☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: RISK-OFF — ES 7,153.50 (−0.73%). WTI CROSSED $100 FOR THE FIRST TIME — $100.04 (+3.81%). BRENT $104.42 (+2.68%). THE OIL SHOCK IS LIVE. TRUMP DISSATISFIED WITH IRAN’S LATEST PROPOSAL — NUCLEAR PROGRAM THE STICKING POINT. IEA WARNS OF ‘UNPRECEDENTED SUPPLY SHOCK.’ MOVE EXPANDING TO 68.42 (+2.17%) — STILL SUB-BASELINE BUT RISING. GOLD CRASHED −2.08% TO $4,596 — FORCED LIQUIDATION EPISODE. NQ −1.31%. NIKKEI −1.82%. BEAR FLATTENER WITH 2Y +4.1 BPS. COR1M 9.20 — NEW ALL-TIME WAR LOW. FOMC DAY 1 BEGINS. TOMORROW: POWELL + MSFT AFTER CLOSE. CB CONSUMER CONFIDENCE 10 AM.

WTI crude crossed $100 for the first time in the war. The catalyst: stalled peace talks. Trump is reportedly dissatisfied with Iran’s latest proposal, with Tehran’s nuclear program remaining the central point of contention. Iran conveyed through Pakistan that hostilities could cease if Washington lifted the naval blockade, agreed to a revised Hormuz transit framework, and provided assurances against future military action. The US has expressed skepticism and is expected to respond with counteroffers — but no timeline is set. The International Energy Agency warned of a ‘potential unprecedented supply shock’ with Hormuz flows — typically 20% of global energy — remaining effectively halted. Now in its ninth week, the conflict has driven energy prices sharply higher: WTI +49.3% from pre-war $67.02 to $100.04; Brent +43.3% from $72.87 to $104.42.

The equity tape is in genuine risk-off. ES at −0.73% with NQ at −1.31% leading lower — the tech-semis rally from Monday’s SOXX +4.67% has FULLY reversed with SOXX now −1.34%. Nikkei −1.82% — Japan’s largest single-session decline in weeks. DAX −0.78%, EuroStoxx −0.62%. International markets are selling harder than the US. The Russell at −0.70% is underperforming ES at −0.73% for the first time in over a week — small-cap risk appetite has been hit by the oil shock. The Dow at +0.07% is the ONLY green index — defensive/value rotation holding the Dow while everything else sells.

Gold crashed −2.08% to $4,596 — the sharpest single-session gold decline since the Day 21 forced-liquidation episode. Silver −2.40%, Platinum −3.12%, Palladium −1.91%. The entire metals complex is in forced liquidation. Gold falling on an oil shock + risk-off session is the classic margin-call signature: investors selling gold positions to meet margin requirements on other positions. Copper −2.08% confirms the industrial-metals demand-destruction read. The metals crash is the session’s most alarming cross-asset signal — it tells you stress is spreading beyond equities into the broader portfolio complex.

MOVE expanded to 68.42 (+2.17%) — the second consecutive session of expansion from the 66.97 post-war low. But MOVE at 68.42 remains 4.79 points BELOW the 73.21 pre-war baseline. The bond market’s capitulation has NOT reversed — MOVE is rising but remains in sub-baseline territory. The question: is this a natural pre-FOMC vol expansion (expected ahead of any Fed decision) or the beginning of a genuine capitulation-reversal driven by $100 oil? If MOVE crosses 73.21 before tomorrow’s FOMC statement, the answer is clear. If MOVE holds sub-70 through the FOMC, the capitulation is intact.

The Number That Matters: WTI $100.04. The Psychological Threshold Has Been Breached. The Stagflation Narrative Returns To The Tape On The Eve Of The FOMC.

$100 WTI on the eve of the FOMC is the worst possible timing for the ‘look through’ thesis. When Powell faces the press tomorrow at 2:30 PM, he will be speaking into $100+ oil, 4.7% year-ahead inflation expectations, and the IEA warning of an ‘unprecedented supply shock.’ The data arc (seven consecutive constructive prints) and the Michigan upward revision (49.8 vs 47.6) had given the Fed perfect cover for stasis-with-dovish-lean. $100 oil removes that cover. Powell must now either: (1) Maintain the ‘look through’ framework despite $100 oil — which risks credibility if oil stays above $100; or (2) Signal concern about oil-driven inflation — which would reverse the front-end rate-cut pricing and potentially snap MOVE back above baseline. The market will parse every word of the statement and press conference for the oil-inflation signal.

The Setup: Bear Flattener — Risk-Off — Oil Shock Active. WTI $100. MOVE Expanding But Sub-Baseline. Gold In Forced Liquidation. FOMC Day 1. Tomorrow: FOMC Statement + Powell Press + MSFT After Close. Thursday: GDP + PCE + AAPL/AMZN/META. The Stagflation Narrative Has Returned.

2. OVERNIGHT SESSION RECAP

Monday Cash Session (Day 42 Close)

Monday’s session started with the SOXX +4.67% / NVDA +4.32% semis breakout that drove NQ leadership but the curve settled in a BEAR STEEPENER — 2Y +1.4 bps, 5Y +2.6 bps, 10Y +3.4 bps, 30Y +3.3 bps. The long end rising faster than the front end was the most bearish curve configuration of the post-ceasefire period. WTI rallied from $96.02 to the high-$97s during the session as peace talks stalled further. The Monday close set up the overnight oil breakout through $100.

Overnight — Oil Shock / Iran Talks Collapse

WTI broke through $100 overnight as Trump expressed dissatisfaction with Iran’s latest proposal. Iran submitted a three-part framework through Pakistan: (1) Lift the naval blockade, (2) Agree to a revised Hormuz transit framework, (3) Provide assurances against future military action. The US rejected the framework as insufficient, particularly on the nuclear dimension — Iran’s nuclear program remains the central obstacle to a deal. No timeline for counteroffers. The IEA issued its sharpest warning yet about ‘unprecedented supply shock’ risks from the sustained Hormuz closure. Brent surged to $104.42 with the Brent-WTI spread widening back to ~$4.38 as the international supply-chain premium re-engaged. Natural gas +7.02% — the entire energy complex bid aggressively.

Asia-Pacific

Nikkei −1.82% to 59,150 — the LARGEST single-session Japanese decline since the Day 32 ceasefire-collapse selloff. Topix −1.06%. The oil-shock pass-through to Japan is acute: Japan imports ~90% of crude, and $100+ oil directly compresses Japanese industrial margins. The Nikkei reversal from Monday’s +0.66% to Tuesday’s −1.82% is a 248 bp two-session swing — the widest of the post-ceasefire period.

Europe

DAX −0.78% to 24,033. EuroStoxx −0.62% to 5,776. European markets hit hard by the oil-shock read-through: $100+ WTI / $104+ Brent directly pressures European energy costs, industrial margins, and consumer purchasing power. European financials and industrials leading the selloff. EUR −0.23% to 1.1721 as the dollar firmed.

US Pre-Market

Day 61 of Operation Epic Fury. Q2 Day 20. Tuesday — FOMC Day 1. FOMC blackout active.

US FUTURES RED: YM 49,379 (+0.07% — ONLY green index, defensive bid), ES 7,153.50 (−0.73%), RTY 2,779.90 (−0.70%), NQ 27,080.50 (−1.31% — the WORST index). The NQ-Dow divergence (−1.31% vs +0.07% = 138 bp) is the widest of the week and confirms this is a TECH-LED SELLOFF driven by the oil shock reversing Monday’s semis rally.

MAG 7 FOUR GREEN / THREE RED — NVDA LEADING DESPITE SOXX SELLOFF: NVDA +4.00% (the second consecutive +4% day — NVDA is diverging from SOXX as the market treats NVDA as an AI-specific name rather than a cyclical semi). GOOG +1.81%. TSLA +0.63%. META +0.53%. MSFT +0.05% (essentially flat — maximum positioning caution into tomorrow’s earnings). AMZN −1.09% (positioning into Thursday’s earnings). AAPL −1.27% (still the structural weak link — now red 7 of 9 sessions). The Mag 7 at 4 green / 3 red while NQ is −1.31% says the non-Mag-7 tech complex is selling HARD — the selloff is concentrated in second-tier tech, software, and the semis broadening trade from Monday.

SECTORS BIFURCATED: XLF +0.76% leading (financials catching a bid ahead of the FOMC — rate-hike repricing supports net interest margins). XLC +0.23%. XLK +0.22% (barely green — NVDA +4% offsetting AAPL −1.27% and broader tech weakness). XLI +0.02%. XLU +0.02%. Five sectors green but mostly flat. XLE −0.18% (energy LAGGING despite $100 WTI — the demand-destruction discount is re-engaging HARD at the $100 level). XLRE −0.78% (rate-sensitive REITs selling on the bear flattener). XLP −1.07%. The XLE/WTI divergence (−0.18% vs +3.81% = 399 bp negative decoupling) is the WIDEST of the entire war — energy equities are pricing demand destruction at $100 rather than supply-constraint revenue gains.

FACTORS MIXED — VALUE LEADING, USMV LAGGING: VLUE +0.74% leading (value rotation alive). IJR +0.19%. MTUM −0.05%. SPHB −0.34%. USMV −0.54%. SPLV −0.22%. USMV-SPHB spread −0.20% (barely risk-on, compressing from Monday’s deeply negative −1.86%). The factor tape has rotated from Monday’s aggressive risk-on to Tuesday’s cautious value-rotation. Neither fully risk-on nor fully defensive — the market is in maximum-uncertainty positioning ahead of the FOMC.

CB CONSUMER CONFIDENCE 10 AM (consensus 89.0, prior 91.8) — the session’s domestic data event. The Michigan revised to 49.8 on Friday captured the ceasefire-extension relief. The CB index is more labor-market-sensitive and will capture both the oil-price stress and the still-tight labor market. A miss below 89.0 would compound the stagflation narrative into the FOMC. A beat would provide a counternarrative.

3. THE PRIOR DAY’S REGIME (34 Macro Price, Strength & Momentum Rankings)

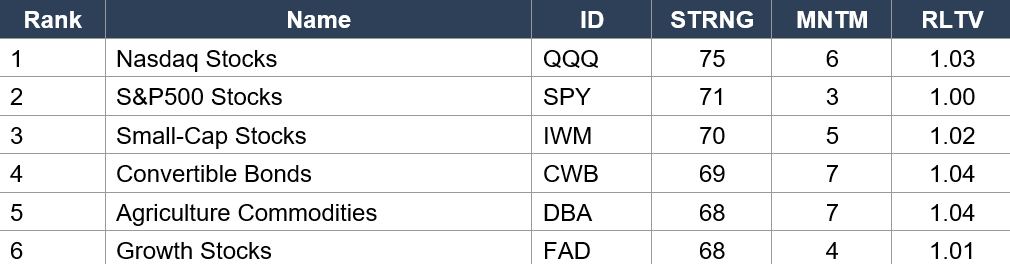

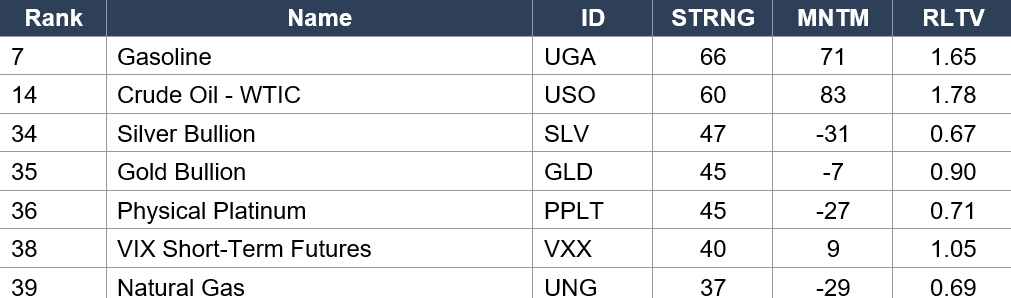

34 Macro Price, Strength & Momentum Rankings — Daily Close, Monday April 27. SPY Baseline: STRNG 71 | MNTM +3 | RLTV 1.00.

Asset Classes — Leaders

Asset Classes — Energy Extremes / Metals Collapse

Regime signal: QQQ (rank 1, STRNG 75) holds #1 for a sixth consecutive data set. SPY (rank 2, STRNG 71) stable. IWM (rank 3, RLTV 1.02) — small-cap outperformance persists in the data even as today’s −0.70% pre-market threatens it. Agriculture Commodities (DBA rank 5, MNTM +7, RLTV 1.04) enters the Leaders for the first time — the oil-shock agricultural pass-through (fuel costs, fertilizer, transport) is landing in the data. ENERGY: Crude Oil (USO rank 14, MNTM +83, RLTV 1.78) — momentum moderated slightly from +88 to +83 but RLTV remains extreme at 1.78. Today’s +3.81% WTI move to $100 will EXTEND this further. Gasoline (UGA rank 7, MNTM +71, RLTV 1.65). PRECIOUS METALS DEEPENING COLLAPSE: Silver (SLV MNTM −31, RLTV 0.67 — NEW WAR LOW for silver RLTV). Platinum (PPLT 0.71). Gold (GLD 0.90). Natural Gas (UNG MNTM −29, RLTV 0.69). Today’s forced-liquidation episode (gold −2.08%, silver −2.40%) will deepen these readings further. VIX (VXX MNTM +9, RLTV 1.05) — fear momentum moderating from +12, but today’s +6.38% VIX move will re-engage. Bitcoin (IBIT rank 16, MNTM −12, RLTV 0.85). Ethereum (ETHA rank 26, MNTM −21, RLTV 0.76).

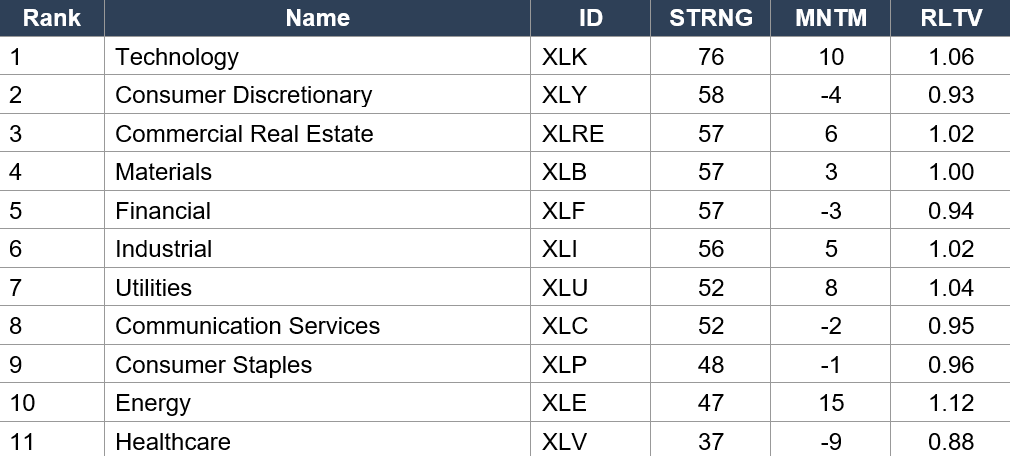

Sector ETFs — Full Ranking

Regime signal: Technology (XLK rank 1, STRNG 76, RLTV 1.06) holds #1 for a fifth consecutive data set. XLK is now 19 STRNG points above the #2 sector (76 vs 57) — the WIDEST leadership gap in the war’s data history. Today’s NQ −1.31% selloff will compress this gap. XLRE (rank 3, STRNG 57) dropped to rank 3 behind Consumer Discretionary. XLY at rank 2 (STRNG 58) despite MNTM −4 / RLTV 0.93 — the absolute STRNG holding while relative strength declines. Utilities (XLU rank 7, MNTM +8, RLTV 1.04) still high-RLTV. Energy (XLE rank 10, MNTM +15, RLTV 1.12 — SIXTH consecutive data set as highest-RLTV sector). Today’s −0.18% XLE on +3.81% WTI tells you the $100 oil threshold is BREAKING the energy Phoenix trade — at $100 WTI, the demand-destruction discount overwhelms the revenue-gain thesis. Health-Care (XLV rank 11, STRNG 37, MNTM −9, RLTV 0.88 — structural laggard continues).

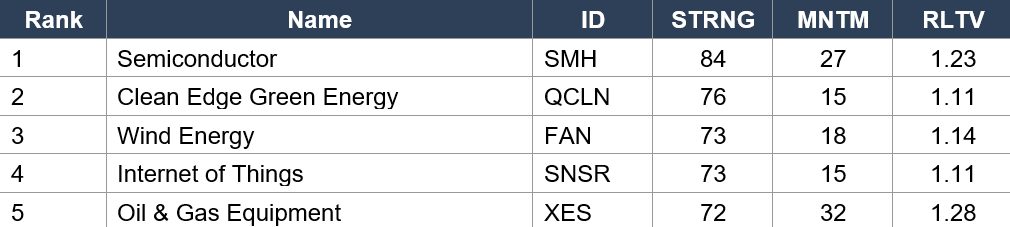

Industry ETFs — Top Leaders

Industry ETFs — Bottom Laggers

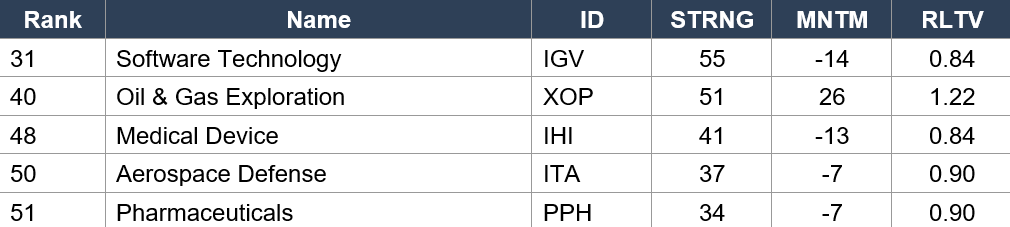

Regime signal: Semiconductor (SMH rank 1, STRNG 84, MNTM +27, RLTV 1.23) holds #1 industry for the SEVENTH consecutive data set — the longest industry-leadership streak of the entire war. Today’s SOXX −1.34% threatens to break this dominance. Oil & Gas Equipment (XES rank 5, MNTM +32, RLTV 1.28 — HIGHEST RLTV of any industry) — the energy value chain is in the Leaders. BUT: today’s XLE −0.18% on $100 WTI signals the RLTV may have peaked — the demand-destruction threshold has been hit. Software Technology (IGV rank 31, MNTM −14, RLTV 0.84) — unchanged, broken. Telecom (IYZ rank 36, MNTM +21, RLTV 1.17) dropped from Leaders to Laggers — the defensive-growth rotation reversed on Monday’s risk-on and today’s risk-off is not restoring it. Aerospace-Defense (ITA rank 50, RLTV 0.90) — defense at the bottom. Pharmaceuticals (PPH rank 51, STRNG 34 — LOWEST of any industry, RLTV 0.90) — pharma has displaced Medical Device at the absolute bottom.

4. MORNING DATA REACTION

10:00 AM — CB CONSUMER CONFIDENCE (Consensus 89.0, Prior 91.8). The Oil-Shock Consumer Read Into The FOMC.

The Conference Board index is more labor-market-sensitive than Michigan (which is more inflation/personal-finance-focused). The 89.0 consensus implies a −2.8 point decline from 91.8 — a modest deterioration reflecting the war’s continued consumer-stress impact. If the print misses below 89 (say 85-87), the stagflation narrative into the FOMC intensifies and the front-end hawkish repricing (2Y +4.1 bps) extends. If the print beats (90+), the labor-market-strength narrative provides a partial counterweight to $100 oil. For tomorrow’s FOMC, Powell will have both Michigan (49.8 revised, record low) and CB confidence on his desk — both readings will frame his view of consumer resilience under the oil shock.

Overnight — WTI Crossed $100. Iran’s Proposal Rejected. Nuclear Program The Sticking Point. IEA Warns Of ‘Unprecedented Supply Shock.’

The oil-shock catalyst: Iran submitted a three-part proposal through Pakistan — lift the blockade, revised Hormuz framework, no-future-attack assurances. Trump rejected it as insufficient, with the nuclear program the central obstacle. The US is expected to respond with counteroffers but no timeline is set. Iran’s FM Araghchi continues to call the blockade ‘an act of war.’ The IEA warned of ‘unprecedented supply shock’ with Hormuz flows remaining halted. WTI trajectory: $81 (Friday Apr 17 crash) → $87.52 (Tuesday) → $90.80 (Wednesday) → $95.79 (Thursday) → $96.02 (Monday) → $100.04 (today). The oil market has retraced the entire Friday de-escalation crash and then some — the frozen-conflict ‘new normal’ is $100 oil, not $85.

Gold $4,596 (−2.08%) — Forced Liquidation Episode. The Fourth Major Gold Selloff Of The War.

Gold at $4,596 is the sharpest single-session decline since the Day 21 forced-liquidation episode that drove gold to its war low of $4,376. Silver −2.40%, Platinum −3.12%, Palladium −1.91%, Copper −2.08%. The entire metals complex is in forced liquidation — margin calls on equity/oil positions forcing gold sales. This is NOT a gold-bearish signal (gold should rise on inflation/oil fears) — it is a liquidity-stress signal. When gold sells alongside equities on an inflationary catalyst, the market is in portfolio-level stress. Cumulative gold from pre-war $5,311.60 is now −$715.60 / −13.5% — the deepest gold drawdown of the war.

5. THE DYRH READ

Regime: Bear Flattener — Risk-Off — Oil Shock Active. WTI $100 crosses the psychological threshold on stalled peace talks. MOVE expanding to 68.42 (+2.17%) but still sub-baseline (73.21). Gold in forced liquidation (−2.08%). Bear flattener with 2Y +4.1 bps leading — hawkish front-end repricing on $100 oil. COR1M 9.20 — NEW ALL-TIME WAR LOW — stock-picking extreme despite macro headlines. FOMC Day 1 begins. Tomorrow: FOMC statement + Powell press + MSFT after close. CB Consumer Confidence 10 AM. Confidence: MODERATE — $100 oil introduces acute inflation-risk uncertainty into the FOMC read.

Yield Curve: Bear Flattener — Front Rising Fastest. 2Y +4.1 bps to 3.840%. The Hawkish Repricing Is Acute On $100 Oil.

All yields rising: 2Y +4.1 bps to 3.840% (LARGEST single-session 2Y move since the Day 38 Retail Sales beat), 5Y +4.0 bps to 3.988%, 10Y +2.6 bps to 4.366%, 30Y +1.9 bps to 4.964%. The front end rising fastest confirms the bear flattener: the market is REMOVING rate-cut probability as $100 oil re-engages near-term inflation concerns. The 2Y at 3.840% is the HIGHEST since mid-March — the entire post-ceasefire front-end rally has been given back. The 30Y at 4.964% approaching the 5.00% level that was touched during the Day 22 bond crisis. If 30Y crosses 5.00% with MOVE rising toward 73.21, the Day 21-22 bond crisis configuration partially returns.

MOVE 68.42 (+2.17%) — Expanding For Second Session But Still Sub-Baseline. 4.79 Points From The 73.21 Reversal Level.

MOVE trajectory: 66.97 (post-war low Friday) → 68.42 (Tuesday, +2.17%). Two consecutive sessions of expansion. The 73.21 baseline is 4.79 points above. MOVE at 68.42 is: (1) Normal pre-FOMC vol expansion — MOVE typically rises 2-3 points into any FOMC meeting; (2) Compounded by $100 oil uncertainty. If MOVE holds below 70 through tomorrow’s FOMC statement, the capitulation thesis survived the oil-shock test. If MOVE breaks 70 before the statement, the FOMC faces elevated rates-vol when Powell speaks — a much more constrained communication environment.

COR1M 9.20 (−17.64%) — NEW ALL-TIME WAR LOW. Below The Prior 10.94 Record. Stock-Picking Is Extreme.

COR1M crashed from 11.17 to 9.20 — a dramatic −17.64% single-session decline and a NEW ALL-TIME WAR LOW, breaking the prior 10.94 record set on April 17. The sub-10 reading is extraordinary: COR1M at 9.20 means every name in the S&P 500 is moving on its own story with essentially zero macro-headline correlation. This is happening on a day with WTI at $100, gold in forced liquidation, and a −0.73% ES selloff — meaning the selloff is IDIOSYNCRATIC rather than systematic. The NVDA +4.00% / AAPL −1.27% / gold −2.08% / WTI +3.81% divergence pattern confirms: there is no single macro trade today. Every asset is trading its own story.

ES 7,153.50 (−0.73%) — Risk-Off. +3.9% Above Pre-War Baseline. The Pullback Is Contained But On Eve Of FOMC.

ES at −0.73% is the largest single-session decline since the Day 37 ceasefire-expiration positioning week. But at 7,153.50, ES is STILL +271.88 / +3.9% above the pre-war 6,881.62 baseline. The pullback has not breached any critical support levels. The −0.73% decline is proportionate to the $100 oil shock — the market is repricing the inflation-risk input to the FOMC without panicking. The Dow at +0.07% green while everything else sells confirms this is a tech/growth selloff, not a broad market meltdown.

6. THE GAME PLAN

Today’s Key Events: CB Consumer Confidence 10 AM (consensus 89.0, prior 91.8). FOMC Day 1 begins (2-day meeting). Visa, PayPal, GE Aerospace Q1 earnings. TOMORROW WEDNESDAY APR 29: FOMC statement 2 PM + Powell press 2:30 PM + MSFT fiscal Q3 after close. THURSDAY APR 30: GDP Q1 8:30 AM (+2.2% est) + Core PCE m/m 8:30 AM (+0.3% est) + ECI + AAPL/AMZN/META after close. FRIDAY MAY 1: ISM Manufacturing + Mastercard + Chevron.

The Bull Case:

MOVE at 68.42 is still 4.79 points sub-baseline — the bond market’s capitulation has NOT reversed despite $100 oil. ES still +3.9% above pre-war. COR1M at 9.20 = extreme stock-picking (the selloff is idiosyncratic, not systematic). NVDA +4.00% — AI demand continues regardless of oil price. Mag 7 at 4 green / 3 red — tech leadership rotating within the complex, not collapsing. Seven consecutive constructive data prints. Michigan revised to 49.8. Pre-FOMC vol expansion is NORMAL and typically reversed post-statement. If Powell maintains ‘look through’ framework tomorrow, the front-end hawkish repricing reverses and MOVE compresses. MSFT after close Wednesday — if Azure re-accelerates, the tech rally resumes. GDP at +2.2% Thursday = growth confirming activity. Core PCE at +0.3% Thursday = inflation cooling. The oil shock could be temporary if Iran re-engages — the ceasefire is extended indefinitely and the diplomatic framework exists.

The Bear Case:

WTI AT $100 — the stagflation threshold. Brent at $104. IEA warning of ‘unprecedented supply shock.’ Gold in forced liquidation (−2.08%) — portfolio stress spreading beyond equities. 30Y at 4.964% approaching the 5.00% Day 22 crisis level. Bear flattener with 2Y +4.1 bps — the entire front-end rate-cut pricing being removed. VIX +6.38% to 19.17. SOXX −1.34% reversing Monday’s +4.67%. NQ −1.31%. Nikkei −1.82%. AAPL −1.27% (7 of 9 sessions red). XLE −0.18% on WTI +3.81% = 399 bp negative decoupling — the WIDEST of the war — energy equities pricing demand destruction at $100. If CB confidence misses badly, the stagflation narrative hardens into the FOMC. If Powell signals concern about $100 oil tomorrow, MOVE could snap above 73.21 and the capitulation reverses. Iran’s proposal rejected — no timeline for counteroffers. The frozen conflict is not frozen — it is RE-ESCALATING economically even without kinetic events. Core PCE Thursday at +0.4% (above consensus) would be the catalyst that forces the Fed’s hand.

Regime: Bear Flattener — Risk-Off — Oil Shock Active. $100 WTI on the eve of the FOMC is the market’s way of saying: ‘the stagflation narrative is back, and the Fed’s response determines everything.’ The bond market (MOVE 68.42, still sub-baseline) says the capitulation can survive $100 oil if Powell validates the ‘look through’ framework. The equity market (ES −0.73%, NQ −1.31%) says $100 oil is being priced as a near-term headwind. The metals complex (gold −2.08%) says portfolio stress is real. The correlation data (COR1M 9.20) says the stress is idiosyncratic, not systematic. Tomorrow is everything: FOMC statement at 2 PM, Powell press at 2:30 PM, MSFT after close. If Powell looks through $100 oil + MSFT delivers: the rally resumes. If Powell blinks + MSFT disappoints: the post-ceasefire regime breaks.

Watch List

Tomorrow FOMC + Powell + MSFT — The Single Most Important Day Of The War

FOMC statement 2 PM (consensus hold at 3.75%). Powell press 2:30 PM. The $100 oil question: does Powell maintain ‘transitory war shock / look through’ or signal concern? MSFT fiscal Q3 after close — Azure growth, Copilot monetization, capex guidance. If Powell is dovish + MSFT delivers: NQ recovers everything. If Powell is hawkish + MSFT disappoints: the 10.8% rally from Day 22 lows is at risk.

CB Consumer Confidence 10 AM — The Stagflation Gauge

Consensus 89.0 vs prior 91.8. A miss below 87 would be the weakest since mid-2022 and would compound the $100 oil / stagflation narrative into the FOMC. A beat above 90 provides partial cover for the ‘look through’ framework.

30Y Yield At 4.964% — The 5.00% Level

The 30Y touched 5.00% on Day 22 during the bond crisis that produced VIX 31.05 and the war’s most acute cross-asset stress. If 30Y crosses 5.00% today or tomorrow, the bond market enters the crisis-adjacent zone regardless of MOVE’s sub-baseline position. Watch the long end as the canary.

Gold Forced Liquidation — Stress Spreading Or Contained?

Gold −2.08% on an oil-shock day is forced liquidation, not fundamental gold selling. If gold stabilizes tomorrow, the stress was a one-day margin event. If gold continues to sell into the FOMC, portfolio stress is deepening and the Day 21-22 forced-liquidation dynamic returns.

Morning check: Day 61. The war is sixty-one days old and WTI just crossed $100. The stagflation narrative is back on the tape on the eve of the FOMC. Gold is in forced liquidation. The bear flattener has 2Y at 3.840% — the highest since mid-March. Brent at $104.42. Nikkei −1.82%. And yet — MOVE at 68.42 is still sub-baseline. COR1M at 9.20 is a new all-time war low. The selloff is idiosyncratic, not systematic. NVDA is +4.00%. The Dow is green. The bond market’s capitulation has not reversed. Tomorrow is everything. FOMC statement. Powell press conference. MSFT after close. $100 oil on the screen when Powell speaks. The ‘look through’ framework faces its ultimate test. If the framework holds, the rally resumes. If the framework breaks, the stagflation regime returns. There is no middle ground. This is the day the war’s market legacy is decided.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.