☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: TRUMP ANNOUNCES 5-DAY PAUSE ON ENERGY STRIKES. At approximately 7:10 AM EST, the President posted on Truth Social: the US and Iran have had “VERY GOOD AND PRODUCTIVE CONVERSATIONS regarding a complete and total resolution of our hostilities in the Middle East.” He ordered the Pentagon to postpone ALL strikes against Iranian power plants and energy infrastructure for five days, “subject to the success of the ongoing meetings and discussions.” This replaces Saturday night’s 48-hour ultimatum that would have expired tonight. Oil CRASHED: Brent −7.62% to $103.64 (largest single-session drop of the war, down from Friday’s $112.19 settlement high), WTI −6.79% to $91.56 (back below $100). Equities surging: ES +1.50%, NQ +1.50%, RTY +2.44% (small caps leading), Nikkei +3.41% (best international session of the war). HOWEVER — Iran’s Foreign Ministry responded within an hour: “There is no dialogue between Tehran and Washington” — called the pause an attempt to “reduce energy prices and buy time.” Behind the scenes: Turkey, Egypt, and Pakistan have been passing messages between US envoy Witkoff and Iranian FM Araghchi over the past two days. Whether Trump directly spoke with Iran or not, the 5-day pause creates a defined diplomatic window. Israel continued striking Tehran even during the pause announcement. The bond market is NOT buying it: 10Y at 4.386% (+0.2 bps), essentially unchanged from Friday’s war high. MOVE at 108.84 (Friday print) — the most important number to watch at the open. Gold is in FREEFALL: −4.14% to $4,385 (worst single session of the war, cumulative −17.4% from pre-war). This is disproportionate to a de-escalation trade and suggests forced liquidation continues on autopilot regardless of war trajectory. All 7 Mag 7 green. 10 of 11 sectors green (XLE the only red). USMV-SPHB spread flipped to −1.48% (risk-on). Gas $3.94/gallon. IEA: crisis “worse than combined 1973 and 1979 oil crises.” Friday’s PCE + Michigan Sentiment coincides with the 5-day pause expiry — the most important data day since the war began.

The Number That Matters: Brent at $103.64 (−7.62%) — the largest single-session oil drop of the entire war. The move from Friday’s $112.19 to $103.64 in pre-market represents an $8.55 crash. Still above $100, but the direction is violently de-escalatory. The market is pricing a PATHWAY TO CESSATION even though Iran denies talks. Trump’s rhetoric shifted from “obliterate power plants” (Saturday) to “productive conversations… complete resolution” (Monday morning) in 36 hours. WTI at $91.56 is back below $100 for the first time since the Day 16 surge. The oil crash is the single strongest signal that the war’s economic damage may have peaked.

The Setup: De-Escalation Relief Rally with Bond Market Skepticism. The equity market and oil are pricing genuine de-escalation: SPHB leading, small caps outperforming by 100 bps, XLE the only red sector, USMV/SPLV selling. But the bond market is barely responding (10Y +0.2 bps) and gold is in freefall (−4.14%, cumulative −17.4%). One of them is wrong. If MOVE collapses from 108 at the open, the bond crisis was event-driven. If MOVE stays above 100, the structural damage (inflation repricing, no cuts until 2027, Iraq force majeure) persists regardless of diplomacy. The 5-day pause expires near Friday’s PCE + Michigan data — the convergence of catalysts that will determine whether Week 4 brings resolution or re-escalation.

2. OVERNIGHT SESSION RECAP

Asia-Pacific

Nikkei +3.41% — the BEST international session of the entire war. TOPIX +3.19%. Japan is the biggest beneficiary of any oil pullback given its energy import dependence. The 5-day pause is being celebrated across Asian markets.

Europe

DAX +0.93%, Euro Stoxx +0.97%. Europe modestly green but underperforming Asia and US. European markets are still processing last week’s ECB/BoE/SNB hawkish holds and the permanent LNG damage from Qatar’s Ras Laffan (17% capacity lost, 3–5 year repair). European natural gas remains elevated.

US Pre-Market

Day 24 — Diplomatic Window Opens. Trump (7:10 AM EST): “VERY GOOD AND PRODUCTIVE CONVERSATIONS” with Iran; 5-day pause on ALL strikes against power plants and energy infrastructure. In a follow-up post, said the US is “very close to meeting our objectives” and American involvement could be “winding down.” Iran FM: “There is no dialogue between Tehran and Washington” — called it an effort to lower energy prices. Behind the scenes: Turkey, Egypt, and Pakistan have been passing messages between US envoy Steve Witkoff and Iranian FM Abbas Araghchi. A source: “The mediation is ongoing and making progress.” Israel continued striking Tehran during the pause announcement. Israeli DM Katz had said strikes would “significantly increase.” Whether Trump directly spoke to Iran or not, the 5-day pause signals he wants an off-ramp from the energy infrastructure escalation.

Weekend recap (Days 22–24): Saturday — Trump’s 48-hour ultimatum: open Hormuz or “obliterate power plants starting with the biggest one first.” Sunday — Brent surged to ~$114 on the ultimatum. Iran Parliament Speaker Ghalibaf warned any power plant strikes trigger “immediate” retaliation on energy infrastructure across the region. Iran’s National Defence Council: attacks on coast/islands would cause “all communication lines in Persian Gulf to be mined.” Saudi Arabia intercepted ballistic missiles toward Riyadh. Kuwait, UAE, Bahrain intercepting Iranian attacks Monday morning. IEA head Birol: crisis “worse than combined 1973 and 1979 oil crises” — at least 40 energy facilities across nine countries severely damaged. US gas $3.94/gallon (+$1 from pre-war). 50,000 US troops deployed. 13 US service members killed. Death toll: 2,200+ (Iran 1,500+ official / 3,320 per HRANA, Lebanon 1,000+).

Prior session (Friday March 20 close — WORST SESSION OF THE WAR): Iraq force majeure on oil exports + Pentagon ground troops deployment. MOVE exploded from 84.88 to 108.84 (+28.24%). 10Y surged +13.5 bps to 4.384%. 30Y hit 4.947%. S5FD crashed to 18.29 (new war low). R2FD crashed to 19.88. All sectors/factors/thematics red. Russell entered correction territory. COR1M hit 38.70 (war high). S&P breached the 200-day MA. Brent hit $112.19 new settlement high. But Trump’s post-close “considering winding down” lifted Mag 7 in after-hours.

This week: Tuesday — New Home Sales, Consumer Confidence. Wednesday — Durable Goods Orders. Thursday — GDP Q4 FINAL, Jobless Claims. FRIDAY — PCE Price Index (February, the Fed’s preferred gauge) + Michigan Sentiment FINAL (March, full post-war survey) — the MOST IMPORTANT data day since the war began, coinciding with the 5-day pause expiry window.

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 03/20/26. Provided for informational purposes only; not as investment advice.

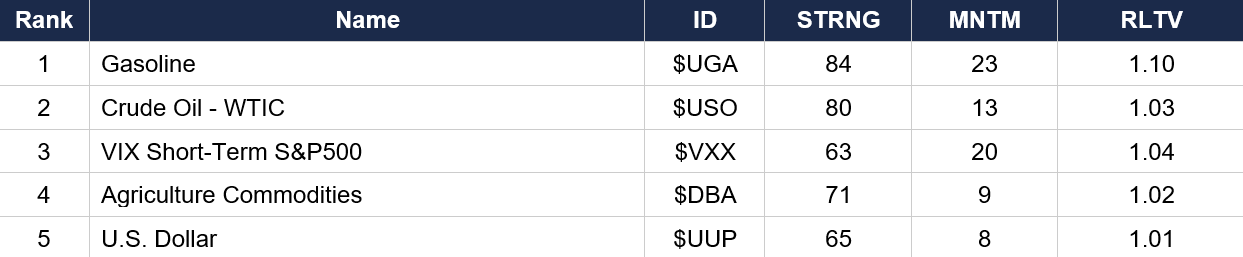

Asset Classes — Top 5

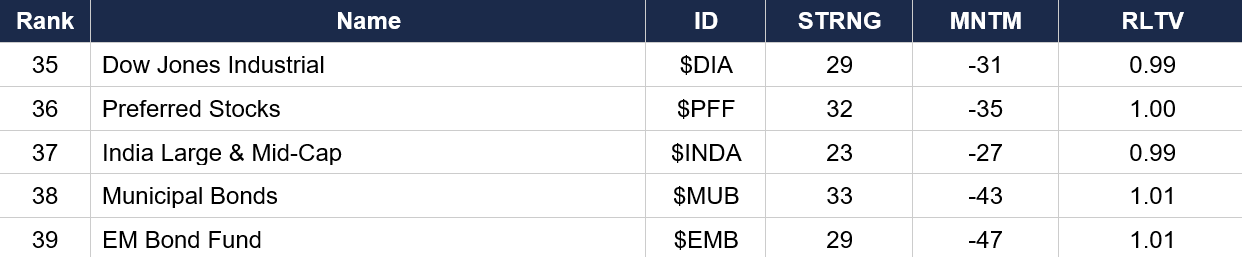

Asset Classes — Bottom 5

Regime signal: VIX ($VXX rank 3, MNTM 20) has SURGED back into the top 3 with the highest VIX momentum since Day 8 — reflecting Friday’s crisis. Agriculture ($DBA rank 4, MNTM 9) maintains strong positioning as food inflation intensifies. Dollar ($UUP rank 5, MNTM 8) still elevated but moderated. Gold ($GLD rank 32, MNTM −31, RLTV 0.91) has COLLAPSED to its lowest ranking and worst RLTV of the entire series — the cumulative damage is unprecedented. Silver ($SLV rank 13, MNTM −21, RLTV 0.86) also devastated. S&P ($SPY rank 28, MNTM −32) near series lows. Nasdaq ($QQQ rank 14, MNTM −23) deeply negative. EM Bonds ($EMB, MNTM −47) worst momentum of any asset for the second consecutive data set. NOTE: Today’s oil crash and equity surge are NOT yet reflected in this data which captures Friday’s close.

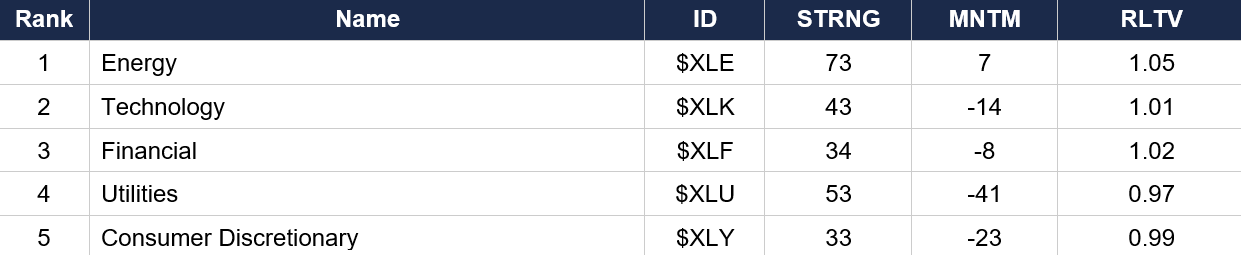

Sector ETFs — Top 5

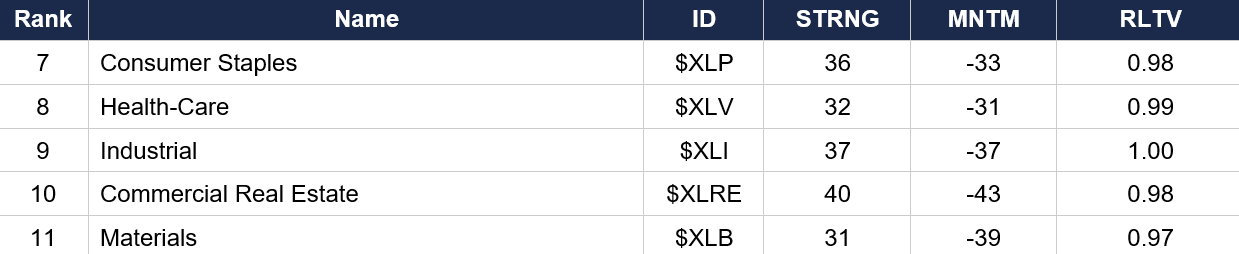

Sector ETFs — Bottom 5

Regime signal: Energy ($XLE rank 1, MNTM 7) still leads but momentum has faded from 13 — the oil pullback from $119 to $103 is registering. Financial ($XLF rank 3, MNTM −8) has risen to the top 3 as banks benefit from higher rates and steeper curves. Utilities ($XLU rank 4, MNTM −41) has COLLAPSED from rank 3 with the worst momentum drop of any sector this session. Technology ($XLK rank 2, MNTM −14) has turned deeply negative. Commercial Real Estate ($XLRE rank 10, MNTM −43) is the worst sector momentum of the series — 4.94% 30Y yields and 6.22% mortgage rates are devastating rate-sensitive real estate. ALL 11 sectors now have negative momentum except Energy.

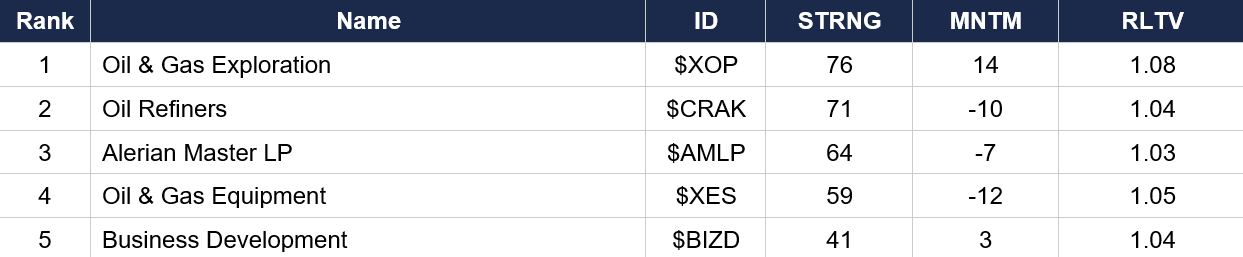

Industry ETFs — Top 5

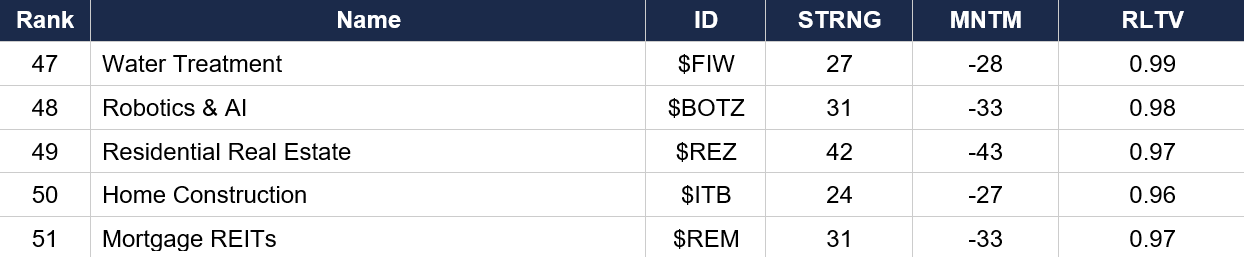

Industry ETFs — Bottom 5

Regime signal: Oil & Gas Exploration ($XOP, MNTM 14) still leads but the energy complex is narrowing — Oil Refiners ($CRAK, MNTM −10) has flipped negative for the first time. Business Development Companies ($BIZD rank 5, MNTM 3) — a floating-rate credit play — is now in the top 5, confirming the rising-rate/higher-for-longer theme. Residential Real Estate ($REZ rank 49, MNTM −43) and Mortgage REITs ($REM rank 51, MNTM −33) at the absolute bottom as 30Y approaching 5% and mortgage rates at 6.22% crush housing and real estate. Gold Miners ($GDX rank 46, MNTM −35, RLTV 0.88) devastated by the gold crash. Aerospace-Defense ($ITA rank 39, MNTM −33) continues plummeting despite an active war.

4. MORNING DATA REACTION

No major US economic data releases at 8:30 AM today. This is a headline-driven session — the Trump 5-day pause, Iran’s response, Hormuz status, and whether MOVE collapses at the open will determine the day’s direction.

Last week’s data recap — the most intense week of the series: PPI +0.7%/3.4% YoY (goods +1.1%, war pass-through confirmed). FOMC: hold 3.50–3.75%, dot plot one cut 2026, core PCE forecast raised to 2.7%, Powell “bar is higher for cuts.” Jobless Claims 205K (labor tight, no Fed cover). ECB held at 2.0% (raised 2026 inflation to 2.6%). BoE held at 3.75% (Mann: “even a hike”). SNB held at 0%. Micron historic beat ($12.20 EPS, $33.5B Q3 guide) completely ignored. FedEx beat + raised. Iraq declared force majeure on oil exports. Pentagon deploying ground troops. MOVE exploded +28% to 108.84. Market now pricing NO rate cuts until 2027.

This week’s calendar — building to Friday’s convergence: Tuesday: New Home Sales (Feb), Conference Board Consumer Confidence (March). Wednesday: Durable Goods Orders (Feb). Thursday: GDP Q4 FINAL, Jobless Claims. FRIDAY: February PCE Price Index (the Fed’s preferred inflation gauge) + Michigan Sentiment FINAL (March — the FIRST complete post-war consumer survey). Friday coincides with the approximate expiry of Trump’s 5-day pause. If PCE is hot AND the pause expires without resolution, the market faces simultaneous inflation confirmation + war re-escalation. If PCE is benign AND talks progress, the de-escalation trade accelerates.

The cumulative data arc tells the stagflation story: GDP 0.7%, NFP −92K, Empire State −0.20, Michigan 55.5 (2nd percentile), CPI 2.4%, PPI 3.4%, Core PCE 3.1%. Growth decelerating while inflation accelerating. The war has now layered a $90+ oil shock, $3.94 gas, and global supply chain disruption on top of an already fragile economy. IEA called it “worse than the combined 1973 and 1979 oil crises.”

5. THE DYRH READ

Regime: De-Escalation Relief Rally — Diplomatic Window Opens with Bond Market Skepticism. Trump’s 5-day pause creates a defined ceasefire window. Equities and oil pricing de-escalation. Bond market and gold not buying it. Confidence: Moderate.

Yield Curve: Tentative Bull Flattener — Bond Market Says “Show Me More.” The 30Y is pulling back marginally (−0.8 bps to 4.939%) while the 10Y is essentially unchanged (+0.2 bps to 4.386%, near its war high of 4.384%). The 5Y remains above 4.00% (4.014%). The 2Y at 3.901% remains above the fed funds upper bound (3.75%). The magnitude of the bond market’s response to the 5-day pause is NEGLIGIBLE compared to the equity/oil reaction. MOVE at 108.84 (Friday’s print) is the CRITICAL watch at the open — if MOVE collapses back toward 90, the bond crisis was event-driven. If it stays above 100, the structural damage (inflation repricing, no cuts until 2027, Iraq force majeure, permanent Ras Laffan damage) persists regardless of Trump’s rhetoric. Until yields materially reverse, the bond crisis is merely PAUSED, not resolved.

Oil Crash — Largest Single-Session Drop of the War. Brent −7.62% to $103.64. WTI −6.79% to $91.56 (back below $100). RBOB −4.97%. Natural gas −3.94%. The 5-day pause on energy infrastructure strikes is the proximate catalyst, but the deeper signal is that Trump’s rhetoric shifted from “obliterate power plants” (Saturday) to “complete and total resolution” (Monday) in 36 hours. The market is pricing a PATHWAY TO CESSATION. Cumulative: Brent +42.2% from pre-war (down from +53.9% Friday). But Brent is still above $100. Iran is still attacking Gulf states (Saudi, Kuwait, UAE, Bahrain intercepting Monday morning). Iraq force majeure still in effect. Qatar’s Ras Laffan damage is permanent (3–5 year repair). The oil pullback is real but the structural supply disruption hasn’t resolved.

Gold in Freefall — Worst Single Session of the War. Gold −4.14% to $4,385.4. Cumulative: −$926 (−17.4%) from pre-war — during an active shooting war. Silver −2.06%. Platinum −4.76%. This decline is DISPROPORTIONATE to a de-escalation trade. On a day when equities surge +1.50% and oil drops 7%, gold should be stable or modestly lower — not crashing 4%. This suggests forced liquidation continues on autopilot: margin calls from Friday’s bond explosion (MOVE +28%) are STILL cascading through the precious metals complex regardless of Monday’s diplomatic headlines. Copper +0.57% (industrial metal green) confirms this is NOT a broad commodity sell — it’s precious metals specifically being liquidated. Watch GVZ at the open: if it collapses from 35.25, gold is selling on de-escalation. If GVZ stays elevated, it’s margin calls.

Equities: Relief Rally — Partial Recovery, Not V-Bottom. ES +1.50% to 6,657 would reclaim the 200-day MA (~6,619) if held at close. Nikkei +3.41% (best of the war). Russell +2.44% (small caps leading — risk-on size rotation). All 7 Mag 7 green (NVDA +2.13% leads). 10 of 11 sectors green, XLE the only red (−1.15% on oil crash). SPHB +1.31%, USMV −0.17% = risk-on factor rotation. SOXX +2.13% leading thematics. But ES +1.50% only recovers HALF of Friday’s −1.52%. This is NOT a V-bottom — it needs follow-through. The 200-day MA was breached Friday; reclaiming it today would mark a successful false breakdown. Breadth from Friday (S5FD 18.29, R2FD 19.88) is at capitulation levels that historically produce violent snapbacks.

The 5-Day Window — The Week’s Architecture. Trump’s pause expires approximately Friday/Saturday (March 27–28). Friday is also PCE + Michigan Sentiment FINAL — the most important data day since the war began. This creates a CONVERGENCE: if talks progress + PCE benign = de-escalation accelerates. If the pause expires without resolution + PCE is hot = simultaneous inflation confirmation + war re-escalation. The market has a defined window to evaluate whether the diplomatic channel is real. Iran’s denial of direct talks is being mediated through Turkey, Egypt, and Pakistan — indirect channels that could produce results even without formal dialogue.

6. THE GAME PLAN

Today’s Key Events: Trump 5-day pause on energy strikes (announced 7:10 AM). Iran’s response evolving (denies direct talks, acknowledges regional mediation). MOVE at market open (bond crisis resolution test). Whether equity rally holds through close; 200-day MA reclaim. No major US data. Tuesday: New Home Sales, Consumer Confidence. Wednesday: Durable Goods. Thursday: GDP FINAL, Jobless Claims. FRIDAY: PCE + Michigan Sentiment FINAL — coincides with 5-day pause expiry.

The Bull Case: The 5-day pause is the single most de-escalatory signal of the entire war. Oil crashed 7.6% (largest drop). Equities surging with textbook risk-on rotation (SPHB leading, small caps outperforming, USMV selling). Nikkei +3.41%. All 7 Mag 7 green. 10/11 sectors green. Breadth at capitulation levels (S5FD 18.29) historically produces violent snapbacks. Turkey/Egypt/Pakistan mediation is “making progress.” Netanyahu said war may “end sooner than people think.” Bessent hinted at 140M barrel unsanction. Trump shifted from “obliterate” to “complete resolution” in 36 hours. If MOVE collapses and yields reverse, the bond crisis was event-driven and normalizes. Copper +0.57% = industrial growth signal.

The Bear Case: Iran explicitly DENIED any talks: “there is no dialogue.” Israel continued striking Tehran during the pause. Gulf states still intercepting Iranian attacks Monday morning. Gold −4.14% (worst of war, cumulative −17.4%) = forced liquidation continuing on autopilot. Bond market barely responded (10Y +0.2 bps at war high). MOVE at 108 — if it stays above 100, the structural damage is permanent. The 5-day pause expires near Friday’s PCE + Michigan — double catalyst risk. Iraq force majeure still in effect. Qatar’s Ras Laffan: 3–5 year repair, 17% LNG lost. IEA: “worse than 1973 and 1979 combined.” Days 13–14’s recovery lasted 3 sessions before Day 15’s reversal — this could follow the same pattern. 50,000 troops deployed + $200B funding request = infrastructure for a longer war.

Regime: De-Escalation Relief Rally with Bond Market Skepticism. The equity market and oil are pricing a genuine diplomatic window. But the bond market is not buying it (10Y unchanged at war highs), and gold’s −4.14% suggests forced liquidation continues. The 5-day pause creates a defined evaluation window — ending near Friday’s PCE + Michigan convergence. If talks progress and MOVE collapses, the recovery broadens. If the pause expires without resolution, the Day 17 bond crisis regime reasserts.

Watch List

MOVE at the open — THE single most important number — Friday’s close was 108.84 (bond crisis). If MOVE opens below 100, the crisis was event-driven and normalizing. If above 100, structural damage persists. This determines whether the bond market joins the equity relief rally.

Iran’s response — is the diplomatic channel real? — Iran denied direct talks but acknowledged regional mediation (Turkey, Egypt, Pakistan). If intermediaries confirm progress by end of day, the rally sustains. If Iran produces evidence of no talks, the market must de-price the diplomatic window.

Gold −4.14% — forced liquidation or de-escalation? — The worst gold session of the war during a de-escalation rally is paradoxical. Watch GVZ at the open: if gold vol collapses, it’s safe-haven unwinding. If GVZ stays elevated, margin calls are still cascading from Friday’s MOVE explosion.

200-day MA reclaim — false breakdown test — ES at 6,657 vs. 200-day MA ~6,619. If ES closes above this level, Friday’s breach was a false breakdown — the most bullish technical signal available. If it fails, the MA becomes resistance.

Friday’s PCE + Michigan + pause expiry — THE convergence — The most important data day since the war began coincides with the 5-day pause window. PCE hot + pause expires = stagflation + re-escalation. PCE benign + talks progress = de-escalation accelerates. Plan the week around this Friday.

Morning check: the strongest de-escalation signal of the entire war. Trump’s 5-day pause, “productive conversations,” and the largest oil crash since February 28. Equities surging with textbook risk-on rotation. But Iran denies talks. The bond market is flat at war-high yields. Gold is crashing 4% in what looks like forced liquidation on autopilot. And the 5-day window expires near Friday’s PCE + Michigan — the most important data convergence of the series. The market has cast its de-escalation vote. Now it has five days to be proven right or wrong.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.