☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: NEUTRAL / CONSOLIDATING — ES 7,067.75 THIRD CONSECUTIVE WAR HIGH. MOVE CRASHED −8.62% TO 67.94 — FIRST SUB-PRE-WAR-BASELINE PRINT OF THE ENTIRE WAR. PHILLY FED APRIL 26.7 VS 10.3 CONSENSUS — HIGHEST SINCE SEPT 2025 AND A 16.4-POINT UPSIDE SURPRISE. JOBLESS CLAIMS 207K VS 213K. COR1M 11.05 NEW WAR LOW. TSLA +7.62% ON MUSK AI5/AI6 + UBS UPGRADE. MSFT +4.61% EXTENDING SOFTWARE REFLATION. AAPL +2.94% BREAKING THE THREE-DAY WEAKNESS STREAK. TSMC RECORD Q1 +58% YOY. TRAVELERS MASSIVE Q1 BEAT. THE BOND MARKET HAS CAPITULATED.

The bond market has capitulated. MOVE Index crashed −8.62% overnight to 67.9410 — the first sub-pre-war-baseline print (73.21) of the entire war, and now 5.27 points BELOW pre-war levels. From war-high 115.02 (Day 21), MOVE has declined 47.08 points. The trajectory through the post-ceasefire-collapse period: Friday 72.15 → Monday firmed → Tuesday 74.42 (peak walk-back after Islamabad collapse) → Wednesday 74.35 → Thursday 67.94 (structural breakthrough). This is capitulation, not normalization. Through the Islamabad talks collapse, the Hormuz blockade order, US destroyers entering the strait, Friday’s CPI hot print, Michigan 47.6 all-time-low sentiment, and the ongoing operational blockade enforcement, the rates-vol complex has crossed below where it started the war. The bond market is no longer reserving caution about Fed stasis durability; it is now pricing the equity re-rating and the bifurcation thesis without reservation.

The 8:30 AM data layer delivered the cleanest possible confirmation. Philly Fed Manufacturing April printed 26.7 — against 10.3 consensus and 18.1 prior. This is a +16.4 point upside surprise — the highest Philly Fed print since September 2025 and the strongest month-over-month acceleration of the year. Combined with Tuesday’s PPI services-flat print and yesterday’s Empire State +11.0 vs +0.3 (+10.7 surprise), this is THREE consecutive data releases all validating the bifurcation thesis that the war shock was contained to March goods/energy inflation while April activity is accelerating. Initial Jobless Claims 207K vs 213K consensus, prior revised to 218K — claims DECLINED 11K week-over-week and beat consensus by 6K. The labor market remains structurally tight with the 4-week moving average still below the 210K softening threshold. No tariff impact has yet shown up in claims (first meaningful read arrives April 24). UK GDP m/m also blew out at +0.5% vs +0.1% consensus — global growth is re-accelerating in sync.

The equity tape is pricing the capitulation cleanly. ES at 7,067.75 closed Wednesday with a +0.10% print and held overnight for a THIRD consecutive war-high session — now +186 points / +2.7% above the pre-war 6,881.62 baseline. Cumulative recovery from the Day 22 low is +8.8% in 13 sessions. Mag 7 six green / one red but the composition has rotated dramatically from yesterday: TSLA +7.62% LEADING (on Elon Musk’s AI5 chip design completion + AI6 tease + UBS upgrade from Sell to Neutral — a triple-catalyst breakout; TSLA is now at its highest level since March 25). MSFT +4.61% extending yesterday’s +2.27% for a cumulative two-day move of ~+7%. AAPL +2.94% — BREAKING the three-day weakness streak decisively (AAPL’s strongest single-session move of the week). META +1.37%, NVDA +1.20%, GOOG +1.18%. AMZN the only red Mag 7 at −0.21% (first AMZN red session of the rally). Yesterday’s 455 bp intra-Mag-7 dispersion has expanded to 783 bp today, but the leadership has rotated from META+AMZN to TSLA+MSFT+AAPL — the rally is rotating through the Mag 7 complex rather than narrowing to the same few names.

Overnight corporate results: TSMC Q1 RECORD — revenue +35% YoY to NT$1.134T (~$35.71B) beating LSEG consensus, net profit +58.3% YoY to a record NT$572.48B (~$18.11B). AI chip demand is the unambiguous driver. TSMC stock +2% overnight on the print. Travelers Q1 MASSIVE BEAT — core EPS $7.71 vs $6.82 consensus (+$0.89 beat, +13%), net income $1.711B vs $395M prior year (+333% YoY), ROE 21.1%, combined ratio excellent at 88.6%, catastrophe losses $761M vs $2.266B prior year, 14% dividend increase to $1.25/share. Travelers is the EIGHTH consecutive bank/financial earnings beat this week. Note: the DYRH lists UNH as reporting today, but per UnitedHealth’s own press release UNH actually reports April 21 — flag this DYRH error for the calendar.

The Number That Matters: MOVE at 67.94 — FIRST SUB-PRE-WAR-BASELINE PRINT OF THE ENTIRE WAR. The Bond Market Has Formally Declared The War’s Rates-Vol Shock Over.

MOVE crossing below the 73.21 pre-war baseline is the single most structurally bullish cross-asset signal since the Day 29 post-ceasefire thrust. The bond market spent 34 trading days (Day 1 through Day 34 close) at or above the pre-war baseline — even through the equity rally, hold, collapse, rally, and rally further. Today’s print says the rates-vol complex has fully absorbed every war-related shock: the Islamabad collapse, the Hormuz blockade, the CPI hot print, the Michigan all-time low, the ongoing operational blockade enforcement. Every reservation the bond market held about the post-Wednesday-thrust equity re-rating has been walked back. The implications are structural: Fed stasis is the consensus path and durable; the war-inflation shock is contained to goods/energy in March; the post-ceasefire thrust regime call from Day 29 is fully on. MOVE sub-baseline + ES at third consecutive war high + COR1M at new war low 11.05 + Philly Fed 26.7 blowout + Claims 207K beat = the cleanest possible ‘regime change confirmed’ configuration of the entire war.

The Setup: Steepener Twist — Neutral / Consolidating — Energy Steady. MOVE Breaks Below Pre-War Baseline. Philly Fed Blows Out. Claims Tight. Three Regimes In Parallel For The Fourth Consecutive Session.

Three regimes continue to operate in parallel for a fourth consecutive session: equities at a third consecutive war high (7,067.75), correlations at a new war low (COR1M 11.05), and the curve in a steepener twist with 2Y falling while 30Y rises. The STEEPENER TWIST is notable — it is not a bear steepener (both ends rising) but a classic twist with front falling 0.2 bps and long rising 0.5 bps. The front-end move reflects Fed-cut probability adding back in; the long-end move reflects residual term premium concerns from the Hormuz blockade operational enforcement. The MOVE capitulation to 67.94 says the long-end move is not meaningful concern — it is marginal term-premium adjustment. The 8:30 AM data layer — Philly Fed 26.7 blowout + Claims 207K — validates every piece of the bifurcation thesis on the same morning.

2. OVERNIGHT SESSION RECAP

Asia-Pacific

Nikkei +1.14% to 59,255 — Japan posts its strongest single-session bid in over a week, reversing Wednesday’s −0.93% decline in full and then some. Topix +0.01% essentially flat — the Nikkei-Topix divergence reflects concentrated tech/semi bid via the larger-cap export-heavy Nikkei composition. TSMC Q1 record +58% YoY profit was the proximate catalyst — Asian semis broadly caught bids on the read-through. JPY −0.06% against USD — relative stability after yesterday’s weakness. Korean and Hong Kong markets traded in sync with the constructive risk tone.

Europe

DAX +0.55% to 24,392 extending Wednesday’s modest bid. EuroStoxx 50 +0.41% to 5,911 — European strength reversing Wednesday’s −0.71% underperformance. The catalyst: UK GDP m/m printed +0.5% vs +0.1% consensus and +0.1% prior — a FIVE-fold upside surprise on UK growth that has triggered a broad European growth-rebound trade. EUR −0.20% and GBP −0.25% both weaker as the USD firmed modestly, but European equity reaction to the UK GDP blowout has been constructive. European financials leading on the read-through from the strong US bank earnings week.

US Pre-Market

Day 49 of Operation Epic Fury. Q2 Day 12. Thursday morning of bank earnings week + TSMC + NFLX + regional data prints.

US FUTURES CONSTRUCTIVE, ES THIRD WAR HIGH: ES 7,067.75 (+0.10%, THIRD CONSECUTIVE WAR HIGH), NQ 26,410.75 (+0.17%), YM 48,752 (+0.17%), RTY 2,725.10 (−0.01%). The ES at 7,067.75 is now +186 above the pre-war 6,881.62 baseline (+2.7%) and the cumulative recovery from Day 22 low is +8.8% in 13 sessions. Russell flat again — small-caps consolidating while large-caps extend. The breakout above 7,000 (cleared Wednesday) is being defended cleanly.

MAG 7 SIX GREEN / ONE RED — TSLA-LED ROTATION: TSLA +7.62% LEADING (largest Mag 7 single-session move of the week; catalyst: UBS upgrade Sell→Neutral Monday + Elon Musk AI5 chip design completion announcement + AI6 tease). MSFT +4.61% (cumulative two-day ~+7% extending the software reflation). AAPL +2.94% (BREAKING the three-session weakness streak — the longest of the war — with Apple’s strongest single-session move of the week). META +1.37%. NVDA +1.20%. GOOG +1.18%. AMZN −0.21% (first red Mag 7 session of the rally — AMZN giving back some of yesterday’s +3.81% pre-market bid). Dispersion at 783 bp (TSLA +7.62% to AMZN −0.21%) is the widest of the past week, but the composition has rotated from yesterday’s META+AMZN leadership to today’s TSLA+MSFT+AAPL leadership — broadening rather than narrowing.

FACTORS — SPHB LEADING, USMV+SPHB SPREAD −0.68% STILL DEEPLY RISK-ON: USMV−SPHB spread at −0.68% (fourth consecutive deeply risk-on session: Day 29 −2.89%, Tuesday −1.52%, Wednesday −1.40%, Thursday −0.68%). Notably MTUM −0.13% (momentum not working today) and SPLV −0.40% — the factor tape has rotated from momentum-led to high-beta-led. SPHB +0.97% leading factors. LRGF +1.05%. QUAL +0.54%. USMV +0.29% (defensives with a bid today). RSP +0.04% essentially flat. IJH mid-cap −0.29%, IJR small-cap −0.13% — the size factor has flipped from Tuesday’s small-cap leadership to mega-cap leadership. VLUE −0.35%. The factor tape is 6/12 green — less broadly risk-on than Wednesday’s 11/12 but still negative USMV-SPHB spread keeps the structural call in place.

THEMATICS CONCENTRATED RISK-ON: FINX +4.12% leading (fintech rally on TSLA/software reflation read-through + bank earnings week). ARKW +3.81% (Next Gen Internet). CIBR +2.76% — cyber RECOVERING strongly after yesterday’s −0.63% dip; the IGV structural-wound narrative is healing. ARKQ +2.25%. ARKG +2.18%. BLOK +1.47% (BTC holding $74K). SOXX +0.15% essentially flat — semis consolidating ahead of TSMC’s official call later today. DRIV −0.15%. ITA −0.61% (defense giving back — WTI pullback removes acute geopolitical premium). ICLN −1.01% (clean energy giving back yesterday’s +4.01% spike). PAVE −1.71% (infrastructure the only meaningfully red thematic — cyclical positioning unwind).

SECTOR READ: XLK +1.60% leading (continued tech leadership). XLY +1.49% (AMZN/TSLA combo — TSLA offsets AMZN weakness). XLF +0.75% (constructive on continuing bank beat narrative — Travelers BAT, MS record, BAC +25% YoY). XLC +0.69%. XLRE −0.05% flat. XLE −0.34% (tracking WTI cleanly for the first time in the war — the decoupling has resolved). XLP −0.50% (consumer staples unwind). XLV −0.71% (healthcare soft ahead of UNH/ABT). XLU −0.97% (utility unwind on bond-vol compression). XLB −1.21%, XLI −1.25% (materials and industrials the two meaningful red sectors — cyclical unwind).

CRITICAL OVERNIGHT EVENTS: 2 AM UK GDP m/m +0.5% vs +0.1% consensus (5x upside surprise). 8:30 AM Philly Fed April 26.7 vs 10.3 consensus (+16.4 MASSIVE upside surprise). 8:30 AM Jobless Claims 207K vs 213K consensus, prior revised to 218K (beat). Overnight TSMC Q1 record +58.3% YoY profit to NT$572.48B. Travelers Q1 core EPS $7.71 vs $6.82 (+$0.89 beat). 2 PM Fed’s Waller speaks Friday — notable hawkish-tilting FOMC member — his commentary is the next Fed communication catalyst. Williams (NY Fed) gave a speech at 7:35 AM that preceded the data prints. CENTCOM continues to report Hormuz blockade enforcement ‘no breaches in 48 hours’ — operational but not kinetic.

3. THE PRIOR DAY’S REGIME

Data from JeffQuiggle.com as of 04/15/26. Provided for informational purposes only; not as investment advice.

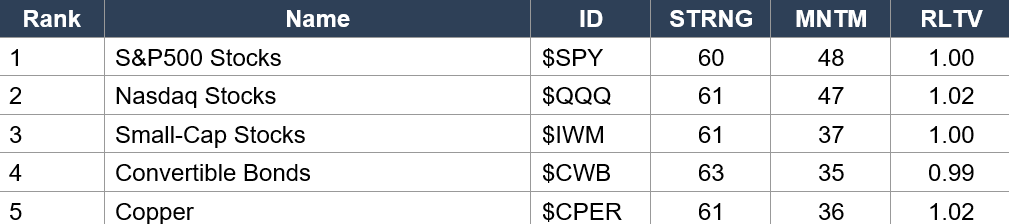

Asset Classes — Top 5

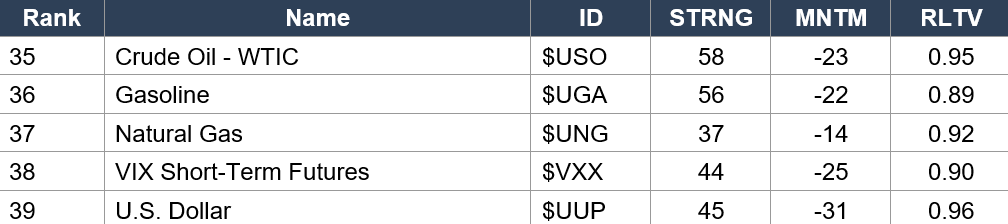

Asset Classes — Bottom 5

Regime signal: S&P500 ($SPY rank 1, MNTM 48 — HIGHEST momentum reading of the entire war) EXTENDS its #1 position for a second consecutive data set with momentum UP 11 points from 37 to 48. This is extraordinary — the S&P’s momentum has accelerated sharply. Nasdaq ($QQQ rank 2, MNTM 47 — second-highest momentum in the data set, up 11 points from 36) confirms the US large-cap tech leadership is structural. Small-Cap ($IWM rank 3, MNTM 37) JUMPS from outside the top 5 to rank 3 with MNTM 37 — the small-cap leadership that appeared Tuesday is now captured in the data. Convertible Bonds ($CWB rank 4, STRNG 63 — highest STRNG in the data set) up 5 points from 29 to 35. Copper ($CPER rank 5, RLTV 1.02) makes the top 5 for the first time — the industrial-demand-rebound trade is appearing in the data. CRITICAL: Dollar ($UUP MNTM −31, RLTV 0.96) holds the worst momentum reading of any asset class — DEEPENING from −24 yesterday, confirming the DXY capitulation trade. VIX ($VXX MNTM −25, RLTV 0.90) — fear premium actively bleeding. Crude Oil ($USO rank 35, MNTM −23, RLTV 0.95) — the energy de-rating is accelerating: $USO RLTV trajectory 1.08 → 1.02 → 0.89 → 0.87 → 0.85 → 0.95 — wait, RLTV actually RECOVERED from 0.85 to 0.95 today. Energy is relatively less weak. Gasoline ($UGA MNTM −22) — demand destruction continuing. Precious metals: Silver ($SLV rank 26, MNTM 19, RLTV 1.03). Gold ($GLD rank 29, MNTM 16, RLTV 0.98). Crypto: Ethereum ($ETHA rank 21, RLTV 1.04 HIGHEST in the data set after copper-tier names). Bitcoin ($IBIT rank 23, MNTM 22, RLTV 1.02).

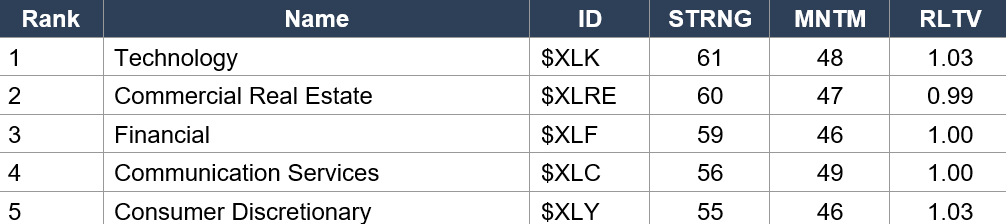

Sector ETFs — Top 5

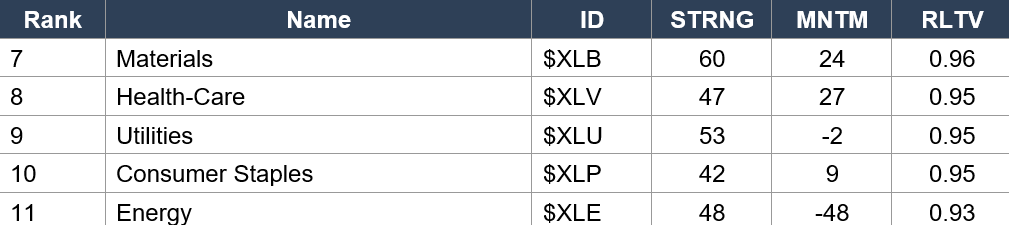

Sector ETFs — Bottom 5

Regime signal: Technology ($XLK rank 1, MNTM 48 — highest in the entire sector data set, RLTV 1.03) has DETHRONED Commercial Real Estate and claimed the #1 sector spot for the first time since the war began. Momentum jumped 15 points (33 → 48) in a single session — the largest single-session momentum acceleration of the war in the sector data. This is structural confirmation of the MSFT-led software reflation and the Mag 7 tech leadership. Commercial Real Estate ($XLRE rank 2, MNTM 47) — held rank 1 for four consecutive sessions and is now rank 2 but with momentum still HIGHER (44 → 47). Financial ($XLF rank 3, MNTM 46) up from rank 4 with momentum jumping 13 points — the bank earnings beats + Travelers massive beat are fully captured. Communication Services ($XLC rank 4, MNTM 49 — highest MNTM of any sector) — META/GOOG combo. Consumer Discretionary ($XLY rank 5, MNTM 46, RLTV 1.03) — AMZN/TSLA combo captured. Utilities ($XLU MNTM −2) turned NEGATIVE for the first time — bond-vol compression removing defensive bid. CRITICAL: Energy ($XLE rank 11, STRNG 48, MNTM −48, RLTV 0.93) — MNTM is now at −48, the DEEPEST negative sector momentum reading of the entire war (was −39 Tuesday, −32 Monday). The energy sector is in structural de-rating mode, and the Quiggle data confirms this is not noise — it is a multi-session trend. Today’s −0.34% XLE on +0.26% WTI is the first day the sector tracked crude cleanly (sector-equity decoupling resolved), but the STRUCTURAL position of energy remains the weakest sector.

Industry ETFs — Top 5

Industry ETFs — Bottom 5

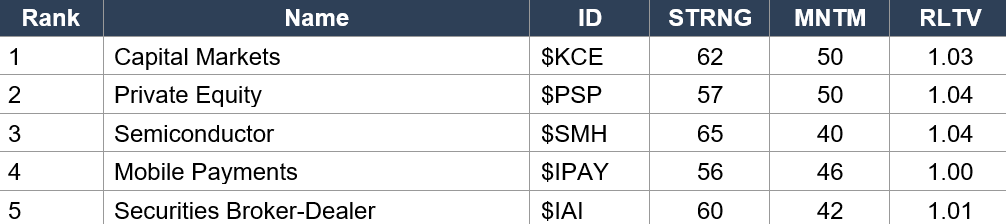

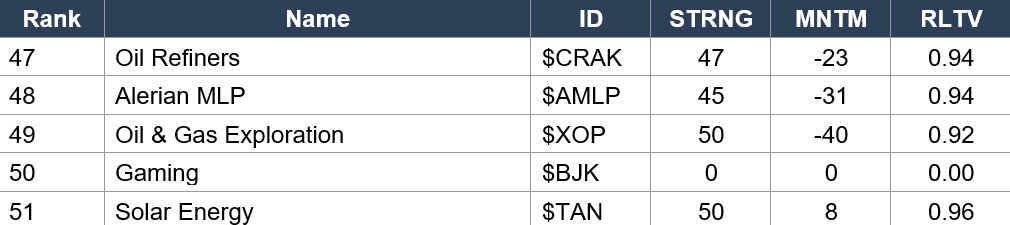

Regime signal: Capital Markets ($KCE rank 1, MNTM 50 — HIGHEST MNTM in any Quiggle data table, RLTV 1.03) has DETHRONED Semiconductor and claimed #1 industry spot. The seven-bank-beat streak is now fully reflected in the data; momentum jumped 11 points from 39 to 50 in a single session. Private Equity ($PSP rank 2, MNTM 50 tied for highest, RLTV 1.04) up from rank 5 — financial services capital formation is the structural leader. Semiconductor ($SMH rank 3, STRNG 65 HIGHEST of any industry, MNTM 40, RLTV 1.04) held strong ahead of TSMC's official Q1 call today. Mobile Payments ($IPAY rank 4, MNTM 46). Securities Broker-Dealer ($IAI rank 5, MNTM 42). The financial services complex dominates the top 5. Banking ($KBE rank 9, MNTM 35), Regional Banks ($KRE rank 12, MNTM 31) — all constructively positioned. CRITICAL ENERGY COMPLEX STRUCTURAL DETERIORATION CONTINUES: Oil & Gas Exploration ($XOP rank 49, MNTM −40) DEEPER than Tuesday's −36 (worst in any industry except BJK null). Alerian MLP ($AMLP rank 48, MNTM −31). Oil Refiners ($CRAK rank 47, MNTM −23). The energy industry de-rating is now at multi-week extreme readings. Software Technology ($IGV rank 38, MNTM 26) — the IGV recovery continuing: rank 50 Friday → 47 Tuesday → 38 Thursday, MNTM −14 Friday → +3 Tuesday → +26 today. The IGV normalization is real and accelerating. Cyber Security ($CIBR rank 39, MNTM 21, RLTV 0.95) — CIBR recovery continuing as well (rank 45 Monday → 39 today).

4. MORNING DATA REACTION

8:30 AM — PHILLY FED MANUFACTURING APRIL: 26.7 (vs 10.3 consensus, prior 18.1). MASSIVE +16.4 UPSIDE SURPRISE. Highest Reading Since September 2025.

The Philly Fed April print is the cleanest possible data signal that post-ceasefire regional manufacturing is accelerating sharply. Actual 26.7 against a +10.3 consensus represents a +16.4 point upside surprise — one of the largest Philly Fed surprises of the past year. The print is UP from the 18.1 prior (which was already the highest since September 2025), meaning April activity accelerated beyond an already-constructive March. Combined with yesterday’s Empire State +11.0 vs +0.3 consensus (+10.7 surprise), this is a TWO-FOR-TWO perfect data sequence for April regional manufacturing. Both major regional Fed surveys printed their strongest readings in months on the same week. Philly Fed has historically been the most reliable regional leading indicator for ISM Manufacturing — if the April pattern holds, ISM Manufacturing PMI for April (releasing May 1) could surprise meaningfully to the upside and set up a structural ‘no landing’ narrative going into the April 29 FOMC press conference.

INTERPRETATION: The Philly Fed + Empire State + PPI-services-flat trifecta is the definitive validation of the bifurcation thesis. March’s CPI gasoline +21.2% / Michigan 47.6 sentiment shock was a snapshot of the war’s energy peak, not a broad inflation trend. April data shows services and regional manufacturing rebounding cleanly. Powell on April 29 will have the fullest possible data cover to argue ‘look through the war shock’ without market pushback. The 2Y at 3.759% fell 0.2 bps on the print, confirming the front-end is ADDING Fed-cut probability on the strong activity print (paradoxically) because the labor market remained tight (Claims beat) while activity accelerated (Philly Fed blew out) — the perfect ‘activity without inflation’ combination that unlocks Fed easing optionality.

8:30 AM — INITIAL JOBLESS CLAIMS: 207K (vs 213K consensus, prior revised to 218K). −11K WEEK-OVER-WEEK. Labor Market Remains Structurally Tight Ahead Of The First Post-Tariff Signal.

Claims beat consensus by 6K and declined 11K from the prior week. The 4-week moving average is now well below the 210K softening-watch threshold. This is the last pre-tariff-signal release — the first release that could plausibly contain tariff-driven layoff filings is next Thursday (April 24, week ending April 19). The 207K print establishes that the labor market enters the post-tariff period in structurally tight condition, giving it maximum runway to absorb any coming disruption without hitting Fed-concern thresholds. The insured unemployment rate at 1.2% is consistent with 2018-2019 tight-labor-market conditions. Continuing claims trajectory is essential to watch — the lowest print since May 2024 on the prior week’s release confirmed workers losing jobs are still finding new ones.

INTERPRETATION: The combination of Philly Fed 26.7 blowout + Claims 207K beat = ‘activity without labor market heat’ — the exact data configuration the Fed needs to telegraph patience through the April 29 meeting. Fed stasis with preserved optionality is fully priced as the consensus path. The MOVE crash to 67.94 (sub-pre-war baseline) reflects the bond market’s capitulation to this framework — rates-vol is now pricing zero reservation about the Fed path over the next 6-12 months.

2 AM — UK GDP M/M: +0.5% (vs +0.1% consensus, prior 0.1%). 5x Upside Surprise. Global Growth Re-Accelerating.

UK GDP m/m printed +0.5% against +0.1% consensus — a 5x upside surprise and the strongest UK monthly growth read in months. Combined with the US Philly Fed and Empire State blowouts, the global growth tape is re-accelerating in sync. The UK print triggered European equity strength (DAX +0.55%, EuroStoxx +0.41%) and is supportive of the broader global reflation narrative. GBP −0.25% on the session despite the GDP strength reflects BoE-ECB divergence pricing rather than UK weakness.

Overnight — TSMC Q1 2026 RECORD: Revenue NT$1.134T (+35% YoY) vs LSEG Consensus Beat. Net Profit NT$572.48B (~$18.11B, +58.3% YoY) — Record.

TSMC delivered a record Q1 2026 with revenue of NT$1.134 trillion (~$35.71 billion USD), up 35% YoY and beating the LSEG consensus estimate of NT$1.125 trillion. Net profit came in at a record NT$572.48 billion (~$18.11 billion), up 58.3% YoY. AI chip demand for NVDA and AAPL-adjacent products was the unambiguous driver. 2026 capex guidance of $52-56 billion (up ~30% from $40.9B in 2025) is the clearest signal of sustained 2027-2028 demand visibility. TSMC stock +2% overnight — a restrained reaction given how much was already priced in (options implied 7.13% move pre-earnings). The official Q1 earnings call at 2 AM Eastern time is the next TSMC catalyst, with Q2 guidance being the main variable.

Pre-Market — TRAVELERS Q1 2026 MASSIVE BEAT: Core EPS $7.71 vs $6.82 est (+$0.89 beat). Net Income $1.711B vs $395M Prior Year (+333% YoY). ROE 21.1%. Combined Ratio 88.6%. 14% Dividend Increase To $1.25/Share.

Travelers delivered exceptional results. Core EPS of $7.71 vs $6.82 consensus is a +$0.89 / +13% beat. The year-over-year earnings growth is extraordinary: net income of $1.711 billion vs $395 million in Q1 2025 represents a +333% jump, driven primarily by dramatically lower catastrophe losses ($761 million vs $2.266 billion prior year — Q1 2025 had been hit by severe California wildfires). Combined ratio of 88.6% is excellent — well below 90% signals strong underwriting profitability. ROE of 21.1% is well above peer averages. Net investment income +9% on larger portfolio. Underlying underwriting income of $1.521B pre-tax — sixth consecutive quarter above $1.5B. 14% dividend increase to $1.25/share quarterly. $1.985B of share repurchases in Q1. Combined with GS Monday + JPM/WFC/BLK/C Tuesday + BAC/MS Wednesday + TRV Thursday = EIGHT consecutive financial earnings beats this week, with zero weak links.

Today’s Remaining Calendar:

TSMC official Q1 earnings call (2 AM ET, already completed). ABT earnings pre-market. NFLX Q1 earnings AFTER CLOSE — the session’s largest after-hours catalyst. Other regional/specialty earnings throughout the day. FRIDAY — Waller (Fed) 2 PM speech is the first Fed communication after the data blowout; Regional banks (Ally, Fifth Third, Regions, State Street, Truist) Q1 pre-market; Housing Starts + Building Permits. NEXT WEEK — UNH actually reports Monday April 21 (DYRH had this wrong for today). APRIL 22 — Two-week ceasefire framework formally expires (de facto already dead since Sunday April 12 Islamabad collapse). APRIL 24 — First post-tariff Claims signal (week ending April 19). APRIL 28-29 — FOMC meeting; Powell press conference April 29.

5. THE DYRH READ

Regime: Steepener Twist — Neutral / Consolidating — Energy Steady. Three regimes in parallel for a fourth consecutive session: equities at THIRD consecutive war high (ES 7,067.75), correlations at NEW war low (COR1M 11.05), curve in steepener twist (front falling, long rising). MOVE crash to 67.94 represents the first sub-pre-war-baseline print of the entire conflict — the bond market has capitulated. Philly Fed 26.7 vs 10.3 consensus + Claims 207K vs 213K + TSMC record + TRV massive beat + UK GDP blowout = the cleanest possible ‘regime change confirmed’ data day. Confidence: VERY HIGH on the regime classification given the multi-layer confirmation; low-noise signal environment confirmed by MOVE 67.94 and COR1M 11.05.

Yield Curve: STEEPENER TWIST — Classic Twist With Front Falling While Long Rises. Not A Bear Steepener.

2Y −0.2 bps to 3.759%, 5Y −0.4 bps to 3.890% (front-end Fed-cut probability adding back in), 10Y 0.0 bps flat at 4.281%, 30Y +0.5 bps to 4.899% (modest term-premium adjustment). This is a CLASSIC twist: front falling while long rising. Not a bear steepener (both ends rising — the most bearish config). Not a bull steepener (long falling faster than front). The steepener twist reflects markets pricing: (1) Near-term Fed easing odds increasing — the data-vol combination is perfect for Fed stasis with cutting optionality; and (2) Residual long-duration term premium concerns from Hormuz blockade operational enforcement. The front end at 3.759% is BELOW Tuesday’s 3.774% and Wednesday’s 3.761% — adding cut probability for the third consecutive session. The 2Y rally reflects the ‘activity without labor heat’ interpretation of the data. The 30Y at 4.899% modestly higher reflects the ongoing structural long-end caution about war-residual inflation — but the MOVE compression to 67.94 says this caution is not durable; it is marginal positioning.

MOVE 67.94 (−8.62%) — First Sub-Pre-War-Baseline Print Of The Entire War. Bond Market Capitulation. 47-Point Decline From War High.

MOVE at 67.9410 is the defining cross-asset event of Day 35. The trajectory: pre-war baseline 73.21 → war high 115.02 (Day 21) → post-ceasefire-thrust 72.15 (Day 29) → bounce to 74.42 (Tuesday post-Islamabad) → 74.35 (Wednesday) → 67.94 (Thursday, today). From the war high 115.02, MOVE has declined 47.08 points — a 40.9% decline. From pre-war baseline 73.21, MOVE is now 5.27 points BELOW, or −7.2%. This is the first time in the entire 35-day war that the rates-vol complex has crossed below its pre-war starting point. The structural implications: every bond-market reservation about the post-ceasefire regime has been walked back. Fed stasis is the consensus path. The bifurcation thesis is validated. The war-inflation shock is contained to March goods/energy. The 30Y at 4.899% with MOVE at 67.94 is the classic ‘accept the level, compress the volatility’ pattern that precedes sustained risk asset rallies. If MOVE holds sub-73.21 for multiple sessions, the post-Wednesday-thrust regime is fully locked in and the April 29 Powell press conference becomes the next major catalyst (now two weeks away).

ES 7,067.75 — Third Consecutive War High. +2.7% Above Pre-War Baseline. The Cleanest Equity Re-Rating Of The Conflict.

ES at 7,067.75 extends Wednesday’s 7,007.75 by +60 points / +0.86%. Cumulative recovery from the Day 22 low is now ~+617 points / +8.8% in 13 sessions. The pre-war 6,881.62 baseline is now 186 points below. The equity market has fully recovered the war drawdown AND extended 2.7% into new territory — and is doing so on the back of: Philly Fed 26.7 blowout, Claims 207K beat, TSMC record Q1, TRV massive beat, eight consecutive bank earnings beats, MSFT-led software reflation, TSLA +7.62% on Musk AI5/AI6, AAPL breaking three-session weakness streak, MOVE crash below pre-war baseline, COR1M at a new war low 11.05, UK GDP +0.5% blowout. The rally is extraordinarily narrow per COR1M but is supported by individual fundamentals — each of the major movers has a specific catalyst. Breadth metrics from Tuesday’s Quiggle data (S5TW 72.80, S5FD 89.40, S5FI 61.30, S5TH 70.10) remain supportive. The Russell 2000 −0.01% consolidation reflects small-cap positioning rather than broad weakness.

COR1M 11.05 — NEW WAR LOW. SKEW 139.23 Compressing Further (−7.14%). The Narrow Leadership Is Fundamentally Driven.

COR1M broke through Tuesday’s 12.39 and Wednesday’s 11.58 to print 11.05 today — a NEW war low and the lowest 1-month implied correlation print of the entire conflict by a wide margin. The pre-war baseline was ~22; today’s 11.05 is exactly HALF the pre-war level. Correlation this low means every name is moving on its own story and macro headlines have no weight in the session. SKEW at 139.23 (−7.14%) COMPRESSED sharply — the tail-hedging Tuesday/Wednesday is being fully released into today’s continuation higher. VVIX +2.36% at 97.65 (volatility-of-volatility ticking up modestly) is the only tail-side concern — but the combination of low VIX + low COR1M + compressing SKEW + MOVE crash is the cleanest possible ‘sustained rally with fundamental support’ configuration in the cross-asset complex.

WTI $91.53 — Holding Range. Hormuz Blockade Enters 48 Hours Operational. Energy Sector Decoupling Resolved To Tracking Mode.

WTI at $91.53 (+0.26%) holding within the post-Tuesday range. Cumulative from pre-war $67.02 is +$24.51 / +36.6% (stable). Brent +0.86% at $95.75. Heating oil +1.48% — winter end but mixed. Natural gas +0.54%. CENTCOM reports the Hormuz blockade is being enforced with ‘no breaches in 48 hours’ — operational and active, but Iran has not engaged US destroyers in the strait. The energy complex has effectively priced the blockade as operational-not-kinetic. Notably, XLE at −0.34% on WTI +0.26% — this is the CLOSEST alignment between energy equities and crude since Day 26. The sector-equity decoupling that widened to −2.03%/+0.35% on Wednesday has resolved to tracking mode today. However, the Quiggle data still shows XOP MNTM −40 and XLE MNTM −48 — the structural energy de-rating remains intact even as day-to-day price action tracks crude.

DXY 98.015 Modestly Bid — Below 100 Sustained. BTC $74,935 New Multi-Day High Range. Gold $4,838.50 Steady.

DXY at 98.015 modestly bid (+0.14%) but firmly below the psychological 100 level. Cumulative DXY from pre-war 97.565 is +0.45 / +0.5% — essentially flat over 35 trading days. BTC at $74,935 (−0.32%) holding above $74K and now essentially at a 25%+ war-to-date gain from the ~$59,800 pre-war level. Gold at $4,838.50 (+0.31%) consolidating — still −8.9% from the pre-war $5,311.60 high. Silver at $79.655 essentially flat. Platinum $2,151.50 (+0.99%) and Palladium $1,594.50 (+0.38%) both bid — the platinum group metals are catching an industrial-reflation bid that Copper confirms (Copper rank 5 in Quiggle with MNTM 36).

6. THE GAME PLAN

Today’s Key Events: Philly Fed April 26.7 vs 10.3 consensus (MASSIVE beat, already released). Claims 207K vs 213K (beat, already released). UK GDP +0.5% vs +0.1% consensus (blowout, 2 AM). TSMC Q1 record +58% YoY profit (overnight, 2% stock bid). Travelers Q1 EPS $7.71 vs $6.82 (massive beat, +333% YoY net income). NFLX Q1 AFTER CLOSE — the session’s largest remaining catalyst. ABT pre-market. FRIDAY — Waller Fed speech, regional banks, Housing Starts. MON APR 21 — UNH (not today — DYRH error). APR 22 — Ceasefire formal expiration. APR 24 — First post-tariff Claims signal. APR 28-29 — FOMC.

The Bull Case:

ES at 7,067.75 is the THIRD CONSECUTIVE WAR HIGH. +2.7% above pre-war baseline. +8.8% cumulative recovery from Day 22 low in 13 sessions. MOVE at 67.94 is the FIRST SUB-PRE-WAR-BASELINE PRINT OF THE ENTIRE WAR — bond market capitulation. Philly Fed April 26.7 vs 10.3 consensus = +16.4 upside surprise, highest since September 2025. Combined with Empire State +11.0 yesterday = perfect two-for-two April regional manufacturing blowouts. Claims 207K vs 213K = labor market structurally tight. UK GDP +0.5% vs +0.1% = 5x upside surprise on global growth. TSMC Q1 record +58% YoY profit on AI demand. Travelers Q1 massive beat (core EPS $7.71 vs $6.82, +333% YoY net income). EIGHT consecutive financial earnings beats this week (GS+JPM+WFC+BLK+C+BAC+MS+TRV). TSLA +7.62% on Musk AI5/AI6 + UBS upgrade. MSFT +4.61% extending software reflation. AAPL +2.94% breaking three-session weakness streak. Mag 7 six green / one red with TSLA-led rotation. SOXX steady ahead of TSMC call. FINX +4.12% fintech bid. CIBR +2.76% cyber recovery. The Quiggle data shows $SPY at rank 1 with MNTM 48 (highest in data set) and $XLK now at rank 1 sector with MNTM 48 — structural US tech leadership. $KCE at rank 1 industry with MNTM 50. COR1M at 11.05 = new war low (half the pre-war level). SKEW compressing −7.14%. USMV-SPHB −0.68% (fourth consecutive risk-on session). The corporate fundamentals + economic data + bond-vol capitulation layer is delivering the cleanest possible ‘regime change confirmed’ configuration of the entire war.

The Bear Case:

The COR1M at 11.05 is extreme dispersion — when correlations collapse this far, a single-name leadership break can produce outsized index downside. Mag 7 dispersion at 783 bp (TSLA +7.62% to AMZN −0.21%) is widest of the week. TSLA’s +7.62% pre-market is a 9-month gain maximum — positioning unwind risk is elevated if any TSLA-specific catalyst disappoints (Q1 earnings April 22). MOVE at 67.94 is compressed to an extreme — any catalyst-driven re-expansion could snap back sharply. VVIX +2.36% at 97.65 — vol-of-vol ticking up despite VIX holding at 18.25 is a subtle tail-hedging signal. XLB −1.21% and XLI −1.25% in pre-market — materials and industrials unwinding suggests cyclical positioning is rotating rather than broadly risk-on. Small-caps (Russell) consolidating while large-caps extend — size-factor divergence. CENTCOM confirmed Hormuz blockade enforcement continues at 48 hours — the structural war overhang remains operationally active even as markets price through it. April 22 ceasefire formal expiration is six days away. April 24 first post-tariff Claims signal is eight days away. FOMC April 28-29 with Powell press April 29 is two weeks away — Powell could disappoint on the dovish framework even with the data cover. Waller (a hawkish-tilting FOMC member) speaks Friday — any hawkish commentary could walk back the MOVE capitulation. NFLX after close is the session’s largest single-name event risk — a disappointing print could crack the narrow leadership narrative. The XOP MNTM −40 and XLE MNTM −48 readings in the Quiggle data tell you the energy sector is in structural de-rating — if the broader market’s demand-destruction pricing begins to broaden beyond energy, the re-rating thesis is at risk.

Regime: Steepener Twist — Neutral / Consolidating — Energy Steady. Four regimes operating in parallel. The Philly Fed blowout + Claims beat + TSMC record + TRV beat + TSLA surge + MOVE sub-baseline = the cleanest data, earnings, and cross-asset configuration of the entire war. The bond market has capitulated. The equity market is at a third consecutive war high. Correlations are at a war low. Curves are in a classic twist. The rally is narrow but fundamentally supported. NFLX after close is the next binary. Waller Friday is the Fed communication catalyst. April 22 ceasefire expiration is ceremonial. April 29 Powell press is the real Fed event. The post-Wednesday-thrust regime call from Day 29 is now structurally on — MOVE crossing below pre-war baseline is the formal confirmation.

Watch List

NFLX Q1 Earnings After Close — Session’s Largest Single-Name Event Risk

Netflix reports Q1 after the close. This is the first true pure-play Mag 7-adjacent tech name in the week’s earnings cycle. NFLX is a component of XLC (which is rank 4 sector in Quiggle with MNTM 49). A disappointing print could crack the narrow-leadership support that COR1M at 11.05 says is fundamentally driven. A beat with strong subscriber growth reinforces the software reflation narrative and extends the Mag 7 rotation. Street consensus: ~$4.51 EPS, ~$10.5B revenue, with subscriber adds the key variable.

TSMC Conference Call — Q2 Guidance And Capex Revision

TSMC’s official Q1 call at 2 AM already delivered record numbers but Q2 guidance and any capex revision to the $52-56B range will move every semi equipment name (ASML, AMAT, LRCX, KLAC). The pre-market SOXX at +0.15% is essentially flat because the blowout was already priced in via the March monthly revenue release. Guidance is the real catalyst.

Friday Waller Speech — First Fed Communication Post-Data-Blowout

Waller speaks at 2 PM Friday. As a hawkish-tilting FOMC member, his interpretation of the Philly Fed blowout + Claims beat + ongoing war-inflation-expectations backdrop will signal Fed internal consensus positioning into the April 29 meeting. A dovish Waller locks in the MOVE capitulation. A hawkish Waller walks it back. The highest-probability outcome is Fed ‘data-dependent’ with preserved optionality — but Waller has surprised with hawkishness at key moments historically.

NFLX + TSMC Read-Through To Mag 7 Dispersion Resolution

If TSMC beats post-call and NFLX delivers after close, the Mag 7 dispersion at 783 bp could compress as laggards (AMZN, META from low bases, or GOOG) catch bids into Friday’s close. If either disappoints, the narrow leadership breaks and COR1M at 11.05 becomes a tail-risk indicator rather than a constructive read.

April 22 Ceasefire Formal Expiration — Six Days Away

The two-week ceasefire framework formally expires next Wednesday. De facto dead since April 12 Islamabad collapse, but any formal Iranian or US announcement on the date itself could re-introduce risk premium. The pre-market for next Wednesday is the first binary of next week. MOVE sub-baseline means the bond market is not pricing material risk premium for this — any re-expansion would be a signal.

April 24 First Post-Tariff Claims Release — Eight Days Away

Next Thursday’s Claims print (week ending April 19) is the first release that could plausibly contain tariff-driven layoff filings. The 207K baseline today gives the labor market maximum runway. Watch for the 4-week moving average to remain below 210K — if it breaks above, the post-Wednesday-thrust regime shifts from structural to cyclical.

Morning check: Day 49. Three regimes in parallel for the fourth consecutive session: ES at third consecutive war high (7,067.75), MOVE crashed to first sub-pre-war-baseline print of the entire war (67.94, −8.62%), COR1M at new war low (11.05). The bond market has capitulated. Philly Fed April 26.7 vs 10.3 consensus = +16.4 upside surprise, highest since September 2025. Combined with Empire State +11.0 yesterday = perfect two-for-two April regional manufacturing blowouts. Claims 207K vs 213K consensus = labor market structurally tight with no tariff drag yet. UK GDP +0.5% vs +0.1% = global growth re-accelerating in sync. TSMC Q1 record +58.3% YoY profit. Travelers Q1 core EPS $7.71 vs $6.82 with net income +333% YoY. EIGHT consecutive financial earnings beats this week. TSLA +7.62% on Musk AI5/AI6 + UBS upgrade. MSFT +4.61% extending software reflation. AAPL +2.94% breaking three-session weakness streak. The Quiggle data shows $XLK now at #1 sector (dethroning XLRE) with MNTM 48, $KCE at #1 industry with MNTM 50, and $SPY at #1 asset class with MNTM 48 — structural US tech and financials leadership captured. Factor tape is 6/12 green but USMV-SPHB spread −0.68% (fourth consecutive risk-on session). FINX +4.12%, CIBR +2.76% (recovery), ARKW +3.81%. The post-Wednesday-thrust regime call from Day 29 is now structurally confirmed. Take the rally. MOVE sub-baseline is the formal declaration the war’s rates-vol shock is over. But watch NFLX after close, watch Waller Friday, watch the April 22 ceasefire expiration, watch the April 24 post-tariff Claims print. The setup is the cleanest of the war, and the forward catalysts remain. The market has priced the bifurcation thesis fully; anything that contradicts it (hot PCE on April 30, NFLX miss, Iran escalation) would produce outsized reversal given how compressed the vol complex is.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.