☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: The war hit the gas fields. Israel struck Iran’s SOUTH PARS GAS FIELD — the world’s largest natural gas reserve, shared with Qatar — the first attack on upstream energy infrastructure since the war began. Trump distanced the US, claiming Israel acted alone. Iran responded by publishing a TARGET LIST of specific energy facilities it plans to strike: Saudi Aramco’s Samref refinery, Jubail petrochemical complex, and UAE’s Al Hosn gas field. Qatar confirmed “extensive damage” to Ras Laffan, the world’s largest LNG export facility (~20% of global LNG supply). Brent surged to $113.14 (+5.36%) — a new ALL-TIME WAR HIGH, +55.3% from pre-war. PRECIOUS METALS MASSACRE: Gold crashed −$342 (−6.98%) to $4,554 — the largest single-session drop since the January 30 crash. Silver collapsed −13.05%. Platinum −8.88%. Palladium −7.85%. Copper −4.49%. This is NOT rate repricing — this is FORCED LIQUIDATION across the entire metals complex. Leveraged funds are being margin-called and dumping liquid assets to raise cash. The 2Y yield at 3.892% has breached the UPPER BOUND of the fed funds target (3.75%) — the market is pricing the next move as a rate HIKE. Jobless Claims fell to 205K (below 215K expected) — the labor market remains tight, giving the Fed ZERO cover to cut. International markets in CRISIS: DAX −3.09%, Nikkei −2.71%, EuroStoxx −2.68%. ECB, BoE, SNB all decide today into the most unstable market since the pandemic. ES at 6,638 (−0.58%) approaching the 200-day MA (∼6,600–6,630) — the last major support. Micron’s historic beat ($12.20 EPS vs. $9.31, $33.5B Q3 guide) was COMPLETELY IGNORED by markets — SOXX −1.85% pre-market. When a 30%+ earnings beat can’t lift the sector, macro is fully dominating micro.

The Number That Matters: Gold at $4,554 (−6.98%). This is the most extreme forced-liquidation signal of the entire war series. Gold has now lost $757 (−14.3%) from pre-war during an active shooting war with energy infrastructure being attacked. The gold/equity loss ratio (7:0.6 = 11.7x) is the highest of the series, confirming the liquidation pressure is concentrated in precious metals. When gold drops 7% during a war, the mechanism is margin calls forcing the sale of liquid positions to cover losses in less liquid ones. Silver’s −13% collapse confirms the entire metals complex is in forced-liquidation mode. The $5,000 floor that held for two sessions has been obliterated.

The Setup: The regime is a Stagflationary Forced Liquidation Crisis — escalating from yesterday’s Hawkish Stagflation Shock. Every crisis signal is flashing: gold −7%, silver −13%, bonds selling with 2Y above fed funds, equities at war lows, VIX above 25 and rising toward 27, breadth in extreme washout, correlation spiking to 35.78, energy at all-time war highs, grains surging on food inflation, Micron’s historic beat ignored. The ONLY assets going up are energy and grains. This is not rotation — this is CASH RAISING. Four central banks decide today into this chaos. The S&P’s 200-day MA (∼6,600–6,630) is the last major support. If it breaks, systematic trend-following selling triggers.

2. OVERNIGHT SESSION RECAP

Asia-Pacific

Nikkei −2.71%, TOPIX −1.25%. Japan devastated by the energy infrastructure escalation — South Pars/Qatar damage threatens Asian LNG supply chains directly. The 3-day recovery from Days 13–14 has been completely erased.

Europe

DAX −3.09% (two consecutive sessions of −2.5–3%), EuroStoxx −2.68%. Europe in CRISIS mode ahead of ECB/BoE decisions. Qatar’s Ras Laffan “extensive damage” directly threatens European gas supply (~15% of Europe’s LNG). Natural gas +3.65% on South Pars attack. If Lagarde signals concern about energy pass-through to core inflation, European markets sell off further.

US Pre-Market

Day 19 — Energy Infrastructure Warfare Begins. Israel struck South Pars gas field — the world’s largest natural gas reserve shared with Qatar. Trump distanced the US, said Israel acted alone and won’t repeat. Iran published a retaliatory TARGET LIST: Saudi Aramco Samref refinery, Jubail petrochemical complex, UAE’s Al Hosn gas field. Qatar confirmed “extensive damage” to Ras Laffan (largest LNG export facility, ~20% of global LNG). US dropped 5,000-lb GBU-72 bunker busters on Hormuz missile sites. Gulf states intercepting drones/missiles. EU rejected Trump’s Hormuz naval coalition call. US eased Venezuela sanctions to boost oil supply. Death toll 2,200+. Gas $3.79/gallon.

FOMC yesterday (March 18): Hold at 3.50–3.75% (11-1, Miran dissented favoring 25bp cut). Dot plot median UNCHANGED at 3.4% end-of-year (one cut), but 4–5 members shifted from two cuts to one. Powell: “not as much progress on inflation as we had hoped.” GDP forecast RAISED to 2.4% (from 2.3%). PCE inflation forecast RAISED to 2.7% headline and core (from 2.4%/2.5%). Powell said uncertainty is “elevated” and if he could have skipped the SEP, “this would be a good one.” S&P fell to session lows on Powell’s inflation comments (−1.36%). Statement added new language: implications of Middle East conflict “are uncertain.” 7 members now see no cuts in 2026 (up from 6 in December).

Micron (MU) reported after the close: EPS $12.20 vs. $9.31 est (+31% beat). Revenue $23.86B vs. $20.07B. Q3 guidance: $33.5B revenue / $19.15 EPS. Entire 2026 HBM supply sold out. A HISTORIC beat — but SOXX −1.85% pre-market. The macro is fully dominating micro. When a 30%+ earnings beat and 200%+ forward revenue guidance can’t lift the sector, the market has decided that inflation/war risk outweighs AI growth.

Today: Jobless Claims released 8:30 AM — 205K (fell 8K, below 215K expected). Labor market remains tight, giving Fed zero cover to cut. ECB decision (expected hold at 2.0%, Lagarde presser). BoE decision (expected hold at 3.75%). SNB, Riksbank, BoJ decisions. Markets pricing >2 ECB hikes and ~40bp BoE tightening in 2026. Friday: Michigan Sentiment.

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 03/18/26. Provided for informational purposes only; not as investment advice.

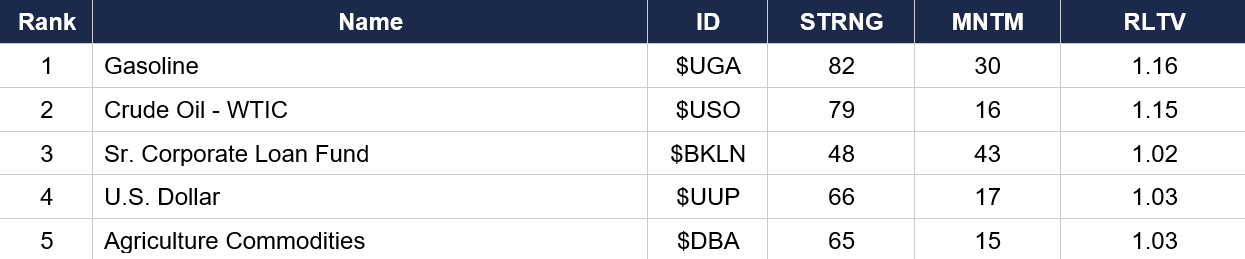

Asset Classes — Top 5

Asset Classes — Bottom 5

Regime signal: Senior Corporate Loans ($BKLN rank 3, MNTM 43) is now the HIGHEST momentum asset of the entire series for any non-energy asset — floating-rate credit is the ultimate shelter in a rising-rate, rising-oil environment. Crypto has dropped out of the top 5 (ETHA rank 6, IBIT rank 7). VIX ($VXX rank 9, MNTM −1) has stabilized near neutral. Gold ($GLD rank 23, MNTM −22) has COLLAPSED in the rankings from rank 20 yesterday — the forced-liquidation rout. Silver ($SLV rank 16, MNTM −13) and Platinum ($PPLT rank 13, MNTM −9) confirm the metals complex destruction. Nasdaq ($QQQ rank 11, MNTM −1) has turned negative for the first time in the recovery. S&P ($SPY rank 19, MNTM −12) deeply negative. Municipal Bonds ($MUB, MNTM −40) and EM Bonds ($EMB, MNTM −35) remain the worst. High Yield ($HYG rank 14, MNTM −3) is deteriorating rapidly — credit stress emerging.

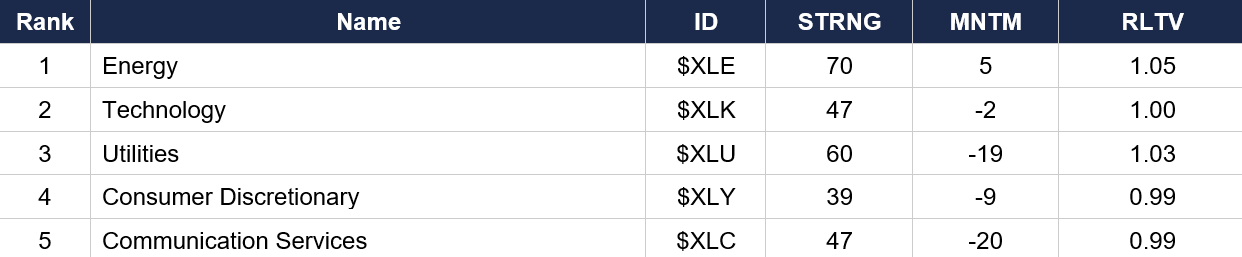

Sector ETFs — Top 5

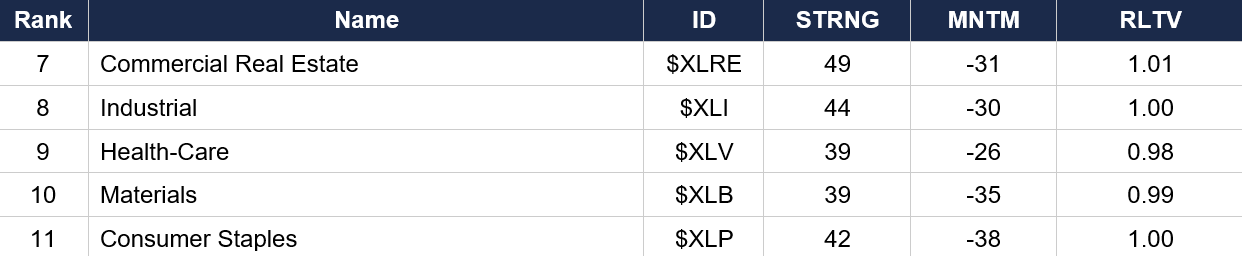

Sector ETFs — Bottom 5

Regime signal: Technology ($XLK rank 2, MNTM −2) has turned NEGATIVE momentum for the first time since the recovery — the GTC/Micron catalyst has been fully overwhelmed by macro. Energy ($XLE rank 1, MNTM 5) is the ONLY sector with positive momentum. Consumer Staples ($XLP rank 11, MNTM −38) is now the WORST sector — even the defensive trade isn’t working. Materials ($XLB rank 10, MNTM −35) crushed by the metals liquidation. Industrial ($XLI rank 8, MNTM −30) and Commercial Real Estate ($XLRE rank 7, MNTM −31) confirm the rate-sensitive destruction from the 30Y approaching 5%.

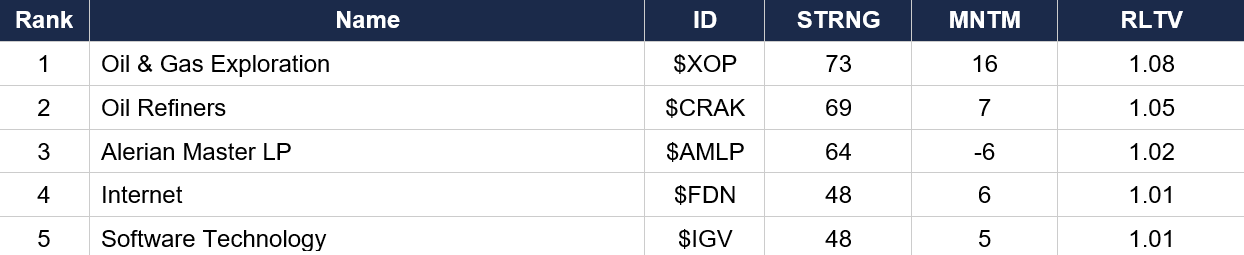

Industry ETFs — Top 5

Industry ETFs — Bottom 5

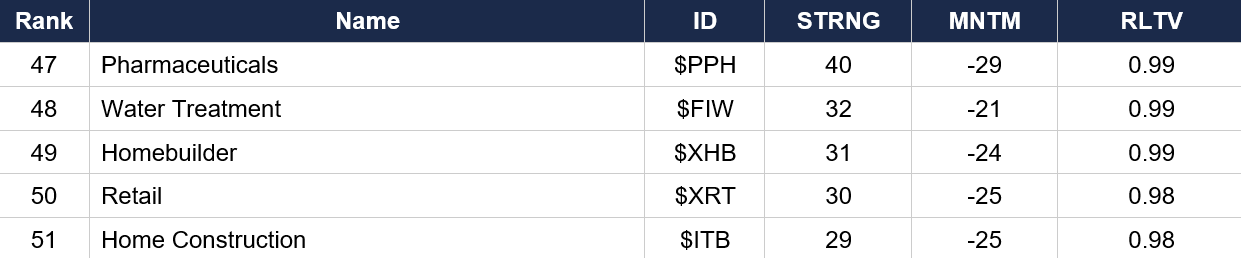

Regime signal: Oil & Gas ($XOP rank 1, MNTM 16) is ACCELERATING — highest momentum since the mid-war peak. Internet ($FDN rank 4, MNTM 6) and Software ($IGV rank 5, MNTM 5) are the ONLY non-energy industries with positive momentum. Semiconductor ($SMH rank 17, MNTM −7) has been crushed despite Micron’s historic beat — confirming macro dominance over micro. Aerospace-Defense ($ITA rank 32, MNTM −22) continues plummeting. Gold Miners ($GDX rank 45, MNTM −29) in freefall alongside the gold crash. Home Construction ($ITB rank 51, MNTM −25) and Homebuilder ($XHB rank 49, MNTM −24) at the bottom as 30Y approaches 5%.

4. MORNING DATA REACTION

Jobless Claims (released 8:30 AM): 205,000 (fell 8K, below 215K expected). Continuing Claims 1.857M (+10K). The labor market remains TIGHT — new seasonal factors introduced. This covers the survey period for March nonfarm payrolls. This is the WORST data for rate-cut hopes: a tight labor market gives the Fed zero cover to cut into rising inflation. The stagflation trap is asymmetric — growth isn’t slowing fast enough in the labor market to justify easing even as GDP decelerates and manufacturing contracts.

FOMC recap (yesterday, March 18): Hold 11-1 (Miran dissented, favoring 25bp cut). Dot plot median unchanged at 3.4% (one cut for 2026). But 4–5 members moved from two cuts to one — “a meaningful amount of movement toward fewer cuts,” per Powell. GDP forecast raised to 2.4%. PCE inflation raised to 2.7% (headline and core). Powell: “not as much progress on inflation as we had hoped” and “bar is higher for cuts.” The statement added that implications of the Middle East conflict “are uncertain.” Stocks fell to session lows. The market verdict: one cut is the ceiling, zero is the base case, and the 2Y at 3.892% is now pricing hike risk.

PPI recap (yesterday 8:30 AM): +0.7% MoM, +3.4% YoY (hottest since Feb 2025). Goods +1.1% (war/oil pass-through). Core ex food/energy/trade +0.3% (9th consecutive). The first hard data confirming inflationary pass-through from the Hormuz closure. Combined with CPI +0.3%/2.4% and Core PCE 3.1%, the inflation side is ACCELERATING while growth decelerates — the stagflation diagnosis is now confirmed across every major inflation gauge.

Today: ECB rate decision (expected hold at 2.0%), Lagarde press conference. BoE (expected hold at 3.75%). SNB, Riksbank, BoJ decisions. Markets pricing >2 ECB hikes and ~40bp BoE tightening for 2026. SIX central bank decisions in 48 hours. If Lagarde signals concern about energy pass-through to core inflation, European markets sell off further. Qatar damage to Ras Laffan threatens European LNG supply directly. Friday: Michigan Sentiment.

5. THE DYRH READ

Regime: Stagflationary Forced Liquidation Crisis — Energy Infrastructure Warfare Begins. Every crisis signal is flashing simultaneously. Confidence: Very High on characterization.

Yield Curve: Bear Steepener — 2Y Above Fed Funds, Long End Accelerating. The 2Y at 3.892% is 14.2 bps ABOVE the fed funds upper bound (3.75%). This means the market is pricing the next move as a rate HIKE, not a cut — a complete reversal from pre-war expectations of two cuts. The long end is CATCHING UP: 30Y bond futures −0.36% (most aggressive of the maturity stack), ZN (10Y) −0.42%. The 30Y at 4.892% is within 11 bps of 5.00% — a level that would trigger a major repricing of mortgage rates, corporate borrowing, and equity risk premiums. MOVE at 81.25 will likely rise as bond selling accelerates. The bond crisis that was “definitively over” 48 hours ago is re-emerging — not as a liquidity crisis but as a structural repricing of the inflation regime. Cumulative: 10Y +35.5 bps from pre-war (new series high).

Metals Massacre: Gold −7%, Silver −13% = Forced Liquidation. Gold −$342 to $4,554 — largest single-session drop since the Jan 30 crash. Cumulative: −$757 (−14.3%) from pre-war during an active war with energy infrastructure being attacked. Silver −13.05%. Platinum −8.88%. Palladium −7.85%. Copper −4.49%. This is NOT rate repricing (yesterday’s mechanism) — this is FORCED LIQUIDATION. The gold/equity loss ratio (7:0.6 = 11.7x) is the highest of the series. Leveraged funds facing higher borrowing costs are dumping their most liquid assets (precious metals) to cover margin calls in less liquid positions. The $5,000 floor that held for two sessions has been obliterated.

Energy Infrastructure Escalation: Brent $113+, Natural Gas Surging. Brent +5.36% to $113.14 — new ALL-TIME war high, +55.3% from pre-war. Natural Gas +3.65% on South Pars/Qatar supply fear. The Brent-WTI spread has blown out to $17.26 — extraordinary international premium reflecting the direct threat to global energy infrastructure. The conflict has crossed from “military targets” to “economic warfare” — attacking upstream production capacity, not just shipping lanes. Iran’s published target list of Saudi, UAE, and Qatari facilities means the escalation ladder has no obvious ceiling. US eased Venezuela sanctions to boost supply.

Equities: 200-Day MA Under Siege, Micron Beat Ignored. ES at 6,638 (−0.58%) approaching the 200-day MA (~6,600–6,630). International: DAX −3.09% (two consecutive −3% sessions), Nikkei −2.71%, EuroStoxx −2.68%. Russell −1.04% (underperforming S&P for first time in days — risk-on unwind). Micron’s historic beat ($12.20 EPS vs. $9.31, $33.5B Q3 guide) completely ignored: SOXX −1.85% pre-market. When a 30%+ beat can’t lift the sector, macro is fully dominating micro. AAPL (+0.10%) the only green Mag 7 name (safe-haven rotation within tech). All 11 sectors were red yesterday. S5FD collapsed from 66.60 to 31.41 (−52.84%) in a single session.

FX: Regime Shift to Flight-to-Safety. Yesterday: dollar up, all currencies down = hawkish repricing. TODAY: dollar DOWN (−0.17%), JPY UP (+0.46%) = genuine PANIC/safe-haven flows. When the dollar weakens during a selloff, international investors are REPATRIATING capital rather than seeking US Treasuries. Implication: Treasuries are no longer a safe haven because bonds are selling off too. The only working haven is JPY. DXY at 99.885 retreating from 100. BTC −2.05% below $70,000.

Volatility & Breadth: Approaching Day 12 Crisis Levels. VIX at 26.75 (+6.62%) — above 25 crisis threshold, rising toward 27 (3.25 points from the 30 panic threshold). VVIX +14.43%. VXN +12.41%. S5FD collapsed from 66.60 to 31.41 (−53%) in one session — will push below 30 today (extreme washout rebound zone). R2FD at 28.54 already below 30. S5TW at 17.49 — catastrophic. S5TH at 47.11 — below the 50 bull/bear line again. COR1M spiked to 35.78 — approaching the Day 12 high of 37.21. SKEW at 136.54 continues falling as tail-risk hedges are cashed in. The 3-day recovery from Days 13–15 has been completely erased in 24 hours.

6. THE GAME PLAN

Today’s Key Events: Jobless Claims released 8:30 AM (205K, below est.). ECB rate decision + Lagarde presser. BoE rate decision. SNB, Riksbank, BoJ decisions. SIX central bank decisions in 48 hours. Friday: Michigan Sentiment. Ongoing: Iran energy infrastructure escalation; Hormuz status.

The Bull Case: S5FD at 31 and R2FD at 28.54 are in the extreme washout rebound zone — historically precedes violent mechanical rebounds. The gold selloff could exhaust as leveraged longs are flushed, creating a violent rebound. ECB/BoE could surprise dovish, emphasizing growth risks over inflation. Trump distanced the US from the South Pars strike, said Israel won’t repeat it — potential de-escalation. Iran’s target list may be posturing. The equity-oil decoupling (ES only −0.58% with Brent +5.36%) shows equities are NOT fully capitulating. Central bank coordination (emergency liquidity, reserve releases) could stabilize. VIX at 26.75 is crisis but NOT yet panic (below 30). The 200-day MA may hold as support.

The Bear Case: EVERY crisis signal flashing simultaneously. Gold −7%, silver −13%, bonds selling with 2Y above fed funds, equities at war lows, VIX above 25 and rising, breadth in extreme washout, Micron beat ignored, international markets down 2–3%, energy at all-time war highs. Energy infrastructure warfare has NO obvious ceiling — Iran’s target list names specific Saudi/UAE/Qatari facilities. Ras Laffan damage threatens ~20% of global LNG. 30Y at 4.892% — 11 bps from 5.00%. The 3-day recovery has been erased in 24 hours. Forced liquidation cascading across the metals complex. Labor market tight (claims 205K) = Fed has zero cover to cut. If gold continues lower, margin calls cascade further. If S&P breaks the 200-day MA, systematic selling triggers. VIX approaching 30 panic threshold.

Regime: Stagflationary Forced Liquidation Crisis. The war crossed from military targets to economic warfare. Gold’s 7% crash confirms forced liquidation at its most extreme. The 2Y above fed funds means the market is pricing hike risk. Brent at $113, new war high. The only assets working are energy, grains, and cash. Four central banks decide today into the worst market instability since the pandemic. The 200-day MA on the S&P is the last line of defense.

Watch List

Gold −7% — forced liquidation or exhaustion? — If gold stabilizes today, the liquidation wave may exhaust. If it continues lower, margin calls cascade and could trigger systemic risk events (fund blowups, prime broker stress). The $4,500 level is the next major support.

S&P 200-day MA (~6,600–6,630) — ES at 6,638. A sustained break below triggers systematic trend-following selling. This is the most significant technical level of the entire war — correction becomes structural bear market.

ECB/BoE today — global monetary policy response — If Lagarde/Bailey signal hiking is on the table, global financial conditions tighten further. If they emphasize growth risks and “wait-and-see,” temporary relief. Qatar’s Ras Laffan damage directly threatens European gas supply.

2Y at 3.892% — hike pricing — 14.2 bps above fed funds upper bound. Multiple sessions above 3.80% = market firmly pricing hike risk. Watch for Fed speakers to push back.

VIX at 26.75 — 3.25 points from panic — Currently in “crisis” territory (25–30 per the Master Template). A breach of 30 = panic regime. The speed of the VIX rise from 22.71 two days ago is alarming.

Morning check: the most dangerous cross-asset configuration since the war began. Gold’s 7% crash. Silver’s 13% collapse. Bonds selling with the 2Y above fed funds. Brent at $113. Energy infrastructure warfare with no ceiling. International markets down 2–3%. Micron’s historic beat completely ignored. The 3-day recovery erased in 24 hours. Four central banks decide today. The 200-day MA is the last line of defense. The only things working are energy, grains, and cash. Every other asset class is being liquidated. This is the session that determines whether the crisis peaks or cascades.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.