — MOVE at 66.97 and COR1M at 11.17 provide clean, low-noise signal environment.

Yield Curve: Bear Flattener — All Yields Rising, Front Leading. The Monday Adjustment After Friday’s Bull Flattener.

All yields rising: 2Y +0.8 bps to 3.793%, 10Y +0.8 bps to 4.314%, 5Y +0.7 bps to 3.929%, 30Y +0.7 bps to 4.919%. Friday’s dramatic bull flattener (2Y −4.7 bps on the Michigan revision) is being partially walked back as Monday’s pre-FOMC positioning takes hold. The 2Y rising from 3.785% to 3.793% (+0.8 bps) is modest and well within normal pre-FOMC adjustment range. The 30Y at 4.919% is stable — the long end is not re-engaging inflation concern despite Brent at $100. This tells you the bond market believes $100 Brent is temporary (either the blockade eases or demand destruction kicks in) rather than permanent.

MOVE 66.97 (−1.08%) — NEW POST-WAR LOW. 6.24 Points Sub-Baseline. 48-Point Decline From War High. The Bond Market Enters The FOMC Week At Maximum Comfort.

MOVE trajectory since the Wednesday peak: 70.78 → 67.70 → 66.97 (via Friday’s bull flattener). From the 115.02 war high, MOVE has declined 48.05 points. The pre-war 73.21 baseline is now 6.24 points above — the widest sub-baseline margin of the conflict. The bond market enters the FOMC week having fully absorbed: the ceasefire extension, the Hormuz re-closure and ship seizure, the Warsh hearing, the Michigan revision, the TSLA capex raise, and Brent at $100. Every catalyst that could have re-expanded MOVE has been digested. If MOVE holds sub-70 through Wednesday’s FOMC, the capitulation thesis from Day 35 is structurally permanent until the next major regime shock.

Brent $100.85 — CROSSED $100 FOR THE FIRST TIME IN THE WAR. The Frozen Conflict’s Supply Constraint Is Becoming Structural.

Brent at $100.85 (+1.74%) is the first $100+ Brent print of the entire 60-day conflict. WTI at $96.02 (+1.72%). The Brent-WTI spread at ~$4.83 has widened modestly from last week’s $3.50 — the Hormuz/freight premium is re-engaging. Brent above $100 while MOVE is at a new war low is the week’s defining divergence. Cumulative energy moves: WTI +$29.00 / +43.3% from pre-war $67.02. Brent +$27.98 / +38.4% from pre-war $72.87. These are massive sustained energy-price increases that have not resolved via either demand destruction or diplomatic de-escalation. The frozen conflict is making $95-100 oil the new normal.

COR1M 11.17 (−11.91%) — Correlations Falling Back Toward War Lows. Stock-Picking Dominance Returns.

COR1M reversed from the 12.68 rebound (Thursday) to 11.17 (Monday) — a dramatic −11.91% single-session decline. Correlations are back near the 10.94 war low from two weeks ago. The macro event calendar (FOMC, mega-earnings) has NOT increased correlations — instead, the individual stock dynamics (NVDA +4.32%, AAPL −0.87%, ITA −1.51%) are dominating. COR1M below 12 entering the FOMC week means: the Fed decision and mega-earnings are not being treated as correlated risk events by the market. Each name is trading on its own story.

6. THE GAME PLAN

THE MEGA WEEK — The Most Consequential Three Days Of The Entire War:

MONDAY APR 27 — No US data. BOJ overnight (consensus hold). Position-building day. TUESDAY APR 28 — FOMC begins (Day 1 of 2-day meeting). Visa, PayPal, GE Aerospace Q1 earnings. WEDNESDAY APR 29 — FOMC statement 2 PM. Powell press conference 2:30 PM. MSFT fiscal Q3 after close. The FOMC-MSFT convergence is the single most concentrated event in the war. THURSDAY APR 30 — Advance GDP Q1 8:30 AM (consensus +2.2%, prior +1.4%). Core PCE Price Index m/m 8:30 AM (consensus +0.3%, prior +0.4%). Employment Cost Index q/q 8:30 AM (consensus +0.8%). APPLE (AAPL), AMAZON (AMZN), META (META) Q1 after close. The GDP + PCE + AAPL/AMZN/META convergence is the second mega-event in 24 hours. FRIDAY MAY 1 — ISM Manufacturing. Mastercard, Chevron Q1.

The Bull Case:

MOVE at 66.97 — new post-war low, 6.24 points sub-baseline. The bond market enters the FOMC week at maximum comfort. Michigan revised to 49.8 vs 48.0 — peak consumer stress behind us. SEVEN consecutive constructive data prints. Mag 7 six green / one red with NVDA +4.32%, SOXX +4.67%. Factor tape deeply risk-on (USMV-SPHB −1.86%, MTUM leading). 34 Macro shows QQQ STRNG 75 (highest of any asset), SMH STRNG 84 / RLTV 1.22 (all-time war highs), XLK STRNG 76 / RLTV 1.07. COR1M 11.17 — stock-picking dominant, low macro noise. Nikkei +0.66%, DAX +0.61%. If FOMC holds with dovish lean (validating ‘look through’) + MSFT delivers Azure acceleration + GDP prints strong + Core PCE cools + AAPL/AMZN/META beat: the equity re-rating extends into a structural bull phase. The data-plus-earnings-plus-Fed package would be the most constructive three-day sequence of the entire war.

The Bear Case:

Brent crossed $100 — the first time in the war. WTI at $96 with oil +43.3% cumulative from pre-war. $100 Brent on the tape when Powell speaks is a DIFFERENT backdrop than $86 last week. If Powell expresses concern about $100 oil / 4.7% inflation expectations / 3.5% long-run expectations, the ‘look through’ framework cracks and MOVE re-expands toward baseline. AAPL −0.87% — still the structural weak link (6 of 8 sessions red). Gold failing to rally on dollar weakness — safe-haven liquidation is extreme (PPLT 0.70, SLV 0.71). VXX RLTV 1.08 — fear outperforming. ITA at rank 51/STRNG 37 — if the frozen conflict thaws into hot conflict, the defense bottom-fishing opportunity was missed. IGV 0.84 — software recovery remains broken. XLV STRNG 39/RLTV 0.88 — healthcare structural laggard. GDP consensus +2.2% may overshoot if Q1 war disruption hit investment more than anticipated. Core PCE consensus +0.3% — any upside print (0.4%+) would be the hawkish catalyst that re-engages MOVE. The FOMC + mega-earnings concentration means any single disappointment could cascade through multiple sessions.

Regime: Bear Flattener — Neutral / Consolidating — Energy Steady. The market enters the mega week from a position of extraordinary rates-vol comfort (MOVE 66.97) and risk-on factor positioning (USMV-SPHB −1.86%). The week resolves in three days: Wednesday (FOMC + MSFT), Thursday (GDP + PCE + AAPL/AMZN/META), Friday (ISM + Mastercard + Chevron). The defining tension is MOVE at a new war low vs Brent at a new war high — one signal says maximum comfort, the other says maximum energy-supply stress. Powell’s interpretation on Wednesday afternoon will determine which signal the market follows into Thursday’s mega-earnings. Position for the convergence, not the individual events. The resolution of this week defines whether the post-ceasefire rally becomes the permanent regime or the frozen conflict’s structural oil premium reasserts the stagflation narrative.

Watch List

Wednesday FOMC + MSFT — The Defining Convergence

FOMC statement 2 PM (consensus hold at 3.75%). Powell press 2:30 PM. The key question: does Powell validate the ‘look through’ framework with Brent at $100? Or does he express concern about inflation expectations (4.7% 1-year, 3.5% long-run)? MSFT fiscal Q3 after close — Azure growth guidance is the variable (39% last quarter, slowed from 40%). If Azure re-accelerates + Powell is dovish: NQ extends. If Azure disappoints + Powell is hawkish: the software reflation breaks.

Thursday GDP + PCE + AAPL/AMZN/META — The Second Mega Day

GDP Q1 at 8:30 AM (consensus +2.2%). Core PCE m/m 8:30 AM (consensus +0.3%). These prints land 12 hours after MSFT and 4 hours before the cash open reacts to both the FOMC and MSFT. Then AAPL, AMZN, META after close. AAPL at −0.87% is the weakest Mag 7 — any miss would deepen the multi-session weakness. AMZN +3.49% today is positioning aggressively. META +2.41%. Three Mag 7 names in 24 hours after two months of war.

Brent $100 — The Energy Threshold

Brent above $100 historically triggers demand-destruction modeling, OPEC+ response, and Fed inflation recalibration. Watch whether Brent holds above $100 through Wednesday — if yes, Powell faces the $100 oil question directly. If Brent fades below $100 pre-FOMC, the pressure eases.

AAPL Structural Weakness — 6 of 8 Sessions Red

AAPL is the lone red Mag 7 at −0.87% and has been red 6 of 8 sessions. AAPL reports Thursday after close. If Apple disappoints (iPhone demand, Services growth, China weakness), the cap-weighted S&P faces its largest single-name earnings risk of the war.

Morning check: Day 60. The war is sixty days old. MOVE at a new post-war low of 66.97 — the bond market has never been more comfortable. Brent crossed $100 for the first time in the war. These two signals cannot coexist forever. Michigan revised to 49.8 vs 48.0 — peak consumer stress behind us. Seven consecutive constructive data prints. Mag 7 six green / one red with NVDA +4.32%, SOXX +4.67%. Factor tape deeply risk-on. COR1M back near war lows. The 34 Macro data shows SMH STRNG 84 (the highest reading for any asset in any table in the entire war), QQQ STRNG 75, XLK STRNG 76 / RLTV 1.07. The energy complex has RLTV above 1.20 across the value chain. Gold is failing to rally. Defense is at the bottom of all 51 industries. Software is broken. Healthcare is the structural laggard. And the week ahead is the most consequential of the war: FOMC + MSFT Wednesday. GDP + PCE + AAPL/AMZN/META Thursday. ISM + Mastercard + Chevron Friday. Three days that resolve whether the post-ceasefire rally becomes the permanent regime or the frozen conflict’s $100 oil reasserts the stagflation narrative. MOVE is the arbiter. Powell is the catalyst. The earnings are the validation. The resolution is this week.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.