☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: The growth leg of the macro narrative has collapsed. February Non-Farm Payrolls: −92,000 vs. +60K expected. The US economy SHED 92,000 jobs — the first negative print since October 2025 and the largest miss relative to consensus in the DYRH series. January revised lower, compounding the shock. This prints into WTI at $85.88 (+6.01%) and Brent at $88.77 (+3.93%) — approaching $90 for the first time since 2024. The combination is textbook RECESSIONARY STAGFLATION: the economy is contracting while energy costs surge. Bonds have RALLIED for the FIRST TIME in the entire series — six straight sessions of selling reversed by the growth collapse. The curve has shifted from bear steepener to bull flattener. Rate cuts are back on the table. Gold bouncing +1.07%. All equities red but SURPRISINGLY RESILIENT: ES −0.76%, RTY −1.19%. The bond rally is partially cushioning the growth shock. XLE the only green sector (+1.50%). VIX at 25.40, above the 25 crisis threshold. S5FD at 29.62 — new series low, below the 30 extreme threshold. The Fed is trapped: oil at $86 means inflation stays elevated, but −92K payrolls means the economy needs cuts.

The Number That Matters: NFP −92,000. The Kaiser Permanente strike (31K healthcare workers) accounts for a portion, but even adjusting, the underlying number is deeply negative. January’s +130K — which helped drive Wednesday’s recovery narrative — has been revised down. The two-day ADP-to-NFP divergence is extreme: Wednesday’s ADP showed +63K private payrolls; today’s BLS shows −92K total including government. This is the data point that fundamentally changes the regime: from “can the economy absorb the oil shock?” to “the economy CANNOT absorb the oil shock.”

The Setup: The regime has evolved through five distinct phases this week. Day 1-2: Stagflation driven by oil while economy still growing. Day 3: Pro-cyclical recovery on strong data (ADP +63K, ISM Services 56.1). Day 4: Recovery broken by oil through $80. Day 5 (today): NFP −92K collapses the growth leg entirely. We have moved from STAGFLATION (strong economy + high inflation) to RECESSIONARY STAGFLATION (contracting economy + high inflation). The bond market confirmed it instantly: first rally in seven sessions. Bull flattener. Rate cuts repriced. Gold bouncing. This is the classic 1970s dilemma — the Fed cannot address both problems simultaneously.

2. OVERNIGHT SESSION RECAP

Asia-Pacific

TOPIX −1.49%. Nikkei (USD) +0.10% (pre-NFP positioning). Japan’s cumulative losses from the war are now severe — direct energy import dependence is devastating. Korea still processing Tuesday’s approximately −12% KOSPI crash.

Europe

DAX −0.47%, Euro Stoxx 50 −0.64%. Europe red ahead of NFP. The overnight oil surge to $86 WTI and $89 Brent is hitting European equities on energy import costs. The 15% tariff uncertainty remains an overhang.

US Pre-Market

February Non-Farm Payrolls: −92,000 vs. +60K expected vs. +130K prior (January also revised down). Released today, March 6, at 8:30 AM EST. The first negative payrolls print since October 2025. The Kaiser Permanente strike (31K healthcare workers) is a factor, but even adjusting, the number is deeply negative. This is the regime-defining data point of the entire DYRH series.

War Day 7: No de-escalation overnight. Israeli strikes continue on Tehran and Lebanon. Lebanese Health Ministry reports civilian casualties including children in past 48 hours. Iran struck Azerbaijan’s Nakhchivan Airport (geographic expansion). Oil surging on continued Hormuz disruption fears and tanker attacks. Reports of Iranian peace talk feelers remain unconfirmed.

Prior session (March 5 close): Dow −784 (−1.61%), S&P −0.56%, Nasdaq −0.26%. WTI $81.01 (+8.51%), Brent $85.41 (+4.93%) — oil broke through the critical $80 threshold. S5FD crashed to 29.62 (new series low). MOVE 74.53 (+6.42%) — back above pre-war level. COR1M 22.97 — above 20 threshold. All factors red. Gold −1.09%. Late-day partial recovery on Reuters headline about Treasury crude stabilization efforts.

Week’s economic data recap: PPI (released Friday February 27): Final demand +0.5% MoM, Core +0.3%. ISM Manufacturing (released Monday March 2): 52.4, Prices Paid 70.5 (highest since mid-2022). JOLTS (released Tuesday March 3). ADP (released Wednesday March 4): +63K (beat), January revised to 11K. ISM Services (released Wednesday March 4): 56.1 (highest since July 2022). Jobless Claims (released yesterday March 5): data reflected pre-war labor conditions. Today’s NFP is the capstone.

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 03/05/26. Provided for informational purposes only; not as investment advice.

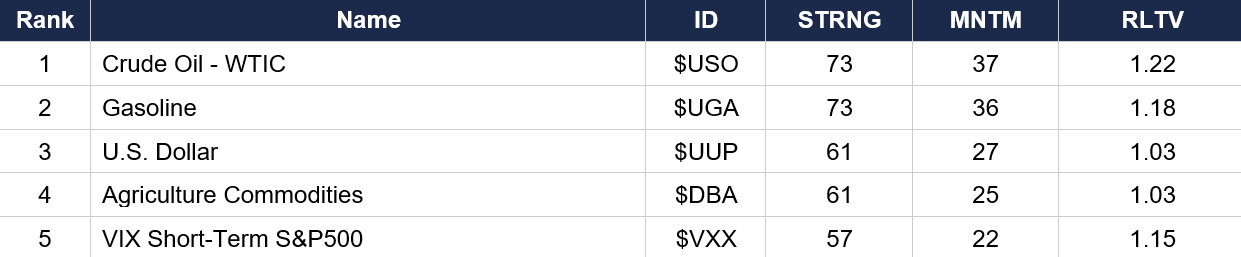

Asset Classes — Top 5

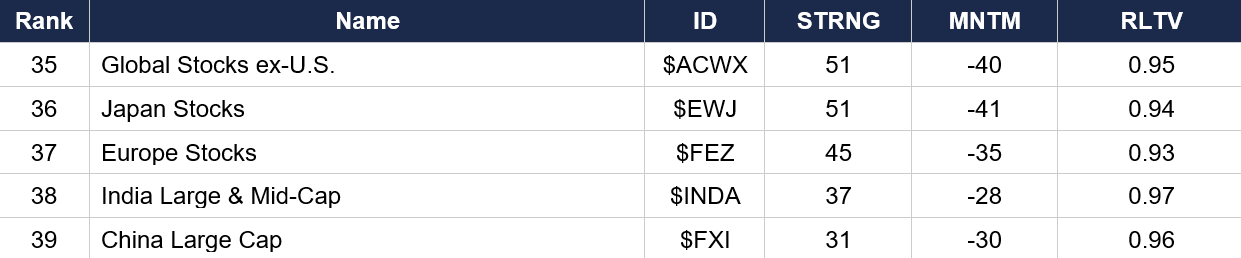

Asset Classes — Bottom 5

Regime signal: Crude oil has RECLAIMED the #1 rank from gasoline. The dollar’s MNTM at 27 remains extraordinary. Agriculture ($DBA) at rank 4 with MNTM 25 confirms the food-inflation impulse from war-driven supply disruption. VIX ($VXX) has re-entered the top 5 at rank 5 (MNTM 22) after yesterday’s +6.95% surge above 25. Bitcoin ($IBIT) has slipped to rank 6 (MNTM 19) — crypto cooling after Wednesday’s surge. Gold at rank 12 (MNTM −8) remains deeply negative — today’s +1.07% bounce may begin to reverse this. Nasdaq ($QQQ rank 10, MNTM 1) and S&P ($SPY rank 19, MNTM −11) are diverging — tech holding up better than the broad market. Japan ($EWJ, MNTM −41) is the worst momentum reading on the entire board. International equities have been devastated: Global ex-US (−40), Europe (−35), Asia ex-Japan (−38), EM (−38). Municipal bonds ($MUB, MNTM −30) remain extreme.

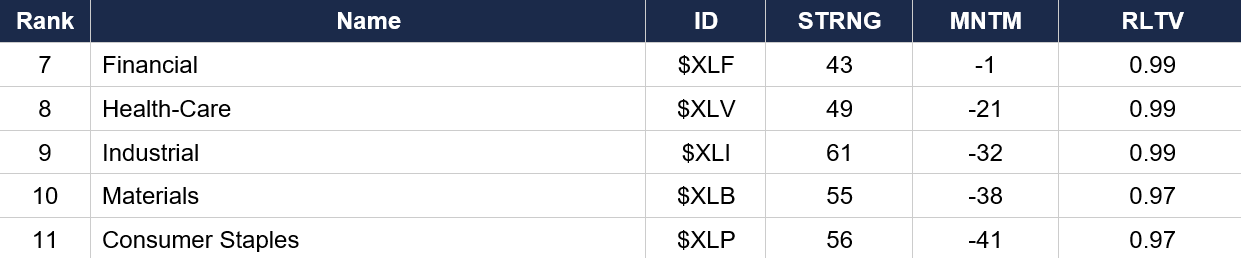

Sector ETFs — Top 5

Sector ETFs — Bottom 5

Regime signal: Communication Services ($XLC) holds rank 1 with MNTM 15. Energy ($XLE) at rank 2 but MNTM still negative (−5) — crude surges but energy equities lag (the “energy earnings vs. energy equity” divergence continues). Consumer Staples ($XLP, MNTM −41) is now the WORST sector momentum on the entire board — an extraordinary reading for a traditionally defensive sector. Materials ($XLB, MNTM −38) and Industrial ($XLI, MNTM −32) confirm the cyclical destruction. Technology ($XLK) at rank 5 with MNTM exactly 0 — tech is neither gaining nor losing momentum, acting as a relative haven.

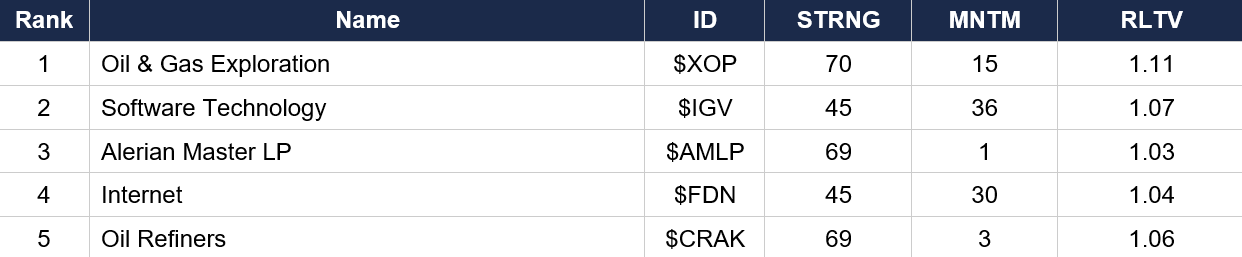

Industry ETFs — Top 5

Industry ETFs — Bottom 5

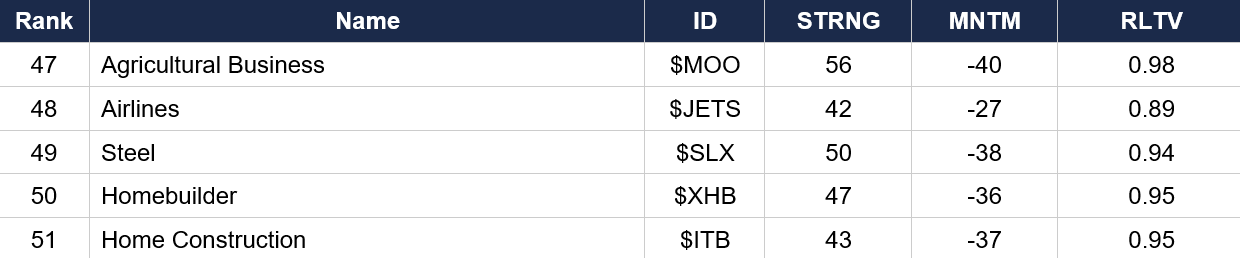

Regime signal: Software ($IGV, MNTM 36) and Internet ($FDN, MNTM 30) hold the highest momentum readings on the industry board — the tech/software complex is acting as a relative safe haven within equities. Oil & Gas Exploration ($XOP) at rank 1 confirms energy dominance. Cyber Security ($CIBR, MNTM 20) at rank 6 reflects the wartime cybersecurity premium. Airlines ($JETS, MNTM −27) continue to collapse on fuel costs. Steel ($SLX, MNTM −38) and Agricultural Business ($MOO, MNTM −40) are the worst industry momentum readings. Home Construction ($ITB, MNTM −37) and Homebuilders ($XHB, MNTM −36) remain devastated by rising rates and energy costs.

4. MORNING DATA REACTION

February Non-Farm Payrolls (released today, March 6 at 8:30 AM): −92,000 vs. +60K expected vs. +130K prior. January revised down. The Kaiser Permanente strike (31K healthcare workers) accounts for a portion, but even adjusting, the underlying number is deeply negative. This is the first negative payrolls print since October 2025.

The NFP print fundamentally changes the macro narrative. Wednesday’s ADP showed +63K private payrolls — the ADP-to-NFP divergence is extreme. The strong ADP and ISM Services (56.1) data from Wednesday that fueled the one-day pro-cyclical recovery have been obliterated by today’s number. The economy was NOT strong enough to absorb the oil shock.

The week’s inflation data for context: ISM Manufacturing Prices Paid at 70.5 (released Monday March 2, highest since mid-2022). PPI Final Demand +0.5% MoM (released Friday February 27). ISM Services Prices declined to 63.0 from 66.6 (released Wednesday March 4). The inflation pipeline was already hot BEFORE the oil shock. Now oil at $86 layers another massive inflation impulse on top of an economy that is shedding jobs.

The Fed’s dilemma: oil at $86 means CPI will accelerate in coming months (energy pass-through), making rate cuts difficult to justify on an inflation basis. But −92K payrolls means the labor market is deteriorating rapidly, creating pressure for rate cuts to support growth. The Fed cannot address both problems simultaneously. This is the classic 1970s stagflation trap.

5. THE DYRH READ

Regime: Recessionary Stagflation — Economy Contracting (NFP −92K) While Energy Costs Surge (WTI $86). The worst-case macro scenario has materialized. Confidence: Very High on characterization.

Yield Curve: Bull Flattener — Complete Regime Reversal. Bonds have RALLIED for the FIRST TIME in the entire DYRH series. After six straight sessions of bear steepening, the curve has completely reversed to a bull flattener on the −92K NFP. All yields falling: 2Y −2.9 bps to 3.554% (leading the decline as rate cuts get repriced), 5Y −2.3 bps, 10Y −2.3 bps to 4.117%, 30Y −1.8 bps. The bond market’s message is unambiguous: the oil shock will damage growth MORE than it will sustain inflation. Growth fear has eclipsed inflation fear. ZB +0.24%, ZN +0.19% — the first green Treasury session in seven. Watch MOVE at the open: if it stays near 74.5 or declines, the flight to safety is orderly. If MOVE spikes above 78, it’s panic bond buying.

Commodity Complex — Oil Approaching $90, Gold Finally Bouncing. WTI +6.01% to $85.88. Brent +3.93% to $88.77. CUMULATIVE: WTI from $67.02 → $85.88 (+$18.86, +28.1%), Brent from $72.87 → $88.77 (+$15.90, +21.8%) — the largest cumulative moves since the Russia-Ukraine shock in early 2022. Oil is completely disconnected from the domestic economy — driven entirely by war, Hormuz, and tanker attacks. This disconnect IS the supply-side stagflation shock. Gold +1.07% to $5,133.1 — finally getting a safe-haven bid on the recession signal. Silver +1.93%, palladium +1.09%. Grains surging: wheat +3.04% (strongest in the series), corn +0.94%. The commodity picture is pure stagflation: energy and food rising while the economy contracts.

Equities: Red But Surprisingly Resilient. ES −0.76%, NQ −0.95%, YM −0.76%, RTY −1.19%. ES at −0.76% following a −92K NFP print is LESS BAD than expected. The bond rally (rate cuts back on the table) is providing a partial offset. Cumulative: ES from 6,881.62 → 6,783.00 (−1.43% from pre-war Friday). All Mag 7 deeply red: NVDA −1.37%, GOOG −1.22%, AMZN −1.15%, TSLA −1.07%, META −1.04%. Small caps worst at −1.19% — most sensitive to growth deterioration.

Sector Rotation: Stagflation Entrenched. XLE the ONLY green sector in pre-market (+1.50%) on $86 oil. Every other sector red. XLI −0.62%, XLB −0.67%, XLV −0.53%. The energy-up/everything-else-down dynamic is now the dominant regime. XLP (−0.07%) holding up slightly better than cyclicals as defensive positioning returns.

Breadth and Volatility: Crisis Levels. S5FD at 29.62 — the new series low, below the 30 extreme threshold. Only 29.6% of S&P stocks above their 5-day moving average. R2FD at 32.01. VIX at 25.40 — above the 25 crisis threshold for the second time in the series. MOVE at 74.53 — back above pre-war levels. COR1M at 22.97 — above 20, macro driving everything again. The breadth washout is more severe than Tuesday’s crisis (S5FD was 36.18 then, now 29.62). This is extreme.

FX: Dollar Still Bid But Currencies Bouncing Post-NFP. DXY at 99.280 (+0.25%) from overnight risk-off, but all G10 currencies are GAINING post-NFP as rate cut expectations weaken the dollar from the intraday perspective. AUD +0.50%, CHF +0.43%, GBP +0.40%. The “bad news is good news for currencies” dynamic: terrible NFP → Fed cuts sooner → dollar weakens. BTC −1.65% to $70,350 — crypto still selling, not acting as a recession hedge.

6. THE GAME PLAN

Today’s Key Events: February NFP at 8:30 AM (already released: −92K actual vs. +60K expected). Unemployment Rate and Average Hourly Earnings also released at 8:30 AM. War headlines continuous. This is a session that will be entirely defined by the NFP response.

The Bull Case: Bonds are rallying for the first time — rate cuts are back on the table. The 2Y fell 2.9 bps instantly. Equities are only −0.76% despite −92K NFP — surprisingly resilient. The Kaiser Permanente strike inflates the negative number (31K of the decline). Gold is finally bouncing (+1.07%), suggesting the forced liquidation phase is definitively over. The bond rally provides a partial floor for rate-sensitive assets. The “bad news is good news” narrative (Fed cuts sooner) could take hold. Peace talk reports remain a potential positive catalyst.

The Bear Case: NFP −92K is a CATASTROPHIC miss. The economy is shedding jobs while oil approaches $90. This is textbook recessionary stagflation — the worst-case macro scenario. The Fed is trapped: can’t cut (oil inflation) and can’t hold (job losses). WTI cumulative +28.1% in one week is an extraordinary supply shock. S5FD at 29.62 is the most extreme breadth washout in the series. VIX above 25 (crisis threshold). MOVE back above pre-war. Wednesday’s pro-cyclical recovery was a one-day bear market rally — the growth data has now collapsed underneath it. Even adjusting for the strike, the underlying payrolls trend has deteriorated sharply (January revised down, underlying February deeply negative).

Regime: Recessionary Stagflation. The NFP print fundamentally changes the macro classification. We have moved from “strongish economy absorbing an oil shock” to “contracting economy hit by an oil shock.” The bond market confirmed it instantly with the first rally of the series. The Fed is in a 1970s-style trap. The only question now: does the bond rally (rate cut hopes) provide a floor for equities, or does the oil surge ($86 heading toward $90) overwhelm everything? Today’s session will set the tone for next week.

Watch List

Brent above $90 — If Brent breaks $90 (currently $88.77), the market enters a zone where consumer spending damage becomes material and corporate margin compression accelerates. This would intensify the recessionary leg.

Bond rally sustainability — The first green bond session in seven. If Treasuries hold their gains through the close, it confirms the shift from inflation-fear to growth-fear. If bonds reverse and sell off despite −92K NFP, the inflation fear is overwhelming even recession signals.

Equities intraday response — ES −0.76% on −92K NFP is surprisingly restrained. Watch if equities rally on “rate cut” hopes (bad-news-is-good-news) or if the recession signal overwhelms. A close below 6,750 would be the worst level of the war.

Gold follow-through — Gold +1.07% is the first meaningful bounce in days. If gold holds above $5,100 and builds on the rally, the safe-haven function is re-established. A reversal back below $5,100 means forced selling resumes.

Peace talks / ceasefire — Still the ultimate wild card. A credible diplomatic headline would reverse oil, reverse equities, reverse everything. The Iranian peace feelers reported yesterday remain unconfirmed.

Morning check: the worst-case scenario has arrived. The economy is shedding jobs while oil approaches $90. Bonds have rallied for the first time in the war, confirming the market has shifted from inflation fear to growth fear. The Fed is trapped. But equities are holding better than expected, and the bond rally is providing a floor. The regime is recessionary stagflation. Today’s session will determine whether rate-cut hopes can offset the growth collapse, or whether the oil surge overwhelms everything.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.