☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: The weekend changed the war’s economic calculus. The US “totally obliterated every military target” on KHARG ISLAND — the terminal handling ~90% of Iran’s crude oil exports — the single most significant escalation from a global oil supply perspective. Oil spiked Sunday: Brent to ~$105.66, WTI above $100.64 (highest since July 2022). But by Monday pre-market, oil is PULLING BACK: WTI $95.87 (−2.88%), Brent $103.28 (flat). Why? Several tankers SUCCESSFULLY TRANSITED the Strait of Hormuz over the weekend — the first meaningful commercial passage since the war began. Iran’s FM Araghchi said Hormuz is “open, but closed to our enemies” — a nuanced shift from total closure. Treasury Secretary Bessent confirmed the US is “allowing Iranian oil tankers to pass through.” No shipping incidents for 3 days. This combination — the BIGGEST military escalation paired with a Hormuz DE-ESCALATION in shipping — has created the most constructive risk-on setup since Day 8. ES +0.95%, Nikkei +1.94% (best of the series), Russell +1.26% back above 2,500, ALL 7 Mag 7 green (META +3.08% on layoff report, NVDA +1.61% on GTC). SPHB leading at +1.38% — the factor signal ABSENT from Friday’s dead cat. Bonds rallying for the first time since Day 8: 30Y at 4.874% (−3.4 bps from 4.908% series high). DXY BACK below 100. VIX −7.91% (largest single-session decline). But gold is down for a SIXTH consecutive session toward $5,000 (−5.3% cumulative) — forced liquidation unbroken. Empire State Manufacturing (released 8:30 AM): −0.20 vs. 3.9 consensus and 7.1 in February — dipped into NEGATIVE territory for the first time since December, the first hard manufacturing survey capturing the war’s impact. Fed week begins with six central bank decisions in 48 hours (Wed–Thu).

The Number That Matters: Empire State Manufacturing at −0.20 — the first hard manufacturing data capturing the war impact. The survey was collected approximately March 2–10, during the conflict. A flip from +7.1 to −0.20 confirms the war is already hitting manufacturing activity. Shipments declined, delivery times lengthened, supply availability worsened. This aligns with the −92K NFP and GDP 0.7% narrative: the economy was fragile before the war, and the war is now showing up in the real-time data. Combined with Friday’s Michigan Sentiment at 55.5 (2nd percentile of history, expectations down 7.5%), the consumer and manufacturing data are both confirming the growth leg of the stagflation diagnosis.

The Setup: The regime is at a potential inflection point. This rally has FIVE characteristics that Friday’s dead cat lacked: (1) SPHB leading at +1.38%, (2) bonds rallying across the curve, (3) DXY retreating below 100, (4) Russell/small caps participating, (5) VIX dropping −7.91%. The Hormuz narrative is shifting from “permanently closed” to “selectively open.” But gold’s sixth consecutive decline says forced liquidation is unbroken. Brent still above $100 for a third session. Empire State at −0.20 confirms the war is hitting manufacturing. Breadth remains catastrophic at every timeframe beyond 5-day. The Fed on Wednesday is the ultimate test: GDP 0.7%, Core PCE 3.1%, oil above $95 — an impossible mandate. If this rally survives to Wednesday, the market may have found a floor at the 200-day MA area (~6,582–6,636).

2. OVERNIGHT SESSION RECAP

Asia-Pacific

Nikkei +1.94% — the BEST international index move of the entire series. TOPIX +0.68%. Japan bouncing hard as the Hormuz tanker transits signal potential reopening — Japan is the most energy-import-dependent major economy and benefits disproportionately from any Hormuz de-escalation.

Europe

DAX +0.61%, Euro Stoxx +0.45%. Europe modestly green. The Hormuz shipping signals and oil pullback are providing relief, but Brent at $103 remains well above pre-war levels. European equities have significantly less bounce than US or Japan — suggesting the market views European energy dependence as structurally more vulnerable.

US Pre-Market

Day 15 — Kharg Island Struck But Hormuz Signals De-Escalating. US “totally obliterated every military target” on Kharg Island (90% of Iran’s oil exports). Oil spiked Sunday to Brent $105.66, WTI $100.64 — then pulled back as tankers successfully transited Hormuz. Iran FM: Hormuz “open but closed to our enemies.” Bessent: US allowing Iranian tankers through the Strait. No shipping incidents for 3 days. Trump called for international naval coalition (China, France, Japan, South Korea, UK). Trump said Iran “wants a deal”; Iran FM: “we never asked for a ceasefire.” Israel running critically low on ballistic missile interceptors. Death toll 2,200+ across Middle East. Pope Leo XIV called for ceasefire.

Empire State Manufacturing (released 8:30 AM): −0.20 vs. 3.9 consensus and 7.1 in February — dipped into NEGATIVE for the first time since December. This is the FIRST hard manufacturing survey capturing the war’s impact (collected approximately March 2–10). Shipments declined, delivery times lengthened, supply availability worsened. New orders increased modestly but the headline flip from expansion to contraction confirms the war is already hitting manufacturing activity.

Friday’s data recap (March 13): Michigan Consumer Sentiment (preliminary March): 55.5 vs. 55.0 forecast, 56.6 prior — 2nd percentile of history. Sentiment fell for the first time in four months to the lowest of 2026. Interviews showed improvement BEFORE the war, but lower readings during the nine days after completely erased gains. Expectations down 7.5%. 1-year inflation expectations held at 3.4% (ending six months of declines). 5-year expectations edged down to 3.2% from 3.3%. Q4 GDP revised to 0.7%. Core PCE at 3.1%. The stagflation trifecta confirmed on Friday: weak growth + sticky inflation + collapsing consumer confidence.

Prior session (March 13 close): S&P −0.61% (4th consecutive decline, 3-week losing streak, 3.42% off ATH). Brent $103.14 (2nd consecutive close >$100). WTI $98.71. 30Y 4.908% (new series high). DXY 100.160 (broke 100). Gold −1.25% to $5,061.7 (5th consecutive decline, −4.7% cumulative). All 7 Mag 7 red for 2nd straight session. 78-point ES intraday reversal (dead cat killed). COR1M 37.21 (series high). SKEW 137.76.

This week — THE BIGGEST WEEK OF THE SERIES: Today 9:15 AM: Industrial Production + Capacity Utilization (February). Today 10:00 AM: NAHB Housing Market Index (March). Today: Nvidia GTC conference begins (Jensen Huang keynote). Tuesday: Pending Home Sales. Wednesday: PPI (February, rescheduled from March 12) 8:30 AM; FOMC Decision 2:00 PM + Economic Projections + Dot Plot; Powell Press Conference 2:30 PM; Bank of Canada decision. Thursday: Bank of Japan (tentative), SNB, Bank of England, ECB decisions; Jobless Claims; Philly Fed Manufacturing; New Home Sales. SIX central bank decisions in 48 hours. Earnings: Dollar Tree (today).

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 03/13/26. Provided for informational purposes only; not as investment advice.

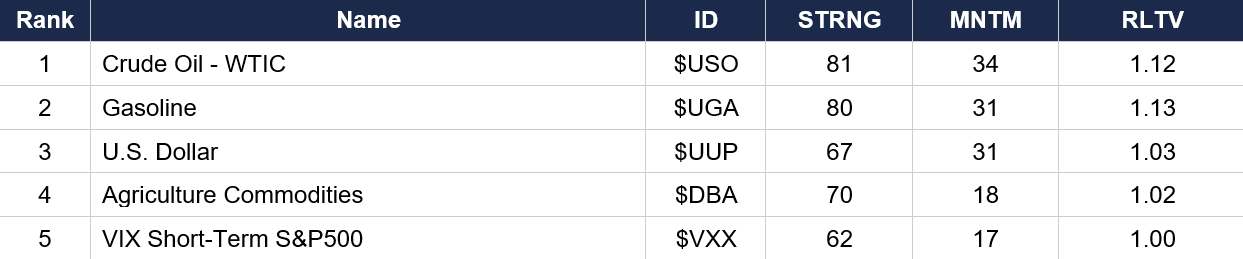

Asset Classes — Top 5

Asset Classes — Bottom 5

Regime signal: Crude oil holds rank 1 with RLTV 1.12. Dollar ($UUP) has surged to rank 3 with MNTM 31 (from 24) — the highest dollar momentum of the series, reflecting the peak safe-haven bid (DXY briefly above 100 Friday). Bitcoin ($IBIT rank 7, MNTM 12) and Ethereum ($ETHA rank 8, MNTM 13) maintaining crypto haven status. Gold ($GLD rank 10, MNTM −9) continues deteriorating — negative momentum during a war confirms forced liquidation. S&P ($SPY rank 19, MNTM −24) and Nasdaq ($QQQ rank 14, MNTM −12) both deeply negative. EM Bonds ($EMB, MNTM −53) is the worst momentum on the entire board — the deepest negative reading of the series for any asset. Corporate Bonds ($LQD, MNTM −46) confirm the credit complex is under severe stress.

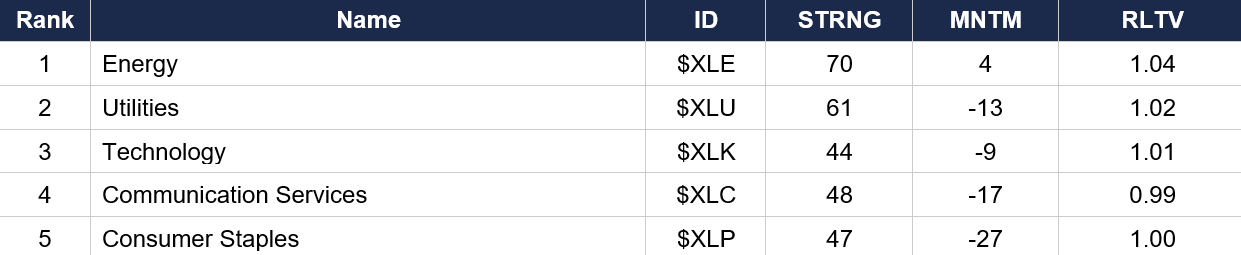

Sector ETFs — Top 5

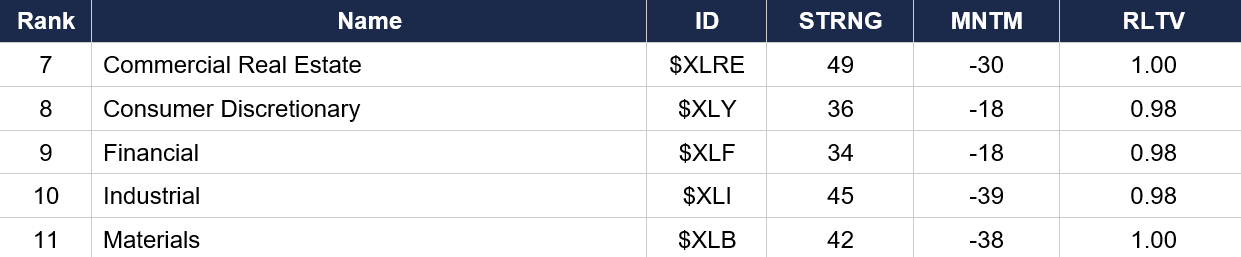

Sector ETFs — Bottom 5

Regime signal: ALL 11 sectors have NEGATIVE momentum — second consecutive reading of universal sector weakness. Energy ($XLE, MNTM 4) is the ONLY sector with single-digit negative or positive momentum. Technology ($XLK, MNTM −9) continues deteriorating. Industrial ($XLI, MNTM −39) and Materials ($XLB, MNTM −38) remain the worst sectors. Consumer Staples ($XLP) has risen to rank 5 (from 9) as a defensive trade — but at MNTM −27, even the defensive rotation is losing momentum. Consumer Discretionary ($XLY, MNTM −18) has dropped to rank 8 — cyclical exposed to the consumer spending crunch.

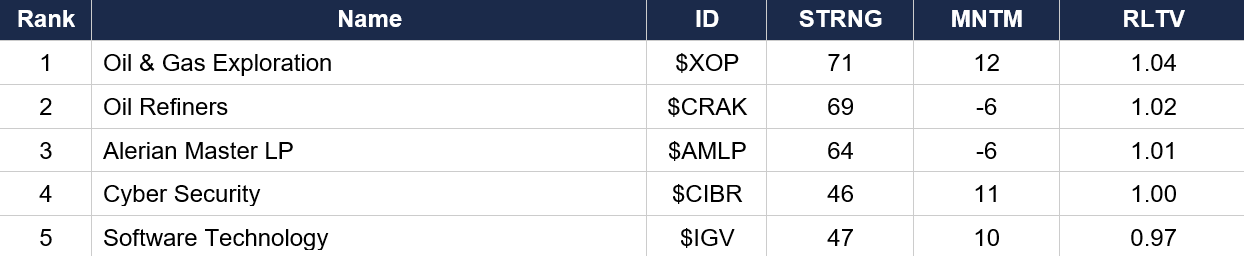

Industry ETFs — Top 5

Industry ETFs — Bottom 5

Regime signal: Oil & Gas ($XOP, MNTM 12) has re-strengthened at rank 1. Alerian MLP ($AMLP rank 3) confirms the midstream energy trade. Software ($IGV rank 5, MNTM 10) and Cyber Security ($CIBR rank 4, MNTM 11) maintain positive momentum — the tech/digital complex is the only non-energy positive-momentum group. Semiconductor ($SMH rank 25, MNTM −19) has been devastated — from rank 16 to rank 25, reflecting the selling in SOXX. Aerospace-Defense ($ITA rank 28, MNTM −24) continues plummeting despite the war. Shipping ($BOAT rank 38, MNTM −45) remains catastrophic from Hormuz closure. Home Construction ($ITB, MNTM −34) and Homebuilder ($XHB, MNTM −34) at the absolute bottom as 30Y yields at 4.87% crush housing.

4. MORNING DATA REACTION

Empire State Manufacturing (released today 8:30 AM, March data): −0.20 vs. 3.9 consensus and 7.1 in February. Dipped into NEGATIVE territory for the first time since December. This is the FIRST hard manufacturing survey capturing the war’s impact — the survey was collected approximately March 2–10, during the conflict. New orders increased modestly but shipments declined, delivery times lengthened, and supply availability worsened. The headline flip from expansion to contraction confirms the war is already hitting NY State manufacturing activity in real-time. This aligns with the −92K NFP and GDP 0.7% narrative: the economy was fragile before the war, and now the war is showing up in hard data.

Friday’s data recap — the Stagflation Trifecta: (1) Q4 GDP revised to 0.7% from 1.4% (the economy was barely growing pre-war). (2) Core PCE at 3.1% YoY, RISING from 3.0% (inflation moving in the wrong direction). (3) Michigan Consumer Sentiment at 55.5, 2nd percentile of history, expectations down 7.5% (consumer confidence collapsing). 1-year inflation expectations held at 3.4%, ending six months of declines. GDP at 0.7% + Core PCE at 3.1% + Michigan at 55.5 = textbook stagflation confirmed in the hard data, ALL pre-war.

Pending today: Industrial Production + Capacity Utilization (February) at 9:15 AM. NAHB Housing Market Index (March) at 10:00 AM. Wednesday is the MAIN EVENT: PPI (February, rescheduled from 3/12 due to government shutdown) at 8:30 AM; FOMC Decision 2:00 PM with Economic Projections, Dot Plot, and Statement; Powell Press Conference 2:30 PM. The Fed faces an impossible mandate: GDP 0.7% says cut, Core PCE 3.1% says don’t, oil above $95 says can’t. September rate cut now off the table; only December priced in; some desks see NO cuts in 2026.

JOLTS January (released Friday March 13 at 10:00 AM, with annual CES revisions): JOLTS data incorporated the annual benchmark update. This release was the first to align with the large downward revisions to employment from the CES benchmark. The revised JOLTS landscape paints a weaker labor market picture, consistent with the −92K NFP and the broader deterioration narrative.

5. THE DYRH READ

Regime: Stagflationary Crisis — Potential Inflection; Genuine Risk-On Bounce with SPHB Leading; Fed Week Begins. Confidence: Moderate-High on characterization.

Yield Curve: Bull Flattener — First Genuine Bond Rally Since Day 8. Yields falling across the entire curve: 5Y leading at −5.8 bps, 2Y −5.4 bps, 10Y −4.9 bps, 30Y −3.4 bps (from 4.908% series high to 4.874%). This is the first significant flight-to-quality bond bid since the post-panic Day 8 rally. The bull flattener signal: front end pricing rate cuts sooner (growth fears) while the long end retreats modestly. In context: weekend tanker transits suggest Hormuz may partially reopen (deflating the inflation premium), oil pulling back from $105+ spike, pre-positioning ahead of Wednesday’s Fed. Cumulative: 10Y +28.5 bps from pre-war (down from peak +33.4). MOVE at 91.17 pulled back from the 95.30 panic peak — if it stays below 90 through the Fed, the “bond crisis” label can be retired.

Oil: Kharg Island — The Double-Edged Sword. WTI −2.88% to $95.87 (from $100+ Sunday spike). Brent flat at $103.28 (third session near/above $100). The Brent-WTI spread has widened to ~$7.41 — the widest of the series — reflecting global (Brent/Hormuz disruption) vs. domestic (WTI/US production insulated) supply dynamics. The Kharg Island strike is paradoxically deflationary for near-term oil supply anxiety: if Iran’s export capacity is “obliterated,” there’s LESS oil to be disrupted through Hormuz, which may accelerate reopening. Gold −0.65% to $5,028.8 — SIXTH consecutive decline, −5.3% cumulative, $5,000 in sight. A breach below $5,000 during a shooting war would be the single most extreme forced-liquidation signal of the entire series.

Equities: Genuine Bounce or Dead Cat? ES +0.95% to 6,699.25 — recovers 152% of Friday’s loss, the FIRST session where the bounce exceeds the prior decline. Nikkei +1.94% (best of series). Russell +1.26% back above 2,500. All 7 Mag 7 green: META +3.08% (20% layoff report), NVDA +1.61% (GTC), TSLA +1.23%. SPHB +1.38% LEADING all factors — the signal absent from Friday’s dead cat. RSP +0.92% (equal weight participating). All 11 sectors green, XLK leading at +1.38%, XLE lagging at +0.40%. SOXX +2.23% on Nvidia GTC. But: breadth remains catastrophic beyond 5-day (S5TW 21.27, S5TH 47.91 below 50, R2TH 47.20 below 50). Bear market by breadth even though index drawdown is only 2.65%.

FX: Dollar Below 100, All G10 Green, BTC Surging. DXY at 99.705 (−0.40%) — BACK BELOW 100 after just one session above. When the dollar weakens while equities AND bonds rally simultaneously, it signals a return to normal risk appetite rather than “sell everything for cash.” BTC +3.68% to $73,950 — strongest crypto move of the series. All G10 currencies green vs. dollar: NZD +0.91%, AUD +0.74%, EUR +0.40%, JPY +0.40%, CHF +0.36%. The FX picture is the most constructive since Day 8.

Volatility: VIX Largest Single-Session Decline. VIX at 25.04 (−7.91%) — the largest VIX decline of the entire series. VIX falling below 26 while S&P bounces +0.95% is consistent with genuine risk-on rather than a head-fake. MOVE at 91.17 (−4.33%) pulled back from the 95.30 peak. Bond volatility moderating. But VIX at 25 is still elevated above the fear threshold (20). COR1M at 37.21 (series high) and SKEW at 137.76 from Friday — the structural stress indicators haven’t reset.

6. THE GAME PLAN

Today’s Key Events: Empire State Manufacturing released at 8:30 AM (−0.20 vs. 3.9 consensus). Industrial Production + Capacity Utilization 9:15 AM. NAHB Housing Index 10:00 AM. Nvidia GTC keynote (Jensen Huang). Dollar Tree earnings. Wednesday: PPI (Feb) 8:30 AM; FOMC Decision 2:00 PM + Dot Plot + Projections; Powell presser 2:30 PM; Bank of Canada. Thursday: BOJ, SNB, BOE, ECB; Jobless Claims; Philly Fed; New Home Sales. SIX central bank decisions in 48 hours.

The Bull Case: This rally has FIVE characteristics Friday’s dead cat lacked: SPHB leading, bonds rallying, DXY retreating, small caps participating, VIX dropping. Tankers successfully transited Hormuz — the “permanently closed” narrative is breaking. Iran’s FM offering nuanced Hormuz stance (“open but closed to enemies”) vs. prior “not one liter.” No shipping incidents for 3 days. Oil pulling back from $105+ despite the Kharg Island strike. Nikkei +1.94% — Japan confidence returning. SOXX +2.23% on GTC. META +3.08% on restructuring. If the rally survives to Wednesday, the 200-day MA area (~6,582–6,636) becomes the floor. Bonds rallying into the Fed is dovish pre-positioning.

The Bear Case: Empire State at −0.20 confirms the war is hitting manufacturing — first contraction since December. Gold’s sixth consecutive decline toward $5,000 (−5.3% cumulative during a shooting war) means forced liquidation is UNBROKEN. Brent still above $100 for a third session. Breadth remains catastrophic at every timeframe beyond 5-day. COR1M at 37.21 (series high) and SKEW at 137.76 (crashed from 152) — the structural stress hasn’t reset. Kharg Island is the BIGGEST military escalation of the war. Iran says it “never asked for a ceasefire” and the war continues. Friday’s dead cat reversed by 11 AM — the most recent precedent. If the Fed sounds hawkish on Wednesday, this rally evaporates. Michigan at 55.5 (2nd percentile) confirms the consumer is in distress. 30Y still at 4.874% — well above pre-war.

Regime: Stagflationary Crisis — Potential Inflection. The rally has genuine risk-on characteristics (SPHB, bonds, DXY, VIX all confirming) but forced liquidation in gold is unbroken, Empire State just flipped negative, breadth is catastrophic beyond 5-day, and the Fed’s impossible mandate on Wednesday is the ultimate test. If ES survives to Wednesday above 6,636 (200-day MA), the market has potentially found a floor. If gold breaches $5,000 or the Fed surprises hawkish, the crisis deepens.

Watch List

Empire State at −0.20 — war hitting manufacturing — First hard manufacturing data confirming the war’s impact. Combined with −92K NFP, GDP 0.7%, Michigan 55.5 — the growth leg of stagflation is being validated in real-time. Watch Industrial Production at 9:15 AM for confirmation.

FOMC Wednesday — THE defining event — GDP 0.7%, Core PCE 3.1%, oil >$95. Hold universally expected. The dot plot revisions, statement language on energy/inflation, and Powell’s press conference determine whether this rally extends or dies. September cut now off the table. Some desks see NO cuts in 2026.

Gold approaching $5,000 — Six consecutive declines, −5.3% cumulative during a shooting war. A breach below $5,000 would be psychologically devastating and confirm forced liquidation as the dominant precious metals dynamic. If gold stabilizes above $5,000 while equities rally, the liquidation cycle may be exhausting.

Key Earnings + Catalysts — Nvidia GTC keynote today — the AI counter-narrative to the war/stagflation story. SOXX +2.23% pre-market signals the semiconductor trade is attempting to reassert. Dollar Tree today. PPI Wednesday 8:30 AM (rescheduled from March 12).

Hormuz tanker transits — will they continue? — The most bullish development of the weekend. If commercial shipping continues through Hormuz without incidents, the oil premium deflates further. If attacks resume, the relief rally dies. No incidents for 3 days per UK maritime agency.

Morning check: the strongest risk-on signal since Day 8, with all five confirmation markers present — SPHB leading, bonds rallying, DXY retreating, VIX dropping, small caps participating. But Empire State just flipped negative at −0.20 — the war is hitting manufacturing. Gold’s sixth decline toward $5,000 says forced liquidation isn’t over. Breadth is catastrophic. The Fed meets in 48 hours with no good options. This rally has better bones than any bounce since Day 8, but the market will tell us by close whether it’s real or another dead cat.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.