☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: THE CEASEFIRE IS DEAD. ISLAMABAD TALKS COLLAPSED SUNDAY AFTER 21 HOURS. TRUMP ORDERED HORMUZ BLOCKADE. US DESTROYERS ENTERED THE STRAIT. WTI +7.88% BACK ABOVE $104. GOLD RED ON FORCED LIQUIDATION. MICHIGAN 47.6 ALL-TIME RECORD LOW. CPI 3.3%. THE REGIME HAS RUPTURED.

After 21 hours of face-to-face talks at the Serena Hotel in Islamabad — the highest-level direct US-Iran negotiations since the 1979 Islamic Revolution — the negotiations collapsed Sunday morning without an agreement. Vice President Vance, who led the US delegation alongside Witkoff and Kushner, told reporters before boarding Air Force Two that Iran ‘chose not to accept our terms’ and that the central sticking point was Tehran’s refusal to make ‘an affirmative commitment that they will not seek a nuclear weapon.’ Iran’s chief negotiator, parliament speaker Ghalibaf, blamed the US for the failure, saying his delegation ‘raised forward-looking initiatives’ but the US ‘failed to gain the trust of the Iranian delegation.’ Within hours, Trump ordered the US Navy to begin a blockade of Iranian ports, told the New York Post that US warships were being ‘reloaded with the best ammunition’ to resume strikes if needed, and posted that Iran’s ‘only reason they are alive today is to negotiate.’

Per WSJ and Wikipedia reporting, several US destroyers entered the Strait of Hormuz for the first time since the war began on what CENTCOM described as a ‘freedom of navigation’ mine-clearance operation. Iran reportedly threatened to attack the ships and one US vessel reportedly turned back after a warning. Iran also reportedly ‘lost track’ of mines it planted during the closure, complicating any near-term reopening. Israel struck more than 200 Hezbollah targets over the weekend, with Lebanon’s health ministry now reporting 350+ killed in the Wednesday Beirut bombardment alone — a Red Cross paramedic was among 35 more killed Sunday. Hezbollah resumed rocket and drone attacks. Trump told NBC Israel would ‘scale back’ Lebanon strikes — but they have not. Pakistan’s FM Dar said Islamabad would continue to mediate, but with talks failed, blockade ordered, and active strikes continuing, the two-week ceasefire framework set to expire April 22 is functionally a dead letter.

The pre-market tape is gapping accordingly but with critical nuance. WTI +7.88% to $104.18 back well above the $100 threshold. Brent +7.32% to $102.17. Heating oil +8.89% (the day’s standout product print). RBOB +4.66%. Gold is RED −1.17% to $4,731.6 even with the escalation — the forced-liquidation signature returning. Silver −3.56%. Every G10 currency is red vs USD with DXY +0.37% — the first clean dollar-as-safe-haven print in over a week. BTC −3.50% to $70,910 breaks below $71K. The futures sell-off is real but CONTAINED at the index level (ES −0.60%, NQ −0.57%, RTY −0.69%, YM −1.06%) suggesting positioning rather than panic. International equities leading the give-back: Nikkei USD −1.50%, DAX −1.36%, EuroStoxx −1.31%. The same cross-asset transmission mechanism we saw at the Wednesday reflation peak is now running in reverse.

The Friday Data Shock That Set the Stage: CPI 3.3% YoY Hot. Michigan 47.6 ALL-TIME RECORD LOW. Inflation Expectations 4.8%.

Friday delivered the week’s actual verdict in two data points issued four hours apart. At 8:30 AM, CPI March printed +0.9% MoM / 3.3% YoY — the largest monthly jump since June 2022. Gasoline surged +21.2% in a single month — the largest monthly increase in the series since the BLS first published it in 1967. Fuel oil +30.7%. Energy index +10.9% (largest since September 2005). Core CPI was a soft +0.2% MoM / 2.6% YoY — the war is mostly an energy-driven inflation so far. At 10:00 AM, the University of Michigan Consumer Sentiment Index preliminary April printed 47.6 — an ALL-TIME RECORD LOW in the survey’s history since 1952. Lower than the 1980 energy crisis (51.7). Lower than the 2008 Great Recession. Lower than the pandemic. Lower than any reading in 74 years. Year-ahead inflation expectations spiked from 3.8% to 4.8% — the largest one-month jump in the survey’s history, blowing past the 4.2% consensus. 5-10 year expectations rose from 3.2% to 3.4% (highest since November 2025). Hsu: ‘Consumers are speaking loud and clear. They are very, very frustrated by the persistence of high prices, and they’re feeling very weighed down with the cost of living.’ 98% of the survey was conducted BEFORE the Tuesday ceasefire announcement — so none of the relief is captured and the current reading reflects peak-war conditions.

The Setup: Ceasefire Collapse — Hormuz Blockade Ordered. Breadth Thrust Rejected In Two Sessions. COR1M Lowest Of The War. The Regime Reset From Wednesday Is Dead At The Macro Level.

Last week’s ‘best week since November’ rally (S&P +3.6%, Nasdaq +4.7%, Dow +3%) was structurally narrow. The Wednesday breadth thrust that was framed as ‘two consecutive thrust sessions historically marking generational lows’ has been REJECTED — S5FD crashed from Wednesday’s 83.10 to Friday’s 58.76 (−29% give-back) in just two sessions, and it happened DURING the rally. S5FI (50-day breadth) at 43.42 is STILL BELOW 50 — the longer-horizon breadth damage was never repaired. COR1M at 13.58 is the LOWEST print of the entire war by a wide margin, telling you the Friday rally was extraordinarily narrow — driven by a few Mag 7 names while the broader index was internally deteriorating. Today’s Monday gap-down is hitting a market that was internally already weak, not a market that was uniformly long. Bank earnings week opens today (GS before the bell, JPM/WFC/C/BLK Tuesday).

2. OVERNIGHT SESSION RECAP

Asia-Pacific

Nikkei USD −1.50% — leading the Asian give-back. TOPIX local at −0.09% essentially flat because the yen weakened (JPY −0.32%) and softened the local-currency Japanese read. The severity of the Nikkei USD decline reflects both the war re-escalation AND the dollar strength returning. Asian markets priced the Islamabad failure during their cash session Sunday night/Monday morning and produced the first meaningful regional selloff since the Wednesday peak.

Europe

DAX −1.36% to 23,709. EuroStoxx 50 −1.31% to 5,799. Europe is the most exposed major economy to the war’s energy dimension and now gives back roughly half of Wednesday’s 4-5% catch-up rally in a single session. Cumulative European give-back since the post-ceasefire peak is approximately 50% of Wednesday’s gain — meaningful but still not a full reversal. EUR −0.39% weakening against the dollar.

US Pre-Market

Day 45 of Operation Epic Fury. Q2 Day 10. The morning after the weekend regime break.

US FUTURES ALL RED BUT CONTAINED: ES 6,814.25 (−0.60%), NQ 25,136.00 (−0.57%), RTY 2,626.1 (−0.69%), YM 47,621 (−1.06% — leading down). The Dow leading at −1.06% is the meaningful tell — industrials and energy-consumers are taking the brunt while NQ −0.57% holds up better because of a few defensive mega-cap names. The 46 bp spread between Dow and Nasdaq reflects the same underlying read: industrial cyclicals are the cleanest expression of the global-growth-rebound thesis being unwound, while mega-cap tech remains relatively insulated. ES at 6,814.25 is only −42 points below Friday’s 6,816.89 close — a measured Sunday-night gap given the magnitude of the weekend news.

ALL 7 MAG 7 RED IN AH FOR THE FIRST TIME SINCE THE WAR BEGAN. NVDA −1.51% leading the give-back from Friday’s +2.57% close. META −0.96%. GOOG −0.96%. MSFT −0.79% (Mag 7 laggard continues). AMZN −0.50%. TSLA −0.46%. AAPL −0.38%. The Mag 7 dispersion has narrowed from Wednesday’s 750 bp intra-Mag 7 spread to today’s 113 bp pre-market spread — the names that were driving the narrow rally are losing their bid simultaneously, and that is the early signature of a broader equity unwind.

CRITICAL WEEKEND DEVELOPMENTS: Vance led the US delegation alongside Witkoff and Kushner. Ghalibaf led the Iranian side. Talks ran 21 hours. Vance: Iran ‘chose not to accept our terms’; the sticking point was the ‘affirmative commitment’ on nuclear weapons. Ghalibaf: US ‘failed to gain the trust of the Iranian delegation.’ Trump NY Post interview: warships being ‘reloaded with the best ammunition.’ Trump Truth Social: Iran’s ‘only reason they are alive today is to negotiate.’ US destroyers entered Hormuz for the first time since the war began on a CENTCOM-described ‘freedom of navigation’ mine-clearance operation. Iran threatened to attack the ships; one US vessel reportedly turned back after a warning. Iran ‘lost track’ of mines planted during the closure. Israel struck 200+ Hezbollah targets over the weekend; Lebanon health ministry reports 350+ killed in Wednesday’s Beirut bombardment alone. Trump told NBC Israel would ‘scale back’ Lebanon strikes — they have not. Pakistan FM Dar said Islamabad will continue to mediate.

PRIOR SESSION CONTEXT: The Day 30 close, Day 31 PM, and Day 31 close DYRH reports were missed Thursday afternoon through Friday. The most recent baseline is Day 30 pre-market (Thursday April 9). Between then and this report, the market staged the ‘best week since November’ rally on continued ceasefire optimism, with ES closing Friday at 6,816.89 essentially flat Thursday-Friday after the Wednesday thrust. The seven-day S&P win streak ended on Friday’s −0.11% close. CPI Friday. Michigan Friday. Then the weekend collapse.

This week’s calendar (verified): TODAY — Goldman Sachs Q1 before the open. Limited fresh economic data. Fed speaker calendar TBD. TUESDAY — JPM, WFC, C, BLK, JNJ Q1 earnings before the open. WEDNESDAY — BAC, PNC, MTB, FHN Q1 earnings. THURSDAY — Morgan Stanley, Schwab, Travelers Q1 earnings; TSMC; NFLX after close. Initial Jobless Claims. Philly Fed. FRIDAY — Ally, Fifth Third, Regions, State Street, Truist Q1. Housing Starts. APRIL 22 — Two-week ceasefire framework formally expires (de facto already dead). APRIL 28-29 — FOMC meeting; Powell press April 29.

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 04/10/26. Provided for informational purposes only; not as investment advice.

Asset Classes — Top 5

Asset Classes — Bottom 5

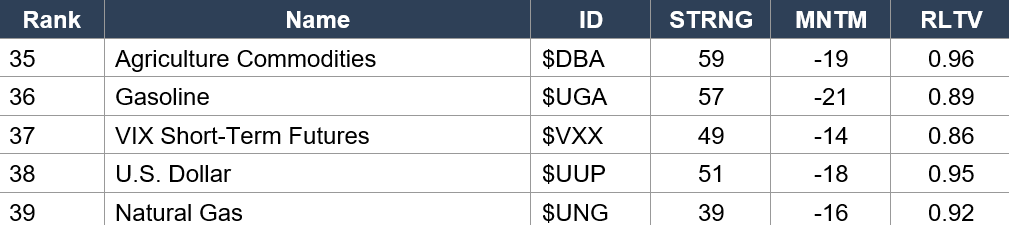

Regime signal: The Friday close Quiggle data captures the full post-ceasefire reflation regime — and today's Monday regime break will destroy most of it. Latin America ($ILF rank 1, STRNG 60, MNTM 27) holds the top spot for the 5th consecutive data set with massively higher STRNG (was 53 last read). India ($INDA rank 2, MNTM 36) has the HIGHEST MOMENTUM of any asset class — EM equities were the post-ceasefire leaders. Europe ($FEZ rank 3, MNTM 29) and Pacific ex-Japan ($EPP rank 4, MNTM 25) round out the international leadership — international equities were completely dominant. Dow Jones ($DIA rank 5, MNTM 29) broke into the top 5 for the first time all war. CRITICAL SHIFTS: Crude Oil ($USO rank 34, STRNG 62, MNTM −15, RLTV 0.87) — COLLAPSED from rank 2 last week to rank 34, with RLTV crashing from 1.02 to 0.87 in three sessions. This is the fastest fall from grace for any commodity in the dataset. Gasoline ($UGA rank 36, MNTM −21) collapsed similarly. Gold ($GLD rank 27, MNTM 12, RLTV 0.98) has momentum turning positive but still ranks mid-table — today's −1.17% gold print will be captured tomorrow. VIX ($VXX rank 37, MNTM −14, RLTV 0.86) at rock-bottom before the regime break. DXY ($UUP rank 38, MNTM −18, RLTV 0.95) collapsed further. These rankings are about to undergo a MASSIVE reshuffle tomorrow as the post-ceasefire reflation data is reversed.

Sector ETFs — Top 5

Sector ETFs — Bottom 5

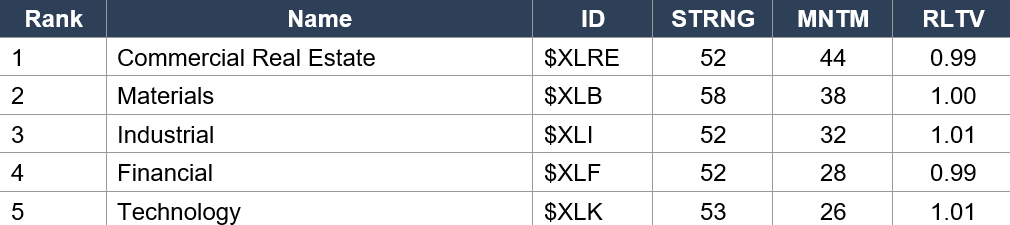

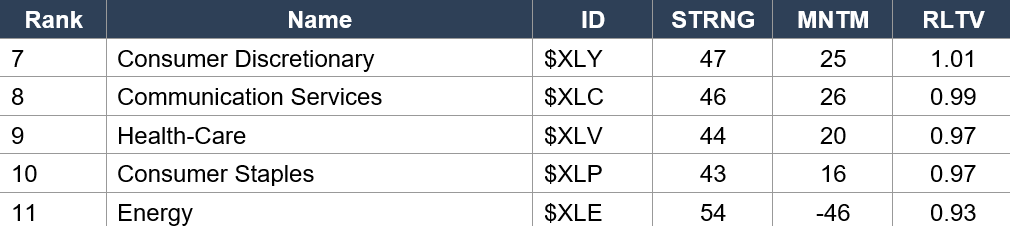

Regime signal: The Energy ($XLE) collapse is now historic: rank 11 — DEAD LAST — with STRNG 54, MNTM −46, RLTV 0.93. The −46 momentum score is THE WORST MOMENTUM READING FOR ANY SECTOR IN ANY DATA SET OF THE ENTIRE WAR by a wide margin. From perennial #1 throughout most of the war to DEAD LAST in the Friday close data — the structural de-rating is now total. Today’s Monday +1.76% XLE pre-market bid on the ceasefire collapse will improve momentum modestly but the damage to STRNG/RLTV is structural. Commercial Real Estate ($XLRE rank 1, MNTM 44 — the HIGHEST momentum reading of any sector) leads the rankings — CRE was the cleanest post-ceasefire bull-flattener beneficiary. Materials ($XLB rank 2, MNTM 38), Industrial ($XLI rank 3, MNTM 32), Financial ($XLF rank 4, MNTM 28), and Tech ($XLK rank 5, MNTM 26) consolidated the post-war cyclical rotation. Consumer Staples ($XLP rank 10, MNTM 16, RLTV 0.97) is the second-worst sector — defensive unwind essentially complete. Tomorrow’s data will capture the first reversal: XLE momentum should spike, cyclicals should bleed.

Industry ETFs — Top 5

Industry ETFs — Bottom 5

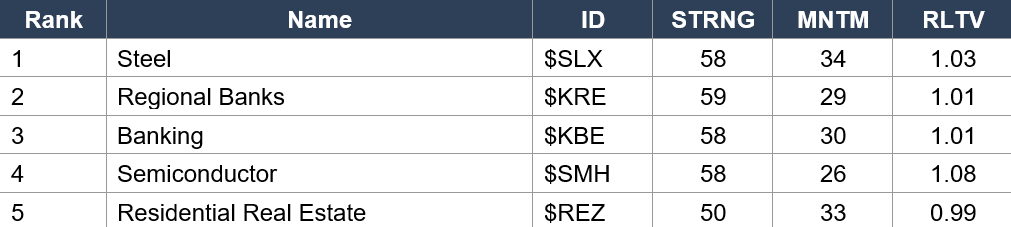

Regime signal: Steel ($SLX rank 1, MNTM 34) has DETHRONED Regional Banks — Steel now leads all industries with the highest momentum score. Semiconductor ($SMH rank 4, MNTM 26, RLTV 1.08) has the HIGHEST RLTV of any industry at 1.08 — chips are the cleanest relative outperformer in the Friday close data, consistent with the narrow Mag 7 rally structure. Gold Miners ($GDX rank 9, MNTM 26, RLTV 1.02) — momentum accelerating on Wednesday’s metals explosion. CRITICAL ENERGY COMPLEX DE-RATING: Oil & Gas Exploration ($XOP rank 49, STRNG 57, MNTM −31, RLTV 0.92), Oil Refiners ($CRAK rank 48, MNTM −26, RLTV 0.94), Alerian MLP ($AMLP rank 47, MNTM −16, RLTV 0.94) — the entire energy infrastructure complex is in the bottom 5, with Exploration having the second-worst momentum of any industry. Today’s +7.88% WTI surge will reverse these readings sharply tomorrow. Software ($IGV rank 50, MNTM −14, RLTV 0.97) is the structural loser — a separate narrative from the war (AI disruption / SaaS demand slowdown) that is layering on top of the macro tape. Gaming ($BJK rank 51) showing zero readings — data anomaly, treat as exclusion rather than signal.

4. MORNING DATA REACTION

Friday CPI March: +0.9% MoM headline / 3.3% YoY. Core +0.2% MoM / 2.6% YoY. Gasoline +21.2% — largest monthly increase since the BLS series began in 1967. Fuel oil +30.7%. Energy index +10.9% (largest since September 2005).

The CPI print confirmed in hard data what the energy market had been pricing: the Iran war produced a measurable inflation shock. Gasoline’s +21.2% monthly jump drove three-quarters of the headline increase. The core at +0.2% MoM / 2.6% YoY was soft — the war is mostly an energy-driven inflation so far, with limited pass-through to services and goods ex-energy. For the Fed, the soft core provides some room but the headline locks out any meaningful easing discussion at the April 28-29 meeting. The bond market is now pricing the Fed as ‘maximally constrained’ — no cut path and no hike path, a stasis that can only break on clean energy disinflation (which the Sunday news just made less likely).

Friday Michigan Sentiment April Preliminary: 47.6 — ALL-TIME RECORD LOW in the survey’s 74-year history (since 1952). Year-ahead inflation expectations 4.8% (up from 3.8%). 5-10yr expectations 3.4% (up from 3.2%).

47.6 is the lowest reading in the history of the survey — lower than the 1980 energy crisis (51.7), lower than 2008 Great Recession, lower than the 2020 pandemic, lower than the 1970s stagflation era. Americans who have lived through gas lines, double-digit mortgage rates, Lehman Brothers, and COVID have not felt this bad about the economy. Year-ahead inflation expectations spiked 100 basis points in a single month — the largest one-month jump in the survey’s history, blowing past the 4.2% consensus. Every demographic group declined — all ages, income brackets, political affiliations. The current economic conditions index fell 10.2% to 50.1. Expectations dropped 10.8% to 46.1. One-year business condition expectations crashed 20%. Critically: 98% of interviews were conducted BEFORE the Tuesday ceasefire announcement. None of the relief is captured. Hsu: ‘Consumers are speaking loud and clear. They are very, very frustrated by the persistence of high prices.’ For the Fed, the inflation expectations de-anchoring is the most dangerous signal — the Fed has repeatedly cited consumer inflation expectations as a precondition for any easing, and a 100 bp one-month jump in the 1-year reading with the 5-10 year reading also rising is exactly what the Fed has feared.

Friday Close Data Complex: VIX 21.35 (+11%), VIX1D 19.07 (+35.54%), MOVE 72.1541 (−2.51%, sub-75) — TWO REGIMES IN PARALLEL.

Friday closed with equity vol spiking (VIX +11%, VIX1D +35.54% — short-dated event-risk panic) while MOVE FELL FURTHER to 72.1541 — a new sub-75 print, the cleanest rates-vol normalization of the war. The bond complex through Friday was telling a completely different story from the equity complex: equities were pricing mounting risk while bonds were pricing full normalization. The Wednesday regime call was confirmed in the bond complex through Friday close — but that was BEFORE the Sunday talks failure, blockade order, and Hormuz operation. The fresh Monday MOVE print when it lands is the binary of the entire week.

This week ahead: TODAY — GS Q1 before open. TUESDAY — JPM, WFC, C, BLK, JNJ (Dimon’s tone is the single highest-information corporate-fundamentals signal of the week). WEDNESDAY — BAC. THURSDAY — Morgan Stanley, Schwab, TSMC, NFLX + Claims + Philly Fed. FRIDAY — Regional banks + Housing Starts. APRIL 22 — Ceasefire formally expires (de facto already dead). APRIL 28-29 FOMC — Powell press conference April 29.

5. THE DYRH READ

Regime: Ceasefire Collapse — Hormuz Blockade Ordered, Inflation Expectations De-Anchor, Breadth Thrust Rejected. The Wednesday regime call is dead at the macro/sentiment/breadth level. It may still be alive at the bond-vol and correlation level (MOVE 72.15 stale; COR1M 13.58 lowest of the war). Today’s fresh MOVE and COR1M prints resolve whether two regimes are operating in parallel for the first time in this cycle. Confidence: High on the regime rupture; moderate on the durability of the internal divergences.

Yield Curve: Bear Steepener (Mild) — Full-Curve Sell-Off Ends The Steepener-Twist Period.

All yields rising with the long end leading marginally: 30Y +2.0 bps to 4.929%, 10Y +1.6 bps to 4.333%, 5Y +1.6 bps to 3.957%, 2Y +1.7 bps to 3.816%. At +0.3 bps differential between long and front, this is one print away from being a parallel bear shift. The single most important observation is that the Day 28-29 close steepener twist (2Y down + 30Y up) and the Day 30 pre-market mild steepener twist have both rolled into a unified ‘everything sold’ tape. The curve is no longer pricing growth-fear at the front while pricing inflation at the long end — it is now pricing inflation across the full curve. The 2Y +1.7 bps move is the first time in this regime cycle that the front end has sold off in pre-market without an offsetting Fed-cut bid; that suggests the rate-cut path probability is being marked down. Michigan inflation expectations at 4.8% + CPI at 3.3% YoY + Hormuz blockade = the Fed is maximally constrained and Fed governor speakers between now and April 29 will likely shift hawkish.

MOVE Friday Close 72.1541 — Stale Into A Regime-Break Monday. The Binary Signal Of The Week.

Between Day 30 pre-market (Thursday at 78.7357) and Friday’s close, MOVE FELL FURTHER to 72.1541 — a −6.58 point decline in roughly 36 trading hours. That is below 75 — fully normalized territory — and was the cleanest possible evidence that the Wednesday sub-80 regime call was structural rather than reflexive. But that print is stale into a Monday where the entire ceasefire framework has collapsed. The fresh MOVE print at or shortly after the cash open is the single highest-information data point of the week. Below 72 = bond crisis structurally dead under maximum stress. 72-75 = normalized, regime largely held. 75-80 = meaningful walk-back, fragility returning. 80-85 = Wednesday’s regime call has to be fully revisited. Above 85 = bond crisis is back, all bets off. The fact that MOVE went into Friday’s close at 72.15 (further below the 80 binary) means the Monday print would need to spike +10 points to re-enter ‘stressed’ territory — a high bar. If MOVE prints anywhere below 80 despite the genuine ceasefire collapse, it is the strongest possible confirmation that the bond complex is structurally regime-changed.

WTI +7.88% To $104.18 — Back Above The Damage Threshold.

The 24-hour range from Friday close ~$96 to Monday pre $104 = +$7.61 / +7.88%. Heating oil leads at +8.89% — distillate stress on shipping disruption return. Brent +7.32% to $102.17. RBOB +4.66%. Natural gas +2.27%. The Hormuz blockade order and US destroyers entering the strait put a structural floor under crude prices for at least the next two weeks — Iran ‘lost track’ of mines, and US vessels are operating in contested waters. WTI back above $100 means the inflation pulse from energy is sustained, not transitory. Cumulative WTI from pre-war $67.02 is now +$37.16 / +55.4% (was +71.4% at the $114.87 war high on April 7, was +39.0% at the $93.17 post-ceasefire low on April 8). The war premium is partially re-pricing — not all the way back to the war high, but well above post-ceasefire levels.

Gold −$55.8 to $4,731.6 — Forced Liquidation Signature Returns.

Gold at −1.17% while oil surges +7.88% = the textbook forced-liquidation pattern Morgan Stanley flagged in Day 2 of the war. Silver −3.56%, platinum −1.45%, copper −0.50% — the metals tape is fully unwound. Gold-down + equities-down + dollar-up forms the classic cross-asset liquidation signature: margin calls on commodity positions forcing gold sales to cover energy exposure. This is the THIRD forced-liquidation episode of the war (Day 2, Day 21, Day 26 Trump primetime). Each prior episode resolved in one to three sessions. The pattern: gold liquidation tells you positioning is hedged, not that gold has lost its hedge function. But the fact that gold is RED on a Sunday-night ceasefire-collapse morning is consequential for any portfolio that assumed the metals tape as a war hedge.

Breadth Thrust Dead — COR1M At 13.58 (Lowest Of The War).

THE GENERATIONAL BREADTH THRUST IS DEAD. S5FD at 83.10 Wednesday was framed as ‘two consecutive thrust sessions historically marking generational lows.’ Two sessions later Friday close, S5FD was 58.76 — a −29% give-back in just two sessions. R2FD crashed from 81.08 to 63.85. S5FI (50-day breadth) at 43.42 is STILL BELOW 50 — the longer-horizon breadth damage from the war was never repaired, and the 5-day thrust was a positioning artifact rather than genuine regime change. Critically: the breadth deterioration from Wed to Fri happened DURING the ‘best week since November’ rally. The rally was extraordinarily narrow — driven by a few Mag 7 names (NVDA, META, GOOG, AMZN) while the broader index was internally deteriorating.

COR1M at 13.58 is THE LOWEST 1-month implied correlation print of the entire war by a wide margin. The combination of collapsing breadth + collapsing correlations is rare and specific — it tells you Friday’s selling was extremely idiosyncratic / sectoral, with individual names trading on their own fundamentals while the index was being held up by a few mega-caps. CIBR −3.71%, USMV −1.18%, XLF −1.09% all moving on different stories. A genuinely macro-driven regime break (which Monday SHOULD be) typically produces SPIKING correlations as everything sells together. If COR1M Monday spikes above 17, the macro-shock thesis is confirmed. If COR1M holds below 16, today’s tape is BOTH a macro shock AND an idiosyncratic regime — which would be unprecedented.

DXY Bid +0.37% — First Clean Dollar Safe-Haven Print In Over A Week.

DXY at 98.800 (+0.37%) with EVERY G10 currency red against the dollar. The dollar safe-haven bid is back after being absent through the entire post-ceasefire rally. AUD −0.67% leads G10 declines (commodity/risk-sensitive currency). NZD −0.47%. EUR −0.39%. GBP −0.33%. JPY −0.32%. CHF −0.21%. CAD −0.17% — the laggard decline because Canadian heavy crude benefits from the WTI surge. BTC −3.50% to $70,910 (breaking below $71K) confirms the high-beta tech-proxy regime under risk-off conditions. The DXY bid is NOT yet above 100 — the dovish-Fed thesis is still holding the dollar below the psychological level even on this escalation.

6. THE GAME PLAN

Today’s Key Events: Goldman Sachs Q1 earnings before open (first bank earnings + first corporate read post-regime-break). Limited fresh economic data. Fresh MOVE print at/after cash open is the binary of the week. Tuesday — JPM/WFC/C/BLK/JNJ (Dimon’s tone is the single highest-information signal of the week). Wednesday — BAC. Thursday — Morgan Stanley, TSMC, NFLX + Claims + Philly Fed. Friday — Regional banks + Housing Starts. April 22 — Ceasefire formally expires (de facto dead). April 28-29 — FOMC.

The Bull Case:

The Monday gap-down is CONTAINED — ES −0.60% is a measured Sunday-night move given the magnitude of the news, not panic. ES at 6,814.25 is only −42 points below Friday’s 6,816.89 close. The futures are pricing positioning unwind, not regime rupture. COR1M at 13.58 (lowest of the war) going into Monday means the macro shock is hitting a market that is extraordinarily dispersed — everything does not have to sell together. MOVE Friday close at 72.1541 (second consecutive sub-75 print) is telling you the bond complex is structurally regime-changed — the fresh Monday print would need to spike +10 points to re-enter stressed territory. Dimon’s tone Tuesday morning could provide a meaningful relief bid into XLF and the broader tape if the consumer-credit message is constructive. The Wednesday S5FD thrust (83.10) was historic even if rejected — historic thrusts rejected historically (2011, 2018) often produced retests rather than clean lows, leaving room for a lower low even within a broader bullish setup. WTI at $104 is well below the $114.87 war high — the Hormuz blockade is priced as partial, not total. Core CPI at 0.2% MoM / 2.6% YoY is soft — the Fed has some room if energy disinflates again. The 30Y at 4.929% is nowhere near the 5.00% crisis zone. TACO is the default base case — Trump extended the ceasefire deadline three times during the war and may yet find a path to re-negotiation.

The Bear Case:

THE CEASEFIRE IS DEAD. 21 hours of direct US-Iran talks collapsed. Hormuz blockade ordered. US destroyers in the strait. Iran ‘lost track’ of mines. Trump ‘warships reloaded with the best ammunition.’ Iran’s ‘only reason they are alive today is to negotiate.’ Israel struck 200+ Hezbollah targets over the weekend. 350+ killed in Wednesday’s Beirut bombardment alone. Hezbollah resumed strikes. WTI +7.88% back above 104.GoldREDonforcedliquidationsignature.Michigan47.6—ALL−TIMERECORDLOWin74yearsofdata.1−yearinflationexpectationsspikedfrom3.8104. Gold RED on forced liquidation signature. Michigan 47.6 — ALL-TIME RECORD LOW in 74 years of data. 1-year inflation expectations spiked from 3.8% to 4.8% — largest one-month jump in survey history. CPI hot at 3.3% YoY with gasoline +21.2% (largest monthly since 1967). S5FI below 50 structurally. Breadth thrust rejected in two sessions. S5FD crashed from 83.10 to 58.76 during the rally. Rally was extraordinarily narrow — a few Mag 7 names carrying the index. All 7 Mag 7 red AH for the first time since the war began. Mag 7 dispersion narrowing to 113 bp (from 750 bp Wednesday). Friday’s CPI/Michigan shock was already producing breadth damage BEFORE the weekend escalation hit. The macro shock is hitting a market that was already internally weak. Fed is maximally constrained — no cut path and no hike path. Fed governor speakers between now and April 29 likely to shift hawkish on the inflation expectations de-anchoring. Bank earnings this week will reveal consumer credit stress, fuel-cost pass-through, forward NII guidance — any cautious tone amplifies the financial sector weakness. CIBR −3.71% Friday is a separate AI disruption story layering on top. Software ( 104.GoldREDonforcedliquidationsignature.Michigan47.6—ALL−TIMERECORDLOWin74yearsofdata.1−yearinflationexpectationsspikedfrom3.8IGV) down 40% YTD is structural, unrelated to the war, and becomes more visible when Iran coverage steps back. The market is pricing a fragile recovery into a weakening underlying economy.

Regime: Ceasefire Collapse — Hormuz Blockade Ordered, Inflation Expectations De-Anchor, Breadth Thrust Rejected. Five separate signals are firing in different directions and the cleanest read is ‘macro shock layered on top of an idiosyncratic-regime micro-tape.’ Energy is exploding. International equities are gapping down with classic transmission. Gold is red on forced liquidation. DXY is bid with every G10 currency red. Yields are up across the curve (parallel bear shift with mild long-end lead). BUT — US futures are CONTAINED, MOVE Friday was sub-75, COR1M is the lowest of the war. The macro shock is hitting a market that was already showing internal failure from Friday’s data, not a market that was uniformly long. Today’s fresh MOVE and COR1M prints resolve the binary. Bank earnings week layers corporate fundamentals on top of the macro shock.

Watch List

Fresh MOVE print — the binary signal of the entire week

Friday close at 72.1541 means the Monday print would need to spike +10 points to re-enter stressed territory. Below 72 = bond crisis structurally dead under maximum stress. 72-75 = regime largely held. 75-80 = fragility returning. Above 80 = Wednesday regime call walked back. Above 85 = bond crisis is back. If MOVE prints anywhere below 80 despite the ceasefire collapse, it is the strongest possible confirmation that the bond complex is structurally regime-changed.

Fresh COR1M print — macro shock vs idiosyncratic regime

COR1M at 13.58 is the lowest of the entire war. A genuinely macro-driven regime break typically produces SPIKING correlations. If COR1M Monday spikes above 17, the macro-shock thesis is confirmed and the idiosyncratic regime is over. If COR1M holds below 16, today’s tape is BOTH a macro shock AND an idiosyncratic regime — unprecedented in this cycle.

Goldman Sachs Q1 earnings before the open — first bank post-regime-break

GS opens bank earnings week with the first corporate read on the post-ceasefire-collapse tape. Trading revenues are likely strong on the volatility. Investment banking guidance is the key tell — if GS signals continued deal pipeline strength despite the macro shock, the XLF unwind may be premature. If GS signals caution, the financials weakness amplifies.

Tuesday’s JPM/WFC/C/BLK/JNJ — Dimon’s tone is the single most important signal of the week

Dimon on consumer credit, oil-shock impact, and forward NII guidance is the highest-information corporate-fundamentals signal of the week. A constructive message provides meaningful relief bid into XLF. A cautious message extends Friday’s financial sector weakness aggressively. BlackRock’s institutional flow data is the secondary read on whether real money is buying or selling the regime.

Gold behavior in the first hour — forced liquidation resolution

Gold’s first-hour cash trade is the cleanest test of whether today’s red is positioning unwind or deeper structural de-risk. If gold reverses higher in the first 30 minutes, the forced-liquidation read needs to be downgraded. If gold continues to sell, the third forced-liquidation episode of the war is confirmed and the metals hedge is structurally broken for this regime.

Mag 7 dispersion — the narrow-rally signature

Mag 7 dispersion has narrowed from Wednesday’s 750 bp intra-Mag 7 spread to today’s 113 bp pre-market spread. If that compression continues through cash trading, the few stocks holding up the index are losing their bid simultaneously — and that is the early signature of a broader equity unwind. META and AMZN holding their idiosyncratic stories through cash trading is the actual test.

April 22 ceasefire formal expiration — de facto dead but watch the rhetoric

The two-week ceasefire framework formally expires April 22 (Wednesday of next week). With talks failed and blockade ordered, the expiration will likely be a non-event since the framework is already de facto dead. But any formal Iranian or US announcement on the date itself is the next narrative inflection.

Morning check: Day 45. The ceasefire is dead. Twenty-one hours of direct US-Iran talks collapsed Sunday morning over Iran’s refusal to commit not to seek nuclear weapons. Vance told reporters Iran ‘chose not to accept our terms.’ Trump ordered the Navy to blockade Iranian ports. US destroyers entered Hormuz for the first time since the war began. Iran ‘lost track’ of its mines. Trump: warships ‘reloaded with the best ammunition.’ WTI +7.88% back above $104. Gold red on forced liquidation. Dollar bid with every G10 currency red. Friday delivered the data that set the stage: CPI 3.3% YoY with gasoline +21.2% (largest monthly since 1967), and Michigan Consumer Sentiment at 47.6 — the lowest reading in 74 years, lower than 1980, lower than 2008, lower than the pandemic. One-year inflation expectations spiked 100 basis points in a single month to 4.8%. The Fed is now maximally constrained. The breadth thrust from Wednesday was rejected in two sessions during the ‘best week since November’ rally — the rally was extraordinarily narrow. S5FI is still below 50. COR1M at 13.58 is the lowest of the entire war. The macro shock is hitting a market that was already internally weak. And yet — ES is only −42 points below Friday’s close. MOVE Friday was 72.15. The bond complex and the equity-correlation complex are telling a story that the rest of the tape is not. Two regimes may be operating in parallel for the first time in this cycle. Dimon Tuesday. Powell April 29. The Hormuz blockade today. Take the regime break seriously, but watch the MOVE print — it’s the only number that will tell you which regime is actually in charge.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.