☀️THE MORNING BELL

Pre-Market Intelligence Report

1. THE QUICK SCAN

Overnight Tape Summary: NEUTRAL / CONSOLIDATING — ES 7,165.50 (+0.24%). UNH Q1 MASSIVE BEAT: ADJUSTED EPS $7.23 VS $6.61 EST (+9.4% BEAT), REVENUE $111.72B VS $109.8B, MCR 83.9%, RAISED FY26 GUIDANCE TO >$18.25. RETAIL SALES 1.7% VS 1.4% HEADLINE / CORE 1.9% VS 1.4% — MASSIVE CONSUMER BEAT. WARSH FED CHAIR-DESIGNATE CONFIRMATION HEARING 10 AM. CEASEFIRE EXPIRES TONIGHT WITH VANCE IN ISLAMABAD. MOVE 67.90 (+3.36%) BOUNCING BUT STILL SUB-BASELINE. FLATTENER TWIST — FRONT RISING, LONG FALLING. WTI $87.52 STABLE. DOW LEADING +0.48%. MAG 7 TWO GREEN / FIVE RED. FACTOR TAPE RISK-ON (USMV-SPHB −0.78%) WITH SPHB LEADING.

The morning data layer is unambiguously strong. UnitedHealth delivered the most anticipated healthcare earnings print of 2026 before the open: adjusted EPS $7.23 vs $6.61 consensus — a +9.4% beat and $0.58 above estimates. Revenue $111.72B vs $109.8B (+1.7% beat). GAAP EPS $6.90 vs $6.85 prior year. The medical benefit ratio at 83.9% came in BETTER than analyst expectations — UNH is managing medical costs more effectively than feared. Most critically, management RAISED its FY2026 adjusted EPS guidance to more than $18.25 per share, up from the prior >$17.75 — a rare upward revision from a company that had fallen 45.5% over the past year and 15.4% YTD. After the Q4 shock ($2.88B charge, 19.6% single-day drop) and the Q1 2025 miss that triggered a 22% single-day selloff, this print is the validation of the recovery story under new CEO Stephen Hemsley.

Retail Sales at 8:30 AM added fuel: March headline +1.7% vs +1.4% consensus (prior +0.6%) and core +1.9% vs +1.4% consensus (prior +0.5%). The core beat of +0.5 pp is the largest positive core retail surprise of 2026. The consumer is not only absorbing the war’s energy-price shock — it is ACCELERATING spending through it. This is the definitive real-economy datapoint that the bifurcation thesis needed: March gasoline prices spiked +21.2% but March consumer spending BEAT consensus by 50 basis points on the core measure. The stagflation narrative from the March CPI/Michigan shock is being systematically dismantled by the April data sequence: PPI services flat, Empire State +11.0, Philly Fed 26.7, Claims 207K, and now Retail Sales +1.9% core.

The geopolitical backdrop is in maximum tension. The ceasefire formally expires TONIGHT. VP Vance is in Islamabad for last-ditch talks — Iran’s participation remains UNCONFIRMED. The weekend saw the first kinetic engagements of the ceasefire period (Iranian gunboats firing on tankers, US Navy seizing the ‘Touska’). The resolution of tonight’s expiration is the single largest overnight event risk of the entire war. WTI at $87.52 (+0.11%) is remarkably stable given the binary — the oil market appears to be waiting for the Islamabad outcome rather than pricing either extension or collapse.

Kevin Warsh’s Fed Chair-Designate confirmation hearing begins at 10 AM before the Senate Banking Committee — the most significant Fed-governance event since Powell’s nomination. Warsh has called for ‘regime change’ at the Fed. Tillis continues to block passage. Powell’s term expires May 15. Trump has threatened to fire Powell if he stays past his term. The hearing defines market expectations for the Fed’s institutional direction over the next four years.

The Number That Matters: UNH +9.4% EPS Beat + Retail Sales Core +1.9% vs +1.4% — The Consumer And Corporate Fundamentals Layer Is Delivering Into The Most Binary Night Of The War.

The combination of UNH’s raised guidance + Retail Sales blowout provides the cleanest possible ‘activity without demand destruction’ signal heading into tonight’s ceasefire expiration. If Vance secures an extension or framework, the data-plus-de-escalation combination would be the most constructive overnight package since Day 29. If talks collapse, the market enters re-escalation with the strongest corporate/consumer fundamentals backdrop of the entire war — a floor under any selloff.

The Setup: Flattener Twist — Neutral / Consolidating — Energy Steady. MOVE Bouncing (+3.36%) But Still Sub-Baseline (67.90 vs 73.21). Ceasefire Expiration Tonight. Warsh Hearing 10 AM. TSLA Wednesday. GOOGL/MSFT/META Thursday. The Most Concentrated Event Calendar Of The Entire War.

2. OVERNIGHT SESSION RECAP

Monday Cash Session (Day 37 Close)

Monday’s cash session was constructive: ES closed at an implied ~7,148.25 level with the S&P 500 gaining modestly despite the weekend re-escalation fears. The curve settled in a BEAR FLATTENER — 2Y +2.1 bps (front-end hawkish repricing), 10Y +1.0 bps, 30Y +0.2 bps. Energy held its range with XLE tracking crude cleanly. The factor tape completed its rotation from Monday morning’s defensive posture to a mixed close. Monday absorbed the weekend shock and set up for Tuesday’s triple catalyst.

Asia-Pacific

Nikkei −0.25% to 59,150 — Japan soft but more contained than Monday’s −1.14% decline. Topix −0.12%. Asian markets stabilizing after the weekend shock as Vance’s Islamabad arrival provided some diplomatic-cover bid. WTI stability at $87.52 (+0.11%) helped Asian oil-importers.

Europe

DAX +0.29% to 24,663. EuroStoxx 50 +0.25% to 5,947. European markets recovering from Monday’s −1.09% DAX selloff — the European tape is interpreting Vance’s Islamabad presence as credible de-escalation effort. The recovery is measured rather than aggressive, consistent with positioning ahead of tonight’s ceasefire expiration binary.

US Pre-Market

Day 54 of Operation Epic Fury. Q2 Day 15. Tuesday — THE TRIPLE CATALYST DAY. FOMC blackout active.

US FUTURES CONSTRUCTIVE: YM +0.48% leading (Dow outperformance = value/cyclical bid), NQ +0.32%, ES +0.24%, RTY +0.19%. The Dow leading ES for the second consecutive session confirms the rotation FROM narrow Mag 7 tech leadership TO broad value/cyclical. RTY at +0.19% lagging but still green — small-cap bid intact but not leading today.

MAG 7 TWO GREEN / FIVE RED — UNH SURGE ABSORBING MAG 7 WEAKNESS: AAPL +1.04% (second consecutive green day — Apple defensive bid returning). NVDA +0.19%. AMZN −0.91%. MSFT −1.12% (giving back into Thursday’s earnings). GOOG −1.18%. TSLA −2.03% (positioning into Wednesday’s earnings). META −2.56% (positioning into Thursday’s earnings — META now the weakest Mag 7 name over the past 3 sessions). The index is green despite 5/7 Mag 7 red because the BREADTH is carrying: Dow +0.48%, RSP +0.32%, mid-cap +0.63%, small-cap +0.56%. The non-Mag 7 market is rallying on the UNH beat + Retail Sales beat while the Mag 7 consolidates ahead of its earnings prints.

FACTORS RISK-ON WITH HIGH BETA LEADING: SPHB +0.65% leading. IJH +0.63%. IJR +0.56%. RSP +0.32%. USMV −0.13%. SPLV −0.50%. USMV-SPHB spread −0.78% (DEEPLY risk-on — the most negative since last week’s five-session streak). 4/12 factors green but the green names are all risk-seeking (SPHB, IJH, IJR, RSP) while the red names are defensive (USMV, SPLV, MTUM, QUAL). This is a clean risk-on rotation INTO value/small-cap/high-beta.

SECTORS: XLB +0.67% leading (materials bid on industrial-cyclical rotation). XLF +0.38% (UNH read-through: health insurer beat = broader financial-sector confidence). XLRE +0.36%. XLI +0.22%. XLK +0.14%. XLE +0.09% (tracking WTI cleanly at +0.11%). Six sectors green. XLV −0.93% (DESPITE UNH massive beat — the sector is selling the news / positioning for the XLV-at-large read that UNH’s MCR improvement is company-specific rather than sector-wide). XLU −0.89%. XLC −0.29% (META −2.56% drag). XLY −0.45% (TSLA −2.03% drag).

8:30 AM — RETAIL SALES MARCH: HEADLINE +1.7% VS +1.4% CONSENSUS. CORE +1.9% VS +1.4% CONSENSUS. MASSIVE CONSUMER BEAT.

The core retail sales beat of +0.5 pp above consensus is the largest positive core surprise of 2026 and the strongest single-month core print since the war began. March retail sales captured the period of peak war-energy-price pressure (gasoline +21.2% CPI, Michigan sentiment 47.6 all-time low) and STILL delivered a massive upside beat. This tells you the consumer is absorbing the energy shock through savings drawdowns, credit usage, or income growth — but NOT through demand destruction. The bifurcation thesis is now supported by FIVE consecutive data beats (PPI services flat, Empire State +11.0, Philly Fed 26.7, Claims 207K, Retail Sales core +1.9%). The front end of the curve responded by RISING: 2Y +3.1 bps as the market trims Fed-cut probability on the strong activity data. The 30Y fell 0.6 bps — long-end growth pessimism remains, creating the flattener twist.

PRE-MARKET — UNITEDHEALTH Q1 2026: ADJUSTED EPS $7.23 VS $6.61 CONSENSUS (+9.4% BEAT). REVENUE $111.72B VS $109.8B. MCR 83.9%. RAISED FY26 GUIDANCE TO >$18.25 FROM >$17.75.

UNH delivered a clean beat across every metric. The adjusted EPS of $7.23 was $0.58 above the ~$6.61 consensus — a 9.4% upside surprise. Revenue of $111.72B topped the ~$109.8B estimate by $1.9B. The medical benefit ratio at 83.9% is the single most important metric for UNH — it came in better than expected, reflecting strong management of medical costs and the release of reserves for unprofitable contracts. The guidance raise to more than $18.25 adjusted EPS from more than $17.75 is the most bullish signal: management is confident enough in the recovery trajectory to lift targets during the most volatile macro backdrop in UNH’s history. This is the stock that fell 45.5% over the past year, suffered a 22% single-day drop on Q1 2025 earnings, and took a $2.88B Q4 charge. Today’s print validates the recovery under CEO Hemsley. The company also plans at least $2B in buybacks by end of Q2 2026. XLV at −0.93% despite the UNH beat suggests the sector is ‘sell the news’ — the beat may be company-specific (cost management, reserve release) rather than a sector-wide medical cost improvement.

3. THE PRIOR DAY’S REGIME (34 Macro Price, Strength & Momentum Rankings)

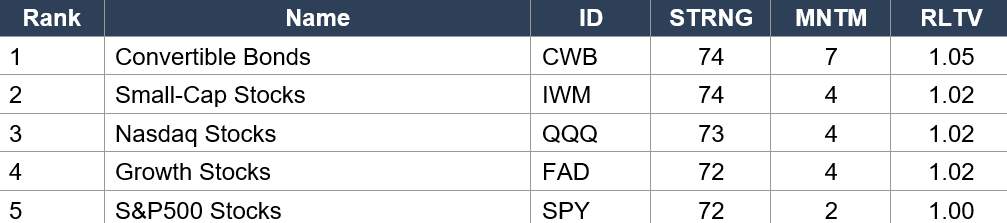

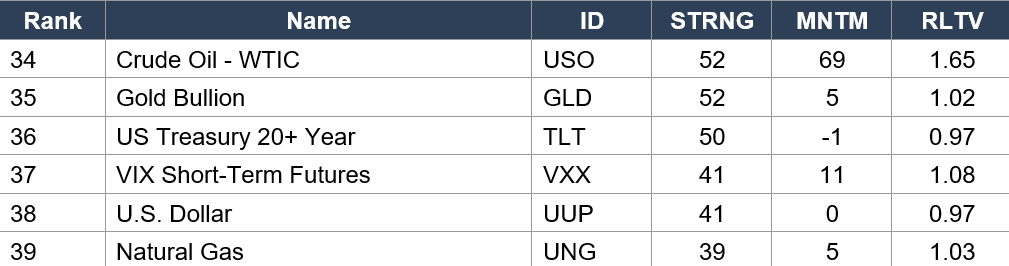

34 Macro Price, Strength & Momentum Rankings — Daily Close, Monday April 20. SPY Baseline: STRNG 72 | MNTM +2 | RLTV 1.00.

Asset Classes — Leaders

Asset Classes — Laggers

Regime signal: THE DATA HAS UNDERGONE A STRUCTURAL ROTATION FROM LAST WEEK. Convertible Bonds (CWB rank 1, STRNG 74 — HIGHEST in the data) has displaced Nasdaq from the #1 asset class position — the credit-risk-appetite trade is leading. Small-Cap (IWM rank 2, STRNG 74, RLTV 1.02) holds rank 2 with STRNG matching CWB — small-cap leadership is now embedded. Nasdaq (QQQ rank 3) dropped from rank 1 — the tech-leadership trade is cooling as rotation broadens. SPY at rank 5 with MNTM +2 (down sharply from last week’s +40) — the entire data set has RE-BASELINED after Friday’s oil crash and Monday’s weekend-risk digestion. CRITICAL ENERGY REVERSAL: Crude Oil (USO rank 34, MNTM +69, RLTV 1.65!!!) has undergone the MOST DRAMATIC single-data-set momentum reversal of the entire war. From MNTM −22 / RLTV 0.89 to MNTM +69 / RLTV 1.65. The Friday oil crash (−14%) followed by Monday’s +4% bounce produced a massive momentum spike. Gasoline (UGA rank 26, MNTM +56, RLTV 1.52) mirrors the pattern. VIX futures (VXX MNTM +11, RLTV 1.08) — fear momentum is positive for the first time in the data. Bitcoin (IBIT rank 18, MNTM −20, RLTV 0.78) — crypto CRATERED from +27/1.01 to −20/0.78 — the largest single-data-set crypto deterioration of the war. Ethereum (ETHA rank 24, MNTM −29, RLTV 0.69) even worse. The weekend risk-off hit crypto hardest of any asset class.

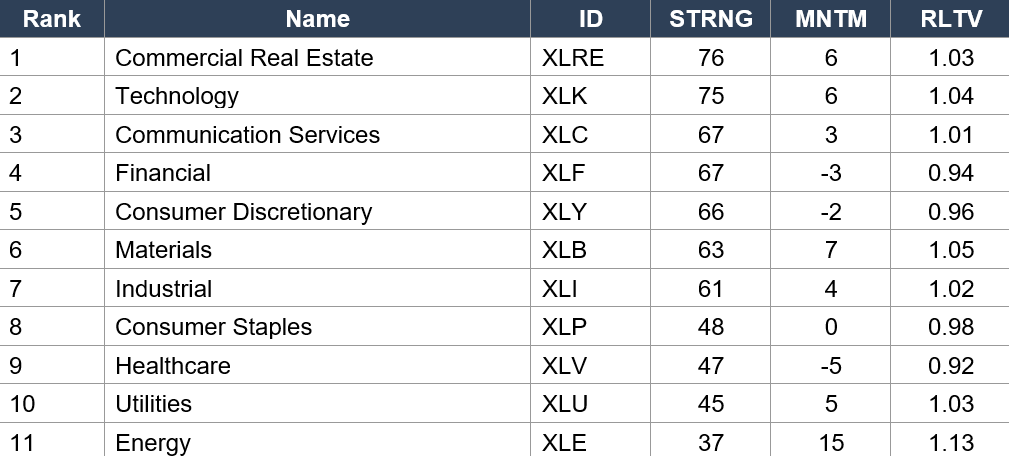

Sector ETFs — Full Ranking

Regime signal: XLRE (rank 1, STRNG 76 — HIGHEST sector STRNG of the entire war, MNTM +6) holds #1 for the SEVENTH consecutive data set — the most dominant sector-leadership streak of the conflict. XLK (rank 2, STRNG 75, RLTV 1.04) holds strong but MNTM cooled from 42 to 6. CRITICAL: Financial (XLF rank 4, MNTM −3, RLTV 0.94) turned NEGATIVE momentum and RLTV fell below 1.00 for the first time — the bank-beat trade from last week has fully unwound in the data. Consumer Discretionary (XLY rank 5, MNTM −2, RLTV 0.96) also negative — TSLA/AMZN weakness captured. Health-Care (XLV rank 9, MNTM −5, RLTV 0.92 — LOWEST RLTV of any sector) is the structural laggard despite today’s UNH beat. ENERGY (XLE rank 11, STRNG 37 — LOWEST STRNG by far, BUT MNTM +15 and RLTV 1.13!!! — HIGHEST RLTV of any sector). The energy sector is in the paradoxical position of having the weakest absolute strength but the STRONGEST relative momentum and relative performance. The oil crash + bounce created massive positive momentum in a structurally weak sector. This is the ‘Phoenix trade’ — the worst-performing sector of the war is suddenly outperforming the market on a relative basis.

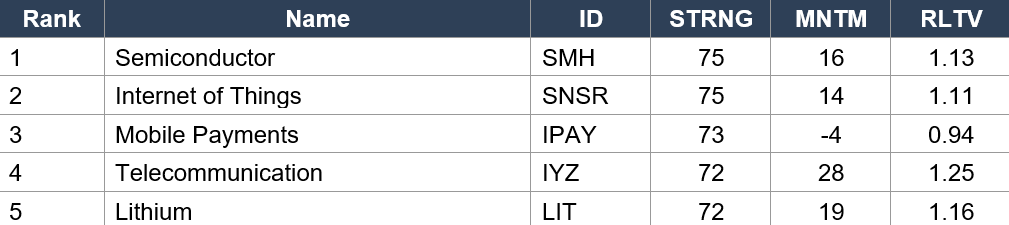

Industry ETFs — Top 5

Industry ETFs — Notable Shifts

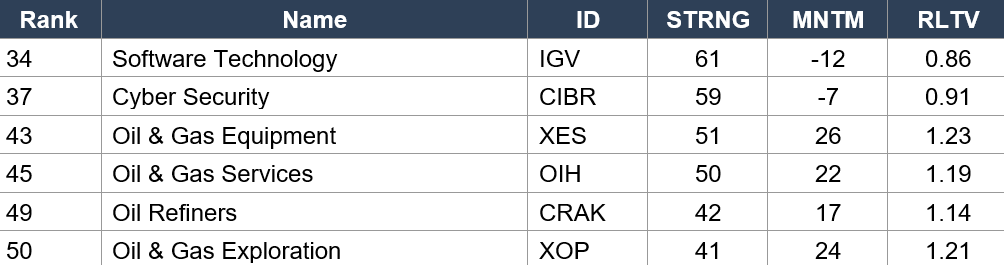

Regime signal: Semiconductor (SMH rank 1, STRNG 75, MNTM 16, RLTV 1.13) holds #1 industry for the THIRD consecutive data set — semis leadership is structural. Telecommunication (IYZ rank 4, MNTM 28, RLTV 1.25 — HIGHEST RLTV of any industry ETF) surged into the top 5 — defensive-growth rotation. CRITICAL SOFTWARE CRASH: Software Technology (IGV rank 34, MNTM −12, RLTV 0.86) COLLAPSED from rank 33/MNTM +25/RLTV 1.09 in the prior data set. The software recovery that was ‘fully structural’ as of Friday has BROKEN in a single session. The Monday risk-off rotation hit software hardest of any non-crypto industry. MSFT at −1.12% pre-market today confirms the pattern. Cyber Security (CIBR rank 37, MNTM −7, RLTV 0.91) also reversed. ENERGY INDUSTRY EXPLOSION: Every energy sub-industry has MASSIVE positive MNTM and RLTV above 1.00: Oil & Gas Equipment (XES MNTM +26, RLTV 1.23), Oil & Gas Exploration (XOP MNTM +24, RLTV 1.21), Oil & Gas Services (OIH MNTM +22, RLTV 1.19), Oil Refiners (CRAK MNTM +17, RLTV 1.14), Shipping-Global (BOAT MNTM +23, RLTV 1.20). The energy complex has undergone the most dramatic single-data-set rotation of the entire war — from structural laggard to relative outperformer in one session. The Friday oil crash + weekend re-escalation + Monday bounce created a momentum shock that flipped the entire energy data landscape.

4. MORNING DATA REACTION

8:30 AM — RETAIL SALES MARCH: +1.7% HEADLINE VS +1.4% CONSENSUS. CORE +1.9% VS +1.4% CONSENSUS. THE CONSUMER IS SPENDING THROUGH THE WAR’S ENERGY SHOCK.

The March retail sales print is the definitive consumer-health datapoint of the war. Headline +1.7% vs +1.4% consensus, prior revised to +0.6%. Core (ex-auto) +1.9% vs +1.4% consensus, prior +0.5%. The +0.5 pp core beat is the largest of 2026. March was the month of peak war-energy-price stress (CPI gasoline +21.2%, Michigan sentiment 47.6 all-time low), and STILL the consumer beat consensus on the core measure by the widest margin of the year. This says: the consumer has enough income/credit/savings momentum to absorb $4+ gasoline and accelerate spending simultaneously. For the Fed, this is the ‘Goldilocks’ datapoint: strong enough to validate growth but not so strong it forces hawkish action (because the front-end is already pricing ‘no cuts near-term’ via the flattener twist). For equities, it is unambiguously bullish — consumer-facing sectors (XLY, XLP, XLF) should benefit from the demand confirmation. The 2Y +3.1 bps response (front-end hawkish repricing) is the market trimming the remaining rate-cut probability as strong consumer data removes urgency for Fed easing.

PRE-MARKET — UNITEDHEALTH Q1 2026 BEAT: Adjusted EPS $7.23 (+9.4% vs $6.61 est). Revenue $111.72B (+1.7% beat). MCR 83.9% (better than expected). RAISED FY26 Guidance To >$18.25 From >$17.75. Stock Soaring. The Recovery Story Is Validated.

After a year of damage control — the cyberattack, CEO Andrew Witty’s departure, the Q1 2025 22% selloff, the Q4 $2.88B charge — UNH delivered a clean beat on every metric that matters. The MCR at 83.9% is the key: it tells you UNH is managing the medical-cost trend that terrified investors in 2025. The guidance raise to >$18.25 from >$17.75 (a +2.8% increase) during a war with active Hormuz re-closure and ceasefire expiration tonight is a statement of operational confidence from CEO Hemsley. The $2B buyback plan by end of Q2 adds capital-return support. UNH entered Tuesday down 45.5% over the past year — the rally from this print could be one of the largest single-stock moves of earnings season given the extreme negative positioning.

5. THE DYRH READ

Regime: Flattener Twist — Neutral / Consolidating — Energy Steady. The strongest morning data combination of the week (UNH +9.4% beat + Retail Sales core +1.9% vs +1.4%) arrives on the same day as the ceasefire expiration, Warsh hearing, and the eve of TSLA/GOOGL/MSFT/META earnings. MOVE at 67.90 (+3.36%) is bouncing from the 65.70 floor but remains sub-baseline (73.21). The bond market has not flinched back above baseline despite the weekend kinetic escalation and oil bounce. COR1M continuing to rise (+15.04% to 12.47) — correlations rebuilding as the macro calendar intensifies. Confidence: MODERATE-HIGH — strong data layer but binary geopolitical event risk tonight.

Yield Curve: FLATTENER TWIST — Front Rising Sharply (+3.1 bps on 2Y), Long Falling (−0.6 bps on 30Y). The Retail Sales Beat Is Repricing The Front End.

2Y +3.1 bps to 3.758% — the front end is rising on the strong Retail Sales / UNH combination; market is trimming near-term rate-cut probability. 5Y +2.3 bps to 3.882%. 10Y +1.0 bps to 4.268%. 30Y −0.6 bps to 4.881% — the LONG END IS FALLING despite the hot consumer data. The flattener twist says: ‘Near-term Fed stays on hold or even turns hawkish (activity too strong to cut), but long-run growth expectations remain pessimistic (war/Hormuz uncertainty depresses term premium).’ This is a more hawkish interpretation of the data than the bull steepener from Friday — the Retail Sales beat REMOVED residual rate-cut probability rather than confirming it. Warsh’s hearing at 10 AM adds a governance layer: if Warsh signals a hawkish institutional direction, the front end could rise further.

MOVE 67.90 (+3.36%) — Bouncing From Floor But Still Sub-Baseline. The Bond Market Has Not Reversed Despite Weekend Kinetic Escalation.

MOVE at 67.9035 rose +3.36% from Friday’s 65.70 — the first EXPANSION in four sessions. But critically, MOVE remains at 67.90, which is still 5.31 points BELOW the 73.21 pre-war baseline. The bounce is positioning-driven (weekend risk, ceasefire expiration binary, Warsh hearing) rather than fundamental-driven. If MOVE stays below 73.21 through the ceasefire expiration, the bond market’s capitulation thesis from Thursday/Friday is intact. If MOVE breaks back above 73.21, the capitulation reversed and the war’s rates-vol overhang returns.

ES 7,165.50 (+0.24%) — Constructive. +4.1% Above Pre-War Baseline. The Broadening Continues.

ES at 7,165.50 extends Monday’s close. The Dow at +0.48% leading ES at +0.24% for the second consecutive session confirms the value/cyclical rotation is sustained, not one-day. RSP (equal weight) at +0.32% outperforming ES (cap weight) at +0.24% for the second consecutive session — breadth broadening is structural. The Mag 7 at 2 green / 5 red while the index is green says the non-Mag 7 market is carrying the index for the first time in the rally — the healthiest possible market structure.

COR1M 12.47 (+15.04%) — Correlations Continuing To Rise. The Macro Calendar Is Pulling Names Back Into Correlated Movement.

COR1M has risen three consecutive sessions: 10.94 (Friday war low) → 12.23 (Monday) → 12.47 (Tuesday). The macro event calendar (ceasefire expiration, Warsh hearing, TSLA/GOOGL/MSFT/META earnings) is re-introducing systematic risk that pulls names into correlated movement. The idiosyncratic stock-picking regime from last week is transitioning to a macro-driven regime. This is consistent with the VIX hold at 18.86 and MOVE bounce to 67.90 — vol metrics stabilizing rather than compressing further.

6. THE GAME PLAN

Today’s Key Events: UNH Q1 pre-market BEAT ($7.23 vs $6.61, raised guidance — already released). Retail Sales BEAT (1.7%/1.9% vs 1.4%/1.4% — already released). Trump speaks 8:30 AM. Warsh Fed Chair-Designate hearing 10 AM. Pending Home Sales 10 AM. LMT, COF pre-market. TONIGHT: CEASEFIRE EXPIRES. Vance in Islamabad. Iran participation UNCONFIRMED. WEDNESDAY: TSLA Q1 after close. Boeing, ServiceNow. THURSDAY: GOOGL / MSFT / META / CAT after close. FRIDAY: PG, Colgate-Palmolive.

The Bull Case:

UNH beat + raised guidance validates healthcare recovery. Retail Sales core +1.9% vs +1.4% = consumer absorbing energy shock without demand destruction. SIX consecutive data beats (PPI/Empire/Philly/Claims/Retail/UNH). ES +4.1% above pre-war, Dow leading, RSP outperforming — broadening. MOVE at 67.90 still sub-baseline despite weekend kinetic escalation. Factor tape risk-on (SPHB leading, USMV-SPHB −0.78%). Small-cap and mid-cap outperforming. 34 Macro rankings show CWB #1 asset class (credit risk-appetite leading). XLRE holds #1 sector for seventh consecutive data set. SMH holds #1 industry for third consecutive. Energy RLTV surged to 1.13 (Phoenix trade alive). If Vance secures extension tonight, Wednesday opens with de-escalation + data beats + earnings week confirmation = the most constructive package since Day 29.

The Bear Case:

CEASEFIRE EXPIRES TONIGHT. Iran has NOT confirmed Islamabad participation. Weekend saw first shots fired + ship seized. If talks fail, war re-escalates with kinetic precedent. MOVE bouncing +3.36% — the capitulation may be reversing. VIX at 18.86 with VXX MNTM +11 / RLTV 1.08 — fear momentum positive in the data for the first time. Mag 7 at 2 green / 5 red with META −2.56% and TSLA −2.03% — positioning into earnings is cautious. Software CRASHED in the 34 Macro data (IGV RLTV 0.86 from 1.09 — the recovery broke). Crypto CRATERED (IBIT RLTV 0.78, ETHA 0.69). XLF turned negative momentum/RLTV in the data (bank-beat trade unwound). Flattener twist is the most complex curve regime to trade — front-end hawkish repricing on strong data removes Fed-cut optionality. Warsh hearing could introduce governance uncertainty if contentious. TSLA Wednesday reports into the ceasefire overnight risk. GOOGL/MSFT/META Thursday is the largest Mag 7 concentration of the war — any disappointment breaks the broadening narrative.

Regime: Flattener Twist — Neutral / Consolidating — Energy Steady. The morning data layer (UNH + Retail Sales) is the strongest of the week but the evening binary (ceasefire expiration) is the most risk-laden of the war. The 34 Macro rankings show a structural rotation: energy surging on relative basis, software collapsing, crypto cratering, credit leading, breadth broadening via small-cap and value. The Mag 7 is no longer the market’s driver — the non-Mag 7 complex is carrying the index. MOVE is bouncing but sub-baseline. Tonight determines everything. Warsh at 10 AM is the governance catalyst. TSLA Wednesday. GOOGL/MSFT/META Thursday. Position for the binary: the market is giving you strong fundamentals as a floor and ceasefire expiration as the ceiling. The resolution of tonight’s talks sets the regime for the rest of the week.

Watch List

TONIGHT — Ceasefire Expires. Vance In Islamabad. THE DEFINING BINARY.

The two-week ceasefire framework expires tonight. VP Vance is leading a US delegation in Islamabad. Iran has NOT confirmed participation. If Vance secures even a temporary extension: Wednesday opens with de-escalation re-rating, WTI targets $80-82, MOVE compresses further, equities extend. If talks collapse: WTI gaps above $90, MOVE could snap back above 73.21 baseline, equities face overnight gap risk into TSLA earnings. The Friday close-to-Monday gap from last weekend’s kinetic escalation was +4% WTI — tonight’s gap could be larger given the formal expiration context.

Warsh Confirmation Hearing 10 AM — Fed Governance Defines The Next Four Years

Warsh has called for ‘regime change’ at the Fed and described ‘breaking heads’ as his approach. Powell’s term expires May 15. Tillis blocking. The hearing’s tone determines whether markets view the Fed transition as smooth (governance premium removed) or contentious (governance uncertainty sustained into May). A dovish-leaning Warsh would compound the bull case. A hawkish Warsh leaning into the strong Retail Sales data would add to the front-end repricing.

TSLA Wednesday After Close — Reports Into Ceasefire Overnight Risk

Tesla Q1 after Wednesday’s close. TSLA at $392.50 (−2.03% today) is positioning cautiously. Q1 deliveries missed expectations. The stock rallied +7.62% last Thursday on AI5/AI6 + UBS upgrade, then gave back to current levels. Wednesday evening is both TSLA earnings AND the first full session after ceasefire expiration — the overnight risk profile is elevated.

GOOGL / MSFT / META Thursday After Close — The Mega Earnings Day

Three of the seven largest companies report on the same day. MSFT has rallied ~+9% over the past week on software reflation but IGV RLTV crashed to 0.86 in the data. META at −2.56% today is the weakest Mag 7 over 3 sessions. GOOG is the swing name. This is the largest single-day concentration of Mag 7 earnings of the war. The results determine whether the post-ceasefire rally becomes permanent or was a positioning trade ahead of binary catalysts.

Morning check: Day 54. UNH delivered a 9.4% EPS beat and raised guidance — the recovery story is validated. Retail Sales core +1.9% vs +1.4% — the consumer is spending through the war’s energy shock. Six consecutive data beats. The market is green despite 5/7 Mag 7 red because breadth is carrying: Dow leading, RSP outperforming, mid-cap and small-cap outperforming. The 34 Macro rankings show a structural rotation: energy surging to RLTV 1.13-1.65, software crashing to 0.86, crypto cratering to 0.69-0.78, credit leading, VIX momentum positive. The entire data landscape has re-baselined from last week’s narrow Mag 7 tech leadership to this week’s broad value/cyclical/small-cap rotation. MOVE is bouncing but sub-baseline. And tonight — the ceasefire expires. Vance is in Islamabad. Iran is uncommitted. The morning gave us the strongest fundamentals floor of the war. Tonight gives us the biggest binary risk. The setup is clear: take the data layer, respect the overnight risk, and let the ceasefire resolution set the regime for the rest of the week. TSLA Wednesday. GOOGL/MSFT/META Thursday. There is nowhere to hide and everywhere to position. This is the week that defines the war’s market legacy.

The bell rings at 9:30. You’re ready.

— 34 Macro

Pressure, not panic. Regime, not reaction.

Cross-asset macro research and education — built for the everyday person.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but 34 Macro does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of 34 Macro websites and systems including but not limited to data scraping, unauthorized entry into 34 Macro systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by 34 Macro and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to 34 Macro or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of 34 Macro.