☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

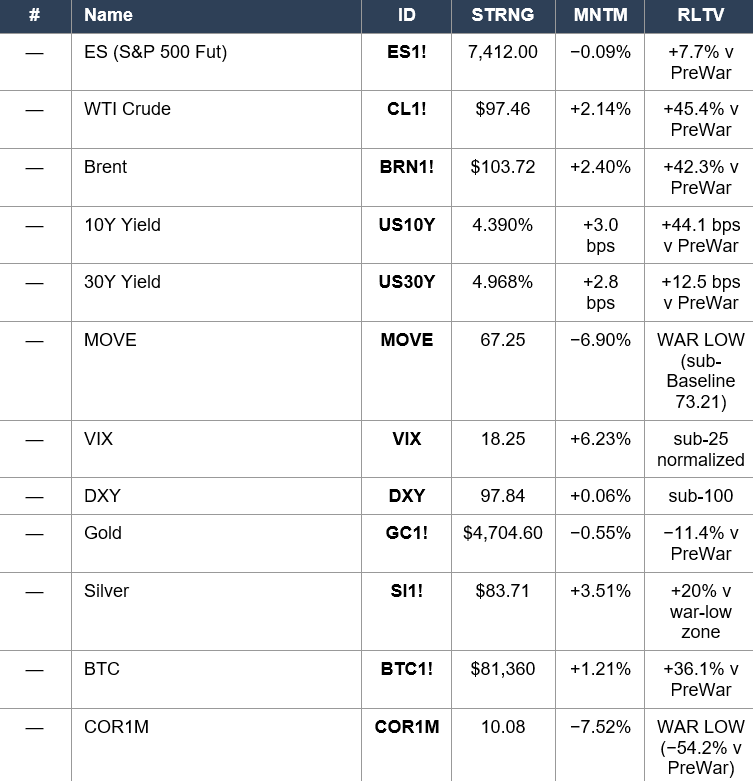

Overnight Tape Summary: IRAN PEACE TALKS COLLAPSED OVER THE WEEKEND. TRUMP REJECTED TEHRAN’S COUNTER-PROPOSAL — HORMUZ SOVEREIGNTY, WAR REPARATIONS, SANCTIONS RELIEF, NO NUCLEAR-PROGRAM CONCESSION — AS “TOTALLY UNACCEPTABLE.” THE OIL SHOCK HAS RE-ENGAGED. WTI $97.46 (+2.14%), BRENT $103.72 (+2.40%). YET MOVE COLLAPSED −6.90% TO 67.25 — THE DEEPEST SUB-BASELINE READING OF THE ENTIRE WAR. THE BOND MARKET IS SIGNALING ALL-CLEAR EVEN AS PEACE FAILS AND OIL SURGES. ES 7,412 (−0.09%) HOLDS THE WAR-HIGH PREMIUM. SOXX +5.67%, XLK +3.44% — SEMIS/TECH EXPLODING IN PRE-MARKET. VALUE +4.45%, MOMENTUM +2.68%, HIGH BETA +2.08% LEADING FACTORS. USMV−SPHB SPREAD FLIPPED TO −2.34%. THE 34 MACRO FRIDAY CLOSE: QQQ STRNG 83 (WAR HIGH), XLK STRNG 84 (WAR HIGH). WARSH CONFIRMATION VOTE TUESDAY NOON. CPI TUESDAY 8:30. WARSH TAKES THE CHAIR FRIDAY.

The week opens with a regime-defining contradiction. Over the weekend, Iran submitted a counter-proposal to the US peace framework via the Pakistani mediation channel. Tehran’s terms — sovereignty recognition over the blockaded Strait of Hormuz, demand for compensation for war damages, release of frozen Iranian assets, lifting of sanctions, an end to all fighting including the Lebanon front, and conspicuously no mention of the nuclear program — were rejected by President Trump as “totally unacceptable.” The Hormuz reopening had been the central thread of the post-Day 38 “frozen conflict” framework. With Tehran’s proposal off the table and the US ambassador to the UN signaling a “very clear red line,” the diplomatic path that had been quietly pricing through markets has just been pulled. WTI gapped higher on the Sunday Asia open and held the move: $97.46 in front-month, +$2.04 (+2.14%) from Friday’s settle, with Brent at $103.72 (+2.40%). The oil shock that markets had concluded was breaking last week is back in the picture.

Yet the rates response is the opposite of what the oil tape implies. MOVE collapsed −6.90% (−4.99 points) to 67.25 — the LOWEST READING OF THE ENTIRE WAR and only −5.96 points above the pre-war 73.21 baseline. Translation: the bond market is signaling structural all-clear, even WITH oil up 2%+, peace talks failed, and yields rising across the curve (2Y +2.9 bps, 5Y +3.5 bps, 10Y +3.0 bps, 30Y +2.8 bps — a Bear Flattener). The decoupling is the cleanest cross-asset statement of the war: yields can rise; oil can rise; peace can fail; and rates volatility still compresses. The bond market has internalized the oil shock and the diplomatic stall. They are no longer regime-altering inputs. Combined with COR1M at 10.08 (−7.52%, a new war low), the macro signal is that disciplined stock-picking and sector rotation dominate, not crisis correlation.

The equity tape reflects the duality. ES at 7,412 (−0.09%) is essentially flat — the war-high premium of +7.7% above pre-war 6,881.62 is intact. Russell +0.10%, Dow −0.04%, NDX −0.13%, Topix +0.39%. But underneath the headline, the pre-market is anything but flat. SOXX +5.67% and XLK +3.44% are exploding — semiconductors and tech are extending Friday’s NFP-driven rally into a Monday gap higher. The factor tape is unambiguous: VLUE Value +4.45%, MTUM Momentum +2.68%, SPHB High Beta +2.08% — the textbook risk-on rotation. USMV Min-Vol −0.27%, SPLV Low-Vol −0.67% — defensives selling off. The USMV−SPHB spread has flipped to −2.34% (Friday: +1.78%) — a 4.12-point swing in factor leadership in two sessions. Mag 7 is split: TSLA +4.02% leading, AAPL +2.05%, NVDA +1.75%, AMZN +0.56%, GOOG +0.44% all green; META −1.16% and MSFT −1.34% — the two names carrying the heaviest capex overhangs are the day’s drags.

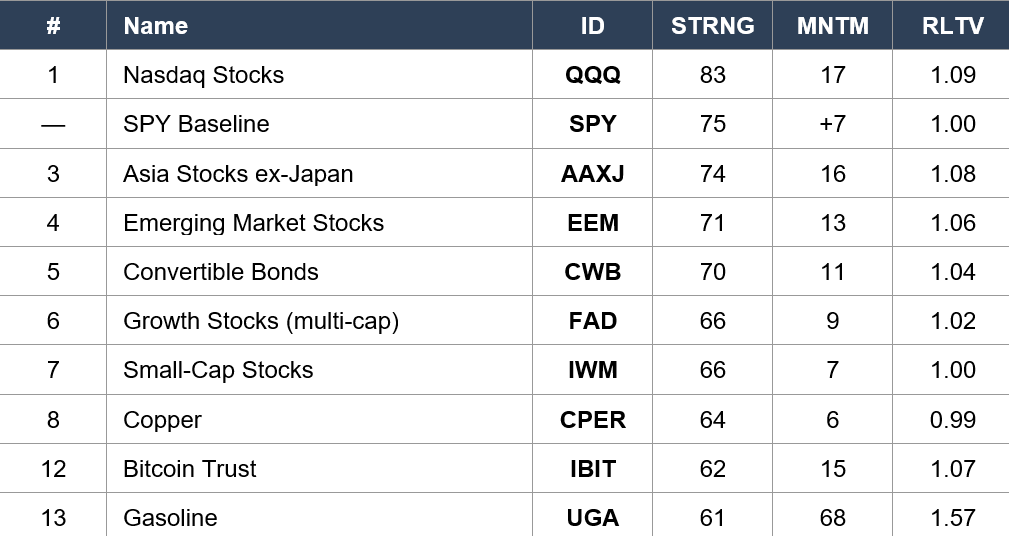

The 34 Macro Friday-close data — captured at 5:20 PM ET on the NFP session — confirms the equity complex hit NEW WAR HIGHS. QQQ at STRNG 83 / MNTM +17 / RLTV 1.09 is a NEW WAR HIGH for Nasdaq strength. XLK Technology at STRNG 84 / MNTM +24 / RLTV 1.16 is a NEW WAR HIGH for the lead sector. SMH Semiconductors at STRNG 81 / MNTM +41 / RLTV 1.32 is back at the war-high tier (the 83/44/1.35 print earlier in the run). SPY baseline at STRNG 75 / MNTM +7 / RLTV 1.00 — the broad market rebuilt strength on Friday after Thursday’s STRNG 73 compression. Bitcoin (IBIT) STRNG 62 / RLTV 1.07 — modest pullback from RLTV 1.16 earlier but firmly in the Leaders. XLE Energy at STRNG 41 / sector rank #9 / RLTV 0.98 — still sub-baseline, the war’s most consistent leadership trade is over but the sector is not collapsing.

The Number That Matters: MOVE 67.25 — A New War Low And The Deepest Sub-Baseline Reading Of The Entire Conflict. The Bond Market Is Saying: Peace Talks Can Fail, Oil Can Surge $2+, Yields Can Rise — None Of It Is Crisis-Adjacent. The Most Important Cross-Asset Indicator In Markets Is Voting Structural Disinflation Of War Premia, Even When The Underlying Geopolitics Re-Engage.

This is a regime statement of the first order. Through 74 days the MOVE has traveled from 73.21 (pre-war) to 115.02 (Day 21 war high) and now to 67.25 (Day 74 war low). The bond market that once priced an actual crisis is now pricing structural normalcy. For equity multiples this is decisive: as long as MOVE stays compressed, the war premium can stretch further regardless of headline oil moves. The Tuesday CPI print, the Tuesday Warsh confirmation vote, and the Friday Warsh transition are walking into a rates complex that has effectively dismissed the war as a vol regime input.

The Setup: Bear Flattener — Iran Talks Stall, Oil Re-Surges — Bond Market Signals All-Clear. ES Holds The War-High Premium. Tech/Semis Explode. Value/Momentum/High-Beta Lead Factors. The 34 Macro Friday Close: QQQ And XLK At New War Highs. Watch CPI Tuesday 8:30 (Consensus 0.6% / 3.7% YoY). Warsh Senate Confirmation Vote Tuesday Noon. Warsh Sworn In Friday.

2. OVERNIGHT SESSION RECAP

Weekend Catalyst — Iran Counter-Proposal Rejected

The market-moving event was the Sunday rejection. Iran submitted its counter-proposal via Pakistan, demanding (1) sovereignty recognition over Hormuz, (2) reparations for war damages, (3) release of frozen Iranian assets, (4) sanctions relief, and (5) cessation of fighting on all fronts including Lebanon — without addressing the US precondition on the nuclear program. President Trump rejected the package as “totally unacceptable.” US Ambassador to the UN Mike Waltz on Fox News Sunday said the US had laid out a “very clear red line.” Israeli PM Netanyahu separately said he wants to “wean” Israel off US military support — moving the $3.8B/year package “to zero” — and spoke with Trump Sunday evening. The diplomatic path that had been the implicit assumption behind the post-Day 38 frozen-conflict framework has narrowed sharply. The next pressure point in the Pakistan mediation cycle is now unclear.

Asia — Nikkei Heavy, Topix Held

Nikkei 62,685 (−1.59%) was the standout overnight weakness, the largest single-session Nikkei drop in three weeks. Yen at −0.25% despite a softer dollar is a paradox — typically a softer dollar (DXY −0.40% at Friday close, now +0.06%) would lift the yen, but the JPY is failing to rally, which suggests positioning is asymmetric or that the Japanese equity weakness is driving forced selling. TOPIX +0.39% — the broader Japan tape held, the weakness is concentrated in cap-weighted Nikkei names. AAXJ (Asia ex-Japan) trades on the 34 Macro Friday close at STRNG 74 / RLTV 1.08 — Leaders tier intact. China FXI at STRNG 57 / RLTV 0.89 — China complex remains weak but stable.

Europe — Modestly Red, Defense Catches A Bid

DAX 24,321 (−0.15%) and EuroStoxx 50 5,877 (−0.17%) both modestly red — much shallower than Friday’s −0.97% DAX drag. The risk tone in Europe is muted but not defensive. Notable: ITA Aerospace & Defense +0.44% pre-market — defense names catching a bid on the Iran rejection, a reversal from Friday’s −0.41%. The de-escalation discount that had been applied to defense is partially unwinding as the diplomatic stall re-engages the geopolitical risk premium.

US Pre-Market — Flat Headline, Roaring Underneath

ES 7,412.00 (−0.09%, −7 pts), NQ 29,294 (−0.13%, −38 pts), Dow 49,672 (−0.04%, −19 pts), Russell 2,871 (+0.10%, +3 pts). The headline futures move is essentially nil. But the sector / factor / thematic tape is anything but. SOXX +5.67% extending Friday’s semis surge into Monday. XLK +3.44% lifting on tech rotation. VLUE +4.45% and MTUM +2.68% — Value and Momentum are co-leading, a rare combination outside of strong macro inflections. SPHB High-Beta +2.08% confirming the risk-on bias. SPLV −0.67% and USMV −0.27% — defensives selling off in lockstep with the rotation. This is structural Monday rotation positioning into CPI Tuesday and the Warsh confirmation vote, not directional conviction either way.

Mag 7 Pre-Market — 5 Green / 2 Red, Capex Names Lagging

TSLA $428.35 (+4.02%) leading — Tesla extending Friday’s rally and pushing toward the post-earnings $430 zone. AAPL $293.32 (+2.05%) — the strongest AAPL print in weeks, reflecting the post-earnings ride (Services $31B record, margin 49.3%, iPhone +22%) finally translating to share-price. NVDA $215.20 (+1.75%) extending its run with the SOXX surge. AMZN $272.68 (+0.56%) recovering from Friday’s −1.39%. GOOG $397.05 (+0.44%) modest. META $609.63 (−1.16%) — capex overhang continuing. MSFT $415.12 (−1.34%) — the $190B capex problem still hasn’t cleared. The Mag 7 rotation pattern is clear: AI-revenue names (TSLA, AAPL, NVDA) outperforming; AI-capex-burden names (META, MSFT) lagging.

Energy — Oil Shock Re-Engages On Iran Rejection

WTI $97.46 (+2.14%) — the headline commodity move of the morning. Cumulative from pre-war: +$30.44, +45.4%. Brent $103.72 (+2.40%) — above the century mark with conviction. Heating Oil +1.24%, RBOB +1.76%, Natural Gas +2.65%. The entire petroleum complex is bid on the diplomatic stall. WTI is back in the $97-100 zone — the same zone that triggered the FOMC fracture and 30Y crossing 5.00% on Day 47-48. The difference today: MOVE is at 67.25 (vs 77.86 on Day 47) — the bond market has dramatically more capacity to absorb the oil move than it did two weeks ago. The oil-to-MOVE transmission mechanism that defined the war’s first two months has visibly weakened.

Metals — Silver Rips, Gold Pauses

Silver $83.71 (+3.51%) is the metals headline — extending Friday’s +2.13% with another big move, putting silver up nearly 6% in two sessions. The silver bid is now structural — from the war-low $70 zone to $83.71 is a +20% recovery. Copper $6.39 (+1.45%) — at year-to-date highs, the global-demand-resilience read is intact. Platinum +1.29%, Palladium +1.53%. Gold $4,704.60 (−0.55%) the lone metals weakness — first down session in four. Gold consolidating at $4,704 while silver rips is consistent with a “risk-on metals bid” rather than a “haven flight to gold” — the metals complex is now an inflation/cycle play, not a fear play.

Softs — Cocoa Explodes +12.15%

Cocoa +12.15% to $4,690 — the day’s largest single-commodity move and a +$508 jump in one session. The Cocoa surge is driven by West Africa supply concerns (Ghana / Côte d’Ivoire production shocks) and is mostly a sectoral story rather than a macro inflation signal, though confectionery-input cost passthrough will eventually flow to CPI food. Cotton +2.08%, Coffee +1.22%, Lumber +0.61%. The softs complex broadly green is a secondary inflation tail.

3. THE PRIOR DAY’S REGIME

34 Macro Price, Strength & Momentum Rankings — Daily Close, Friday May 8. SPY Baseline: STRNG 75 | MNTM +7 | RLTV 1.00.

Asset Classes — Leaders

Asset Classes — Oil Compressing / Bonds Lagging / Vol Tail

Regime signal: THE EQUITY COMPLEX REBUILT TO NEW WAR HIGHS ON THE NFP BEAT. QQQ at STRNG 83 / MNTM +17 / RLTV 1.09 is a NEW WAR HIGH for Nasdaq strength — eclipsing the prior 80 print from Wednesday May 6. SPY baseline recovered from STRNG 73 (Thursday) to STRNG 75 (Friday) — the +2-point move on the NFP-day session confirms the broad market embraced the labor data. AAXJ Asia at STRNG 74, EEM Emerging Markets STRNG 71 — international equity leadership is strong; the dollar weakness late last week supported EM. Copper CPER jumped to rank #8 at STRNG 64 — copper is now firmly in the Leaders and is an active risk-on confirmation. IBIT Bitcoin STRNG 62 / RLTV 1.07 — modest pullback in RLTV from earlier-week 1.16 but firmly Leaders-tier. USO Crude Oil dropped to rank #26 (STRNG 52 / RLTV 1.62) — the oil compression continued into Friday’s close. The bond complex remains the war’s most consistent lagger: TLT STRNG 48, IEF STRNG 47, SHY STRNG 45 — all in the bottom seven. VXX at STRNG 39 / RLTV 0.95 — fear premium effectively extinguished, the lowest STRNG VXX of the war.

Sector ETFs

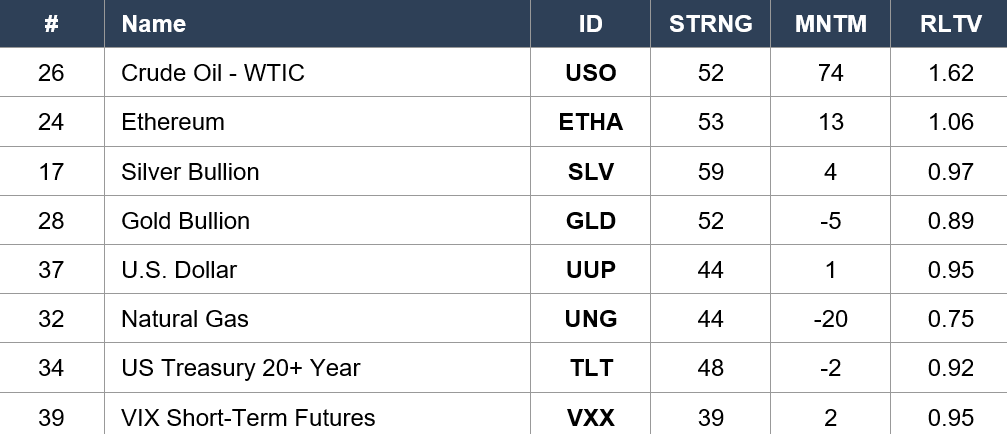

Regime signal: XLK TECHNOLOGY HIT A NEW WAR HIGH FOR SECTOR STRENGTH. XLK at STRNG 84 / MNTM +24 / RLTV 1.16 — the +4-point STRNG jump from Thursday’s 80 is the largest single-session sector-leader expansion of the war series. XLK’s RLTV at 1.16 holds the war-high zone. XLY Consumer Discretionary at STRNG 63 / RLTV 0.95 — discretionary participation in a risk-on regime continues; +1 STRNG from Thursday. XLRE Real Estate at STRNG 60 — REITs catching the falling-yields bid. The CRITICAL development is XLP Consumer Staples jumping to rank #4 at STRNG 57 — a defensive lifting INTO the Middle tier on a risk-on session is unusual and may reflect post-NFP positioning sleepers (staples names with international exposure benefiting from a weaker dollar). XLE Energy at STRNG 41 / rank #9 / RLTV 0.98 — sub-baseline for the second consecutive session, confirming the war’s most consistent leadership trade has ended. XLV Health-Care fell to STRNG 40 / rank #10 — defensive collapse. XLU Utilities at STRNG 38 / RLTV 0.97 — the deepest sector lagger position of the entire war series. The sector tape is now the cleanest possible risk-on configuration: Tech leading at a war high, Discretionary participating, defensives at war lows, Energy normalizing.

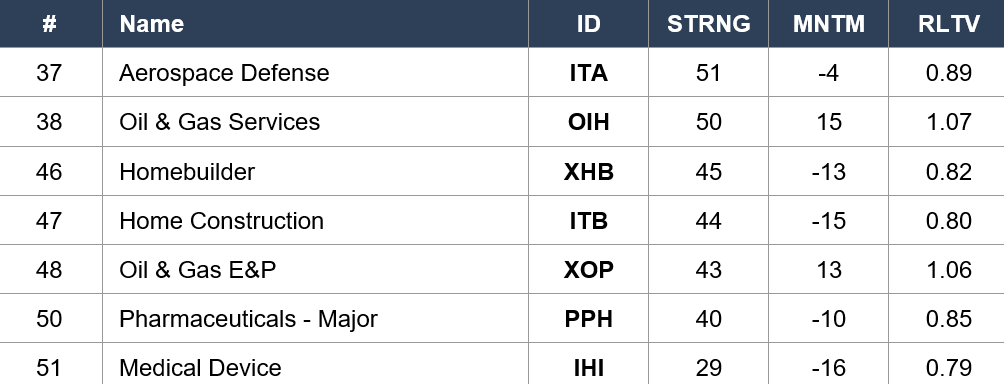

Industry ETFs — Leaders

Industry ETFs — Laggers

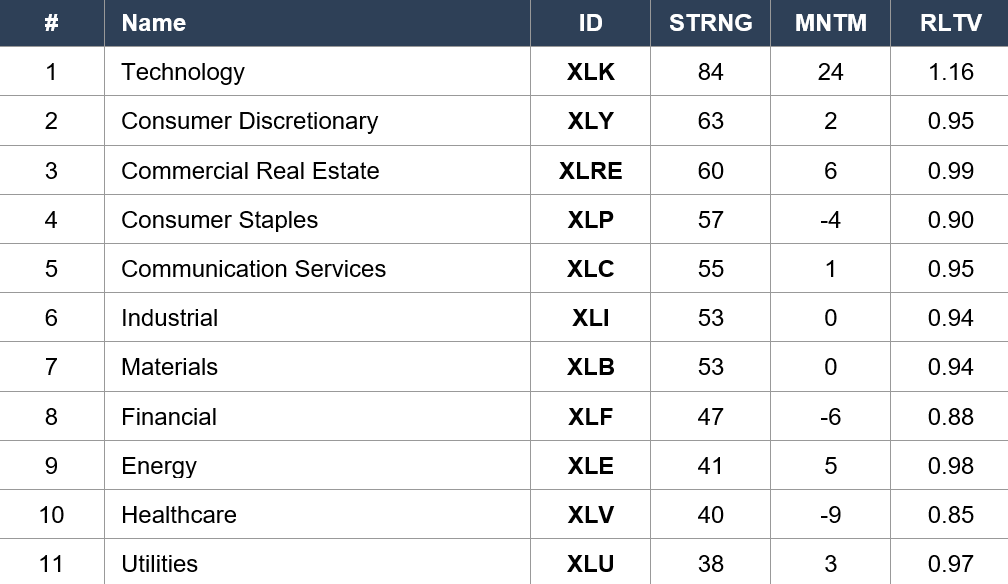

Regime signal: AI/SEMIS DOMINANCE INTACT, CLEAN-ENERGY COMPLEX EMERGES, MEDICAL DEVICES POST NEW WAR LOW. SMH Semiconductor at STRNG 81 / MNTM +41 / RLTV 1.32 — back to the war-high tier (prior peak 83/44/1.35). The +4 STRNG move from Thursday’s 77 confirms semis are re-asserting leadership. The Top 10 reads as a powerful AI/clean-tech configuration: SMH, SNSR (IoT), CIBR (Cyber), BOTZ (Robotics & AI moving up from STRNG 68 to 74, a +6 point jump), PBW (Clean Energy +4 to 72 / RLTV 1.11), SLX (Steel), LIT (Lithium RLTV 1.19), QCLN (Clean Edge +3 to 68 / RLTV 1.13), IGV (Software), ICLN (Clean Energy), TAN (Solar). The CLEAN ENERGY COMPLEX (PBW, QCLN, ICLN, TAN, FAN Wind, all RLTV > 1.00) is now a coherent leading theme — a notable development given two months of clean-energy-policy headwinds. BOAT Shipping at STRNG 63 / RLTV 1.10 — global trade flows bid amid the Hormuz uncertainty. The Laggers: IHI Medical Devices at STRNG 29 / RLTV 0.79 — a NEW WAR LOW for industry-level strength (prior low 33 just last week). PPH Pharma Major STRNG 40 — deteriorating further. ITA Defense at STRNG 51 / RLTV 0.89 — defense at the bottom on Friday’s close, despite Monday’s pre-market bid post-Iran rejection. XHB Homebuilders and ITB Home Construction at the bottom of the rates-sensitive complex (RLTV 0.82 and 0.80). XOP Oil & Gas E&P at #48 — the upstream complex remains the worst-performing energy industry despite the WTI premium. The capital is concentrated in AI/clean-tech speculation; rates-sensitive housing, defensive pharma/medtech, and traditional value cohorts remain deeply lagging.

4. MORNING DATA REACTION

No US Data Pre-Market — All Eyes On Tuesday

The Monday session is data-light by design — the week’s entire macro arc is loaded into Tuesday-Thursday. No US prints before the bell. The morning narrative is therefore being defined by (1) the weekend Iran rejection and oil shock, and (2) Friday’s NFP follow-through in cross-asset positioning. The DYRH timestamp at 8:50 AM EST captures pre-CPI positioning rather than data response.

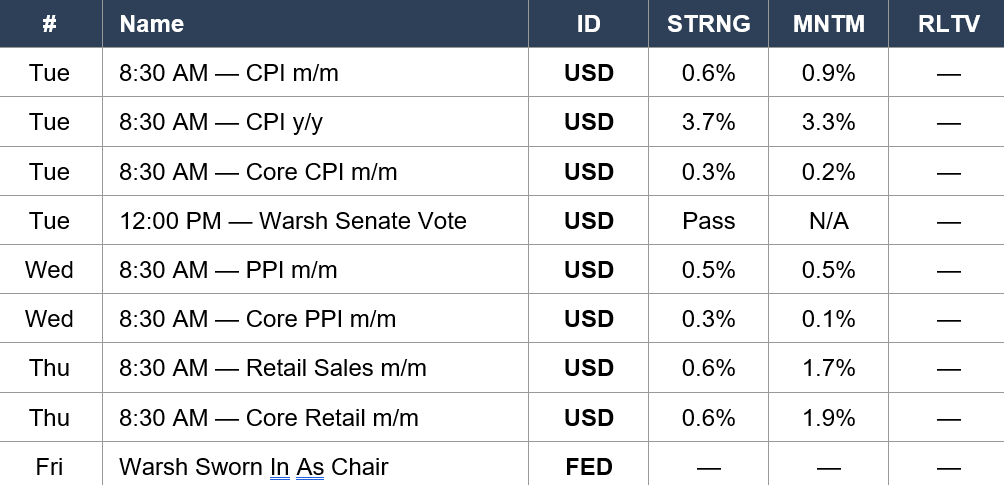

This Week — The Heaviest US Macro Calendar Of The War

CPI Tuesday — The First $94+ Oil Inflation Read

April CPI is the most important data print of the war’s endgame phase. Consensus: 0.6% m/m headline (vs 0.9% prior — a deceleration on monthly basis but with the YoY accelerating to 3.7% from 3.3%). Core CPI: 0.3% (vs 0.2% prior). The 0.6% headline consensus is built around gasoline pass-through (gasoline retail spike of ~21% recorded in March CPI flowing into April), and the 3.7% YoY is the highest reading since 2022. Watch the energy contribution carefully — with WTI averaging $90-95 across April and now back to $97, the energy disinflation is paused. Watch shelter for any easing as front-end yields have fallen. Watch services ex-shelter as the Fed’s preferred core measure.

Warsh Confirmation Vote Tuesday 12:00 PM

The Senate floor vote on Kevin Warsh as Fed Chair is scheduled for noon Tuesday. The vote is expected to pass — Warsh cleared the Banking Committee on the FOMC week earlier in the run. Confirmation is procedural but symbolically critical; with Warsh formally confirmed Tuesday, the path to his Friday May 15 swearing-in is clear. Market reaction will hinge on the vote margin (broad bipartisan support = continuity; narrow margin = hawkish lean signal).

5. THE DYRH READ

Yield Curve Regime: Bear Flattener

The curve flipped to a Bear Flattener on the Iran rejection / oil shock combination. Yields rising at every tenor with the front end rising faster: 2Y +2.9 bps to 3.918%, 5Y +3.5 bps to 4.041%, 10Y +3.0 bps to 4.390%, 30Y +2.8 bps to 4.968%. The 2s/30s spread is 105.0 bps — modest curve compression. The Bear Flattener signals (1) renewed inflation pricing on the oil move at the long end, (2) trimming of front-end cut pricing on the labor strength + oil resurgence combination, with the market essentially debating whether Warsh will lean hawkish on day one. The 30Y at 4.968% is only 3.2 bps below the 5.00% crisis threshold — close, but the rates VOL (MOVE 67.25) says the market is comfortable holding there.

MOVE Index: 67.25 (−6.90%) — New War Low

MOVE collapsed −4.99 points to 67.25 — the LOWEST READING OF THE ENTIRE 74-DAY WAR. From the Day 21 war high of 115.02, MOVE has declined 47.77 points (−41.5%). MOVE is now only −5.96 points below the pre-war 73.21 baseline — the closest the rates complex has come to fully normalizing since the war began. The cleanest cross-asset statement: MOVE compressed by nearly 7% even with oil up 2.14%, peace talks failed, and yields up 3 bps. The bond market has internalized the oil shock and the diplomatic stall and is signaling structural disinflation of war-vol premia. As long as MOVE sits below 70, the equity multiple has room to extend.

S&P 500: ES 7,412 — War-High Premium Intact

ES at 7,412.00 is essentially flat (−0.09%, −7 pts) but holds +7.7% above the pre-war 6,881.62 baseline. The cumulative gain of +530.38 ES points has been earned through 74 days of war, oil shocks, a fractured FOMC, three Mag 7 capex shocks, and now a failed weekend peace push. The market’s ability to hold the war-high premium through Sunday’s Iran rejection is the most important behavioral signal: the war is no longer a regime-altering input. Through the Tuesday CPI and the Friday Warsh handoff, the burden of proof has shifted to bears.

Key Levels & Cumulative War Moves

Volatility & Breadth — Two-Way Signals

VIX 18.25 (+6.23%) — equity vol expanded on the weekend news, but the absolute level remains well below 25. VVIX 96.78 (+3.39%) expanded modestly. VXN 23.76 (+2.63%) — Nasdaq vol up despite the SOXX surge, which suggests options markets are not yet pricing the tech rally as durable. VIX1D 12.70 (+2.58%) — short-vol bid is muted, no immediate event concern beyond CPI. GVZ Gold-Vol 26.48 (−2.03%) — gold-vol compressing alongside gold price weakness. MOVE 67.25 (−6.90%) — the war low. The vol complex is two-way: rates vol all-clear vs equity vol modestly expanding. Breadth holds the constructive Friday read with S5TH 70.10, S5FI 61.30, R2TH 51.20. COR1M at 10.08 (−7.52%) — a new war-low correlation reading, the deepest stock-picker regime of the war.

6. THE GAME PLAN

Today: No US data. Iran rejection / oil shock the morning narrative. Cross-asset positioning into CPI Tuesday. Heavy week: CPI Tue 8:30 + Warsh Senate vote Tue 12:00 + PPI Wed 8:30 + Retail Sales Thu 8:30 + Warsh sworn in Friday May 15. Earnings: CEG / CRCL today, JD Tue, CSCO / BABA Wed, AMAT Thu.

The Bull Case

MOVE 67.25 — a NEW WAR LOW for rates vol, the deepest sub-baseline reading of the entire 74-day conflict. The bond market has internalized the oil shock and the diplomatic stall. ES 7,412 holds +7.7% above pre-war — the war-high premium is intact through the weekend’s adverse news. SOXX +5.67% and XLK +3.44% pre-market — semis and tech extending Friday’s rally. VLUE +4.45%, MTUM +2.68%, SPHB +2.08% — the textbook risk-on factor rotation; USMV−SPHB spread flipped to −2.34% (a 4.12-point swing from Friday’s +1.78%). 34 Macro Friday close: QQQ STRNG 83 (NEW WAR HIGH), XLK STRNG 84 (NEW WAR HIGH), SMH STRNG 81 (war-high tier), BOTZ STRNG 74 (jumped from 68), clean-energy complex (PBW, QCLN, ICLN, TAN, FAN) all RLTV >1.00 as a new leading theme. Bitcoin (IBIT) STRNG 62 / RLTV 1.07. Silver +3.51% and Copper +1.45% — base/precious metals confirming the risk-on tape. AAPL +2.05% and TSLA +4.02% — the AI-revenue Mag 7 names leading. COR1M at 10.08 — a new war-low correlation reading, confirming stock-pickers and sector rotation dominate. If CPI Tuesday prints inline (3.7% YoY consensus), Warsh confirmation passes broadly, and PPI / Retail Sales follow suit, the equity complex enters the Warsh era at war-high premium with the rates complex fully normalized.

The Bear Case

The Iran peace track has just collapsed. Trump rejected Tehran’s counter-proposal as “totally unacceptable” — the Hormuz reopening framework that markets had quietly priced is in disarray. Netanyahu signaled US-Israel military aid divergence. WTI back to $97.46 / +45.4% from pre-war / +2.14% in one session. Brent above $103. With oil reasserting upward and CPI Tuesday’s YoY at 3.7% consensus (highest since 2022), the inflation risk has re-entered the regime. Yields rising across the curve (Bear Flattener). Mag 7 split with META −1.16% and MSFT −1.34% — the AI-capex overhang is still active. Nikkei −1.59% — the largest international weakness in weeks. ITA Defense bidding pre-market — geopolitical hedge re-engaging. IHI Medical Devices at STRNG 29 / NEW WAR LOW — defensive healthcare cracking. XLU Utilities at STRNG 38 — the deepest sector lagger of the war series. If CPI prints hot (above 3.7% YoY or above 0.3% core), the Bear Flattener intensifies, MOVE bounces off the 67.25 low, and the rates-vol-driven equity multiple expansion unwinds in 24 hours. Warsh confirmation on a narrow margin would signal hawkish risk into the FOMC handoff.

Regime: Bear Flattener — Iran Talks Stall, Oil Re-Surges — Bond Market Signals All-Clear. The most important regime statement is the divergence — MOVE collapsed to a war low even as the oil shock re-engaged and peace talks failed. The bond market has structurally separated the geopolitical regime from the rates regime. As long as MOVE stays below 70, equity multiples can extend. The week’s tests: CPI Tuesday 8:30 (the first $94+ oil inflation print), Warsh Senate vote Tuesday 12:00, PPI Wednesday, Retail Sales Thursday, Warsh sworn in Friday May 15. Five days to a new Fed chair inheriting the most internally consistent risk-on regime of the war.

Watch List

Tuesday 8:30 AM — April CPI / Core CPI

Consensus: headline 0.6% m/m (vs 0.9% prior), 3.7% YoY (vs 3.3%), Core 0.3% m/m (vs 0.2%). The 3.7% YoY would be the highest annual headline reading since 2022. Watch energy contribution carefully — April averaged $90-95 WTI before today’s re-surge to $97. Watch shelter for any easing reflecting front-end yields lower. Above 0.7% headline / 0.4% core = hot, Bear Flattener intensifies, MOVE bounces, equity multiple compresses. Inline 0.6% headline / 0.3% core = neutral, market churns. Below 0.5% headline / 0.2% core = cool, MOVE compression extends, equity multiple expands further.

Tuesday 12:00 PM — Warsh Senate Confirmation Vote

Procedural vote on Kevin Warsh as Fed Chair. Expected to pass. Watch the margin — broad bipartisan support signals policy continuity; narrow margin or significant Democratic opposition would signal hawkish lean and could re-engage the FOMC fracture (Hammack/Kashkari/Logan vs Miran). If the vote slips or is delayed, the May 15 handoff timeline becomes uncertain and the rates complex re-prices.

Wednesday 8:30 AM — April PPI / Core PPI + Earnings (CSCO, BABA)

PPI consensus: headline 0.5% m/m (vs 0.5% prior), Core 0.3% (vs 0.1% prior — a notable acceleration). PPI is the cleanest read on ISM Prices Paid pass-through given the 84.6 reading on the manufacturing print. CSCO (Cisco Systems) reports — networking/enterprise tech, key for the AI-infrastructure thesis. BABA (Alibaba) reports — China consumer and the cleanest read on EM consumer in a $97 oil environment.

Thursday 8:30 AM — April Retail Sales + AMAT Earnings

Retail Sales consensus: 0.6% m/m headline (vs 1.7% prior — significant deceleration), Core 0.6% (vs 1.9%). With NFP +115K and AHE 0.2% miss, retail sales is the consumer-spending validation. AMAT (Applied Materials) — the semiconductor capital-equipment bellwether and the cleanest AI-capex confirmation. With SMH at STRNG 81 / RLTV 1.32, AMAT’s commentary on China, foundry orders, and DRAM/NAND capex will move SOXX and the broader semis complex meaningfully.

Friday May 15 — Warsh Takes The Chair

Day 78 of the war. Kevin Warsh is sworn in as Fed Chair, the first chair transition since Powell took office in 2018. Warsh inherits MOVE at war-low (currently 67.25), ES at war-high premium, an FOMC fractured 8-4 between hawks and doves, and an oil shock that has just re-engaged after a five-day pullback. Warsh’s first FOMC is June 17-18. Market positioning into the handoff will be defined by this week’s CPI/PPI/Retail Sales prints.

Today’s Earnings — CEG (Constellation Energy) AMC, CRCL (Circle Internet) AMC

CEG reports after the close. Constellation Energy is the cleanest read on power demand for AI data centers — the AI-capex story’s back-end. With the AI complex (SMH, BOTZ, IGV) re-asserting leadership and capacity constraints visible across the data-center pipeline, CEG’s commentary on nuclear PPA pricing and AI-driven demand visibility matters for the entire AI ecosystem. CRCL (Circle Internet, the USDC stablecoin issuer) reports — the cleanest crypto-payments read alongside IBIT Bitcoin STRNG 62 / RLTV 1.07.

Energy — Iran Talks Failed, Oil Back To $97

WTI bounced from Wednesday’s $90.54 low to $97.46 in three sessions — a +$6.92 / +7.6% retracement. The five-session crash from $108 was always at risk of an Iran-news reversal, and the weekend rejection delivered exactly that. Watch for next pressure points: another Pakistan-mediated round (timing unknown), any Hormuz incident (immediate snap to $100+), or US-Iran direct contact. WTI between $95-100 is the new equilibrium until either side moves the diplomatic frame. XLE Energy at STRNG 41 / sector rank #9 reflects the equity market’s view that even with oil back to $97, the demand-destruction discount remains embedded.

AI/Semis — SOXX +5.67% Pre-Market — Is This A Goldman Upgrade Or Structural?

SOXX +5.67% in pre-market is a massive single-session move and signals either a specific catalyst (analyst upgrade, capacity-utilization announcement, NVDA / AVGO / TSM data) or a structural rotation back into semis on the AI-revenue thesis post-MSFT / META capex shock. SMH at STRNG 81 / MNTM +41 / RLTV 1.32 supports the structural read. If today’s SOXX print holds into the close, the AI rotation regime is confirmed and AMAT Thursday earnings becomes the catalyst for the next leg. If SOXX fades during the day, it’s a Friday-NFP residual that will mean-revert.

Morning check: Day 74. The weekend changed the diplomatic picture. Iran submitted a counter-proposal via Pakistan demanding Hormuz sovereignty, reparations, sanctions relief, and an end to all fighting — without addressing the nuclear program. Trump rejected it as “totally unacceptable.” US Ambassador Waltz signaled a “very clear red line.” The Hormuz reopening framework that had been quietly pricing through markets has stalled. WTI gapped to $97.46 (+2.14%) and Brent crossed $103.72 (+2.40%) on the Sunday news. Yields rose across the curve into a Bear Flattener: 2Y +2.9 bps, 5Y +3.5 bps, 10Y +3.0 bps to 4.390%, 30Y +2.8 bps to 4.968%. And yet — the bond market’s vol complex collapsed. MOVE −6.90% to 67.25 — a NEW WAR LOW, the lowest single reading of rates volatility in the entire 74-day conflict, only −5.96 points below the pre-war 73.21 baseline. The decoupling is the cross-asset statement of the war’s endgame phase: oil can rise, peace can fail, yields can climb, and the rates complex still signals structural all-clear. ES 7,412 (−0.09%) holds +7.7% above pre-war 6,881.62 — the war-high premium is intact through the weekend’s adverse news. SOXX +5.67% and XLK +3.44% pre-market — semis and tech exploding. VLUE +4.45%, MTUM +2.68%, SPHB +2.08% — Value, Momentum, and High Beta co-leading. USMV−SPHB spread flipped to −2.34% (vs +1.78% Friday). The 34 Macro Friday close: QQQ at STRNG 83 (NEW WAR HIGH), XLK at STRNG 84 (NEW WAR HIGH), SMH at STRNG 81 / RLTV 1.32 (war-high tier), BOTZ jumped to STRNG 74, the clean-energy complex (PBW / QCLN / ICLN / TAN / FAN) emerged as a coherent leading theme with all RLTVs above 1.00. The Laggers: IHI Medical Devices at STRNG 29 (NEW WAR LOW for industry strength), XLU Utilities at STRNG 38 (deepest sector lagger of the war), XHB / ITB at the bottom of the rates-sensitive complex. COR1M at 10.08 — a new war-low correlation reading, the deepest stock-picker regime of the entire 74-day series. The week ahead is the heaviest US macro calendar of the war: CPI Tuesday 8:30 (0.6% / 3.7% YoY / 0.3% core consensus), Warsh Senate confirmation vote Tuesday noon, PPI Wednesday, Retail Sales Thursday, Warsh sworn in Friday May 15. AMAT semis-capex bellwether Thursday. The five-day arc into a new Fed chair, taking over a market at war-high premium with rates vol at war low. Pressure, not panic. Regime, not reaction. The bond market has spoken.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.