☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: Monday produced the most dramatic intraday reversal of the entire DYRH series. The S&P opened down 1.5% with oil at $119.50 and VIX above 31 — and closed +0.83% after Trump declared the war “very complete, pretty much.” Oil crashed $30 from $120 to $90. VIX was crushed back below 30 to 25.02. Gold bounced +1.78% — the DEFINING SIGNAL CHANGE: forced liquidation is ending, safe-haven function returning. Silver surged +5.05%. Dollar weakened below 99. European markets bouncing sharply (DAX +2.05%, Euro Stoxx +2.04%). But the narrative is CONFLICTED this morning: Defense Secretary Hegseth said today will be “our most intense day of strikes inside Iran.” The Pentagon’s official account posted “We have Only Just Begun to Fight” — directly contradicting Trump’s de-escalation rhetoric. G7 energy ministers are meeting this morning but France’s finance minister said they agreed NOT to release strategic reserves for now (“we’re not there yet”). Saudi Aramco CEO warned of “catastrophic consequences” for oil markets if Hormuz flows don’t resume. Oil pre-market: WTI $89.54 (−5.52%), Brent $92.18 (−6.85%). US futures essentially flat: ES −0.21%, NQ −0.07%. The regime is transitional — war premium deflating on conflicting signals.

The Number That Matters: Oil’s $30 whipsaw. Brent: $119.50 (Sunday night) → $98.96 (Monday settle) → $89.58 (4pm after Trump comments) → $92.18 (Tuesday pre-market). WTI: $119.48 → $94.77 → $86.47 → $89.54. The crash was driven by three simultaneous catalysts: Trump’s “very complete” comment, G7 signaling SPR readiness (300–400M barrels under discussion), and IEA Director Birol noting “there is plenty of oil, we have no oil shortage.” But oil has bounced from after-hours lows as Hegseth’s “most intense strikes” provide a floor. Cumulative: WTI still +33.6% from pre-war $67.02; Brent +26.5% from $72.87. The premium is deflating but far from gone.

The Setup: The regime is in genuine flux — entirely headline-dependent. Trump says “very complete”; the Pentagon says “just begun.” The market is CHOOSING to believe Trump’s de-escalation while ignoring Hegseth’s escalation. If reality aligns with Hegseth (most intense strikes today), the relief trade unwinds. If Trump’s rhetoric proves accurate, oil plunges further and the war premium collapses. G7 energy ministers meeting this morning is the key policy catalyst. CPI tomorrow at 8:30 AM is the binary event for the rates complex. Oracle (ORCL) reports after the close today — the first major tech earnings report in the $100-oil-scare environment. The cross-asset signals are telling: gold bouncing, silver surging, safe havens working again, VIX below 30. The acute crisis phase appears to be ending. But breadth remains at extreme washout levels (S5FD 27.43, S5TW still falling) and SKEW is spiking to 158 — smart money is buying tail protection even as the surface calms.

2. OVERNIGHT SESSION RECAP

Asia-Pacific

TOPIX +0.56%, Nikkei (USD) +0.04% — Japan stabilizing after Monday’s −5.2% cash session crash. The recovery is tepid. Korea still digesting last week’s two circuit breakers. The Asian session was relatively calm compared to Monday’s carnage.

Europe

DAX +2.05%, Euro Stoxx 50 +2.04% — MASSIVE European bounce. The strongest single-session European recovery in the DYRH series. Europe was the most oversold region given direct energy import dependence, and Trump’s de-escalation rhetoric + oil’s $30 crash triggered violent short covering. European defense names likely selling (de-escalation trade).

US Pre-Market

Day 11 — Conflicting Signals. Trump told CBS Monday the war is “very complete, pretty much” and “far ahead of schedule.” At a later press conference he struck a more aggressive tone: “If Iran does anything that stops the flow of Oil within the Strait of Hormuz, they will be hit TWENTY TIMES HARDER.” Hegseth this morning: “Today will be our most intense day of strikes inside Iran.” The Pentagon posted: “We have Only Just Begun to Fight.” Iran death toll 1,200+. US 7 soldiers killed (8th died from injuries). 11 MQ-9 Reapers lost. 5,000+ targets struck. 50+ Iranian vessels destroyed.

Iran struck Bahrain’s Bapco oil refinery for the SECOND time in 24 hours (380K bbl/day). Abu Dhabi’s ADNOC Ruwais Industrial Complex (922K bpd refining capacity) hit by drone — no injuries reported. Iran continues launching drones and rockets across Gulf states. Israel struck Hezbollah financial infrastructure in Lebanon. Lebanon’s president said Lebanon is ready for direct talks with Israel. Over 667,000 displaced in Lebanon (100,000+ in just 24 hours). Iran’s internet blackout now at 240 hours — among the most severe government shutdowns on record globally. Unconfirmed reports that new supreme leader Mojtaba Khamenei may have been wounded.

Monday’s session: The strongest intraday reversal of the series — S&P from −1.5% to +0.83% (2.33% swing). Nasdaq +1.38%. Russell +1.12%. VIX crushed from 31.46 to ~25.50 (−14%). Oil settled WTI $94.77 then crashed to $86.47 after Trump comments. 10Y traded down to 4.10% per CNN.

G7 energy ministers meeting this morning to discuss SPR release further. France’s finance minister said Monday they agreed NOT to release reserves for now (“we’re not there yet”). IEA reserves estimated at ~1 billion barrels (excluding China/Canada). Jefferies: “Strategic reserves would help if the war is measured in weeks; if months, reserves alone would not be sufficient.” Saudi Aramco CEO warned of “catastrophic consequences” for oil markets if Hormuz flows don’t resume.

This week: TODAY — G7 energy ministers meeting; Oracle (ORCL) Q3 earnings after close. Wednesday — CPI (February) 8:30 AM (consensus: headline +0.3% MoM, 2.4% YoY; core +0.3% MoM, 3.0% YoY) — THE critical release. Thursday — PPI (February) 8:30 AM; Jobless Claims; Adobe (ADBE) earnings after close. Friday — Michigan Consumer Sentiment (preliminary March, first survey capturing war/oil shock); JOLTS (January, rescheduled to March 13).

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 03/09/26. Provided for informational purposes only; not as investment advice.

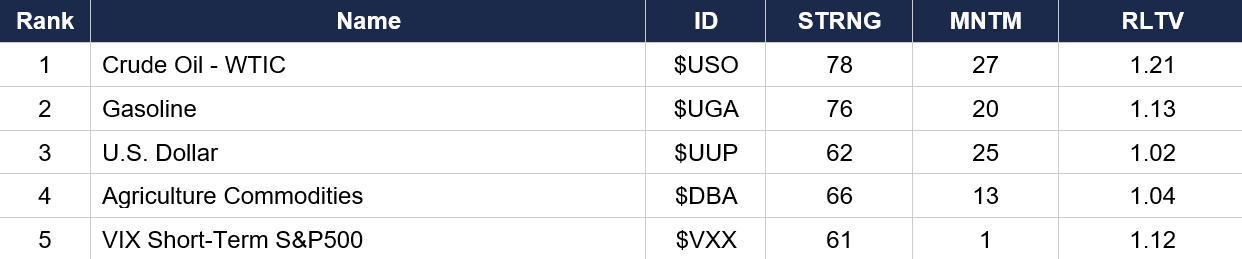

Asset Classes — Top 5

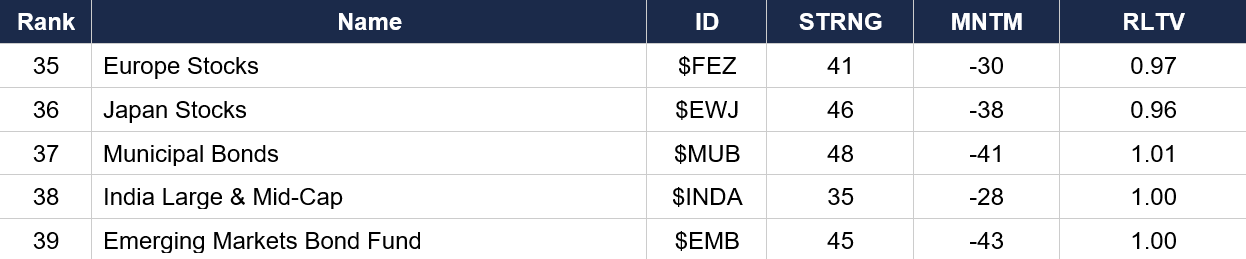

Asset Classes — Bottom 5

Regime signal: Crude oil and gasoline hold the top 2 but MNTM has DECELERATED sharply — crude from 55 to 27, gasoline from 45 to 20. The oil momentum peak is behind us. VIX ($VXX) has collapsed to rank 5 with MNTM at just 1 (from 31) — the volatility trade is being unwound. Agriculture ($DBA) holds rank 4 with MNTM 13 (from 29). Gold has risen to rank 11 (MNTM −2) — improving from −8, consistent with the safe-haven bid returning. Senior Corporate Loans ($BKLN) at rank 7 with MNTM 24 is a notable outlier — floating-rate credit performing well as rate-cut expectations are suppressed. Nasdaq ($QQQ rank 10, MNTM 8) has jumped significantly from 0 — the tech recovery is generating real momentum. S&P ($SPY rank 16, MNTM −3) still negative. EM Bond Fund ($EMB, MNTM −43) is the worst momentum on the entire board.

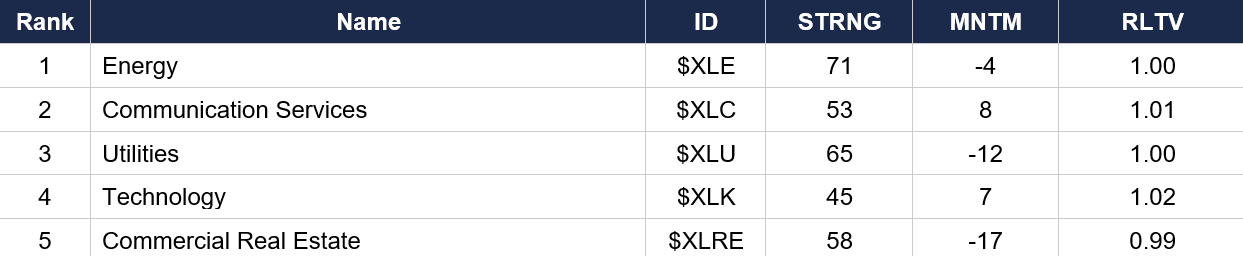

Sector ETFs — Top 5

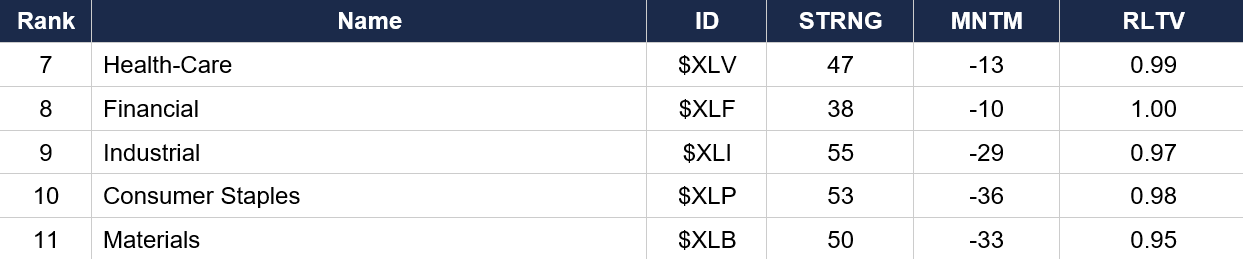

Sector ETFs — Bottom 5

Regime signal: Energy ($XLE) has SEIZED rank 1 from Communication Services for the first time — but its MNTM is still −4 (negative). The rank is driven by relative strength (RLTV 1.00), not momentum. Technology ($XLK) at rank 4 with MNTM 7 confirms the tech recovery. Consumer Discretionary ($XLY) at rank 6 with MNTM −1 — flat momentum, the cyclical recovery stalling. Materials ($XLB, MNTM −33) and Consumer Staples ($XLP, MNTM −36) remain the worst sector momentum — these sectors have been destroyed by the war. Industrial ($XLI, MNTM −29) confirms cyclical destruction. The sector landscape is shifting from “energy only” to “energy + tech” leadership.

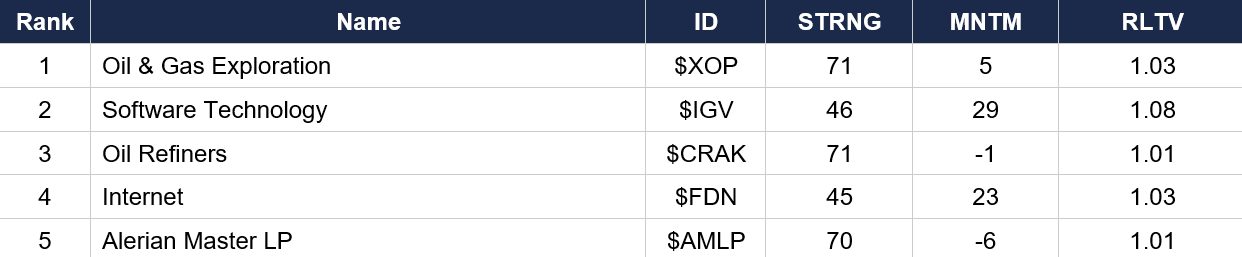

Industry ETFs — Top 5

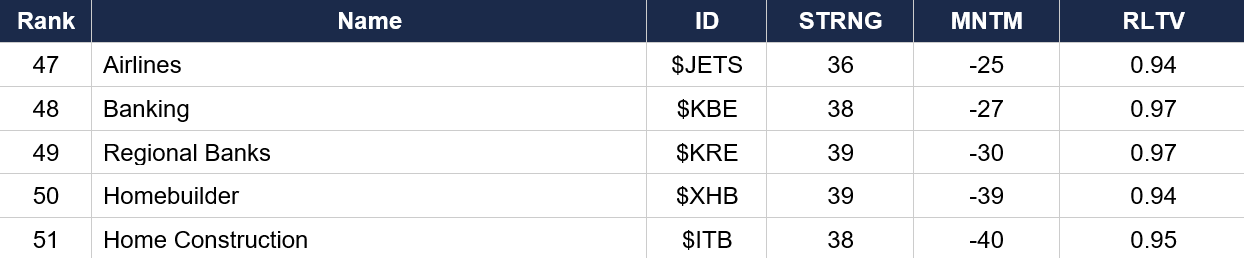

Industry ETFs — Bottom 5

Regime signal: Software ($IGV, MNTM 29) and Internet ($FDN, MNTM 23) remain the highest non-energy momentum on the board — the tech/software complex continues to act as a relative safe haven. Oil & Gas Exploration ($XOP) holds rank 1 but MNTM has fallen to 5 (from 19) — the energy momentum peak is past. Cyber Security ($CIBR, MNTM 17) at rank 6 reflects persistent wartime premium. Aerospace-Defense ($ITA) has plummeted to rank 12 (MNTM −7) as the de-escalation trade hits defense names. Home Construction ($ITB, MNTM −40) is the worst industry momentum on the board. Airlines ($JETS, MNTM −25) still in freefall on fuel costs.

4. MORNING DATA REACTION

No major US economic data releases today. The session will be driven by the G7 energy ministers’ meeting this morning, Hegseth’s “most intense strikes” rhetoric, war headlines, and Oracle earnings after the close.

Yesterday’s data context: Friday’s NFP (released March 6) at −92K remains the regime-defining data point. Unemployment 4.4%. December revised to −17K. The growth leg has collapsed. But Wednesday’s ADP (+63K) and ISM Services (56.1) from last week showed the pre-war economy was bifurcated — strong services, weak manufacturing, collapsing payrolls.

The week’s critical data ahead: Wednesday’s February CPI (8:30 AM) is the MOST IMPORTANT release of the series. February CPI will NOT reflect $100 oil (oil was $67–70 pre-war), but it sets the baseline. Consensus: headline +0.3% MoM, 2.4% YoY; core +0.3% MoM, 3.0% YoY. If core CPI comes in hot, the Fed is completely boxed in. If benign, the market may rally briefly on the “inflation was contained before the war” narrative. Thursday’s PPI and Friday’s Michigan Sentiment (first consumer survey capturing the war/oil shock) round out the week.

Prior week’s data recap: PPI (released Friday February 27): Final demand +0.5% MoM. ISM Manufacturing (released Monday March 2): 52.4, Prices Paid 70.5 (highest since mid-2022). ISM Services (released Wednesday March 4): 56.1 (highest since July 2022), Prices declined to 63.0. ADP (released Wednesday March 4): +63K. NFP (released Friday March 6): −92K.

5. THE DYRH READ

Regime: Transitional — War Premium Deflating on Conflicting Signals. Monday was a regime-defining session. The market transitioned from Recessionary Stagflation (Energy Supply Crisis) to a more ambiguous state. Confidence: Low-Moderate. Entirely headline-dependent.

Yield Curve: Bear Steepener — Long End Leading. The curve dynamic has shifted again. The 30Y is leading higher (+4.3 bps) while the 2Y rises modestly (+1.3 bps). The 2Y-10Y spread is WIDENING. This is the market re-separating the growth impulse (front end — “Fed may need to cut eventually”) from the inflation impulse (long end — “oil at $90 keeps inflation elevated”). LEVELS are DOWN from the Day 8 pre-market peak: 10Y from 4.156% to 4.125% (−3.1 bps). Bond futures are green except ZB (−0.03%) — the front end and belly are rallying while the long bond hesitates. This is the classic growth-scare-with-inflation-overlay curve. Wednesday’s CPI is the binary event: benign = front-end rally continues; hot = bear flattener resumes and the “no Fed put” narrative returns.

Commodity Complex — Oil Crashing, Gold Bouncing, Metals Surging. WTI at $89.54 (−5.52%), Brent at $92.18 (−6.85%) — oil in freefall from Sunday’s $120 highs. The $30 crash is the most dramatic oil reversal since the Russia-Ukraine war in 2022. But oil has bounced from the $86 after-hours lows. Hegseth’s “most intense strikes” and Iran continuing to attack Gulf infrastructure (Bapco refinery, ADNOC Ruwais) are providing a floor. GOLD at $5,194.3 (+1.78%) — THE MOST IMPORTANT SIGNAL CHANGE. Gold was selling throughout the crisis despite war escalation. Now it’s bouncing while oil falls. This means: forced liquidation is ENDING, margin pressure easing, safe-haven flows RETURNING. Silver +5.05% is surging. Platinum +2.07%, palladium +1.06%, copper +0.80%. The entire metals complex is bid — the liquidation cycle that defined Days 2–8 is BREAKING.

Equities: Monday’s Historic Reversal + Flat Pre-Market. ES −0.21%, NQ −0.07% — essentially flat. Monday was the strongest intraday reversal of the series: S&P from −1.5% to +0.83% (2.33% swing). Nasdaq +1.38%. The intraday recovery pattern has RESET — Monday’s >100% recovery was the first to close above the prior session’s close after a gap-down. Cumulative ES damage reduced to −1.38% from −2.95%. Mag 7 Monday close: ALL green, led by NVDA +2.72% (Morgan Stanley upgrade), GOOG +2.58%. Pre-market mixed but benign: TSLA +0.72%, META +0.36% green; NVDA −0.25%, GOOG −0.23% digesting. XLE has flipped from ONLY green sector to ONLY red sector — the complete rotation away from “war economy” positioning.

Factor/Sector Rotation: From War Economy to Growth Economy. The sector and factor structure has completely reversed. XLE (energy) went from the only green sector to the only red sector in one session. ITA (defense) is selling on de-escalation. XLK +1.80% and SOXX +3.98% led Monday’s close — tech and semis driving recovery. Factor rotation: SPHB +1.78% and MTUM +2.39% leading, while USMV −0.01% and SPLV −0.28% lagging — risk-on structure confirmed. This confirms the market is rotating FROM war-economy positioning TO growth-economy positioning. But pre-market today shows slight giveback across all factors.

Safe Havens Working Again — Liquidation Cycle Breaking. Gold +1.78%, silver +5.05%, CHF +0.56%, JPY +0.39%, BTC +2.17%. All traditional safe havens are functioning again after FAILING throughout the crisis. The dollar is weakening below 99. This is the most significant cross-asset shift since the war began: when safe havens work, the forced-liquidation dynamic has ended. But SKEW at 157.98 (+4.07%) — smart money is buying tail protection even as VIX drops below 30. This divergence (falling VIX, rising SKEW) signals institutional hedging against a re-escalation scenario.

Breadth: Still Extreme Despite Rally. S5FD at 27.43 — only 27% of S&P stocks above their 5-day average despite Monday’s green close. S5TW (20-day) at 33.79 is STILL FALLING. The rally is NARROW — driven by mega-cap tech, not broad participation. R2FD bounced to 26.48 from the 20.59 lows but remains deep washout. If breadth doesn’t expand, the rally fails. The VIX-SKEW-breadth divergence is the most important analytical signal today: surface calm, underlying fragility.

6. THE GAME PLAN

Today’s Key Events: G7 energy ministers meeting this morning (SPR decision pending — France said “not yet” on Monday). Hegseth’s “most intense strikes” — real-time headline risk. Oracle (ORCL) Q3 earnings after close — first major tech report in the $100-oil-scare environment. War headlines continuous. Wednesday: CPI 8:30 AM. Thursday: PPI, Jobless Claims, Adobe (ADBE) earnings. Friday: Michigan Sentiment, JOLTS (rescheduled to March 13).

The Bull Case: Monday’s intraday reversal was the most powerful of the series (2.33% swing). Oil crashed $30 from $120 — the panic premium is unwinding. Gold bouncing and safe havens working again = forced liquidation ending. VIX crushed back below 30 to 25.02. Europe surging (DAX +2.05%). Dollar weakening. Factor rotation to risk-on (SPHB/MTUM leading). SOXX +3.98%. If G7 announces a credible SPR release and Trump’s de-escalation proves real, oil could plunge to $75–80 and the war premium collapses. CPI Wednesday could show benign pre-war inflation. Rumors of Mojtaba Khamenei wounded could signal regime fragility. Lebanon ready for talks with Israel. Oracle beat could reinforce the tech-as-shelter narrative.

The Bear Case: Hegseth says today will be “most intense” strikes. The Pentagon posted “We have Only Just Begun to Fight” — directly contradicting Trump. G7 agreed NOT to release reserves on Monday. Iran struck Bahrain’s Bapco refinery for the second time and Abu Dhabi’s ADNOC Ruwais complex (922K bpd). Hormuz remains closed. Oil still $90 (vs. $67 pre-war). Saudi Aramco CEO: “catastrophic consequences” if Hormuz doesn’t reopen. S5FD at 27.43 means the rally is narrow and fragile. S5TW still falling. SKEW spiking to 158 = smart money not convinced. Breadth hasn’t confirmed. COR1M still at 27.83 — macro driving everything. If Hegseth’s escalation proves more accurate than Trump’s rhetoric, the relief trade unwinds violently.

Regime: Transitional — War Premium Deflating on Conflicting Signals. Monday’s $30 oil crash and S&P reversal suggest the acute crisis phase is ending. But the war is NOT over, Hegseth is escalating, breadth is wrecked, and smart money is hedging. The binary question: does reality align with Trump (“very complete”) or Hegseth (“most intense day”)? The market is betting on Trump. If that bet is wrong, the reversal will be violent.

Watch List

Trump vs. Hegseth — THE binary risk — “Very complete” vs. “most intense day of strikes.” The market is choosing to believe Trump. If today’s strikes produce a major escalation (Iranian retaliation, tanker hit, Hormuz mine deployment), the relief trade reverses instantly.

G7 SPR decision — “Not there yet” on Monday. Energy ministers meeting again this morning. A formal announcement of 300–400M barrels would cap oil at $75–80. Continued delay lets oil re-escalate on any negative headline.

CPI Wednesday 8:30 AM — THE binary event for rates. February CPI won’t reflect $100 oil but sets the pre-war baseline. Hot core = Fed completely trapped, bear flattener resumes. Benign = front-end rally continues, “inflation was contained” narrative.

Key Earnings This Week — Oracle (ORCL) today after close — first major tech/cloud report in the $100-oil-scare environment; AI/cloud demand signal vs. enterprise spending freeze. Adobe (ADBE) Thursday after close — software demand durability. Dollar General (DG) Thursday before open — low-income consumer barometer as gas prices surge. NIO today before open — China EV demand under oil shock.

Breadth expansion or failure — S5FD at 27.43 means 73% of S&P stocks are below their 5-day average despite Monday’s green close. If breadth doesn’t expand today, the rally is narrow and fragile. A break above 35 would signal genuine recovery; staying below 30 signals a bull trap.

Morning check: Monday was a historic reversal — the market chose to believe Trump’s “very complete” over the Pentagon’s “just begun.” Oil crashed $30 from $120. Gold is bouncing. Safe havens are working again. VIX below 30. But Hegseth says today will be the most intense strikes yet. The G7 hasn’t released reserves. Breadth is wrecked. Smart money is hedging. The regime is transitional and entirely headline-dependent. Oracle after the close and CPI tomorrow are the data catalysts. The war isn’t over — but the market is pricing like it is.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.