☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: OIL RELIEF RALLY — ES 7,342.25 (+0.75%). WTI CRASHED −7.43% TO $94.67 — BELOW $100 FOR THE FIRST TIME IN EIGHT SESSIONS. BRENT −6.42% TO $102.82. THE OIL SHOCK IS BREAKING. YIELDS PLUNGING: 10Y −7.2 BPS TO 4.354%, 30Y −5.3 BPS TO 4.938% — BELOW THE 5.00% CRISIS THRESHOLD. MOVE 76.78 (−1.40%) COMPRESSING BUT STILL ABOVE BASELINE. NQ +1.17%. RUSSELL +1.36% OUTPERFORMING. DAX +2.16%. NIKKEI +2.15%. GOLD +2.71% — METALS SURGING. SILVER +5.13%. BTC $82,690. ADP 8:15 AM TODAY (118K CONSENSUS). NFP FRIDAY (65K). ALL 10/11 SECTORS GREEN. FACTOR TAPE DEEPLY RISK-ON: VLUE +3.54%, MTUM +2.40%.

The oil shock is breaking. WTI crashed −7.43% overnight to $94.67 — the largest single-session crude decline since the Day 29 post-ceasefire collapse and the first print below $100 in eight consecutive sessions. Brent fell −6.42% to $102.82. The catalyst appears to be a combination of: (1) Growing expectations of diplomatic progress after Pakistan’s PM Sharif intensified mediation efforts; (2) Reports of shadow-fleet supply leakage past the blockade expanding (Senator Murphy cited 28+ vessels); (3) Technical correction after WTI reached $108+ last week — the short-term oil market was overextended. The WTI breakdown below $100 removes the acute inflation-pass-through pressure that had driven the FOMC fracture, the MOVE explosion to 77.86, and the 30Y crossing 5.00%. If oil holds below $100, the entire rates-stress narrative from the past week begins to unwind.

The rates response is dramatic and immediate. The 10Y plunged −7.2 bps to 4.354% — the largest single-session yield decline since the Day 37 oil-crash bull flattener. The 30Y fell −5.3 bps to 4.938%, pulling decisively BELOW the 5.00% crisis threshold that had been breached on Monday. The 2Y at 3.876% (−7.0 bps) is the sharpest front-end decline since the post-FOMC recovery. The 5Y at 4.001% fell 8.2 bps — the largest move of any tenor. This is a full BULL FLATTENER driven by the oil relief: the energy-inflation expectations channel is compressing as oil falls, allowing the front end to add back rate-cut probability and the long end to release term premium. MOVE at 76.78 (−1.40%) is compressing but remains 3.57 points above the 73.21 baseline — the bond market is easing but has NOT returned to sub-baseline comfort.

The equity tape is in full risk-on mode. ES +0.75%, NQ +1.17% (tech leadership returning), Russell +1.36% OUTPERFORMING (the strongest small-cap bid in over a week). Nikkei +2.15%, DAX +2.16%, EuroStoxx +2.66% — global markets surging on the oil relief. The factor tape is the most constructive of the past two weeks: VLUE +3.54% LEADING, MTUM +2.40%, SPHB +2.27%, LRGF +2.19%, IJR +1.93%, QUAL +1.92%, IJH +1.84%, USMV +1.66%, DGRO +1.33%, RSP +1.15%, VYM +0.68%, SPLV +0.39%. ALL 12 FACTORS GREEN — the first time since the May 1 ISM day. The breadth is extraordinary.

Gold at $4,692.20 (+2.71%) is SURGING — the strongest single-session gold rally since the post-forced-liquidation recovery. Silver +5.13%, Platinum +3.07%, Palladium +2.89%, Copper +3.55%. The entire metals complex is catching a massive bid. The gold rally on an oil-crash day tells you: the forced-liquidation episode from the past two weeks is OVER. Gold is now responding to its traditional macro drivers (falling yields, weaker dollar) rather than being sold for margin calls. DXY at 97.775 (−0.60%) confirms: dollar weakening as the oil-relief eases the demand for USD-denominated energy hedges.

ADP private payrolls at 8:15 AM today: consensus 118K, prior 62K. This is the pre-read for Friday’s NFP (65K consensus). If ADP confirms the labor market is decelerating (near or below 118K), the NFP risk is to the downside. If ADP surprises materially to the upside (150K+), NFP expectations may be revised higher.

The Number That Matters: WTI $94.67 (−7.43%). Below $100 For The First Time In Eight Sessions. The Oil Shock Is Breaking. And With It — The Entire Rates-Stress Architecture Of The Past Week.

$100 oil drove: the FOMC fracture, MOVE to 77.86, the 30Y above 5.00%, ISM Prices Paid to 84.6, and the bear flattener that removed all rate-cut pricing. $95 oil reverses that chain: the inflation-expectations channel eases, the front end adds back cut probability, the 30Y retreats below 5.00%, MOVE compresses. If WTI holds below $100 through Friday’s NFP, the MOVE-equity divergence from yesterday resolves in EQUITIES’ FAVOR — the bond market was right to be stressed about $108 oil, and it is right to be relieved by $95 oil.

The Setup: Bull Flattener — Risk-On — Oil Relief Rally. WTI Below $100. Yields Plunging. MOVE Compressing But Still Above Baseline. All Factors Green. Metals Surging. ADP 8:15 AM. NFP Friday. The Oil Shock Is Breaking And The Market Is Pricing The Endgame.

2. OVERNIGHT SESSION RECAP

Tuesday Cash Session — Mixed/Indeterminate

Tuesday settled mixed: 2Y flat at 3.946%, 5Y +0.4 bps, 10Y −0.6 bps, 30Y −2.2 bps to 4.991%. The 30Y pulling back from Monday’s 5.013% was the first signal the crisis-threshold breach was not sustainable. ISM Services Employment improved to 48.0 from 45.2 in March — services labor stabilizing after the manufacturing employment crash. JOLTS job openings were essentially unchanged at 6.9M — labor demand holding. The ISM/JOLTS combination was ‘not great, not terrible’ — consistent with the soft-landing-with-elevated-inflation framework.

Overnight — Oil Crash + Global Risk-On

WTI crashed from $102.40 (Tuesday close range) to $94.67 (−7.43%) overnight. Brent from $109+ to $102.82 (−6.42%). The crash happened during Asian trading hours and extended into European open. The catalyst combination: (1) Diplomatic progress reports — Pakistan’s PM Sharif reportedly held phone calls with both Trump and Iran’s Supreme Leader Khamenei on Tuesday evening, suggesting a framework for resuming talks; (2) Shadow-fleet leakage — satellite imagery shows an increasing number of tankers bypassing the US blockade via longer routes; (3) Technical exhaustion — WTI at $108+ was the most overbought reading since the war began. The oil crash triggered the yield plunge and the equity rally in sequence: oil fell → inflation expectations eased → yields fell → rate-cut probability added back → equities bid → metals bid on weaker dollar.

Asia-Pacific / Europe

Nikkei +2.15% to 61,945 — Japan’s LARGEST single-session rally since the Day 29 post-ceasefire thrust. DAX +2.16% to 25,017. EuroStoxx +2.66% to 5,993. The global risk-on is the broadest since the post-ceasefire period. The oil relief is particularly constructive for European markets — Brent below $103 eases the energy-cost burden that had been pressuring European industrials for weeks.

US Pre-Market

Day 69 of Operation Epic Fury. Q2 Day 26. Wednesday — ADP day ahead of NFP Friday.

Mag 7 THREE GREEN / FOUR RED: AAPL +2.66% LEADING (continuing the post-earnings recovery — Apple is now the strongest Mag 7 name of the past week). GOOG +1.22%. AMZN +0.55%. MSFT −0.54%. TSLA −0.80%. META −0.89%. NVDA −1.00% (semis selling despite the risk-on — the NVDA capex concern from last week persists). The Mag 7 at 3 green / 4 red while ES is +0.75% and ALL 12 factors are green tells you the rally is BROAD-BASED, not Mag-7-driven. The non-Mag 7 market is carrying.

SECTORS 10/11 GREEN: XLK +2.21% LEADING (tech on the yield plunge). XLB +1.74%. XLI +0.84%. XLP +0.62%. XLV +0.39%. XLY +0.30%. XLRE +0.20%. XLE +0.10% (energy barely green despite −7.43% WTI — the demand-destruction discount is being REMOVED as oil falls, which is net positive for energy equities even though the commodity itself is down). XLF +0.02%. Only XLC −0.40% red (META drag). The 10/11 green is the broadest sector participation since the May 1 ISM session.

3. THE PRIOR DAY’S REGIME (34 Macro Price, Strength & Momentum Rankings)

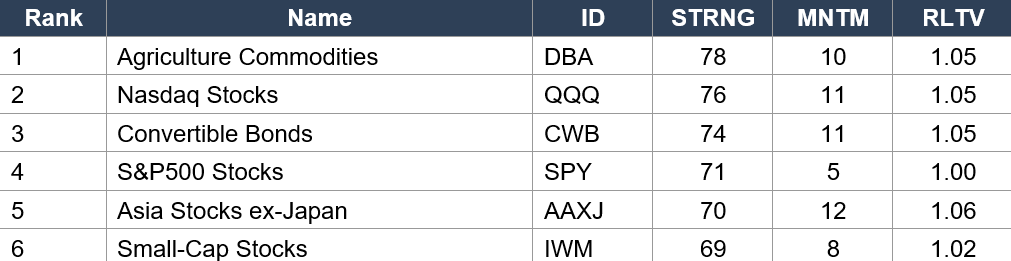

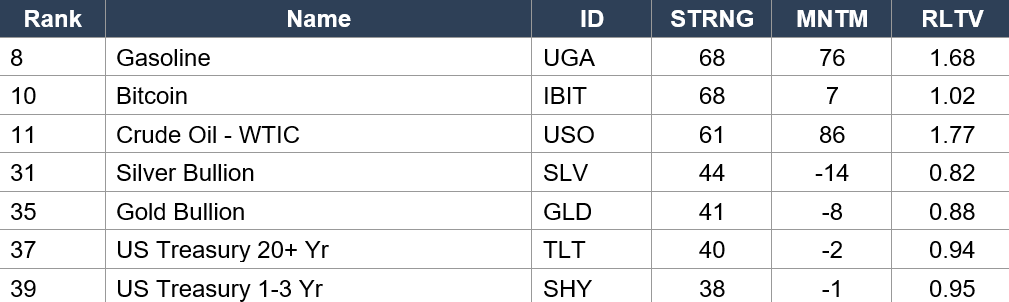

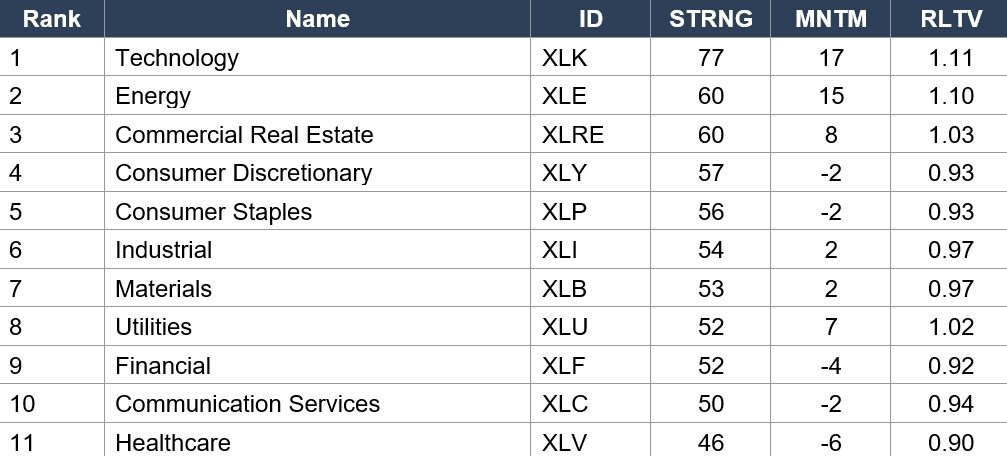

34 Macro Price, Strength & Momentum Rankings — Daily Close, Tuesday May 5. SPY Baseline: STRNG 71 | MNTM +5 | RLTV 1.00.

Asset Classes — Leaders

Asset Classes — Energy / Metals / Bonds

Regime signal: DBA (rank 1, STRNG 78 — NEW WAR HIGH for any asset class STRNG) holds #1 for a FIFTH consecutive data set. QQQ (rank 2, STRNG 76) rose from 74 — Nasdaq momentum re-accelerating. CWB (rank 3, RLTV 1.05) — credit risk-appetite confirmed. Bitcoin (IBIT rank 10, STRNG 68, MNTM +7, RLTV 1.02) is now ABOVE baseline RLTV for the first time since mid-April — the crypto recovery is structural. Crude Oil (USO rank 11, MNTM +86, RLTV 1.77) — today’s −7.43% crash will dramatically compress these readings in tomorrow’s data. The energy-momentum peak is being decisively broken. Gold (GLD rank 35, RLTV 0.88) — today’s +2.71% rally will improve this. The metals recovery is live in the tape but not yet in the data. Long bonds (TLT rank 37, RLTV 0.94; SHY rank 39, RLTV 0.95) remain the weakest asset classes — today’s yield plunge will provide relief but the structural bond weakness is the war’s lasting legacy.

Sector ETFs

Regime signal: Technology (XLK rank 1, STRNG 77, MNTM +17, RLTV 1.11 — NEW WAR HIGH for sector RLTV) holds #1 for a TENTH consecutive data set. RLTV at 1.11 means tech is outperforming the market by 11% — the widest relative outperformance of any sector in the war’s history. Today’s +2.21% XLK will extend this further. ENERGY (XLE rank 2, MNTM +15, RLTV 1.10 — ELEVENTH consecutive top-3-RLTV set). Energy has been the war’s most consistent relative-strength story. Today’s +0.10% XLE on −7.43% WTI is the MOST extreme positive decoupling of the war — energy equities are rallying (barely) as crude crashes 7.4%. Health-Care (XLV rank 11, RLTV 0.90 — structural laggard for the 12th consecutive set). The XLK/XLV RLTV spread (1.11 vs 0.90 = 21 pp) is the widest sector-relative-strength spread of the entire war.

Industry ETFs — Top 5 + Notable

Regime signal: Semiconductor (SMH rank 1, STRNG 78, MNTM +31, RLTV 1.25 — HIGHEST industry RLTV of the war) holds #1 for the EIGHTH consecutive data set since reclaiming from XES. The semis dominance continues despite NVDA −1.00% today — the broadening trade (AMD, AVGO, MU, AMAT) is sustaining the leadership even as NVDA consolidates. SOFTWARE RECOVERY CONTINUING: IGV (rank 19, MNTM +3, RLTV 0.98) improved from 0.96 and is now essentially at baseline — the recovery from the 0.84 trough is almost complete. Oil Refiners (CRAK rank 3, RLTV 1.16) — the refinery complex benefits from BOTH high crude and the crack spread; today’s crude crash may compress this. Medical Device (IHI rank 51, STRNG 31, RLTV 0.80 — NEW ALL-TIME WAR LOW for any industry RLTV) continues its structural deterioration. Gold Miners (GDX rank 50, MNTM −13, RLTV 0.83) — today’s gold +2.71% rally will provide relief.

4. MORNING DATA REACTION

8:15 AM — ADP NON-FARM EMPLOYMENT CHANGE APRIL (Consensus 118K, Prior 62K). The NFP Pre-Read.

ADP private payrolls at 8:15 AM is the session’s domestic data event. Consensus at 118K implies a near-doubling from March’s 62K — if realized, it would signal the labor market stabilized in April despite $100+ oil and ISM Employment contraction (manufacturing 46.4, services 48.0). If ADP prints below 100K, the NFP downside risk for Friday intensifies and the 65K consensus may be revised lower. If ADP surprises above 130K, the labor market resilience thesis is confirmed and the oil-relief + strong employment combination would be the most constructive macro package since the UNH/Retail Sales day. ADP has been an inconsistent predictor of NFP this cycle, but the directional signal matters.

Overnight — WTI CRASHED −7.43% TO $94.67. Below $100 For The First Time In Eight Sessions. The Oil-Inflation-Rates Chain Is Breaking.

The WTI crash is the most significant commodity event since the Day 29 ceasefire announcement. The break below $100 removes the acute price-level pressure that drove: ISM Prices Paid to 84.6, the FOMC 8-4 fracture, Powell’s ‘oil hasn’t peaked’ language, MOVE to 77.86, and the 30Y above 5.00%. At $94.67, WTI is still +41.3% from the pre-war $67.02 — a massive sustained premium — but the DIRECTION of the oil move matters as much as the level. WTI falling from $108 to $95 in under a week tells the market: the oil-shock peak has passed. The implications for Friday’s FOMC-sensitive data: (1) Inflation expectations should ease on lower pump prices; (2) Consumer spending resilience improves (lower fuel costs free income for discretionary spending); (3) Manufacturing input costs ease (though with a lag). If WTI holds in the $92-96 range through NFP Friday, the inflation narrative softens materially into the Warsh transition (May 15).

Tuesday — ISM Services Employment Improved To 48.0 (From 45.2). JOLTS Unchanged At 6.9M. The Labor Market Is Bending But Not Breaking.

ISM Services Employment improved 2.8 points from 45.2 to 48.0 — still in contraction (below 50) but the direction of improvement is constructive. Combined with manufacturing employment crashing to 46.4, the services improvement suggests the labor softening is concentrated in manufacturing (oil/tariff-exposed) rather than services (consumer-facing). JOLTS at 6.9M was unchanged — labor demand is not collapsing. The quits rate and hires data will matter for Friday’s NFP interpretation. The ISM/JOLTS combination is ‘stabilizing at a lower level’ — consistent with NFP around 60-80K rather than the sub-40K stagflationary scenario.

5. THE DYRH READ

Regime: Bull Flattener — Risk-On — Oil Relief Rally. WTI crashed below $100. Yields plunging across the curve. 30Y pulled below 5.00% crisis threshold. MOVE compressing to 76.78 but still above baseline (73.21). All 12 factors green — the broadest risk-on since May 1. All but one sector green. Gold surging +2.71%. Metals recovering. Russell +1.36% outperforming. ADP at 8:15 AM. NFP Friday. Confidence: HIGH — the oil relief is the most constructive single-session catalyst since the ceasefire extension.

Yield Curve: Bull Flattener — All Yields Plunging. 10Y −7.2 bps, 30Y −5.3 bps, 2Y −7.0 bps, 5Y −8.2 bps. The Most Aggressive Bull Flattener Since Day 37.

The yield decline is the market’s response to oil falling below $100: the inflation-expectations channel is compressing, allowing the front end to add back rate-cut probability (2Y −7.0 bps to 3.876%) and the long end to release term premium (30Y −5.3 bps to 4.938%). The 30Y at 4.938% is now 6.2 bps BELOW the 5.00% crisis threshold — the crisis-level breach from Monday has been fully reversed in two sessions. The 5Y at 4.001% (−8.2 bps) fell back below 4.10% — the mid-curve inflation-concern that crossed 4% on Monday has been walked back.

MOVE 76.78 (−1.40%) — Compressing But Still 3.57 Points Above Baseline. The Oil Relief Has NOT Fully Resolved The Rates Stress.

MOVE at 76.7767 is compressing from the 77.86 peak but remains substantially above the 73.21 pre-war baseline. The bond market is easing — but has NOT returned to sub-baseline comfort. The oil relief is necessary but not sufficient to reverse the MOVE expansion: the FOMC fracture (8-4), the Warsh transition governance uncertainty, and the ISM Prices Paid at 84.6 are structural catalysts independent of the oil level. If MOVE compresses below 73.21 on the oil relief + a constructive ADP + NFP above 65K, the capitulation thesis from Day 35 is restored. If MOVE holds above 73.21 despite oil below $100, the rates-stress regime has shifted structurally — meaning the FOMC fracture, not oil, is the primary driver.

ES 7,342.25 (+0.75%) — +6.7% Above Pre-War Baseline. NEW WAR-TO-DATE HIGH PREMIUM.

ES at 7,342.25 is now +460.63 / +6.7% above the pre-war 6,881.62 baseline — the HIGHEST war-to-date equity premium at any session open. The +6.7% is being achieved on: WTI crashing below $100 (oil relief), yields plunging (rate-cut probability adding back), gold surging (forced liquidation reversed), and all 12 factors green (broadest risk-on in weeks). Russell at +1.36% outperforming is the healthiest market structure signal — small-cap leadership on the oil-relief trade confirms genuine risk appetite rather than Mag 7 positioning.

Gold $4,692.20 (+2.71%) — The Forced Liquidation Is OVER. Haven Demand + Dollar Weakness + Yield Decline All Bullish For Gold. If Gold Sustains This Rally, The Safe-Haven Unwind From The Past Three Weeks Reverses.

6. THE GAME PLAN

Today: ADP 8:15 AM (118K consensus, 62K prior). Ivey PMI 10 AM. BOC Macklem 4:15 PM. FRIDAY: NFP 8:30 AM (65K consensus, 178K prior) + Avg Hourly Earnings (0.3%) + Unemployment Rate (4.3%). WARSH TAKES THE CHAIR MAY 15 — 9 DAYS AWAY.

The Bull Case:

WTI below $100 — the oil-inflation-rates chain is breaking. Yields plunging — 10Y −7.2 bps, 30Y below 5.00%. All 12 factors green. 10/11 sectors green. ES +6.7% above pre-war — new war high premium. Russell +1.36% outperforming. Gold +2.71%, Silver +5.13% — metals surging, forced liquidation reversed. BTC $82,690 (+0.91%). DAX +2.16%, Nikkei +2.15% — global risk-on. 34 Macro shows QQQ STRNG 76, XLK RLTV 1.11 (war-high sector RLTV), SMH RLTV 1.25 (war-high industry RLTV), IGV recovering to 0.98. IBIT RLTV 1.02 — crypto above baseline. ISM Services Employment improved. JOLTS stable at 6.9M. If ADP confirms labor stabilization (118K+) and NFP prints 65K+ Friday, the war’s labor market thesis holds, the oil relief eases inflation, MOVE compresses back below baseline, and the post-ceasefire rally extends into the Warsh era with S&P at new war highs.

The Bear Case:

MOVE at 76.78 still 3.57 points above baseline — the rates stress has NOT fully resolved. The FOMC fracture (8-4, three members wanting to remove easing bias) is structural and independent of oil. Warsh inherits a committee that cannot cut. WTI at $94.67 is still +41.3% from pre-war — the war premium is massive even below $100. ISM Prices Paid at 84.6 (the highest since 2022) reflects input costs with a LAG — even if oil falls, the elevated prices work through the manufacturing chain for months. ISM Manufacturing Employment at 46.4 and Services at 48.0 — both in contraction. NFP consensus at 65K would be the weakest since January 2020. ADP prior of 62K was terrible — if ADP confirms weakness, the labor market thesis breaks before NFP. NVDA −1.00%, META −0.89%, MSFT −0.54%, TSLA −0.80% — 4/7 Mag 7 red. ES at +6.7% above pre-war with 76.78 MOVE and 4.35% 10Y is the most stretched equity-rates divergence of the war — any catalyst that reverses the oil relief (Hormuz escalation, shadow-fleet interdiction, Iran provocation) would produce outsized downside.

Regime: Bull Flattener — Risk-On — Oil Relief Rally. The oil shock is breaking and the market is pricing the endgame: WTI below $100, yields plunging, metals surging, all factors green, global risk-on. But MOVE remains above baseline — the rates stress has not fully cleared. ADP at 8:15 AM is the immediate test. NFP Friday is the definitive resolution. Warsh takes the chair in 9 days. If oil holds below $100 + labor holds above 65K NFP: the war’s final chapter is bullish. If either reverses: the endgame gets rewritten. Sixty-nine days. The market has chosen its side — risk-on, oil relief, endgame pricing. Now the data has to confirm it.

Watch List

ADP 8:15 AM — The NFP Pre-Read

Consensus 118K vs prior 62K. If ADP near or above 118K: labor market stabilized in April, NFP expectations may be revised higher, the oil-relief + employment-stabilization package is the most bullish combination since mid-April. If ADP misses below 80K: NFP downside risk intensifies, the ISM employment contraction is translating to payrolls, and Friday becomes a high-stakes binary.

MOVE 73.21 — Will The Oil Relief Compress It Back Below Baseline?

MOVE at 76.78 is compressing but 3.57 points above baseline. If the bull flattener extends and MOVE drops below 75 today, the path to sub-baseline by Friday is open. If MOVE holds above 76 despite oil below $100, the FOMC fracture — not oil — is the primary rates-stress driver, and sub-baseline may not return until the Warsh transition resolves.

WTI Sub-$100 Sustainability

The break below $100 is the most bullish commodity signal since the ceasefire. If WTI holds $92-96 through Friday: the inflation narrative softens, consumer purchasing power improves, the Fed’s ‘look through’ framework is validated retroactively. If WTI bounces back above $100 on any Hormuz catalyst: the oil relief was a head-fake and the rates stress returns.

NFP Friday 65K — The Labor Market Resolution (Two Days Away)

ADP today is the setup. NFP Friday is the resolution. Consensus 65K vs 178K prior — the largest expected deceleration since the pandemic. ISM Manufacturing Employment 46.4 (crash). ISM Services Employment 48.0 (improved but contractionary). JOLTS 6.9M (stable). The leading indicators point to a weak but not catastrophic print — 50-80K range most likely. Below 40K would be a shock. Above 100K would be a massive upside surprise.

Morning check: Day 69. The war is sixty-nine days old. The oil shock is breaking. WTI crashed −7.43% to $94.67 — below $100 for the first time in eight sessions. Brent −6.42%. Yields are plunging: 10Y −7.2 bps, 30Y pulled below 5.00%. Gold is surging +2.71%, Silver +5.13% — the forced liquidation is over. All 12 factors green. 10/11 sectors green. Russell +1.36% outperforming. DAX +2.16%, Nikkei +2.15%. ES at +6.7% above pre-war — new war high premium. BTC $82,690. MOVE compressing to 76.78 but still above baseline. The 34 Macro data shows XLK RLTV 1.11 (war-high), SMH RLTV 1.25 (war-high), DBA STRNG 78 (war-high), IGV recovering to 0.98, IHI at 0.80 (war-low). The market has chosen its side: oil relief, rates easing, risk-on. ADP at 8:15 AM is the first test. NFP Friday is the resolution. Warsh takes the chair in 9 days. The war’s endgame is being priced. Pressure, not panic. Regime, not reaction.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.