☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

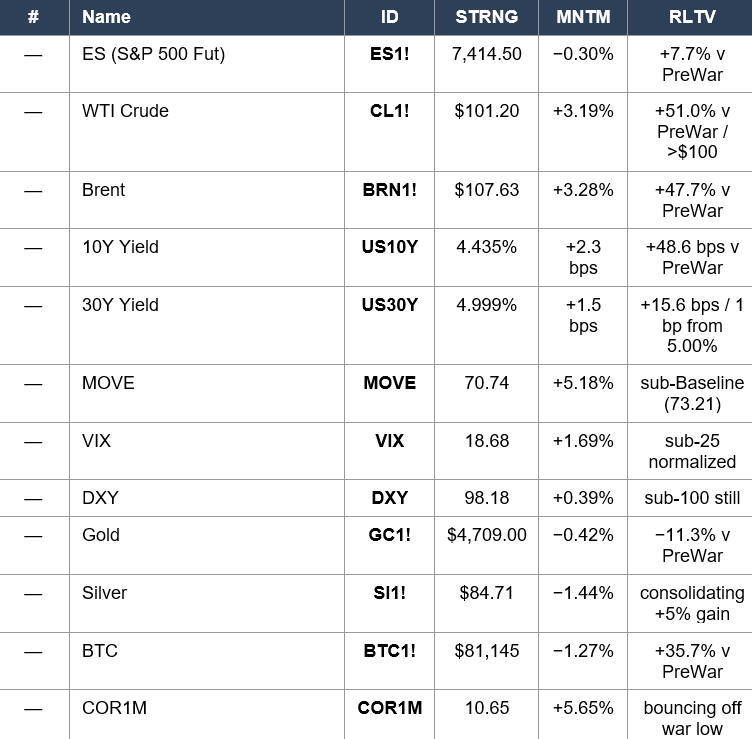

Overnight Tape Summary: CPI PRINTED HOT. CORE CPI 0.4% VS 0.3% CONSENSUS — BEAT (HOTTEST CORE READING OF THE WAR SERIES). HEADLINE CPI 0.6% INLINE. YOY 3.8% VS 3.7% — BEAT, THE HIGHEST ANNUAL CPI READING SINCE 2022. WTI CROSSED $100 — $101.20 (+3.19%) FOR THE FIRST TIME IN WEEKS. BRENT $107.63 (+3.28%). MOVE BOUNCED OFF YESTERDAY’S WAR LOW: 67.25 → 70.74 (+5.18%) — RATES VOL RE-ENGAGING. 30Y AT 4.999% — ONE BASIS POINT FROM THE 5.00% CRISIS THRESHOLD. ES 7,414.50 (−0.30%). MAG 7 SPLIT: TSLA +3.89%, NVDA +1.97% LEAD; GOOG −2.59%, META −1.77%, AMZN −1.35%, MSFT −0.59%, AAPL −0.22%. XLE +2.64% PRE-MARKET LEADS — OIL BID FINALLY REACHING ENERGY EQUITIES. 34 MACRO MONDAY CLOSE: XLK STRNG 85 (NEW WAR HIGH), SMH STRNG 82 (NEW WAR HIGH), XLE RLTV 1.00 RECOVERED TO BASELINE. WARSH SENATE CONFIRMATION VOTE 11:59 AM TODAY. WARSH SWORN IN FRIDAY MAY 15.

Three releases at 8:30 AM defined the morning. Core CPI rose 0.4% month-over-month — a beat of 0.1% versus the 0.3% consensus and double the prior month’s 0.2%. On an annualized basis the core impulse is approximately 4.8% — the hottest single-month core reading of the entire 75-day war. Headline CPI printed 0.6% m/m inline with consensus, decelerating from the 0.9% March print but still elevated. The YoY headline came in at 3.8% versus a 3.7% consensus and 3.3% prior — the highest annual CPI reading since 2022 and a clean above-consensus surprise. Combined, the trio reads as: gasoline / headline pass-through moderating but services and shelter core re-accelerating. This is not a hot-energy print disguising soft underlying inflation — it is the opposite, hot underlying inflation even as the gasoline tail begins to fade. Fed math is unambiguous: today’s core CPI removes any operative case for a near-term cut and validates the hawkish FOMC dissenters (Hammack, Kashkari, Logan) who pushed to remove the easing bias on the May 6 meeting.

And then the oil tape detonated. WTI gapped above $100 to $101.20 — a +$3.13 / +3.19% session, the strongest single-session WTI move in over a week and a CRITICAL TECHNICAL DEVELOPMENT. WTI last sat above $100 on Day 48 (April 29), in the heart of the FOMC-fracture rates crisis. The Sunday Iran rejection lit the fuse; the Monday session held the $97 zone; this morning crude blew through the round number on conviction. Brent confirmed at $107.63 (+3.28%) — well above the century. Heating Oil +2.65%, RBOB +2.40%. The petroleum complex is bid on the diplomatic stall + the threat of escalation that the failed Pakistan-mediated counter-proposal implies. Now, with WTI back to $101 and CPI hot, the inflation transmission channel is fully live, and the bond market is being asked to choose: maintain Monday’s war-low MOVE complacency, or re-price the regime.

The rates response is unambiguous. MOVE jumped +3.48 points (+5.18%) to 70.74 — bouncing off yesterday’s 67.25 war low with the largest single-session expansion since Day 47. The MOVE remains below the 73.21 pre-war baseline (−2.48 points) but the trajectory has reversed. 30Y yield rose +1.5 bps to 4.999% — ONE BASIS POINT FROM THE 5.00% CRISIS THRESHOLD that was last breached on Day 47-48 during the FOMC-fracture rates crisis. The 30Y at 4.999% with MOVE bouncing is the most important technical configuration in markets today. If the 30Y crosses 5.00% on a sustained basis during the cash session, the bond crisis framework re-engages and the equity multiple expansion of the past two weeks unwinds. If 5.00% holds as resistance, today’s repricing is contained. The curve is in a Bear Flattener: 2Y +2.6 bps to 3.977%, 5Y +1.9 bps to 4.092%, 10Y +2.3 bps to 4.435%, 30Y +1.5 bps to 4.999%.

Equities are absorbing the test with characteristic dispersion. ES 7,414.50 (−0.30%) is modestly red — the war-high premium at +7.7% above pre-war 6,881.62 is holding. NQ −0.69% is heavier, reflecting Mag 7 weakness. RUT −0.48% — small caps are under pressure as the front-end yield rise removes cut-pricing. Europe is heavier: DAX −1.09%, EuroStoxx −0.99% — the strong-dollar / hot-US-inflation combination tightening EU financial conditions. The Mag 7 internal tape is the key signal: TSLA $445 (+3.89%) leading — Tesla now above the post-earnings $430 zone with structural momentum. NVDA $219 (+1.97%) extending the semis bid. But everything else is heavy: GOOG −2.59% as the largest Mag 7 drag, META −1.77%, AMZN −1.35%, MSFT −0.59%, AAPL −0.22%. Five of seven red on a hot CPI — the AI-capex-burden trio (META / MSFT / AMZN) plus GOOG and AAPL absorbing the multiple compression on the long end of the rates move. TSLA and NVDA are the only Mag 7 names with enough single-name momentum to override the macro tape.

The 34 Macro Monday-close data (captured at 5:20 PM ET) confirms the equity complex CONTINUED to extend even as the Iran rejection / oil shock unfolded. XLK Technology at STRNG 85 / MNTM +24 / RLTV 1.16 is a NEW WAR HIGH for sector leadership strength (eclipsing Friday’s 84). SMH Semiconductor at STRNG 82 / MNTM +42 / RLTV 1.33 is a NEW WAR HIGH for industry-level strength (eclipsing Friday’s 81 and the prior peak 81). SPY baseline at STRNG 76 / MNTM +7 / RLTV 1.00 — up from Friday’s 75. The CRITICAL development buried in Monday’s data: XLE Energy RLTV recovered to 1.00 EXACTLY, after sitting sub-baseline for two sessions — the war’s most consistent leadership trade has begun reasserting alongside the oil move. IHI Medical Devices at STRNG 24 / RLTV 0.77 is a NEW WAR LOW for the entire industry universe.

The Number That Matters: 30Y At 4.999% — One Basis Point From The 5.00% Crisis Threshold. With Core CPI Beat (0.4%), Headline YoY At Highest Since 2022 (3.8%), And WTI Above $100 — The Inflation Transmission Channel Is Fully Live. The Bond Market Has To Choose: Hold The 5.00% Resistance Or Break It And Re-Engage The Day 47-48 Rates Crisis Framework.

This is the day the data tested the rates complex’s war-low complacency. MOVE at 67.25 on Monday was the cleanest “structural all-clear” reading of the war. Twenty-four hours later, with hot CPI and $101 oil, MOVE has bounced 5.18% and the 30Y is staring at the 5.00% threshold. The bond market’s capacity to absorb both an inflation surprise AND an oil shock simultaneously is being tested in real time. The Warsh Senate confirmation vote at 11:59 AM — exactly three and a half hours after CPI printed — drops directly into this configuration. Friday’s Warsh swearing-in is now arriving with the inflation regime re-engaged and the oil shock at $100+.

The Setup: Bear Flattener — Hot Core CPI + $100 Oil — 30Y One BPS From The Crisis Threshold. ES Holds The War-High Premium. Tech/Semis At War-High STRNG. XLE Recovering To Baseline. Mag 7 Split: TSLA/NVDA Lead, Everything Else Heavy. Warsh Senate Confirmation Vote 11:59 AM. Warsh Sworn In Friday Day 78.

2. OVERNIGHT SESSION RECAP

Asia — Nikkei Heavy Continues

Nikkei 62,575 (−0.60%) is down for a second consecutive session — Monday’s −1.59% has extended. The yen at −0.23% despite a strengthening dollar is the recurring carry-trade unwind signal — the JPY-DXY relationship has broken from typical correlation patterns since the Iran rejection. TOPIX +0.13% — broader Japan held; the weakness is once again concentrated in cap-weighted Nikkei tech and exporter names. AAXJ at Monday close STRNG 74 / RLTV 1.08 — Asia ex-Japan leadership intact. China FXI at STRNG 59 / RLTV 0.89 — the China complex is improving incrementally but remains in the Middle. The Asia tape ahead of the cash open is muted-to-negative.

Europe — Heavy Session On Strong Dollar + Hot CPI Front-Running

DAX 24,146 (−1.09%) and EuroStoxx 50 5,877 (−0.99%) — Europe is the heaviest international tape this morning. The European weakness is being driven by (1) the dollar bouncing to DXY 98.18 (+0.39%) — a +0.34 move from yesterday is a meaningful FX tightening for export-heavy DAX names; (2) the broader hot-CPI front-running ahead of the US 8:30 release; and (3) European energy-equity exposure to a $107 Brent print that hits European industrial input costs harder than US equivalents. The EUR fell to 1.1762 (−0.28%). GBP plunged −0.73% — the largest G10 currency move of the morning, reflecting BoE positioning ahead of summer cuts. The European session is delivering the cleanest “US hot inflation = global tightening” read.

US Pre-Market — Modest Red, Heavy Internal Dispersion

ES 7,414.50 (−0.30%, −22 pts) is essentially the same level as yesterday’s pre-market (7,412) — the cumulative two-day move is approximately flat despite Sunday’s Iran rejection and today’s hot CPI. The market’s capacity to hold +7.7% above pre-war through both events is the key behavioral signal. NQ −0.69% is heavier on Mag 7 weakness. RUT −0.48% reflects the small-cap rate-sensitivity drag. Dow −0.02% effectively flat. Yields rose across the curve into the data and held the move post-print. The session set-up is asymmetric: hot CPI was the bearish-tail event, and yet the ES drawdown is bounded; if the 11:59 AM Warsh vote passes cleanly and the 30Y holds the 5.00% line, today is a “buy the dip on hot CPI” session rather than a regime break.

Mag 7 Pre-Market — TSLA / NVDA Lead, Everything Else Heavy

TSLA $445.00 (+3.89%) is the standout — Tesla now above the post-earnings $430 zone with conviction, putting the cumulative move from last week’s $400 level at approximately +11%. The Tesla strength is now a structural single-name story that’s overriding the macro tape. NVDA $219 (+1.97%) extending Friday’s and Monday’s rallies as semis remain the strongest single-industry complex. GOOG $386.77 (−2.59%) — the day’s largest Mag 7 drag, reflecting both the long-end yield move pressuring Google’s multiple AND specific antitrust / regulatory commentary that’s been swirling. META $598.86 (−1.77%) continuing the capex-overhang theme. AMZN $269 (−1.35%), MSFT $412.66 (−0.59%), AAPL $292.68 (−0.22%) — the AI-capex-burden cohort plus AAPL absorbing the rate move. Aggregate Mag 7 weighting: 5 red / 2 green. The internal rotation is the cleanest possible “single-name momentum vs macro multiple compression” split: TSLA and NVDA have enough demand-thesis traction to override; everyone else absorbs the rate move.

Sector Snapshot — XLE Finally Catches The Oil Bid

The pre-market sector tape is the inverse of recent days: XLE +2.64% leading on the oil shock — energy equities finally tracking crude higher after weeks of decoupling. XLK +1.34% extending Monday’s war-high STRNG print. XLB +1.30%, XLI +1.06% — cyclicals participating with the inflation reflation read. XLU +0.94% — utilities bounced on the rate-sensitive bid even with yields rising (counterintuitive but consistent with the deep-laggard mean reversion). XLY −0.69% (consumer discretionary heavy on the rate move), XLP −0.96% (staples slipping further), XLC −1.16% (communications heaviest on GOOG’s −2.59% drag). The 6/11 green / 5 red split is more constructive than the headline ES move suggests — energy and cyclicals are participating where the AI-capex names are dragging.

Factors — MTUM / VLUE Lead, USMV Flat

MTUM Momentum +1.61%, VLUE Value +1.42% — the same Value-and-Momentum co-leadership as Monday, though at smaller magnitudes (Monday was +4.45% / +2.68%). SPHB High-Beta +0.45% — modest, the high-beta cohort is digesting Monday’s +2.08% surge. USMV Min-Vol +0.07% essentially flat. SPLV Low-Vol +0.04% flat. The USMV−SPHB spread is now −0.38% (vs Monday’s −2.34%) — still negative (risk-on) but compressed dramatically. The factor tape is consolidating Monday’s rotation rather than extending it. IJR Small-Cap −0.72% — the rate-sensitive small-cap cohort is the weakest size factor on the curve move.

Energy & Metals — Petroleum Explodes, Silver Pauses, Gold Holds

WTI $101.20 (+3.19%) is the morning’s commodity headline — the first $100+ WTI print since Day 48. Cumulative from pre-war: +$34.18, +51.0%. Brent $107.63 (+3.28%) — comfortably above the century. The entire petroleum complex is bid: Heating Oil +2.65%, RBOB +2.40%. Natural Gas −1.00% is the lone weakness. Metals are taking a pause after Monday’s rip: Silver $84.71 (−1.44%) consolidating the +5% two-session gain. Gold $4,709 (−0.42%) holding the $4,700 zone. Copper $6.48 (+0.37%) marginally up. Palladium −1.15%, Platinum −0.16%. The metals consolidation alongside the petroleum surge is the cleanest possible “energy-led inflation tail” configuration — the metals bid that powered the post-NFP rally has paused as the oil shock takes the inflation baton.

3. THE PRIOR DAY’S REGIME

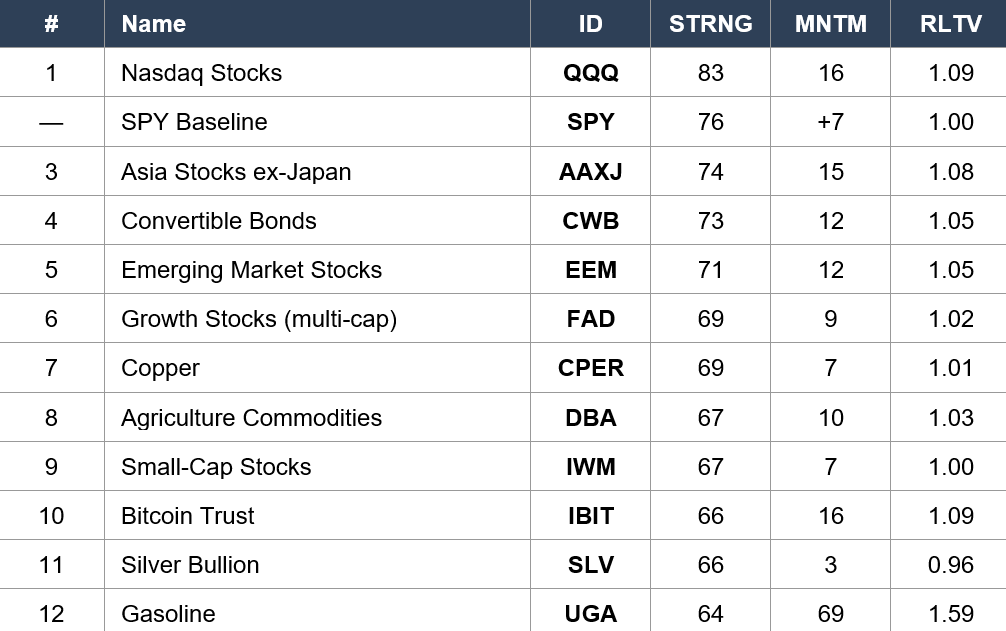

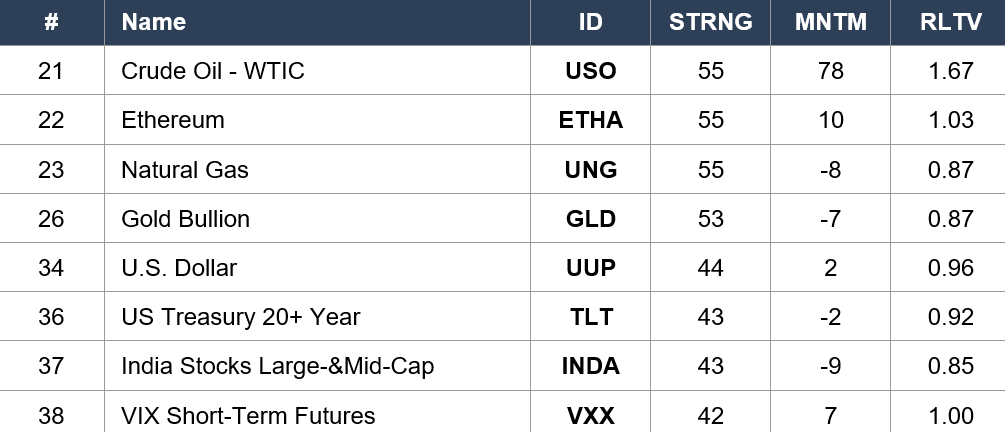

34 Macro Price, Strength & Momentum Rankings — Daily Close, Monday May 11. SPY Baseline: STRNG 76 | MNTM +7 | RLTV 1.00.

Asset Classes — Leaders

Asset Classes — Oil Re-Engaging / Bonds Lagging / Vol Tail

Regime signal: THE EQUITY COMPLEX EXTENDED ITS STRENGTH AND THE COMMODITY/CRYPTO LEADERS RE-EMERGED. SPY baseline rose to STRNG 76 (from Friday’s 75) — the broad market embraced the post-NFP regime even as the Iran rejection / oil shock developed. QQQ held the war high at STRNG 83 / RLTV 1.09. Copper (CPER) jumped to rank #7 at STRNG 69 / RLTV 1.01 — copper has now sustained Leaders-tier strength for three sessions, the cleanest “global demand resilience” signal of the war. Agriculture (DBA) jumped from rank #14 to #8 at STRNG 67 / RLTV 1.03 — the soft-commodity inflation tail is structurally bid. Bitcoin (IBIT) STRNG 66 / RLTV 1.09 — up from Friday’s 62/1.07, crypto is re-extending. Silver (SLV) STRNG 66 / RLTV 0.96 — a massive +7 STRNG jump from Friday’s 59 reflects the +5%-in-two-sessions silver rally. The Middle tier signals the regime test: USO Crude STRNG 55 / RLTV 1.67 — RLTV expanded back from 1.62 to 1.67 reflecting the oil resurgence in front-month positioning; Natural Gas (UNG) jumped from STRNG 44 to 55 (+11) — gas catching the petroleum complex bid. The bond complex remains the war’s most consistent lagger: TLT STRNG 43, IEF STRNG 43, SHY STRNG 42 — bottom-five entrenched. VXX at STRNG 42 / RLTV 1.00 — VXX RLTV touched baseline for the first time in two weeks, fear is showing modest signs of re-engagement.

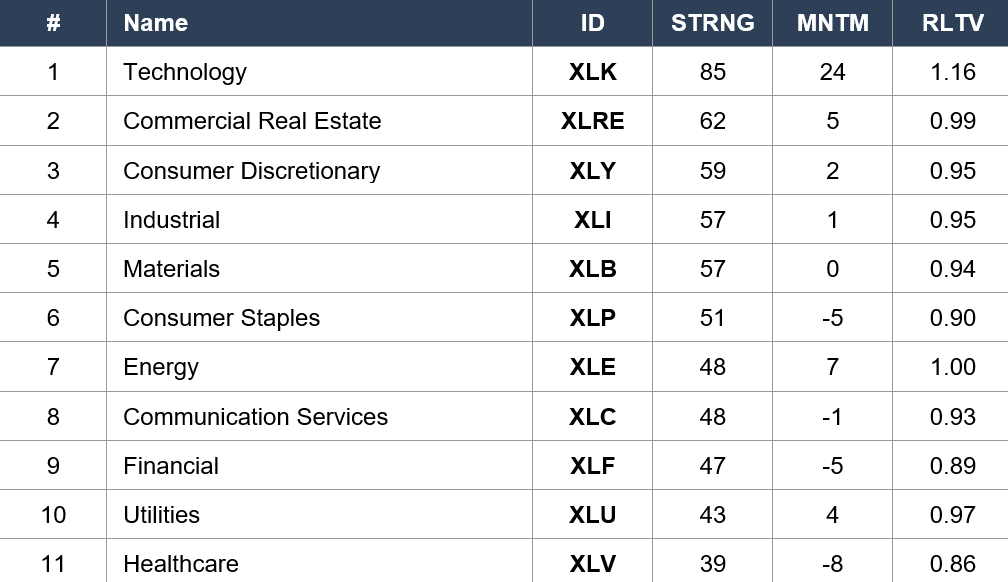

Sector ETFs

Regime signal: XLK NOTCHED A NEW WAR HIGH AT STRNG 85 / RLTV 1.16 — the +1 STRNG move from Friday extends the tech leadership for a fourth consecutive day. The CRITICAL Energy development: XLE jumped from STRNG 41 / RLTV 0.98 (Friday) to STRNG 48 / RLTV 1.00 (Monday) — a +7 STRNG point move and RLTV recovery back to baseline EXACTLY. The “Energy Phoenix” trade that I declared over four sessions ago has begun reasserting alongside the oil shock; the war’s most consistent leadership trade is not dead, it was sidelined. If today’s pre-market XLE +2.64% holds into the close, XLE could re-enter the Leaders tier within 2-3 sessions. XLRE Real Estate at #2 (STRNG 62 / RLTV 0.99) — REITs strong even as rates rise, a notable counter-trend. The MAJOR development on the defensive side: XLP Consumer Staples FELL from STRNG 57 to 51 (−6), XLC Communications cracked from STRNG 55 to 48 (−7), XLV Health-Care fell from STRNG 40 to 39 — defensives now occupy 4 of the bottom 5 sector positions. XLV at STRNG 39 / RLTV 0.86 is the deepest sector laggard of the war series — defensive healthcare has broken. The sector tape is now the cleanest possible risk-on + energy-re-emergence configuration.

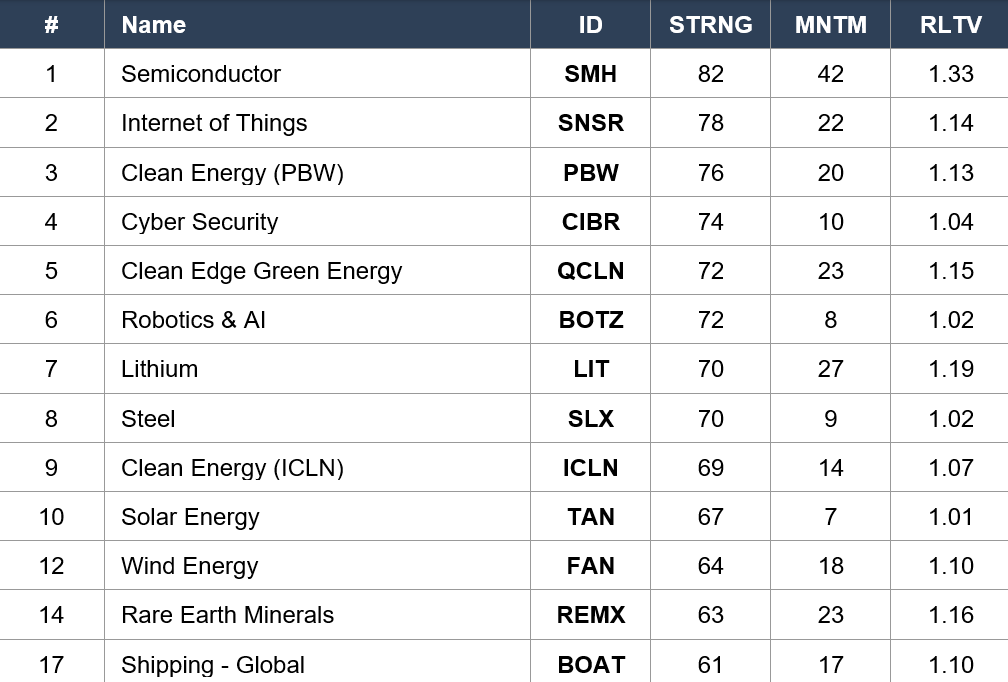

Industry ETFs — Leaders

Industry ETFs — Laggers

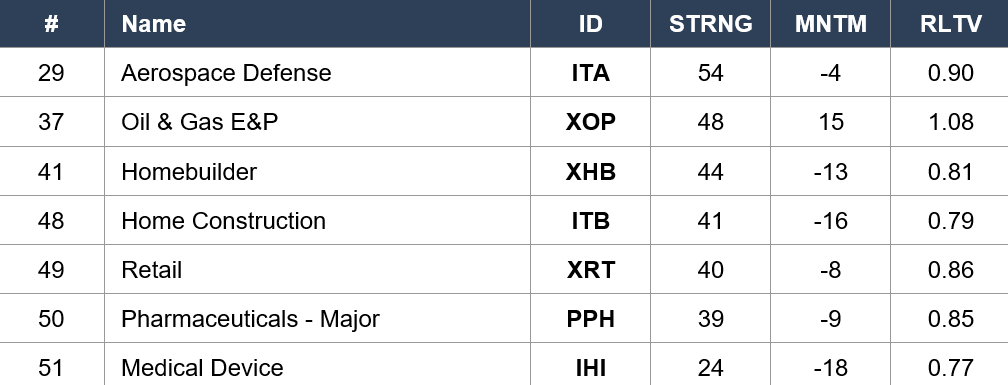

Regime signal: SMH SEMICONDUCTOR HIT A NEW WAR HIGH AT STRNG 82 / MNTM +42 / RLTV 1.33 — surpassing Friday’s 81 and reclaiming the war-high tier. The CLEAN-ENERGY COMPLEX has now fully crystallized as a coherent leading theme: PBW jumped from STRNG 72 to 76 (+4, rank #5 → #3), QCLN STRNG 72 / RLTV 1.15 (rank #5), ICLN STRNG 69 / RLTV 1.07 (rank #9), TAN STRNG 67 / RLTV 1.01 (rank #10), FAN STRNG 64 / RLTV 1.10 (rank #12) — five clean-energy industries all in the Leaders or near-Leaders, all RLTV >1.00. LIT Lithium STRNG 70 / RLTV 1.19 — battery materials commanding RLTV that exceeds the broader complex. REMX Rare Earth STRNG 63 / RLTV 1.16 — China-supply geopolitical hedge bid. The Laggers tell the day’s structural pain: IHI Medical Devices at STRNG 24 / RLTV 0.77 — a NEW WAR LOW for any industry-level strength reading, the deepest single-industry capitulation of the war. PPH Pharma Major STRNG 39 — defensive healthcare across both ETFs (XBI Biotech and PPH Pharma) deteriorating. ITB Home Construction STRNG 41 / RLTV 0.79 — rates-sensitive housing at war lows. XRT Retail STRNG 40 — consumer discretionary retail (specialty / brick-and-mortar) crashing despite the broader XLY at sector rank #3. XOP Upstream Energy at STRNG 48 — the worst-performing energy industry, despite WTI at $101 and Brent at $107. The capital is concentrated in AI/Semis/Clean-Tech/Speculation; healthcare, housing, retail, and defensive cohorts remain deeply lagging.

4. MORNING DATA REACTION

Core CPI m/m — 0.4% (BEAT — Hot, Consensus 0.3%)

April Core CPI rose 0.4% month-over-month, a beat of 0.1% versus consensus and DOUBLE the prior month’s 0.2%. On an annualized basis the core impulse is approximately 4.8% — the hottest single-month core reading of the entire 75-day war. This is the print that recession-callers and Fed-cut-traders did not want to see. With NFP +115K confirming labor resilience last Friday and now core CPI at 0.4%, the FOMC’s dovish dissent (Miran) is functionally isolated and the hawks (Hammack, Kashkari, Logan) have the data wind at their back. The Fed math now points to Warsh inheriting a “no near-term cut” trajectory unless something breaks in Q2 jobs or growth. Watch components: services ex-shelter (the Fed’s preferred core gauge), shelter (any easing from front-end yield falls), and energy contribution as gasoline transmits.

Headline CPI m/m — 0.6% (INLINE, Consensus 0.6%)

The headline 0.6% decelerated from the prior 0.9% — gasoline pass-through is moderating month-over-month. The deceleration is consistent with the April WTI average of $90-95 (vs the March average closer to $100). With WTI back to $101 this morning, the May headline CPI is set to re-accelerate. Today’s headline inline read combined with the hot core beat tells the cleanest possible story: gasoline / headline is the tail, services / shelter / core is the persistent body of inflation pressure. This is exactly the inflation profile that disqualifies a near-term cut while keeping the recession risk subdued.

CPI y/y — 3.8% (BEAT — Hot, Consensus 3.7%)

YoY headline CPI accelerated to 3.8% — the highest annual reading since 2022 and a 0.1% above-consensus surprise. The base-effect math through Q2 keeps this elevated; without a sharp m/m decline in May-June, YoY will print at or above 4.0% by midsummer. For the Warsh FOMC inheriting on Friday, this is the inflation regime variable they need to confront: not whether inflation is “high” by historical standards (it is), but whether it is RE-ACCELERATING. Today’s data is the first month since November 2024 where headline YoY has accelerated by 0.5+ percentage points in a single month.

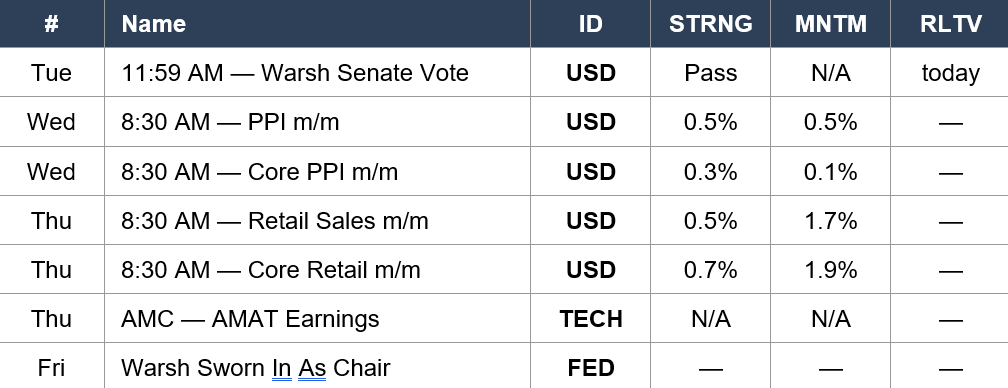

Today 11:59 AM — Warsh Senate Confirmation Vote

The Senate floor vote on Kevin Warsh as Fed Chair is scheduled for 11:59 AM ET (per the DYRH calendar; some sources have it at 12:00 PM). The vote arrives three and a half hours after the hot CPI print — into a market that is now testing the 30Y 5.00% threshold and re-pricing inflation expectations. A clean bipartisan passage (60+ votes) would signal policy continuity and offer modest reassurance to the bond market that the Warsh transition is not adding hawkish risk. A narrow margin (51-49 or close) would signal that even moderate Democrats are concerned about a hawkish Fed lean — and could push the 30Y through 5.00%. Watch the vote count carefully as the cleanest single political-economy read into the Friday handoff.

Coming Up Today & This Week

5. THE DYRH READ

Yield Curve Regime: Bear Flattener

The curve is in a Bear Flattener configuration, with yields rising at every tenor and the front end rising marginally faster than the long end: 2Y +2.6 bps to 3.977%, 5Y +1.9 bps to 4.092%, 10Y +2.3 bps to 4.435%, 30Y +1.5 bps to 4.999%. The 2s/30s spread compressed to 102.2 bps from yesterday’s 105.0 — modest curve compression. The Bear Flattener is consistent with: (1) front-end repricing of cut probability lower on the labor strength + CPI beat combination, (2) long-end repricing of inflation expectations higher on the oil shock + core CPI hot. With the 30Y at 4.999% — within ONE BASIS POINT of the 5.00% crisis threshold that defined the Day 47-48 bond market crisis — every basis point of further 30Y selling is now consequential.

MOVE Index: 70.74 (+5.18%) — Bounced Off War Low

MOVE expanded +3.48 points to 70.74 — bouncing off yesterday’s 67.25 war low with the largest single-session expansion since Day 47. MOVE remains below the 73.21 pre-war baseline (−2.47 points), but the trajectory has reversed sharply. The bond market’s war-low complacency from Monday is being tested today by the hot CPI + $100+ oil combination. If MOVE crosses 73 (pre-war baseline) by Wednesday’s PPI, the rates-vol-driven equity multiple expansion of the past two weeks would unwind. The 67.25 → 70.74 move in one session is the cleanest possible “rates vol re-engages on data + commodity shock” signature. Watch: if MOVE compresses back below 70 during the cash session, today’s data is digested. If MOVE pushes above 72, the regime is reversing.

S&P 500: ES 7,414.50 — War-High Premium Holds Through Both Tests

ES at 7,414.50 (−0.30%, −22 pts) holds +7.7% above pre-war 6,881.62. The market’s ability to maintain the war-high premium THROUGH the weekend Iran rejection AND today’s hot CPI print is the structural signal. Across 75 days the cumulative ES gain is +532.88 points despite an air war, an oil crash and recovery, three Mag 7 capex shocks, the FOMC fracture, the 30Y crossing 5.00%, MOVE at 115.02 war high, GDP miss, Iran ceasefire collapse, weekend rejection, hot CPI, and $101 oil. Every regime test the market has been given, the equity multiple has absorbed and held. The Tuesday Warsh vote, the Wednesday PPI, the Thursday Retail Sales + AMAT, and the Friday Warsh handoff are the remaining tests.

Key Levels & Cumulative War Moves

Volatility & Breadth — Vol Re-Engaging, Breadth Holds

MOVE +5.18% (the headline rates-vol bounce), VXN +4.12% (Nasdaq vol re-engaging on the Mag 7 dispersion), GVZ +3.78% (gold vol expanding alongside gold pause — unusual), VIX +1.69% (modest equity vol bid), VVIX +1.32%. VIX1D −9.29% — the short-vol bid is selling off because today’s event (CPI) is now in the rear view and tomorrow’s PPI is the next pressure point. The vol complex is in clean Wednesday-positioning mode. Breadth holds the Friday read: S5TH 70.10, S5FI 61.30, R2TH 51.20 — no breadth degradation despite the headline weakness. COR1M at 10.65 (+5.65% from yesterday’s 10.08 war low) — correlation bouncing modestly but still in the deepest stock-picker regime of the war. The vol expansion is data-driven; the breadth durability is the cleaner signal that the regime has not broken.

6. THE GAME PLAN

Today: Core CPI 0.4% BEAT (hot), Headline CPI 0.6% inline, YoY 3.8% BEAT (highest since 2022). WTI crossed $100 to $101.20. 30Y at 4.999%. MOVE bounced off war low. Warsh Senate vote 11:59 AM. Wed: PPI 8:30. Thu: Retail Sales 8:30 + AMAT AMC. Fri: Warsh sworn in (Day 78).

The Bull Case

ES 7,414.50 holds +7.7% above pre-war — through Iran rejection AND hot CPI, the war-high premium is intact. MOVE at 70.74 — bounced off war low but still BELOW the 73.21 pre-war baseline; rates vol remains in the structurally normalized zone despite both shocks. 30Y at 4.999% holding the 5.00% line as resistance — the bond market has not yet broken. 34 Macro Monday close: XLK STRNG 85 (NEW WAR HIGH), SMH STRNG 82 (NEW WAR HIGH), SPY baseline up to STRNG 76. XLE RLTV recovered to 1.00 EXACTLY — the war’s most consistent leadership trade is re-emerging alongside the oil shock; the energy reflation pivot is constructive at the macro level even as it pressures CPI. Pre-market XLE +2.64% leading sectors — finally tracking oil. XLK +1.34%, XLB +1.30%, XLI +1.06% — cyclicals and tech participating. TSLA +3.89%, NVDA +1.97% — the AI-revenue Mag 7 names extending. Copper at $6.48 (+0.37%) holding the global-demand-resilience read. The clean-energy complex (PBW +4 STRNG to 76, QCLN, ICLN, TAN, FAN all in Leaders/near-Leaders) is a coherent new leadership theme. Bitcoin (IBIT) STRNG 66 / RLTV 1.09. If the Warsh Senate vote passes broadly at 11:59 AM, the 30Y holds 5.00% as resistance into the close, and PPI Wednesday prints inline or cool — the equity multiple expansion resumes and the Friday Warsh handoff arrives clean.

The Bear Case

Core CPI 0.4% is HOTTER than expected — the cleanest inflation re-acceleration print of the war. YoY 3.8% is the highest since 2022. WTI at $101.20 / +51% from pre-war / first $100+ print in weeks. Brent $107.63. 30Y at 4.999% — ONE BASIS POINT from the 5.00% crisis threshold that defined the Day 47-48 bond market crisis. MOVE bounced +5.18% off yesterday’s war low — the trajectory has reversed. The Mag 7 internal tape is split with 5/7 red and GOOG −2.59%, META −1.77%, AMZN −1.35% — the AI-capex-burden trio plus GOOG dragging. Europe heavy: DAX −1.09%, EuroStoxx −0.99% — the strong-dollar / hot-US-CPI combination is tightening global financial conditions. GBP plunged −0.73%. DXY +0.39% to 98.18. XLP Consumer Staples and XLV Healthcare at sector-rank #6 and #11 — defensives are breaking down at the same time risk metrics are stressed (an asymmetric signal). IHI Medical Devices at STRNG 24 / RLTV 0.77 — NEW WAR LOW. PPH Pharma at STRNG 39. XLV at STRNG 39 — defensive healthcare cracking. The Warsh vote at 11:59 AM is on a narrower-than-comfortable margin risk. Wednesday’s PPI consensus has Core PPI at 0.3% vs 0.1% prior — already pricing a hot expansion; an upside surprise alongside today’s hot core CPI could push the 30Y through 5.00%. Friday’s Warsh handoff arrives into an inflation regime that has just re-accelerated.

Regime: Bear Flattener — Hot Core CPI + $100 Oil — 30Y One BPS From The Crisis Threshold. The day’s defining tension is between the 30Y at 4.999% (the inflation/duration test) and the equity tape’s ability to hold +7.7% above pre-war through both today’s hot CPI AND yesterday’s Iran rejection. The bond market’s war-low MOVE complacency was tested; the response is a +5.18% bounce, but the level remains sub-baseline. The next 48 hours — Warsh vote today, PPI Wednesday — determine whether the multiple compression accelerates or the structural risk-on regime reasserts. Three days to a new Fed chair inheriting a re-engaged inflation read, the first $100+ oil print in weeks, and a 30Y staring at 5.00%.

Watch List

Today 11:59 AM — Warsh Senate Confirmation Vote

The Senate floor vote on Kevin Warsh. Expected to pass per consensus. WATCH THE MARGIN: 65+ votes = broad bipartisan continuity, modest bond-market reassurance; 55-64 = normal partisan party-line passage; 51-54 = narrow margin signals significant Democratic concern about hawkish lean, could push 30Y through 5.00%; failure or delay = regime break. The vote arrives 3.5 hours after the hot CPI print into a 30Y at 4.999%.

Today 30Y Yield — The 5.00% Crisis Threshold

The 30Y at 4.999% is the day’s single most important technical level. Last breached on Day 47 (April 28) during the FOMC-fracture rates crisis, the 5.00% line is the bond market’s “crisis threshold” — a level above which forced-liquidation dynamics and term-premium expansion historically accelerate. If the 30Y holds 5.00% as resistance during the cash session, today’s repricing is contained. If the 30Y breaks above 5.00% and closes above the line, the bond crisis framework re-engages and the equity multiple expansion of the past two weeks unwinds rapidly.

Wednesday 8:30 AM — April PPI / Core PPI + Earnings (CSCO, BABA)

PPI consensus: headline 0.5% m/m (vs 0.5% prior — flat), Core 0.3% m/m (vs 0.1% prior — a 3x acceleration). Given ISM Manufacturing Prices Paid at 84.6 (highest since 2022) and today’s core CPI beat, the consensus PPI estimates may be set too low — particularly on the core. Above 0.5% Core PPI would compound today’s CPI repricing; below 0.2% would provide relief. CSCO (Cisco Systems) reports AMC Wednesday — networking/enterprise tech bellwether, key for the AI-infrastructure thesis. BABA (Alibaba) reports — China consumer and EM consumption read.

Thursday 8:30 AM — April Retail Sales + AMAT Earnings

Retail Sales consensus: 0.5% m/m headline (vs 1.7% prior — significant deceleration expected), Core 0.7% (vs 1.9%). With NFP +115K and today’s hot core CPI in the data, retail sales becomes the consumer-resilience confirmation. AMAT (Applied Materials) reports — semiconductor capital-equipment bellwether and the cleanest AI-capex read given SMH at STRNG 82 / RLTV 1.33 NEW WAR HIGH. AMAT’s commentary on China, foundry orders, and DRAM/NAND capex will define the SOXX trajectory through end of week.

Friday May 15 — Warsh Sworn In (Day 78)

Kevin Warsh takes the Fed chair. He inherits MOVE bouncing (currently 70.74), 30Y at 4.999%, ES at war-high premium, hot core CPI just released, $101 oil, and an FOMC fractured 8-4. The market’s positioning into Friday will be defined by Wednesday PPI and Thursday Retail Sales. Warsh’s first FOMC is June 17-18; his first FOMC dot plot will be the cleanest read on the new hawkish baseline.

Energy — WTI Crosses $100 First Time Since Day 48

WTI at $101.20 is the first $100+ print since April 28 (Day 48), in the heart of the FOMC-fracture rates crisis. Brent $107.63 well above the century. The trajectory: weekend Iran rejection → Monday $97.46 → Tuesday $101.20. If the diplomatic stall continues, $105 is the next technical target; a Hormuz incident sends WTI to $110+ immediately. Watch XLE Energy carefully — Monday’s RLTV recovery to 1.00 + today’s pre-market +2.64% suggests the energy reflation trade is fully back. XLE rank could climb from #7 to #3-#4 in the 34 Macro data within a week if the oil move sustains.

AI/Semis — XLK And SMH Both At New War Highs

XLK Technology STRNG 85 / RLTV 1.16 (new war high). SMH Semiconductor STRNG 82 / MNTM +42 / RLTV 1.33 (new war high). Despite the hot CPI, despite the 30Y at 4.999%, despite the Mag 7 internal dispersion (META / GOOG / AMZN red), the tech and semis complexes are extending leadership at the industry level. Pre-market SOXX +2.39% extending. AMAT Thursday earnings is the catalyst test — a beat keeps the semis complex at war-high tier; a miss or cautious guide could finally compress SMH off its peak. Until then, AI/Semis remains the war’s structural leadership trade.

Morning check: Day 75. The data tested the rates complex’s war-low complacency. April Core CPI printed 0.4% m/m against a 0.3% consensus — a clean beat and the hottest core CPI print of the war series, double the prior month’s 0.2%. Headline CPI 0.6% landed inline, but the YoY accelerated to 3.8% versus a 3.7% consensus and 3.3% prior — the highest annual CPI reading since 2022. The cross-asset response was immediate. WTI gapped above $100 to $101.20 (+3.19%) on the diplomatic stall combined with the inflation read — the first $100+ WTI print since Day 48 in late April. Brent $107.63 above the century. The 30Y rose to 4.999% — ONE BASIS POINT from the 5.00% crisis threshold that defined the Day 47-48 bond market crisis. MOVE expanded +5.18% to 70.74 — bouncing off yesterday’s 67.25 war low with the largest single-session move since Day 47. The Mag 7 split: TSLA $445 (+3.89%) and NVDA $219 (+1.97%) lead, but GOOG −2.59%, META −1.77%, AMZN −1.35%, MSFT −0.59%, AAPL −0.22% — 5 of 7 red, the AI-capex-burden trio plus GOOG dragging. ES 7,414.50 (−0.30%) holds +7.7% above pre-war — the war-high premium is intact through both the weekend Iran rejection AND today’s hot CPI. Pre-market XLE +2.64% finally leading sectors as oil reaches energy equities. The 34 Macro Monday close shows the equity complex at NEW WAR HIGHS: XLK Technology STRNG 85 / RLTV 1.16 (sector war high), SMH Semiconductor STRNG 82 / MNTM +42 / RLTV 1.33 (industry war high), SPY baseline up to STRNG 76. The critical Energy development: XLE RLTV recovered to 1.00 EXACTLY — the war’s most consistent leadership trade is re-emerging alongside the oil shock. IHI Medical Devices at STRNG 24 / RLTV 0.77 — NEW WAR LOW for industry strength. The Warsh Senate confirmation vote drops at 11:59 AM, 3.5 hours after CPI printed, into a 30Y at 4.999%. The next 48 hours — vote today, PPI Wednesday, Retail Sales / AMAT Thursday, Warsh sworn in Friday — determine whether today’s repricing is contained or whether the bond crisis framework re-engages. Through every test, the equity multiple has absorbed and held. Pressure, not panic. Regime, not reaction. The data has spoken; the bond market has its first response. The next move is the vote.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.