☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: The war entered its fifth day with no de-escalation — but the market character has changed. For the first time in the DYRH series, international equities are GREEN: TOPIX +2.49%, DAX +1.43%, Euro Stoxx +1.46%. Energy has stabilized: WTI +0.07% to $74.61 — the first sub-1% crude move since the war began. Gold is bouncing +1.20% to $5,185.4, reversing yesterday’s −3.54% margin-call liquidation. The entire metals complex is green (platinum +3.88%, palladium +2.87%, silver +2.57%). The dollar is retreating for the first time: DX −0.18%. The factor structure has reversed: SPHB +1.24% leads while USMV is flat — high beta outperforming min vol for the first time in the war. The ARK complex is surging (ARKW +1.51%, ARKG +0.96%). US futures essentially flat: ES −0.12%, NQ −0.06%, RTY +0.08%. VIX pulling back for the first time to 23.22 (−1.48%). But bonds are STILL selling: 30Y leading the bear steepening (+2.2 bps). MOVE at 77.75 (crisis level). ADP Employment at 8:15 AM is today’s binary catalyst.

The Number That Matters: WTI at $74.61 — essentially flat (+$0.05) for the first time since the war began. After surging $12.54 (+22%) from Friday’s $62.02 to yesterday’s close of $74.56, crude has STOPPED going up. This is the most important cross-asset signal of the morning. If oil stops surging, the stagflation impulse moderates, bond selling can decelerate, and the inflation-fear premium built into all other assets begins to unwind. The Trump tanker escort and war-risk insurance announcement, combined with Iran’s degraded military capability (17 ships sunk, no navy/air force/radar per Trump) and the shorter “two weeks” Israeli war timeline, appears to be capping the energy upside.

The Setup: The regime is transitioning. The acute liquidation phase appears to be ending. The evidence is multi-dimensional: energy stabilization, metals bounce (liquidation over), dollar retreat, international equity recovery, factor reversal (cyclicals leading defensives), and the first VIX pullback of the war. However, three conditions must be met for this transition to be confirmed: (1) ADP data at 8:15 AM must not reignite stagflation fears; (2) the intraday recovery must hold through the close — if today opens flat and closes red, the pattern shifts from “buy the dip” to “sell the rally”; (3) bonds must stop selling — if the bear steepening accelerates with 10Y through 4.10%, the rate shock will overwhelm the equity re-risking attempt.

2. OVERNIGHT SESSION RECAP

Asia-Pacific

TOPIX +2.49% — the first green international session in the DYRH series. Japan imported essentially all of its energy and was crushed over Monday-Tuesday (Nikkei −5.5% cumulative). The bounce is a “catch-up recovery” from extreme oversold conditions. Korea’s KOSPI plunged approximately 12% on Tuesday (worst day on record per Reuters), far exceeding the initial −7.24% report — catching up from Monday’s holiday closure. Nikkei (USD) +0.65%, more muted than TOPIX.

Europe

DAX +1.43%, Euro Stoxx 50 +1.46%. Europe getting its first bid after approximately −7.5% cumulative losses over Monday-Tuesday. Trump’s tanker escort and insurance announcement directly addresses Europe’s energy supply chain vulnerability. Energy stocks were the overnight bright spot but XLE has since turned red in US pre-market (−0.48%).

US Pre-Market

Operation Epic Fury — Day 5. The war continues to escalate militarily even as markets attempt to price in resolution. Israel launched its “10th wave of attacks” targeting internal security command centers in Tehran, Karaj, and Isfahan. Death toll in Iran now exceeds 1,045 (up from 787). MAJOR ESCALATION: Iranian Navy frigate IRIS Dena reportedly sunk in the Indian Ocean approximately 40 nautical miles south of Sri Lanka — 32 crew rescued, 100+ unaccounted for. This marks a GEOGRAPHIC EXPANSION of the conflict far beyond the Middle East.

CENTCOM Commander Admiral Cooper: US has “destroyed 17 Iranian ships, including the most operational Iranian submarine.” Trump told reporters Iran has “no navy, air force, air detection, or radar” after the attacks. Israel bombed the Assembly of Experts building as they met to elect Khamenei’s successor — targeting Iran’s political succession. IRGC announced ground forces entered battlefield operations with 230 drones. Turkey/NATO intercepted an Iranian ballistic missile in the eastern Mediterranean — NATO is now DIRECTLY involved. Russia warned Bushehr nuclear power plant is under threat. Israeli official: war goals achievable in “two weeks total.” Iran’s missile strikes on Israel have “significantly decreased” — potentially rationing munitions.

Prior session (March 3 close): ES −0.92% (recovered from −2.5% at the lows); Dow −403 pts (recovered from −1,277 at the lows). Gold −3.54% (deepened losses even as equities recovered). WTI $74.56 (+4.67%). S5FD 36.18 (−34.76%) — the most extreme breadth washout in the series. All 11 sectors red, all 12 factors red.

ADP National Employment Report (February) at 8:15 AM EST — HIGH IMPACT. Prior: +22K (January, a massive miss vs. 48K expected). Consensus: approximately 48K. This is the first major labor data since the war began. A weak print (<20K) reignites stagflation fears; a strong print (>70K) challenges the growth scare but pushes rates higher. Either way, the data will be interpreted through the war lens — even a strong print may be dismissed as backward-looking.

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 03/03/26. Provided for informational purposes only; not as investment advice.

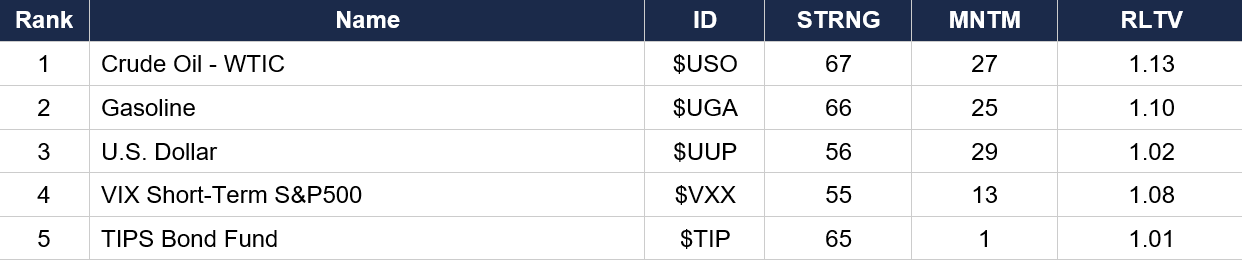

Asset Classes — Top 5

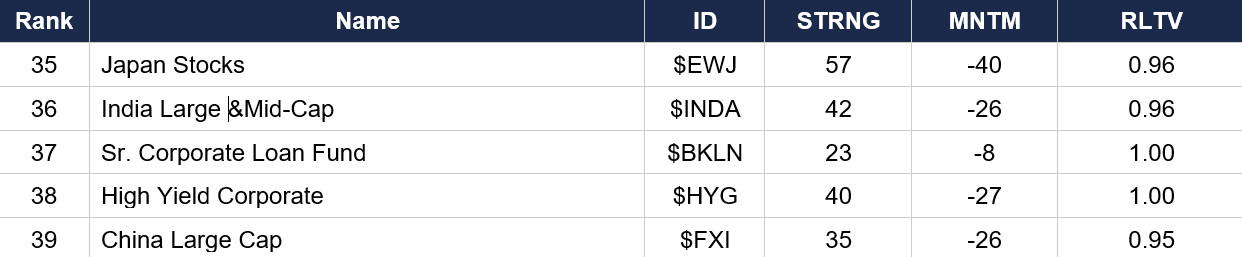

Asset Classes — Bottom 5

Regime signal: The top three are unchanged — crude oil, gasoline, and the US dollar continue to dominate. But VIX ($VXX) has entered the top 5 at rank 4 (MNTM 13) — volatility as an asset class now ranks ahead of bonds and gold. This is new: the market is allocating to vol itself as an asset. The dollar’s MNTM surged to 29, the highest momentum reading on the entire board. Gold has CRASHED to rank 13 (MNTM −9) — down from rank 4 last week. Yesterday’s −3.54% margin-call liquidation obliterated gold’s momentum score. Today’s +1.20% bounce may begin to stabilize this, but the damage is done in the rankings. Japan ($EWJ, MNTM −40) is now the worst momentum reading on the entire board — the KOSPI −12% and Nikkei’s cumulative losses have devastated Asian equity momentum. S&P 500 ($SPY rank 23, MNTM −9) and Nasdaq ($QQQ rank 19, MNTM −3) continue sliding but at a slower pace.

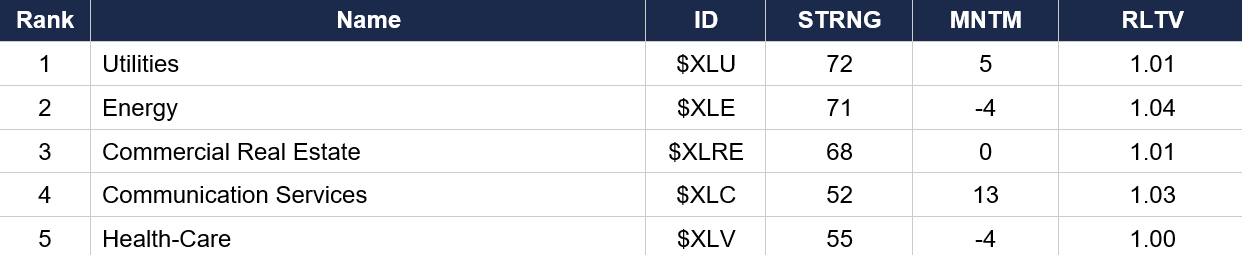

Sector ETFs — Top 5

Sector ETFs — Bottom 5

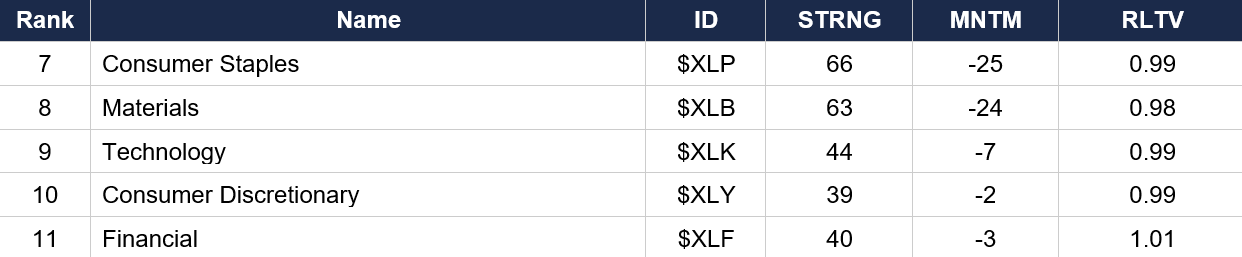

Regime signal: Communication Services ($XLC) has surged to rank 4 with MNTM 13 — the highest sector momentum on the board. This is a significant shift: a pro-cyclical sector now has the strongest momentum. Energy MNTM has turned negative (−4) for the first time — the “buy energy for war protection” trade is fading in the rankings even as crude prices remain elevated. Industrial MNTM collapsed further to −18. Consumer Staples MNTM at −25 remains the worst. Materials MNTM −24. The board is showing an unusual split: utilities and energy hold top ranks on strength, but the momentum leaders are shifting to communication services and commercial real estate.

Industry ETFs — Top 5

Industry ETFs — Bottom 5

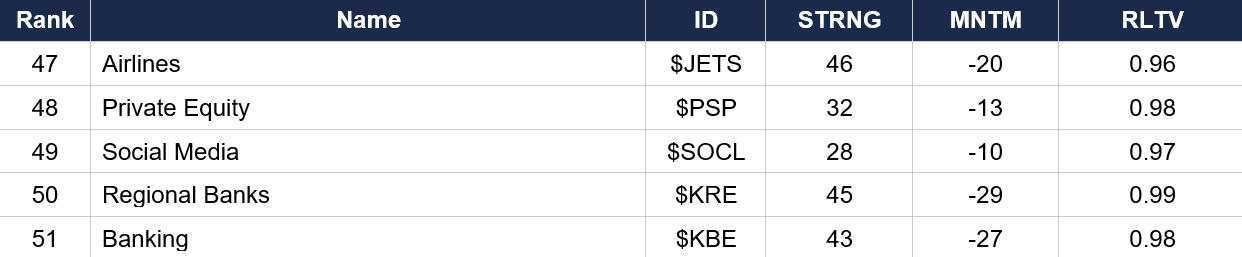

Regime signal: Software ($IGV) at rank 7 with MNTM 24 — still the highest industry momentum on the board, diverging sharply from Semiconductors ($SMH rank 39, MNTM −20). The software-semis divergence is widening. Rare Earth Minerals ($REMX) has fallen to rank 9 with MNTM collapsing to 0 (from 26 last week) — the strategic mineral hoarding impulse has faded. Gold Miners ($GDX) dropped to rank 17 (MNTM −10) reflecting yesterday’s gold crash. Aerospace-Defense ($ITA) at rank 5 but MNTM at 0 — the defense trade is exhausted. Agricultural Business ($MOO, MNTM −30) is the worst industry momentum on the board. Regional Banks ($KRE, MNTM −29) and Banking ($KBE, MNTM −27) remain near the absolute bottom. Steel ($SLX, MNTM −29) joining the worst readings.

4. MORNING DATA REACTION

ADP National Employment Report (February) at 8:15 AM EST is today’s key data event. Prior: +22K (January), which was a massive miss vs. 48K expected. December was revised to 37K. The two-month trend has been extremely weak. Consensus for February is approximately 48K.

This report drops into a market already pricing stagflation — but attempting to transition to a more constructive regime. A strong number (>70K) could ease growth fears but would reinforce the “Fed on hold” narrative and push yields higher, potentially overwhelming the equity re-risking attempt. A weak number (<20K) would confirm the pre-war labor market was already deteriorating and compound stagflation fears. The labor data will be interpreted through the war lens: even a strong print may be dismissed as backward-looking; a weak print will be amplified.

Context from Monday’s ISM Manufacturing (released March 2): Headline 52.4 (vs. 51.7 est., prior 52.6) — expansion held for the second consecutive month. But Prices Paid surged to 70.5 (vs. 59 prior) — the highest since mid-2022, driven by steel, aluminum, and tariff-related costs. New Orders 55.8 (strong). Employment 48.8 (still contracting). The ISM confirmed manufacturing expansion with intensifying input cost pressure — the Prices Paid surge at 70.5 is the stagflationary signal, and that was BEFORE the Hormuz closure and the $12+ oil surge.

Friday’s PPI (released February 27): Final demand +0.5% MoM (vs. +0.4% December). Core PPI (ex-food/energy/trade) +0.3% MoM for the ninth consecutive increase. The inflation pipeline was already hot before the war.

5. THE DYRH READ

Regime: Transitional — Acute Liquidation Phase Ending, Pro-Cyclical Re-Risking Emerging, But Bond Market and Breadth Not Confirming. Confidence: Moderate-High on “liquidation phase ending.” Low-Moderate on sustainability.

Yield Curve: Bear Steepening Emerging — Critical Shift. The curve regime has CHANGED. For the first three days, the curve was bear-flattening (front end leading). Today the structure has inverted: 30Y leading at +2.2 bps (+0.47%) while 2Y barely moves (+0.2 bps, +0.06%). This is bear STEEPENING — the market is shifting from “near-term Fed path repricing” to “long-term inflation and fiscal premium.” The market believes the Fed will NOT cut (front end stable) but is pricing sustained higher oil and war spending as a permanent upward shift in the inflation trajectory. 10Y at 4.079% (+1.4 bps) — the pace of increase is decelerating (+8.7 → +2.9 → +1.4 bps per day). The 30Y at 4.728%. ADP data at 8:15 AM is a binary catalyst for the curve.

Commodity Complex — Energy Stabilizing, Metals Liquidation OVER. WTI +0.07% to $74.61 — essentially flat, the first sub-1% crude move since the war began. Brent +0.95% to $82.17. Heating oil actually RED (−0.26%) for the first time after three consecutive extreme surges. Natural gas −1.77%. The energy stabilization is the single most important cross-asset signal this morning. Gold bouncing +1.20% to $5,185.4 after yesterday’s −3.54%. Platinum +3.88% (reversing −10.34%), palladium +2.87%, silver +2.57%, copper +1.11%. The entire metals complex green — when all five metals reverse simultaneously after a synchronized crash, forced selling has cleared and natural buyers are re-entering. The liquidation phase is definitively over.

Factor Structure Reversed — Pro-Cyclical For First Time. SPHB +1.24% leading while USMV is flat — the COMPLETE REVERSAL of the past four sessions’ hierarchy. The USMV-SPHB spread has flipped to approximately −124 bps (high beta outperforming min vol by 124 bps). IJH +0.31% and IJR +0.17% green — mid-cap and small-cap participating in the risk-on rotation. DGRO −0.29% lagging as dividend and income strategies are sold in favor of cyclical positioning. This factor reversal confirms the regime is shifting from “sell everything” to “buy the beaten-down.”

Sector Rotation: First Pro-Cyclical Tilt. XLC +0.82% leads (communication services), XLY +0.48% (consumer discretionary), XLB +0.42% (materials — going from worst sector at −2.46% yesterday to third-best today). XLE at −0.48% is the WORST sector — the “buy energy for war protection” trade is unwinding. XLP −0.15% and XLF −0.16% are mild laggards. The shift from energy/defensive leadership to cyclical/growth leadership is the sector-level confirmation of the regime transition.

VIX: 23.22 (−1.48%) — First Red VIX in the Series. Still well above 20 and the pre-war baseline, but the pullback is directionally significant. The broader vol complex remains structurally elevated: MOVE at 77.75 (crisis level from prior close), GVZ 38.77, VXN 27.51, VVIX 116.02. If VIX1D (prior close 20.30) opens below 18, the near-term panic has subsided. If it remains above 20, significant intraday risk remains.

Breadth at Extreme Washout — Rebound Setup. S5FD at 36.18 (−34.76%) and R2FD at 32.83 (−31.19%) from yesterday’s close are the most extreme breadth readings in the series. When only 36% of S&P stocks are above their 5-day average, historical precedent favors violent short-term rebounds. The question for today: does the international bounce, metals reversal, factor rotation, and VIX pullback translate into breadth improvement? If S5FD recovers above 40, it confirms a short-term bottom. If it stays below 36, damage is deepening regardless of index-level recovery.

FX — Dollar Retreats, Everything Recovers. DX at 98.830 (−0.18%) — first red dollar session since the war began after three consecutive green sessions. Nearly all currencies green vs. USD: JPY +0.29%, NZD +0.23%, CHF +0.19%, EUR +0.18%, GBP +0.09%. BTC surging +3.73% to $71,020 — the biggest BTC move since Monday’s +5.46%. The dollar retreat plus gold bounce plus crypto surge equals the “panic bid for USD safety” is unwinding.

6. THE GAME PLAN

Today’s Key Events: ADP National Employment Report 8:15 AM (HIGH IMPACT — binary catalyst). War headlines continuous. The data matters more today than any prior session because the market is at a regime inflection point.

The Bull Case: Energy has stopped surging (WTI +0.07%) — the core driver of the stagflation impulse is pausing. Metals liquidation is over — the entire precious metals complex has reversed. Dollar retreating for the first time. International equities bouncing from extreme oversold (TOPIX +2.49%, DAX +1.43%). Factor structure reversed to pro-cyclical (SPHB leading). ARK complex surging. VIX pulling back. Iran’s military capability being systematically destroyed (17 ships, no radar). Israeli assessment: war goals achievable in “two weeks.” Breadth at levels that historically precede violent rebounds. Monday recovered 100% of losses, Tuesday recovered 63% — the buy-the-dip playbook has worked twice. ADP strong print (>70K) would ease growth fears.

The Bear Case: Bonds are STILL selling — the long end is accelerating in a bear steepening pattern. MOVE at 77.75 (crisis level). The bond market is NOT participating in the risk-on rotation. The war is still escalating: death toll above 1,045, Iranian frigate sunk near Sri Lanka (geographic expansion), IRGC ground forces engaged, Turkey/NATO intercepting missiles, Bushehr nuclear plant threatened. The recovery-weakening pattern: Monday recovered 100%, Tuesday 63% — if today opens flat and fades, the pattern confirms transition from “buy dips” to “sell rallies.” ADP weak print (<20K) would reignite stagflation fears. KOSPI −12% (worst day on record). S5FD at 36.18 means underlying breadth damage is severe regardless of index-level moves.

Regime: Transitional. Acute Liquidation Phase Ending, Pro-Cyclical Re-Risking Emerging, But Bond Market and Breadth Not Confirming. The overnight session is the first constructive pre-market in the DYRH series. The combination of energy stabilization, metals bounce, dollar retreat, international recovery, and factor reversal suggests the worst of the liquidation is over. But bonds still selling and breadth at crisis levels mean this transition is fragile. ADP at 8:15 AM is the gatekeeper.

Watch List

ADP at 8:15 AM — Binary catalyst. Strong (>70K) eases growth fears but pushes rates higher. Weak (<20K) reignites stagflation. The number will be interpreted through the war lens either way.

10Y above 4.10% — If the bear steepening accelerates and 10Y breaks back above 4.10%, the rate shock will overwhelm the equity re-risking attempt. Currently at 4.079%.

Intraday recovery pattern — Monday recovered 100%. Tuesday recovered 63%. If today opens flat/green and closes red, the “sell the rally” pattern is confirmed — a bearish shift in market character.

Gold stabilization — Gold +1.20% pre-market after −3.54% yesterday. If gold holds above $5,150, the margin-call phase is definitively over. If it reverses back below $5,100, forced selling has resumed.

Ceasefire / diplomatic headlines — Israeli official says “two weeks” to achieve war goals. Any credible ceasefire signal would trigger a massive short squeeze across all assets priced for escalation.

Morning check: the war continues to escalate, but the market character has changed. Energy has stopped surging. Gold is bouncing. The dollar is retreating. International equities are green for the first time. The acute liquidation phase appears to be ending. But bonds are still selling, breadth is at crisis levels, and ADP at 8:15 AM is a binary catalyst that could override the entire overnight narrative. The regime is transitional — constructive but fragile.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.